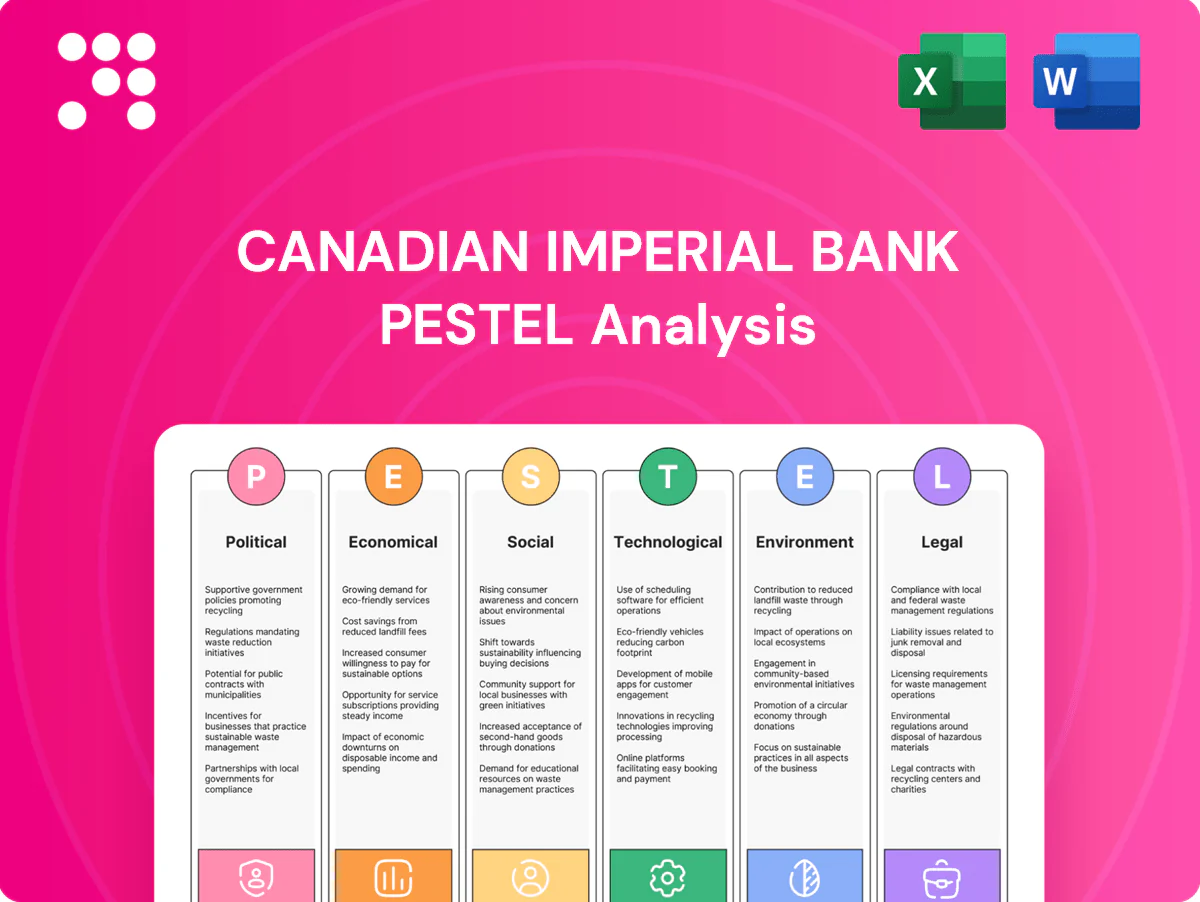

Canadian Imperial Bank PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Unlock strategic advantage with our PESTLE Analysis of Canadian Imperial Bank. Explore how political, economic, social, technological, legal and environmental forces will affect growth and risk. Purchase the full report to get actionable, editable insights ready for investment or strategy decisions.

Political factors

Federal stability and policy direction

Canada’s stable federal government underpins predictable banking policy and public spending, shaping credit demand amid a Bank of Canada policy rate near 5.00%, which affects borrowing costs and mortgage demand.

Election cycles can shift priorities on housing affordability, infrastructure and taxation, materially influencing retail and commercial loan growth.

U.S. administration changes under President Biden since 2021 affect regulatory tone and cross‑border dynamics; CIBC must scenario‑plan for policy pivots that alter consumer and business sentiment.

