CIE Automotive SWOT Analysis

Make Insightful Decisions Backed by Expert Research

CIE Automotive combines scale, diversified OEM relationships, and advanced manufacturing know-how, but faces EV-driven technology shifts, margin pressure, and supply-chain volatility. Discover strategic opportunities and hidden risks in our full SWOT—complete, editable Word and Excel deliverables with actionable insights for investors and strategists. Purchase now to plan with confidence.

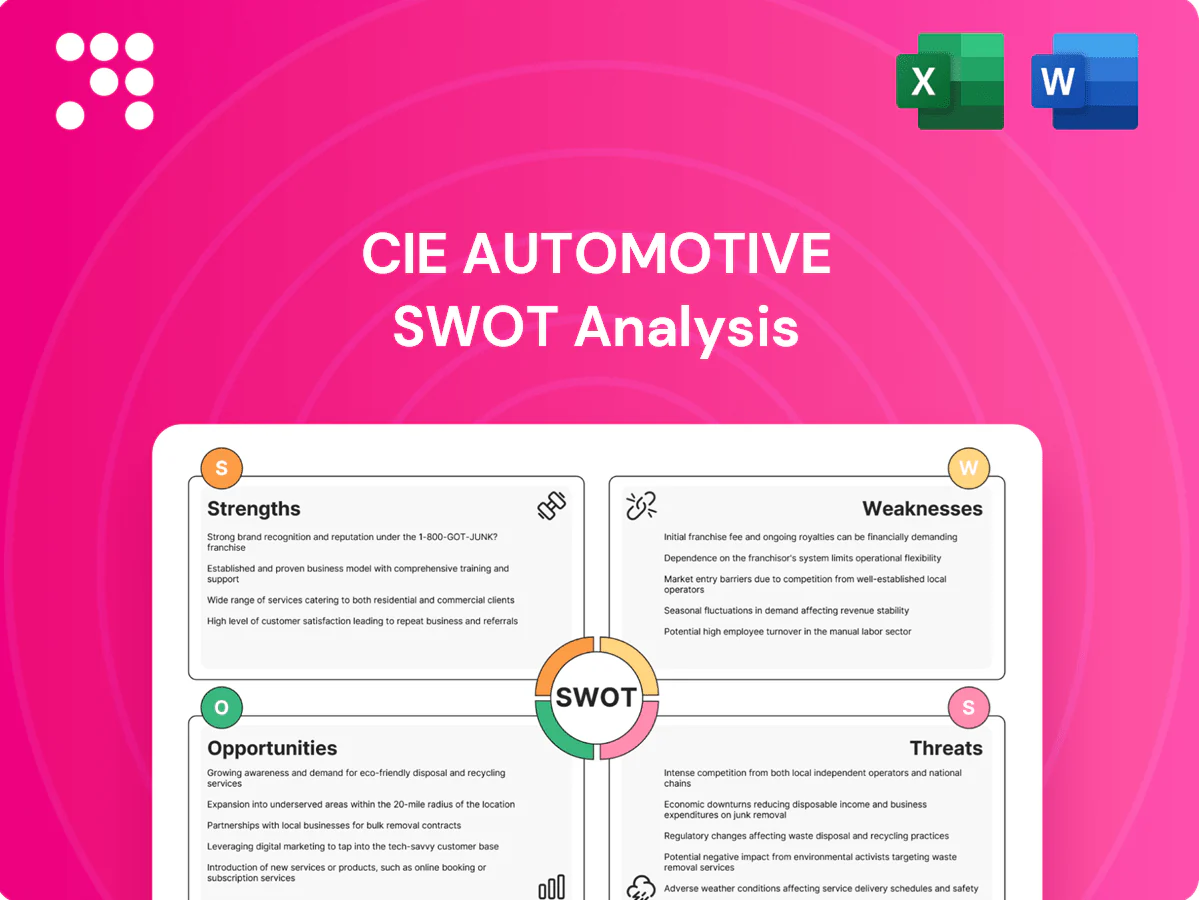

Strengths

Diversified manufacturing technologies

CIE Automotive operates over 100 plants in 16 countries and reported roughly €5bn revenue in FY2024; spanning forging, casting, machining and injection molding reduces reliance on any single process, enables program rerouting to optimal cost/capability, speeds response to OEM design changes and volume swings, and boosts value capture across metal, plastic and aluminum components.

