Chubu Electric Power Porter's Five Forces Analysis

From Overview to Strategy Blueprint

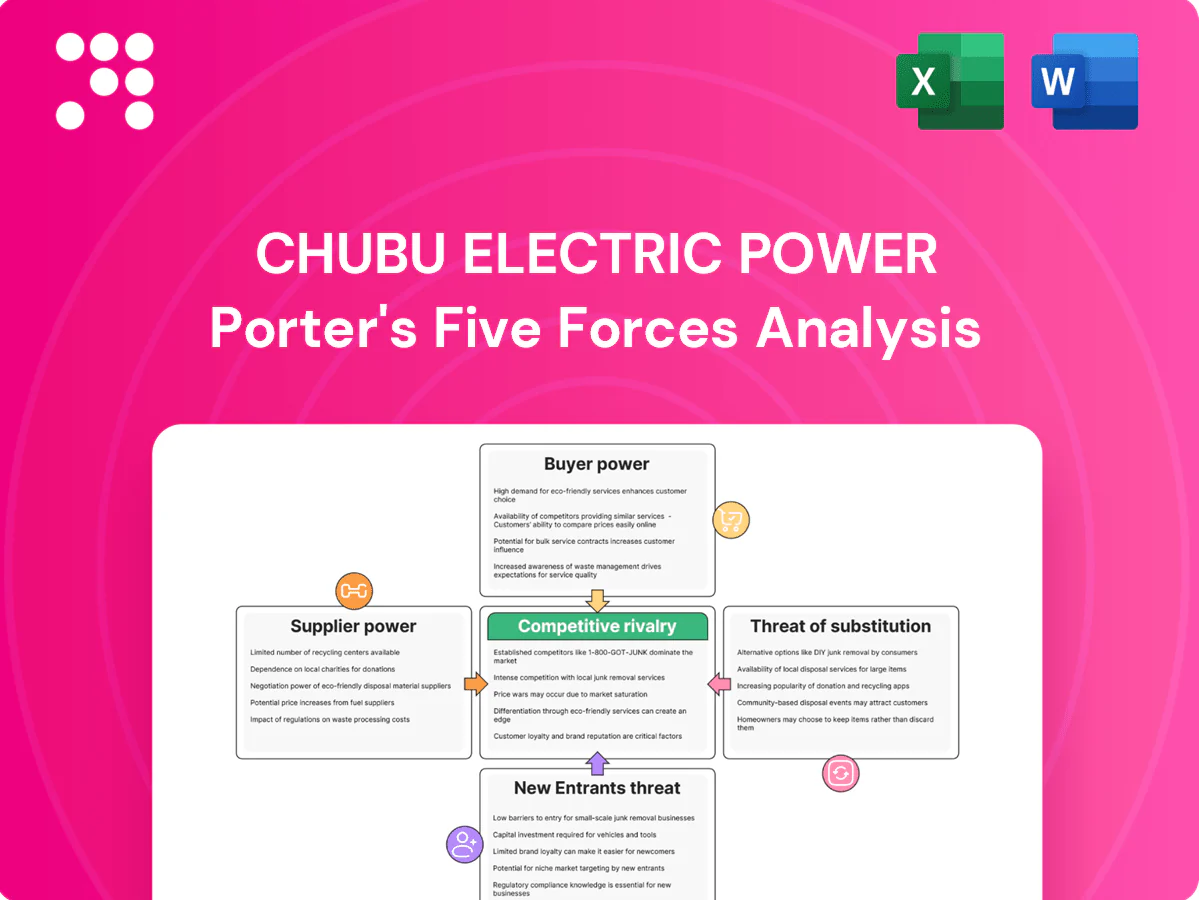

Chubu Electric Power faces moderate supplier leverage due to fuel imports, high buyer sensitivity from regulated tariffs, and low threat of new entrants given capital intensity; substitute risks rise with renewables and distributed generation. Competitive rivalry is steady among incumbents, while regulatory shifts shape industry dynamics. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings and strategic implications.