Housing and affordability interventions

Canadian governments enforce insured-mortgage rules (high-ratio LTV >80%) and cap insured amortizations at 25 years, plus tweak down‑payment and supply incentives; these policies shift origination volumes, pricing and risk mix. Municipal/provincial zoning and property‑tax changes affect housing turnover, while CIBC’s retail mortgage sensitivity requires rapid product and underwriting adjustments amid a Bank of Canada policy rate near 5% (2024).

Canada–U.S. trade and cross‑border relations

Bilateral relations shape currency, investment flows and corporate activity in CIBC’s core markets. The US accounted for about 75% of Canadian exports in 2023, linking trade friction directly to FX and cross‑border investment. Tariffs and reshoring initiatives, exemplified by the CHIPS Act’s roughly 52 billion USD in incentives, shift client cash flows and capital needs. Geopolitical shocks can tighten funding conditions and elevate credit risk, stressing advisory pipelines.

Public investment and industrial strategy

Canada’s long-term infrastructure program commits CAD 180 billion (Investing in Canada Plan 2016–2028), and federal fiscal programs targeting green energy and critical minerals create sizable financing opportunities for CIBC; government guarantees and subsidies (via programs and crown agencies) lower project risk and expand bankable pipelines. Timing and execution risks can delay cashflows and credit drawdowns; CIBC can align sector coverage to capture subsidized growth while enforcing prudent risk controls and project due diligence.

Sanctions and geopolitical tensions

Evolving sanctions regimes targeting Russia, China and other hotspots since 2022 have narrowed permissible counterparty exposures, forcing Canadian Imperial Bank to tighten limits on correspondent banking and trade finance and increasing screening complexity. Compliance costs have risen materially, with global sanctions‑compliance spending estimated near US$60bn in 2024, pressuring margins on cross‑border payments. Clients in defence, dual‑use tech and extractives now face enhanced due diligence; policy missteps could cause reputational fines and operational disruptions.

- Impact: tighter counterparty limits, higher screening false positives

- Cost: global compliance spend ~US$60bn (2024)

- Clients: defence, dual‑use, extractives require enhanced KYC

- Risk: reputational damage and regulatory fines from policy errors

BoC ≈5% rate, US ≈75% of exports and US$60B sanctions raise cross-border risk

Canada’s stable federal policy and a Bank of Canada policy rate near 5.00% (2024) shape credit costs and mortgage demand. Election cycles and provincial zoning/tax shifts materially influence retail and commercial loan growth. Strong US linkage (US ≈75% of Canadian exports, 2023) plus rising sanctions/compliance costs (~US$60bn, 2024) increase cross‑border risk and operational expense.

| Metric | Value |

|---|---|

| BoC policy rate (2024) | ~5.00% |

| US share of exports (2023) | ~75% |

| Investing in Canada Plan | CAD 180B (2016–2028) |

| Global sanctions/compliance spend (2024) | ~US$60B |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Canadian Imperial Bank, with data-backed trends and forward-looking insights to identify risks and opportunities; formatted for direct use in executive reports, pitch decks, and strategic planning.

A concise, visually segmented PESTLE summary for Canadian Imperial Bank that’s easy to drop into presentations, editable for region- or business-line notes, and shareable across teams to streamline external risk discussions and strategic planning.

Economic factors

Interest rate cycle and NIM

Central bank paths — Bank of Canada at about 4.75% and US fed funds near 5.25–5.50% in mid‑2025 — directly drive CIBC's NIM: easing compresses NIM but can lift loan volumes and lower credit losses, while prolonged higher‑for‑longer rates raise deposit betas and delinquency rates; balance‑sheet hedging and active deposit repricing/segmentation remain critical levers to protect margins.

GDP growth and credit demand

Moderate North American GDP growth near 2% in 2024–25 supports CIBC business lending, fee income and capital-markets activity, bolstering corporate loan demand and transaction volumes. Economic slowdowns compress credit demand, raise loan-loss provisions and pressured loan growth seen in 2023–24. Divergence across energy, real estate and tech requires portfolio reweighting. CIBC should shift toward resilient sectors and fee-based revenue to mitigate cyclical softness.

Housing market dynamics

Canada's household debt-to-disposable-income ratio was about 176% (Q4 2024, Bank of Canada), making mortgages highly rate-sensitive; renewals at higher rates have lifted payment burdens and could raise arrears despite currently low insured-arrear rates (~0.15%, CMHC). Supply constraints and immigration targets of ~500,000/year through 2025 underpin long-term demand. Prudent underwriting, OSFI stress-testing and LGD controls remain vital for CIBC.