Global OEM customer base

Supplying vehicle manufacturers worldwide spreads program and regional risk, with CIE Automotive operating in 22 countries. Its multi-continent footprint of about 90 plants supports just-in-time delivery and localization. Global OEM relationships enable cross-selling of assemblies and engineered solutions, and scale reinforced preferred-supplier status, contributing to FY2024 revenue of roughly €4.6bn.

System-level assemblies expertise

Beyond single parts, CIE Automotive delivers system-level assemblies integrating multiple materials and processes, raising switching costs and margins versus commoditized components. Co-engineering with OEMs embeds CIE early in platform cycles, reflected in 2024 sales of about €4.1bn and EBITDA margin near 11%. This differentiation improves performance, weight and total cost for OEM platforms.

Innovation and sustainability focus

CIE Automotive leverages lightweighting, recyclable materials and process efficiency to align with OEM ESG targets, supporting a supplier role as global BEV sales reached about 14 million units in 2023; the group reported roughly €3.3bn revenue in 2023, underpinning scale for sustainable R&D. Investments in energy-efficient production reduce costs and emissions, while design-for-manufacture accelerates PPAP and program launches, helping secure EV and next‑gen platform awards.

- Lightweighting aligned with OEM ESG

- ~€3.3bn revenue (2023) supports sustainable R&D

- Design-for-manufacture speeds PPAP/launch

- Supports wins in EV and next‑gen platforms

Exposure to EV platforms

CIE Automotive leverages aluminum, precision machining and thermal/structural part expertise to meet EV platform demands; CIE reported €3.6bn revenue in FY2023, underscoring scale. The shift from powertrain to chassis, body and e-mobility components sustains relevance as OEMs electrify. Early penetration in EV programs can lock long-lived platform contracts and drive growth as electrification advances.

- Capabilities: aluminum, precision machining, thermal/structural

- Shift: powertrain → chassis/body/e-mobility

- Timing: early EV program wins secure platforms

- Growth: positioned for electrification-driven revenue expansion

Global supplier: €5.0bn revenue, 100+ plants in ≈22 countries, ~11% EBITDA

CIE Automotive's scale—roughly €5.0bn revenue in FY2024 and over 100 plants—supports diversified processes (forging, casting, machining, injection) and global OEM programs. Multi‑continent footprint (≈22 countries) enables JIT/localization and risk spreading. System-level assemblies, co-engineering and ~11% EBITDA margin (2024) raise switching costs and margin resilience.

| Metric | Value | Relevance |

|---|---|---|

| Revenue FY2024 | €5.0bn | Scale for R&D/supply |

| Plants | >100 | Process diversity |

| Countries | ≈22 | Localization/JIT |

| EBITDA margin 2024 | ~11% | Profitability |

What is included in the product

Delivers a strategic overview of CIE Automotive’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats to assess competitive position, growth drivers, operational gaps and market risks.

Provides a concise SWOT matrix for CIE Automotive to align strategy quickly and relieve analysis bottlenecks. Ideal for executives and analysts needing a visual, at-a-glance snapshot of strategic positioning for fast decision-making.

Weaknesses

Cyclical end-market dependence

CIE Automotive’s revenue tracks global automotive production, so downturns directly reduce top-line growth and can flip profitable quarters into losses. Demand shocks rapidly cascade into plant underutilization, raising per-unit costs and idle-capacity charges. High fixed-cost exposure compresses margins during slowdowns, while forecasting errors amplify inventory buildups and working-capital strain.

Capital-intensive operations

Multiple production stages demand continuous capex for presses, foundries, tooling and automation, driving high fixed investment needs and long lead times for capacity additions.

Tooling amortization and ongoing maintenance represent material recurring costs that pressure margins until programs reach scale.