Suppliers Bargaining Power

Fuel suppliers concentration

Chubu relies heavily on imported LNG, coal and oil from concentrated global suppliers, exposing it to supply shocks and price spikes that pressure margins. Price volatility and geopolitical risks in 2024 continued to lift fuel costs and input-cost risk for Japanese utilities. Extensive long-term contracts and hedging smooth short-term swings but constrain procurement flexibility. Partial offset comes from domestic gas procurement via JERA, co-owned by Chubu and TEPCO, with JERA remaining Japan’s largest LNG buyer in 2024.

JERA vertical integration buffer

JERA, a 50/50 JV between TEPCO Fuel & Power and Chubu Electric, centralizes LNG procurement and thermal operations. Its scale and portfolio optionality improve bargaining terms and reduce exposure to single-cargo disruptions. However, alignment with market indices in 2024 still transmits global LNG price movements to buyers.

Equipment OEM and EPC lock-in

Gas turbines, boilers and grid equipment are dominated by Siemens Energy, GE, Mitsubishi Power and IHI, collectively supplying roughly 70–80% of large thermal and grid orders, creating technical lock-in and 18–30 month lead times that boost vendors' pricing and maintenance leverage. Standardization and multi-vendor procurement reduce dependence, while Japan's domestic suppliers and 10–20 year lifecycle O&M contracts balance reliability and total cost of ownership.

Renewables component supply

Solar modules, inverters and wind nacelles remain tied to international chains, with China supplying ~80% of PV modules in 2024 and top inverter vendors holding >60% market share; currency swings and tightening trade policies have driven delivered costs up to 8–12% in recent quarters, while increased localization and diversified sourcing cut lead-time risk by ~30%.

- Concentration: China ~80% PV

- Inverter share: >60%

- Cost impact: FX/trade +8–12%

- Localization cuts lead time ~30%

- Spare parts/service: critical to uptime

Fuel transport and infrastructure

Concentrated LNG, coal, oil markets and vendor lock-in drive strong supplier leverage in Chubu

Chubu faces strong supplier leverage from concentrated LNG/coal/oil markets and global price volatility, partially mitigated by JERA (Japan’s largest LNG buyer) and long-term contracts. Critical equipment vendors (Siemens/GE/Mitsubishi/IHI) create technical lock-in and 18–30 month lead times. Terminals/regas capacity (36 terminals, ~107 mtpa in 2024) and shipping volatility further strengthen supplier bargaining power.

| Metric | 2024 |

|---|---|

| Japan LNG terminals | ~36 |

| Regas capacity | ~107 mtpa |

| PV modules from China | ~80% |

| Thermal/grid vendor share | 70–80% |

| Lead times (equipment) | 18–30 months |

What is included in the product

Tailored Porter's Five Forces analysis for Chubu Electric Power, uncovering key drivers of competition, buyer and supplier power, entry barriers, and threat of substitutes. Identifies disruptive forces and regulatory dynamics that shape pricing, profitability, and strategic positioning for investors and executives.

A clear, one-sheet summary of all five forces for Chubu Electric Power—perfect for quick regulatory, supply-chain and market-risk decisions.

Customers Bargaining Power

Liberalized retail market

Since retail liberalization in 2016, Japan hosts over 600 retail electricity providers (METI, 2024), enabling easy switching and transparent tariff comparison for residential and SME customers. About 20–30% switching prevalence in recent years raises churn risk and price sensitivity, especially for tariff and green-energy choices. Loyalty programs and bundled services are increasingly used to stem defections and bolster retention.

Industrial load concentration

Large manufacturers in Chubu region (including major auto and steel plants) create concentrated demand blocks that give them strong negotiating leverage with Chubu Electric, which serves over 7 million customers as of 2024. They secure bespoke tariffs, demand-response terms and strict reliability SLAs while on-site generation and third-party PPAs (increasingly adopted in 2023–24) boost bargaining power. Long-term contracts lock volumes but typically compress utility margins as prices and risk allocation shift to customers.