Labor market and wages

Tight Canadian labor markets (unemployment near 5.0% in 2024) have supported consumer spending and retail credit quality, while wage growth (~4.1% average hourly wage growth in 2024) has elevated CIBC’s operating costs and pressured efficiency ratios. Cooling employment could quickly weaken retail loan performance, prompting closer credit monitoring. Strategic workforce planning and automation investments can offset cost inflation.

- Unemployment: ~5.0% (2024)

- Wage growth: ~4.1% YoY (2024)

- Impacts: supports spending and credit quality; raises operating costs

- Mitigation: workforce planning, automation

FX and funding conditions

CAD/USD moves (around 1.35 USD/CAD in July 2025) affect CIBC’s translated earnings and cross‑border capital needs; market volatility has pushed wholesale funding spreads intermittently wider, pressuring liquidity buffers while banks maintain LCRs above 100% to absorb shocks. Diversified funding—roughly 60–70% deposits plus secured channels—combined with active ALM and hedging preserves earnings stability.

- FX rate: ~1.35 USD/CAD (Jul 2025)

- LCR: >100% (industry standard)

- Deposit funding: ~60–70% of mix

BoC ≈5% rate, US ≈75% of exports and US$60B sanctions raise cross-border risk

Higher-for-longer BoC (~4.75%) and Fed (5.25–5.50%) in mid-2025 squeeze NIMs but can boost loan volumes; active ALM, deposit repricing and hedging are key. Moderate GDP (~2% 2024–25) supports corporate lending and fees while sectoral divergence (energy, real estate, tech) requires reweighting. High household debt (176% Q4 2024) and mortgage renewals raise arrears risk despite low insured arrears (~0.15%).

| Metric | Value |

|---|---|

| BoC rate | ~4.75% |

| Fed funds | 5.25–5.50% |

| GDP | ~2% (2024–25) |

| Household DTI | 176% (Q4 2024) |

| Insured arrears | ~0.15% (CMHC) |

Preview Before You Purchase

Canadian Imperial Bank PESTLE Analysis

The preview shown here is the exact Canadian Imperial Bank PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. No placeholders or teasers; the content, layout, and structure visible here are the final file you’ll download immediately after payment.

Your Shortcut to Market Insight Starts Here

Unlock strategic advantage with our PESTLE Analysis of Canadian Imperial Bank. Explore how political, economic, social, technological, legal and environmental forces will affect growth and risk. Purchase the full report to get actionable, editable insights ready for investment or strategy decisions.

Political factors

Federal stability and policy direction

Canada’s stable federal government underpins predictable banking policy and public spending, shaping credit demand amid a Bank of Canada policy rate near 5.00%, which affects borrowing costs and mortgage demand.

Election cycles can shift priorities on housing affordability, infrastructure and taxation, materially influencing retail and commercial loan growth.

U.S. administration changes under President Biden since 2021 affect regulatory tone and cross‑border dynamics; CIBC must scenario‑plan for policy pivots that alter consumer and business sentiment.

Housing and affordability interventions

Canadian governments enforce insured-mortgage rules (high-ratio LTV >80%) and cap insured amortizations at 25 years, plus tweak down‑payment and supply incentives; these policies shift origination volumes, pricing and risk mix. Municipal/provincial zoning and property‑tax changes affect housing turnover, while CIBC’s retail mortgage sensitivity requires rapid product and underwriting adjustments amid a Bank of Canada policy rate near 5% (2024).

Canada–U.S. trade and cross‑border relations

Bilateral relations shape currency, investment flows and corporate activity in CIBC’s core markets. The US accounted for about 75% of Canadian exports in 2023, linking trade friction directly to FX and cross‑border investment. Tariffs and reshoring initiatives, exemplified by the CHIPS Act’s roughly 52 billion USD in incentives, shift client cash flows and capital needs. Geopolitical shocks can tighten funding conditions and elevate credit risk, stressing advisory pipelines.

Public investment and industrial strategy

Canada’s long-term infrastructure program commits CAD 180 billion (Investing in Canada Plan 2016–2028), and federal fiscal programs targeting green energy and critical minerals create sizable financing opportunities for CIBC; government guarantees and subsidies (via programs and crown agencies) lower project risk and expand bankable pipelines. Timing and execution risks can delay cashflows and credit drawdowns; CIBC can align sector coverage to capture subsidized growth while enforcing prudent risk controls and project due diligence.