Returns depend on sustained plant utilization and program longevity; contract terminations or low volumes markedly erode ROI.

Accelerating vehicle electrification and digital manufacturing risk faster asset obsolescence, raising replacement and upgrade frequency.

Commodity and energy cost sensitivity

Metal resins, alloys and electricity represent CIE Automotive’s largest variable inputs, exposing margins to raw-material and energy swings; when input spikes occur pass-through clauses often lag, compressing operating margins for several quarters. Hedging programs limit but do not remove price volatility, leaving residual exposure to sudden commodity moves. Persistent regional energy price gaps (industrial gas/electricity) can make certain plants structurally less competitive versus peers located in lower-cost regions.

Complexity in multi-plant coordination

Global footprint of over 100 facilities across 25 countries adds logistics, quality and planning complexity; launch discipline must be flawless to meet diverse OEM and regulatory standards. Supply-chain shocks propagate rapidly, increasing variability that drives scrap, rework and expediting costs.

- Network scale: over 100 plants

- Regulatory/OEM diversity: multi-country launches

- Risk propagation: fast cross-process impact

- Cost effects: higher scrap, rework, expediting

Legacy exposure to ICE components

Legacy exposure to ICE components leaves CIE vulnerable as EV adoption accelerates; global EV sales share rose to about 14% in 2023 (IEA) and continued increasing in 2024, pressuring demand for some product lines. Reallocating capacity to EV-relevant parts requires capital and time, risking margin dilution during the transition while customer nominations increasingly favor newer technologies.

- High ICE share in legacy portfolio

- Capacity reallocation needs CAPEX and time

- Short-term margin dilution risk

- Customer nominations shifting to EV components

Suppliers' margins squeeze as production volatility and rising EV share force costly retooling

Revenue tightly tracks global vehicle production, so downturns and forecast errors quickly cut utilization, raise per-unit costs and compress margins; high fixed capex and tooling amortization amplify this exposure. Legacy ICE mix faces disruption as EV share reached about 14% in 2023 and continued rising in 2024, forcing costly reallocation and potential short-term margin dilution.

| Metric | Value |

|---|---|

| Plants | Over 100 |

| Countries | 25 |

| EV share (IEA) | ~14% (2023), rising in 2024 |

What You See Is What You Get

CIE Automotive SWOT Analysis

This is the actual CIE Automotive SWOT analysis document you'll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the complete structure and insights. Buy to unlock the editable, full version.

Make Insightful Decisions Backed by Expert Research

CIE Automotive combines scale, diversified OEM relationships, and advanced manufacturing know-how, but faces EV-driven technology shifts, margin pressure, and supply-chain volatility. Discover strategic opportunities and hidden risks in our full SWOT—complete, editable Word and Excel deliverables with actionable insights for investors and strategists. Purchase now to plan with confidence.

Strengths

Diversified manufacturing technologies

CIE Automotive operates over 100 plants in 16 countries and reported roughly €5bn revenue in FY2024; spanning forging, casting, machining and injection molding reduces reliance on any single process, enables program rerouting to optimal cost/capability, speeds response to OEM design changes and volume swings, and boosts value capture across metal, plastic and aluminum components.

Global OEM customer base

Supplying vehicle manufacturers worldwide spreads program and regional risk, with CIE Automotive operating in 22 countries. Its multi-continent footprint of about 90 plants supports just-in-time delivery and localization. Global OEM relationships enable cross-selling of assemblies and engineered solutions, and scale reinforced preferred-supplier status, contributing to FY2024 revenue of roughly €4.6bn.

System-level assemblies expertise

Beyond single parts, CIE Automotive delivers system-level assemblies integrating multiple materials and processes, raising switching costs and margins versus commoditized components. Co-engineering with OEMs embeds CIE early in platform cycles, reflected in 2024 sales of about €4.1bn and EBITDA margin near 11%. This differentiation improves performance, weight and total cost for OEM platforms.