Green procurement demands

Corporate buyers increasingly demand renewables and emissions cuts, with RE100 surpassing 400 members in 2024, shifting demand toward guaranteed green supply. Preference for RE100-style contracts alters pricing and product mix, boosting negotiation leverage as certificated renewables and EACs become more available. Chubu can recapture value by offering flexible, verifiable green products and bespoke PPA-like solutions.

Wholesale market alternatives

JEPX access lets retailers and large users source spot power, and with over 600 retail entrants by 2024 customers can push Chubu Electric for pass-through savings during low-price periods; high spot volatility, however, can quickly restore supplier leverage. Hedging and indexed contracts are widely used to balance risks between buyers and Chubu.

- JEPX access: market alternative

- 600+ retailers (2024)

- Low-price pressure → pass-through demand

- Volatility shifts leverage to supplier

- Hedging/indexed contracts mitigate risk

Service quality expectations

Service quality expectations hinge on reliability, outage response, and digital billing, which directly shape perceived value and long-term retention for Chubu Electric; poor performance increases customer switching propensity despite regulatory reliability baselines.

Advanced analytics, time-of-use plans, and advisory services lower buyer power by creating differentiated offerings and stickier revenue streams, complementing mandatory regulatory standards that only set minimums.

- Reliability drives perceived value

- Outage response affects churn

- Digital billing and TOU reduce switching

- Regulatory baselines vs differentiation

Retailer surge and 20–30% churn reshape power market as corporates drive renewables

Since 2016 liberalization, 600+ retailers (METI, 2024) and JEPX access give residential/SME buyers high switching power (20–30% churn) while 7M customer base and large manufacturers hold concentrated bargaining leverage. Corporate demand for renewables (RE100 400+ members, 2024) raises green-contract negotiation strength; tailored products and TOU reduce buyer power.

| Metric | Value (2024) |

|---|---|

| Retailers | 600+ |

| Chubu customers | 7M |

| Switching rate | 20–30% |

| RE100 members | 400+ |

What You See Is What You Get

Chubu Electric Power Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Chubu Electric Power you’ll receive—no mockups or placeholders. The document is fully formatted, professionally written, and ready for immediate download upon purchase. What you see is the complete deliverable, suitable for strategic decision-making and valuation work.

From Overview to Strategy Blueprint

Chubu Electric Power faces moderate supplier leverage due to fuel imports, high buyer sensitivity from regulated tariffs, and low threat of new entrants given capital intensity; substitute risks rise with renewables and distributed generation. Competitive rivalry is steady among incumbents, while regulatory shifts shape industry dynamics. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings and strategic implications.

Suppliers Bargaining Power

Fuel suppliers concentration

Chubu relies heavily on imported LNG, coal and oil from concentrated global suppliers, exposing it to supply shocks and price spikes that pressure margins. Price volatility and geopolitical risks in 2024 continued to lift fuel costs and input-cost risk for Japanese utilities. Extensive long-term contracts and hedging smooth short-term swings but constrain procurement flexibility. Partial offset comes from domestic gas procurement via JERA, co-owned by Chubu and TEPCO, with JERA remaining Japan’s largest LNG buyer in 2024.

JERA vertical integration buffer

JERA, a 50/50 JV between TEPCO Fuel & Power and Chubu Electric, centralizes LNG procurement and thermal operations. Its scale and portfolio optionality improve bargaining terms and reduce exposure to single-cargo disruptions. However, alignment with market indices in 2024 still transmits global LNG price movements to buyers.