Sanctions and geopolitical tensions

Evolving sanctions regimes targeting Russia, China and other hotspots since 2022 have narrowed permissible counterparty exposures, forcing Canadian Imperial Bank to tighten limits on correspondent banking and trade finance and increasing screening complexity. Compliance costs have risen materially, with global sanctions‑compliance spending estimated near US$60bn in 2024, pressuring margins on cross‑border payments. Clients in defence, dual‑use tech and extractives now face enhanced due diligence; policy missteps could cause reputational fines and operational disruptions.

- Impact: tighter counterparty limits, higher screening false positives

- Cost: global compliance spend ~US$60bn (2024)

- Clients: defence, dual‑use, extractives require enhanced KYC

- Risk: reputational damage and regulatory fines from policy errors

BoC ≈5% rate, US ≈75% of exports and US$60B sanctions raise cross-border risk

Canada’s stable federal policy and a Bank of Canada policy rate near 5.00% (2024) shape credit costs and mortgage demand. Election cycles and provincial zoning/tax shifts materially influence retail and commercial loan growth. Strong US linkage (US ≈75% of Canadian exports, 2023) plus rising sanctions/compliance costs (~US$60bn, 2024) increase cross‑border risk and operational expense.

| Metric | Value |

|---|---|

| BoC policy rate (2024) | ~5.00% |

| US share of exports (2023) | ~75% |

| Investing in Canada Plan | CAD 180B (2016–2028) |

| Global sanctions/compliance spend (2024) | ~US$60B |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Canadian Imperial Bank, with data-backed trends and forward-looking insights to identify risks and opportunities; formatted for direct use in executive reports, pitch decks, and strategic planning.

A concise, visually segmented PESTLE summary for Canadian Imperial Bank that’s easy to drop into presentations, editable for region- or business-line notes, and shareable across teams to streamline external risk discussions and strategic planning.

Economic factors

Interest rate cycle and NIM

Central bank paths — Bank of Canada at about 4.75% and US fed funds near 5.25–5.50% in mid‑2025 — directly drive CIBC's NIM: easing compresses NIM but can lift loan volumes and lower credit losses, while prolonged higher‑for‑longer rates raise deposit betas and delinquency rates; balance‑sheet hedging and active deposit repricing/segmentation remain critical levers to protect margins.

GDP growth and credit demand

Moderate North American GDP growth near 2% in 2024–25 supports CIBC business lending, fee income and capital-markets activity, bolstering corporate loan demand and transaction volumes. Economic slowdowns compress credit demand, raise loan-loss provisions and pressured loan growth seen in 2023–24. Divergence across energy, real estate and tech requires portfolio reweighting. CIBC should shift toward resilient sectors and fee-based revenue to mitigate cyclical softness.

Housing market dynamics

Canada's household debt-to-disposable-income ratio was about 176% (Q4 2024, Bank of Canada), making mortgages highly rate-sensitive; renewals at higher rates have lifted payment burdens and could raise arrears despite currently low insured-arrear rates (~0.15%, CMHC). Supply constraints and immigration targets of ~500,000/year through 2025 underpin long-term demand. Prudent underwriting, OSFI stress-testing and LGD controls remain vital for CIBC.

Labor market and wages

Tight Canadian labor markets (unemployment near 5.0% in 2024) have supported consumer spending and retail credit quality, while wage growth (~4.1% average hourly wage growth in 2024) has elevated CIBC’s operating costs and pressured efficiency ratios. Cooling employment could quickly weaken retail loan performance, prompting closer credit monitoring. Strategic workforce planning and automation investments can offset cost inflation.

- Unemployment: ~5.0% (2024)

- Wage growth: ~4.1% YoY (2024)

- Impacts: supports spending and credit quality; raises operating costs

- Mitigation: workforce planning, automation

FX and funding conditions

CAD/USD moves (around 1.35 USD/CAD in July 2025) affect CIBC’s translated earnings and cross‑border capital needs; market volatility has pushed wholesale funding spreads intermittently wider, pressuring liquidity buffers while banks maintain LCRs above 100% to absorb shocks. Diversified funding—roughly 60–70% deposits plus secured channels—combined with active ALM and hedging preserves earnings stability.