Innovation and sustainability focus

CIE Automotive leverages lightweighting, recyclable materials and process efficiency to align with OEM ESG targets, supporting a supplier role as global BEV sales reached about 14 million units in 2023; the group reported roughly €3.3bn revenue in 2023, underpinning scale for sustainable R&D. Investments in energy-efficient production reduce costs and emissions, while design-for-manufacture accelerates PPAP and program launches, helping secure EV and next‑gen platform awards.

- Lightweighting aligned with OEM ESG

- ~€3.3bn revenue (2023) supports sustainable R&D

- Design-for-manufacture speeds PPAP/launch

- Supports wins in EV and next‑gen platforms

Exposure to EV platforms

CIE Automotive leverages aluminum, precision machining and thermal/structural part expertise to meet EV platform demands; CIE reported €3.6bn revenue in FY2023, underscoring scale. The shift from powertrain to chassis, body and e-mobility components sustains relevance as OEMs electrify. Early penetration in EV programs can lock long-lived platform contracts and drive growth as electrification advances.

- Capabilities: aluminum, precision machining, thermal/structural

- Shift: powertrain → chassis/body/e-mobility

- Timing: early EV program wins secure platforms

- Growth: positioned for electrification-driven revenue expansion

Global supplier: €5.0bn revenue, 100+ plants in ≈22 countries, ~11% EBITDA

CIE Automotive's scale—roughly €5.0bn revenue in FY2024 and over 100 plants—supports diversified processes (forging, casting, machining, injection) and global OEM programs. Multi‑continent footprint (≈22 countries) enables JIT/localization and risk spreading. System-level assemblies, co-engineering and ~11% EBITDA margin (2024) raise switching costs and margin resilience.

| Metric | Value | Relevance |

|---|---|---|

| Revenue FY2024 | €5.0bn | Scale for R&D/supply |

| Plants | >100 | Process diversity |

| Countries | ≈22 | Localization/JIT |

| EBITDA margin 2024 | ~11% | Profitability |

What is included in the product

Delivers a strategic overview of CIE Automotive’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats to assess competitive position, growth drivers, operational gaps and market risks.

Provides a concise SWOT matrix for CIE Automotive to align strategy quickly and relieve analysis bottlenecks. Ideal for executives and analysts needing a visual, at-a-glance snapshot of strategic positioning for fast decision-making.

Weaknesses

Cyclical end-market dependence

CIE Automotive’s revenue tracks global automotive production, so downturns directly reduce top-line growth and can flip profitable quarters into losses. Demand shocks rapidly cascade into plant underutilization, raising per-unit costs and idle-capacity charges. High fixed-cost exposure compresses margins during slowdowns, while forecasting errors amplify inventory buildups and working-capital strain.

Capital-intensive operations

Multiple production stages demand continuous capex for presses, foundries, tooling and automation, driving high fixed investment needs and long lead times for capacity additions.

Tooling amortization and ongoing maintenance represent material recurring costs that pressure margins until programs reach scale.

Returns depend on sustained plant utilization and program longevity; contract terminations or low volumes markedly erode ROI.

Accelerating vehicle electrification and digital manufacturing risk faster asset obsolescence, raising replacement and upgrade frequency.

Commodity and energy cost sensitivity

Metal resins, alloys and electricity represent CIE Automotive’s largest variable inputs, exposing margins to raw-material and energy swings; when input spikes occur pass-through clauses often lag, compressing operating margins for several quarters. Hedging programs limit but do not remove price volatility, leaving residual exposure to sudden commodity moves. Persistent regional energy price gaps (industrial gas/electricity) can make certain plants structurally less competitive versus peers located in lower-cost regions.

Complexity in multi-plant coordination

Global footprint of over 100 facilities across 25 countries adds logistics, quality and planning complexity; launch discipline must be flawless to meet diverse OEM and regulatory standards. Supply-chain shocks propagate rapidly, increasing variability that drives scrap, rework and expediting costs.