Equipment OEM and EPC lock-in

Gas turbines, boilers and grid equipment are dominated by Siemens Energy, GE, Mitsubishi Power and IHI, collectively supplying roughly 70–80% of large thermal and grid orders, creating technical lock-in and 18–30 month lead times that boost vendors' pricing and maintenance leverage. Standardization and multi-vendor procurement reduce dependence, while Japan's domestic suppliers and 10–20 year lifecycle O&M contracts balance reliability and total cost of ownership.

Renewables component supply

Solar modules, inverters and wind nacelles remain tied to international chains, with China supplying ~80% of PV modules in 2024 and top inverter vendors holding >60% market share; currency swings and tightening trade policies have driven delivered costs up to 8–12% in recent quarters, while increased localization and diversified sourcing cut lead-time risk by ~30%.

- Concentration: China ~80% PV

- Inverter share: >60%

- Cost impact: FX/trade +8–12%

- Localization cuts lead time ~30%

- Spare parts/service: critical to uptime

Fuel transport and infrastructure

Concentrated LNG, coal, oil markets and vendor lock-in drive strong supplier leverage in Chubu

Chubu faces strong supplier leverage from concentrated LNG/coal/oil markets and global price volatility, partially mitigated by JERA (Japan’s largest LNG buyer) and long-term contracts. Critical equipment vendors (Siemens/GE/Mitsubishi/IHI) create technical lock-in and 18–30 month lead times. Terminals/regas capacity (36 terminals, ~107 mtpa in 2024) and shipping volatility further strengthen supplier bargaining power.

| Metric | 2024 |

|---|---|

| Japan LNG terminals | ~36 |

| Regas capacity | ~107 mtpa |

| PV modules from China | ~80% |

| Thermal/grid vendor share | 70–80% |

| Lead times (equipment) | 18–30 months |

What is included in the product

Tailored Porter's Five Forces analysis for Chubu Electric Power, uncovering key drivers of competition, buyer and supplier power, entry barriers, and threat of substitutes. Identifies disruptive forces and regulatory dynamics that shape pricing, profitability, and strategic positioning for investors and executives.

A clear, one-sheet summary of all five forces for Chubu Electric Power—perfect for quick regulatory, supply-chain and market-risk decisions.

Customers Bargaining Power

Liberalized retail market

Since retail liberalization in 2016, Japan hosts over 600 retail electricity providers (METI, 2024), enabling easy switching and transparent tariff comparison for residential and SME customers. About 20–30% switching prevalence in recent years raises churn risk and price sensitivity, especially for tariff and green-energy choices. Loyalty programs and bundled services are increasingly used to stem defections and bolster retention.

Industrial load concentration

Large manufacturers in Chubu region (including major auto and steel plants) create concentrated demand blocks that give them strong negotiating leverage with Chubu Electric, which serves over 7 million customers as of 2024. They secure bespoke tariffs, demand-response terms and strict reliability SLAs while on-site generation and third-party PPAs (increasingly adopted in 2023–24) boost bargaining power. Long-term contracts lock volumes but typically compress utility margins as prices and risk allocation shift to customers.

Green procurement demands

Corporate buyers increasingly demand renewables and emissions cuts, with RE100 surpassing 400 members in 2024, shifting demand toward guaranteed green supply. Preference for RE100-style contracts alters pricing and product mix, boosting negotiation leverage as certificated renewables and EACs become more available. Chubu can recapture value by offering flexible, verifiable green products and bespoke PPA-like solutions.

Wholesale market alternatives

JEPX access lets retailers and large users source spot power, and with over 600 retail entrants by 2024 customers can push Chubu Electric for pass-through savings during low-price periods; high spot volatility, however, can quickly restore supplier leverage. Hedging and indexed contracts are widely used to balance risks between buyers and Chubu.

- JEPX access: market alternative

- 600+ retailers (2024)

- Low-price pressure → pass-through demand

- Volatility shifts leverage to supplier

- Hedging/indexed contracts mitigate risk

Service quality expectations

Service quality expectations hinge on reliability, outage response, and digital billing, which directly shape perceived value and long-term retention for Chubu Electric; poor performance increases customer switching propensity despite regulatory reliability baselines.