- FX rate: ~1.35 USD/CAD (Jul 2025)

- LCR: >100% (industry standard)

- Deposit funding: ~60–70% of mix

BoC ≈5% rate, US ≈75% of exports and US$60B sanctions raise cross-border risk

Higher-for-longer BoC (~4.75%) and Fed (5.25–5.50%) in mid-2025 squeeze NIMs but can boost loan volumes; active ALM, deposit repricing and hedging are key. Moderate GDP (~2% 2024–25) supports corporate lending and fees while sectoral divergence (energy, real estate, tech) requires reweighting. High household debt (176% Q4 2024) and mortgage renewals raise arrears risk despite low insured arrears (~0.15%).

| Metric | Value |

|---|---|

| BoC rate | ~4.75% |

| Fed funds | 5.25–5.50% |

| GDP | ~2% (2024–25) |

| Household DTI | 176% (Q4 2024) |

| Insured arrears | ~0.15% (CMHC) |

Preview Before You Purchase

Canadian Imperial Bank PESTLE Analysis

The preview shown here is the exact Canadian Imperial Bank PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. No placeholders or teasers; the content, layout, and structure visible here are the final file you’ll download immediately after payment.

Description

Your Shortcut to Market Insight Starts Here

Unlock strategic advantage with our PESTLE Analysis of Canadian Imperial Bank. Explore how political, economic, social, technological, legal and environmental forces will affect growth and risk. Purchase the full report to get actionable, editable insights ready for investment or strategy decisions.

Political factors

Federal stability and policy direction

Canada’s stable federal government underpins predictable banking policy and public spending, shaping credit demand amid a Bank of Canada policy rate near 5.00%, which affects borrowing costs and mortgage demand.

Election cycles can shift priorities on housing affordability, infrastructure and taxation, materially influencing retail and commercial loan growth.

U.S. administration changes under President Biden since 2021 affect regulatory tone and cross‑border dynamics; CIBC must scenario‑plan for policy pivots that alter consumer and business sentiment.

Housing and affordability interventions

Canadian governments enforce insured-mortgage rules (high-ratio LTV >80%) and cap insured amortizations at 25 years, plus tweak down‑payment and supply incentives; these policies shift origination volumes, pricing and risk mix. Municipal/provincial zoning and property‑tax changes affect housing turnover, while CIBC’s retail mortgage sensitivity requires rapid product and underwriting adjustments amid a Bank of Canada policy rate near 5% (2024).

Canada–U.S. trade and cross‑border relations

Bilateral relations shape currency, investment flows and corporate activity in CIBC’s core markets. The US accounted for about 75% of Canadian exports in 2023, linking trade friction directly to FX and cross‑border investment. Tariffs and reshoring initiatives, exemplified by the CHIPS Act’s roughly 52 billion USD in incentives, shift client cash flows and capital needs. Geopolitical shocks can tighten funding conditions and elevate credit risk, stressing advisory pipelines.

Public investment and industrial strategy

Canada’s long-term infrastructure program commits CAD 180 billion (Investing in Canada Plan 2016–2028), and federal fiscal programs targeting green energy and critical minerals create sizable financing opportunities for CIBC; government guarantees and subsidies (via programs and crown agencies) lower project risk and expand bankable pipelines. Timing and execution risks can delay cashflows and credit drawdowns; CIBC can align sector coverage to capture subsidized growth while enforcing prudent risk controls and project due diligence.

Sanctions and geopolitical tensions

Evolving sanctions regimes targeting Russia, China and other hotspots since 2022 have narrowed permissible counterparty exposures, forcing Canadian Imperial Bank to tighten limits on correspondent banking and trade finance and increasing screening complexity. Compliance costs have risen materially, with global sanctions‑compliance spending estimated near US$60bn in 2024, pressuring margins on cross‑border payments. Clients in defence, dual‑use tech and extractives now face enhanced due diligence; policy missteps could cause reputational fines and operational disruptions.