- Network scale: over 100 plants

- Regulatory/OEM diversity: multi-country launches

- Risk propagation: fast cross-process impact

- Cost effects: higher scrap, rework, expediting

Legacy exposure to ICE components

Legacy exposure to ICE components leaves CIE vulnerable as EV adoption accelerates; global EV sales share rose to about 14% in 2023 (IEA) and continued increasing in 2024, pressuring demand for some product lines. Reallocating capacity to EV-relevant parts requires capital and time, risking margin dilution during the transition while customer nominations increasingly favor newer technologies.

- High ICE share in legacy portfolio

- Capacity reallocation needs CAPEX and time

- Short-term margin dilution risk

- Customer nominations shifting to EV components

Suppliers' margins squeeze as production volatility and rising EV share force costly retooling

Revenue tightly tracks global vehicle production, so downturns and forecast errors quickly cut utilization, raise per-unit costs and compress margins; high fixed capex and tooling amortization amplify this exposure. Legacy ICE mix faces disruption as EV share reached about 14% in 2023 and continued rising in 2024, forcing costly reallocation and potential short-term margin dilution.

| Metric | Value |

|---|---|

| Plants | Over 100 |

| Countries | 25 |

| EV share (IEA) | ~14% (2023), rising in 2024 |

What You See Is What You Get

CIE Automotive SWOT Analysis

This is the actual CIE Automotive SWOT analysis document you'll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the complete structure and insights. Buy to unlock the editable, full version.

Description

Make Insightful Decisions Backed by Expert Research

CIE Automotive combines scale, diversified OEM relationships, and advanced manufacturing know-how, but faces EV-driven technology shifts, margin pressure, and supply-chain volatility. Discover strategic opportunities and hidden risks in our full SWOT—complete, editable Word and Excel deliverables with actionable insights for investors and strategists. Purchase now to plan with confidence.

Strengths

Diversified manufacturing technologies

CIE Automotive operates over 100 plants in 16 countries and reported roughly €5bn revenue in FY2024; spanning forging, casting, machining and injection molding reduces reliance on any single process, enables program rerouting to optimal cost/capability, speeds response to OEM design changes and volume swings, and boosts value capture across metal, plastic and aluminum components.

Global OEM customer base

Supplying vehicle manufacturers worldwide spreads program and regional risk, with CIE Automotive operating in 22 countries. Its multi-continent footprint of about 90 plants supports just-in-time delivery and localization. Global OEM relationships enable cross-selling of assemblies and engineered solutions, and scale reinforced preferred-supplier status, contributing to FY2024 revenue of roughly €4.6bn.

System-level assemblies expertise

Beyond single parts, CIE Automotive delivers system-level assemblies integrating multiple materials and processes, raising switching costs and margins versus commoditized components. Co-engineering with OEMs embeds CIE early in platform cycles, reflected in 2024 sales of about €4.1bn and EBITDA margin near 11%. This differentiation improves performance, weight and total cost for OEM platforms.

Innovation and sustainability focus

CIE Automotive leverages lightweighting, recyclable materials and process efficiency to align with OEM ESG targets, supporting a supplier role as global BEV sales reached about 14 million units in 2023; the group reported roughly €3.3bn revenue in 2023, underpinning scale for sustainable R&D. Investments in energy-efficient production reduce costs and emissions, while design-for-manufacture accelerates PPAP and program launches, helping secure EV and next‑gen platform awards.

- Lightweighting aligned with OEM ESG

- ~€3.3bn revenue (2023) supports sustainable R&D

- Design-for-manufacture speeds PPAP/launch

- Supports wins in EV and next‑gen platforms

Exposure to EV platforms

CIE Automotive leverages aluminum, precision machining and thermal/structural part expertise to meet EV platform demands; CIE reported €3.6bn revenue in FY2023, underscoring scale. The shift from powertrain to chassis, body and e-mobility components sustains relevance as OEMs electrify. Early penetration in EV programs can lock long-lived platform contracts and drive growth as electrification advances.