Advanced analytics, time-of-use plans, and advisory services lower buyer power by creating differentiated offerings and stickier revenue streams, complementing mandatory regulatory standards that only set minimums.

- Reliability drives perceived value

- Outage response affects churn

- Digital billing and TOU reduce switching

- Regulatory baselines vs differentiation

Retailer surge and 20–30% churn reshape power market as corporates drive renewables

Since 2016 liberalization, 600+ retailers (METI, 2024) and JEPX access give residential/SME buyers high switching power (20–30% churn) while 7M customer base and large manufacturers hold concentrated bargaining leverage. Corporate demand for renewables (RE100 400+ members, 2024) raises green-contract negotiation strength; tailored products and TOU reduce buyer power.

| Metric | Value (2024) |

|---|---|

| Retailers | 600+ |

| Chubu customers | 7M |

| Switching rate | 20–30% |

| RE100 members | 400+ |

What You See Is What You Get

Chubu Electric Power Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Chubu Electric Power you’ll receive—no mockups or placeholders. The document is fully formatted, professionally written, and ready for immediate download upon purchase. What you see is the complete deliverable, suitable for strategic decision-making and valuation work.

Description

From Overview to Strategy Blueprint

Chubu Electric Power faces moderate supplier leverage due to fuel imports, high buyer sensitivity from regulated tariffs, and low threat of new entrants given capital intensity; substitute risks rise with renewables and distributed generation. Competitive rivalry is steady among incumbents, while regulatory shifts shape industry dynamics. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings and strategic implications.

Suppliers Bargaining Power

Fuel suppliers concentration

Chubu relies heavily on imported LNG, coal and oil from concentrated global suppliers, exposing it to supply shocks and price spikes that pressure margins. Price volatility and geopolitical risks in 2024 continued to lift fuel costs and input-cost risk for Japanese utilities. Extensive long-term contracts and hedging smooth short-term swings but constrain procurement flexibility. Partial offset comes from domestic gas procurement via JERA, co-owned by Chubu and TEPCO, with JERA remaining Japan’s largest LNG buyer in 2024.

JERA vertical integration buffer

JERA, a 50/50 JV between TEPCO Fuel & Power and Chubu Electric, centralizes LNG procurement and thermal operations. Its scale and portfolio optionality improve bargaining terms and reduce exposure to single-cargo disruptions. However, alignment with market indices in 2024 still transmits global LNG price movements to buyers.

Equipment OEM and EPC lock-in

Gas turbines, boilers and grid equipment are dominated by Siemens Energy, GE, Mitsubishi Power and IHI, collectively supplying roughly 70–80% of large thermal and grid orders, creating technical lock-in and 18–30 month lead times that boost vendors' pricing and maintenance leverage. Standardization and multi-vendor procurement reduce dependence, while Japan's domestic suppliers and 10–20 year lifecycle O&M contracts balance reliability and total cost of ownership.

Renewables component supply

Solar modules, inverters and wind nacelles remain tied to international chains, with China supplying ~80% of PV modules in 2024 and top inverter vendors holding >60% market share; currency swings and tightening trade policies have driven delivered costs up to 8–12% in recent quarters, while increased localization and diversified sourcing cut lead-time risk by ~30%.

- Concentration: China ~80% PV

- Inverter share: >60%

- Cost impact: FX/trade +8–12%

- Localization cuts lead time ~30%

- Spare parts/service: critical to uptime

Fuel transport and infrastructure

Concentrated LNG, coal, oil markets and vendor lock-in drive strong supplier leverage in Chubu

Chubu faces strong supplier leverage from concentrated LNG/coal/oil markets and global price volatility, partially mitigated by JERA (Japan’s largest LNG buyer) and long-term contracts. Critical equipment vendors (Siemens/GE/Mitsubishi/IHI) create technical lock-in and 18–30 month lead times. Terminals/regas capacity (36 terminals, ~107 mtpa in 2024) and shipping volatility further strengthen supplier bargaining power.