- Impact: tighter counterparty limits, higher screening false positives

- Cost: global compliance spend ~US$60bn (2024)

- Clients: defence, dual‑use, extractives require enhanced KYC

- Risk: reputational damage and regulatory fines from policy errors

BoC ≈5% rate, US ≈75% of exports and US$60B sanctions raise cross-border risk

Canada’s stable federal policy and a Bank of Canada policy rate near 5.00% (2024) shape credit costs and mortgage demand. Election cycles and provincial zoning/tax shifts materially influence retail and commercial loan growth. Strong US linkage (US ≈75% of Canadian exports, 2023) plus rising sanctions/compliance costs (~US$60bn, 2024) increase cross‑border risk and operational expense.

| Metric | Value |

|---|---|

| BoC policy rate (2024) | ~5.00% |

| US share of exports (2023) | ~75% |

| Investing in Canada Plan | CAD 180B (2016–2028) |

| Global sanctions/compliance spend (2024) | ~US$60B |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Canadian Imperial Bank, with data-backed trends and forward-looking insights to identify risks and opportunities; formatted for direct use in executive reports, pitch decks, and strategic planning.

A concise, visually segmented PESTLE summary for Canadian Imperial Bank that’s easy to drop into presentations, editable for region- or business-line notes, and shareable across teams to streamline external risk discussions and strategic planning.

Economic factors

Interest rate cycle and NIM

Central bank paths — Bank of Canada at about 4.75% and US fed funds near 5.25–5.50% in mid‑2025 — directly drive CIBC's NIM: easing compresses NIM but can lift loan volumes and lower credit losses, while prolonged higher‑for‑longer rates raise deposit betas and delinquency rates; balance‑sheet hedging and active deposit repricing/segmentation remain critical levers to protect margins.

GDP growth and credit demand

Moderate North American GDP growth near 2% in 2024–25 supports CIBC business lending, fee income and capital-markets activity, bolstering corporate loan demand and transaction volumes. Economic slowdowns compress credit demand, raise loan-loss provisions and pressured loan growth seen in 2023–24. Divergence across energy, real estate and tech requires portfolio reweighting. CIBC should shift toward resilient sectors and fee-based revenue to mitigate cyclical softness.

Housing market dynamics

Canada's household debt-to-disposable-income ratio was about 176% (Q4 2024, Bank of Canada), making mortgages highly rate-sensitive; renewals at higher rates have lifted payment burdens and could raise arrears despite currently low insured-arrear rates (~0.15%, CMHC). Supply constraints and immigration targets of ~500,000/year through 2025 underpin long-term demand. Prudent underwriting, OSFI stress-testing and LGD controls remain vital for CIBC.

Labor market and wages

Tight Canadian labor markets (unemployment near 5.0% in 2024) have supported consumer spending and retail credit quality, while wage growth (~4.1% average hourly wage growth in 2024) has elevated CIBC’s operating costs and pressured efficiency ratios. Cooling employment could quickly weaken retail loan performance, prompting closer credit monitoring. Strategic workforce planning and automation investments can offset cost inflation.

- Unemployment: ~5.0% (2024)

- Wage growth: ~4.1% YoY (2024)

- Impacts: supports spending and credit quality; raises operating costs

- Mitigation: workforce planning, automation

FX and funding conditions

CAD/USD moves (around 1.35 USD/CAD in July 2025) affect CIBC’s translated earnings and cross‑border capital needs; market volatility has pushed wholesale funding spreads intermittently wider, pressuring liquidity buffers while banks maintain LCRs above 100% to absorb shocks. Diversified funding—roughly 60–70% deposits plus secured channels—combined with active ALM and hedging preserves earnings stability.

- FX rate: ~1.35 USD/CAD (Jul 2025)

- LCR: >100% (industry standard)

- Deposit funding: ~60–70% of mix

BoC ≈5% rate, US ≈75% of exports and US$60B sanctions raise cross-border risk

Higher-for-longer BoC (~4.75%) and Fed (5.25–5.50%) in mid-2025 squeeze NIMs but can boost loan volumes; active ALM, deposit repricing and hedging are key. Moderate GDP (~2% 2024–25) supports corporate lending and fees while sectoral divergence (energy, real estate, tech) requires reweighting. High household debt (176% Q4 2024) and mortgage renewals raise arrears risk despite low insured arrears (~0.15%).

| Metric | Value |

|---|---|

| BoC rate | ~4.75% |

| Fed funds | 5.25–5.50% |

| GDP | ~2% (2024–25) |

| Household DTI | 176% (Q4 2024) |

| Insured arrears | ~0.15% (CMHC) |

Preview Before You Purchase

Canadian Imperial Bank PESTLE Analysis

The preview shown here is the exact Canadian Imperial Bank PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. No placeholders or teasers; the content, layout, and structure visible here are the final file you’ll download immediately after payment.