- Capabilities: aluminum, precision machining, thermal/structural

- Shift: powertrain → chassis/body/e-mobility

- Timing: early EV program wins secure platforms

- Growth: positioned for electrification-driven revenue expansion

Global supplier: €5.0bn revenue, 100+ plants in ≈22 countries, ~11% EBITDA

CIE Automotive's scale—roughly €5.0bn revenue in FY2024 and over 100 plants—supports diversified processes (forging, casting, machining, injection) and global OEM programs. Multi‑continent footprint (≈22 countries) enables JIT/localization and risk spreading. System-level assemblies, co-engineering and ~11% EBITDA margin (2024) raise switching costs and margin resilience.

| Metric | Value | Relevance |

|---|---|---|

| Revenue FY2024 | €5.0bn | Scale for R&D/supply |

| Plants | >100 | Process diversity |

| Countries | ≈22 | Localization/JIT |

| EBITDA margin 2024 | ~11% | Profitability |

What is included in the product

Delivers a strategic overview of CIE Automotive’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats to assess competitive position, growth drivers, operational gaps and market risks.

Provides a concise SWOT matrix for CIE Automotive to align strategy quickly and relieve analysis bottlenecks. Ideal for executives and analysts needing a visual, at-a-glance snapshot of strategic positioning for fast decision-making.

Weaknesses

Cyclical end-market dependence

CIE Automotive’s revenue tracks global automotive production, so downturns directly reduce top-line growth and can flip profitable quarters into losses. Demand shocks rapidly cascade into plant underutilization, raising per-unit costs and idle-capacity charges. High fixed-cost exposure compresses margins during slowdowns, while forecasting errors amplify inventory buildups and working-capital strain.

Capital-intensive operations

Multiple production stages demand continuous capex for presses, foundries, tooling and automation, driving high fixed investment needs and long lead times for capacity additions.

Tooling amortization and ongoing maintenance represent material recurring costs that pressure margins until programs reach scale.

Returns depend on sustained plant utilization and program longevity; contract terminations or low volumes markedly erode ROI.

Accelerating vehicle electrification and digital manufacturing risk faster asset obsolescence, raising replacement and upgrade frequency.

Commodity and energy cost sensitivity

Metal resins, alloys and electricity represent CIE Automotive’s largest variable inputs, exposing margins to raw-material and energy swings; when input spikes occur pass-through clauses often lag, compressing operating margins for several quarters. Hedging programs limit but do not remove price volatility, leaving residual exposure to sudden commodity moves. Persistent regional energy price gaps (industrial gas/electricity) can make certain plants structurally less competitive versus peers located in lower-cost regions.

Complexity in multi-plant coordination

Global footprint of over 100 facilities across 25 countries adds logistics, quality and planning complexity; launch discipline must be flawless to meet diverse OEM and regulatory standards. Supply-chain shocks propagate rapidly, increasing variability that drives scrap, rework and expediting costs.

- Network scale: over 100 plants

- Regulatory/OEM diversity: multi-country launches

- Risk propagation: fast cross-process impact

- Cost effects: higher scrap, rework, expediting

Legacy exposure to ICE components

Legacy exposure to ICE components leaves CIE vulnerable as EV adoption accelerates; global EV sales share rose to about 14% in 2023 (IEA) and continued increasing in 2024, pressuring demand for some product lines. Reallocating capacity to EV-relevant parts requires capital and time, risking margin dilution during the transition while customer nominations increasingly favor newer technologies.

- High ICE share in legacy portfolio

- Capacity reallocation needs CAPEX and time

- Short-term margin dilution risk

- Customer nominations shifting to EV components

Suppliers' margins squeeze as production volatility and rising EV share force costly retooling

Revenue tightly tracks global vehicle production, so downturns and forecast errors quickly cut utilization, raise per-unit costs and compress margins; high fixed capex and tooling amortization amplify this exposure. Legacy ICE mix faces disruption as EV share reached about 14% in 2023 and continued rising in 2024, forcing costly reallocation and potential short-term margin dilution.

| Metric | Value |

|---|---|

| Plants | Over 100 |

| Countries | 25 |

| EV share (IEA) | ~14% (2023), rising in 2024 |

What You See Is What You Get

CIE Automotive SWOT Analysis

This is the actual CIE Automotive SWOT analysis document you'll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the complete structure and insights. Buy to unlock the editable, full version.