| Metric | 2024 |

|---|---|

| Japan LNG terminals | ~36 |

| Regas capacity | ~107 mtpa |

| PV modules from China | ~80% |

| Thermal/grid vendor share | 70–80% |

| Lead times (equipment) | 18–30 months |

What is included in the product

Tailored Porter's Five Forces analysis for Chubu Electric Power, uncovering key drivers of competition, buyer and supplier power, entry barriers, and threat of substitutes. Identifies disruptive forces and regulatory dynamics that shape pricing, profitability, and strategic positioning for investors and executives.

A clear, one-sheet summary of all five forces for Chubu Electric Power—perfect for quick regulatory, supply-chain and market-risk decisions.

Customers Bargaining Power

Liberalized retail market

Since retail liberalization in 2016, Japan hosts over 600 retail electricity providers (METI, 2024), enabling easy switching and transparent tariff comparison for residential and SME customers. About 20–30% switching prevalence in recent years raises churn risk and price sensitivity, especially for tariff and green-energy choices. Loyalty programs and bundled services are increasingly used to stem defections and bolster retention.

Industrial load concentration

Large manufacturers in Chubu region (including major auto and steel plants) create concentrated demand blocks that give them strong negotiating leverage with Chubu Electric, which serves over 7 million customers as of 2024. They secure bespoke tariffs, demand-response terms and strict reliability SLAs while on-site generation and third-party PPAs (increasingly adopted in 2023–24) boost bargaining power. Long-term contracts lock volumes but typically compress utility margins as prices and risk allocation shift to customers.

Green procurement demands

Corporate buyers increasingly demand renewables and emissions cuts, with RE100 surpassing 400 members in 2024, shifting demand toward guaranteed green supply. Preference for RE100-style contracts alters pricing and product mix, boosting negotiation leverage as certificated renewables and EACs become more available. Chubu can recapture value by offering flexible, verifiable green products and bespoke PPA-like solutions.

Wholesale market alternatives

JEPX access lets retailers and large users source spot power, and with over 600 retail entrants by 2024 customers can push Chubu Electric for pass-through savings during low-price periods; high spot volatility, however, can quickly restore supplier leverage. Hedging and indexed contracts are widely used to balance risks between buyers and Chubu.

- JEPX access: market alternative

- 600+ retailers (2024)

- Low-price pressure → pass-through demand

- Volatility shifts leverage to supplier

- Hedging/indexed contracts mitigate risk

Service quality expectations

Service quality expectations hinge on reliability, outage response, and digital billing, which directly shape perceived value and long-term retention for Chubu Electric; poor performance increases customer switching propensity despite regulatory reliability baselines.

Advanced analytics, time-of-use plans, and advisory services lower buyer power by creating differentiated offerings and stickier revenue streams, complementing mandatory regulatory standards that only set minimums.

- Reliability drives perceived value

- Outage response affects churn

- Digital billing and TOU reduce switching

- Regulatory baselines vs differentiation

Retailer surge and 20–30% churn reshape power market as corporates drive renewables

Since 2016 liberalization, 600+ retailers (METI, 2024) and JEPX access give residential/SME buyers high switching power (20–30% churn) while 7M customer base and large manufacturers hold concentrated bargaining leverage. Corporate demand for renewables (RE100 400+ members, 2024) raises green-contract negotiation strength; tailored products and TOU reduce buyer power.

| Metric | Value (2024) |

|---|---|

| Retailers | 600+ |

| Chubu customers | 7M |

| Switching rate | 20–30% |

| RE100 members | 400+ |

What You See Is What You Get

Chubu Electric Power Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Chubu Electric Power you’ll receive—no mockups or placeholders. The document is fully formatted, professionally written, and ready for immediate download upon purchase. What you see is the complete deliverable, suitable for strategic decision-making and valuation work.