Ciena Porter's Five Forces Analysis

Don't Miss the Bigger Picture

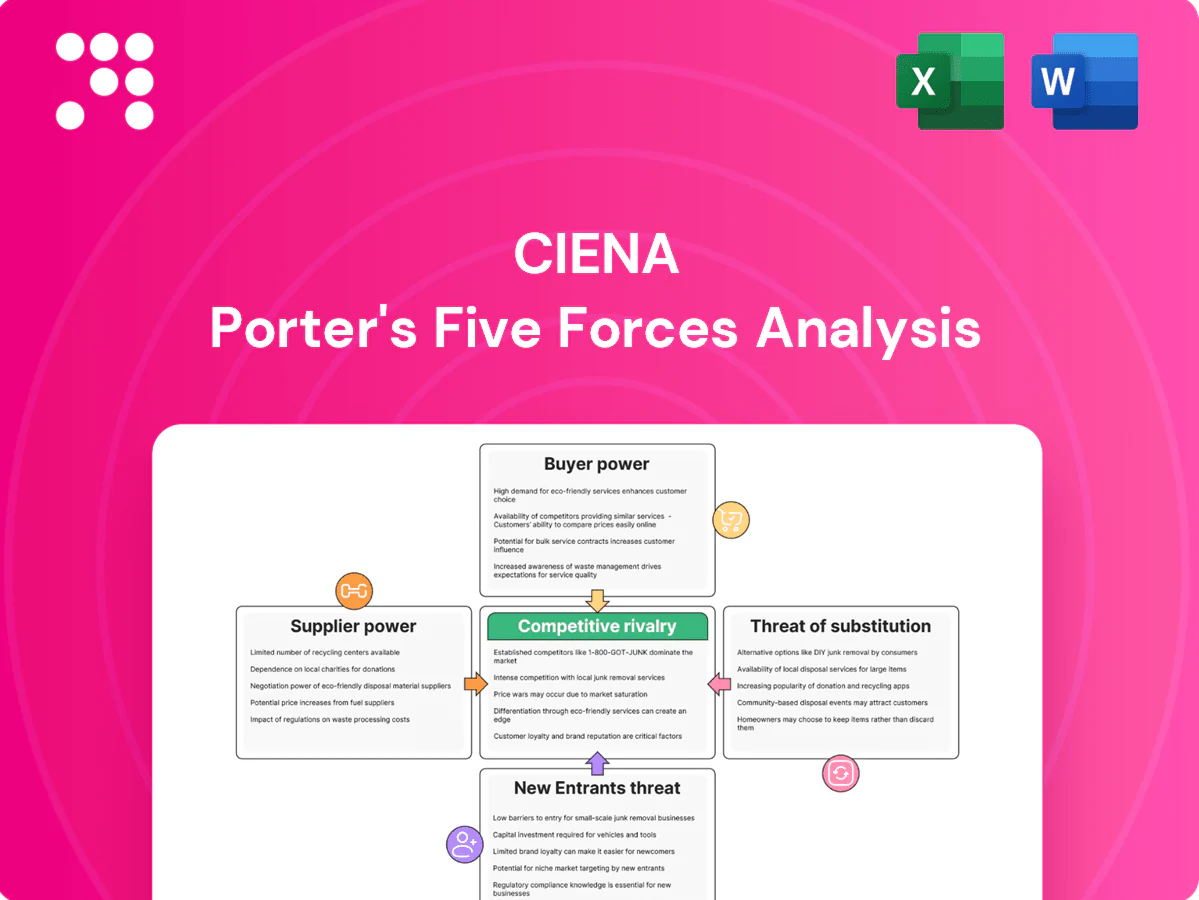

Ciena’s Porter's Five Forces snapshot highlights strong supplier power, intense rivalry, moderate buyer leverage, low threat of substitutes, and meaningful barriers to entry. These forces shape margins and strategic choices across optical networking and services. This brief teaser only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ciena’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated component sources

Ciena depends on a narrow supplier base for coherent DSPs, high-end optics and specialty semiconductors, which increases supplier leverage during tight cycles or process-node transitions. In 2024 semiconductor lead times remained elevated at 20+ weeks, amplifying risk to Ciena’s delivery cadence and cost structure. Dual-sourcing is feasible for some legacy parts but not for bleeding-edge components, so any disruption can ripple through margins and backlog.

Advanced manufacturing dependence

Critical ASICs and modules for Ciena rely on advanced foundries and contract manufacturers; TSMC and Samsung together controlled roughly 70% of advanced-node capacity through 2023–2024, concentrating supplier power. Capacity constraints or node migrations have repeatedly shifted pricing leverage to suppliers, raising component costs. Long qualification cycles, typically 12–18 months, make rapid switching difficult. This dependence can compress Ciena margins during supply imbalances.

Proprietary IP in optics

Key Ciena modules embed supplier-owned IP in lasers, modulators and pluggables, and the global optical transceiver market was roughly USD 11B in 2024, concentrating bargaining power with incumbents. Proprietary designs limit interchangeability and can raise switching costs, with IP holders able to command premiums often in the 10–30% range for newest performance tiers. Ciena reduces exposure through in-house optics design and close co-development with key suppliers to retain margin and roadmap control.

Logistics and materials sensitivity

Specialty optical materials and global logistics raise cost and availability risk for Ciena; in 2024 supply-chain fragility contributed to longer lead times for tunable lasers and photonic components. Geopolitical export controls on advanced optics and semiconductors further constrain sourcing. Buffer inventory reduces stockouts but ties up working capital against Ciena’s ~3.1B 2024 revenue, boosting supplier leverage when their chains are compliant and resilient.

- Materials sensitivity: high

- Geopolitics/export controls: constrained

- Inventory trade-off: working capital impact

- Supplier strength: firms with resilient, compliant chains

Software and tooling reliance

Development tools, firmware, and testing platforms for Ciena often originate from niche vendors, creating dependency that lets suppliers dictate licensing and support terms which can delay delivery schedules and maintenance windows.

Deep integration into Ciena’s optical hardware and network OS raises switching friction, increasing migration costs and time; vendors with unique testbeds or firmware expertise can command higher fees and stricter SLAs.

Supply risk: >20-week lead times, TSMC+Samsung ~70% share, optical ~USD 11B

Ciena faces high supplier leverage due to narrow sources for DSPs, optics and specialty semiconductors; 2024 semiconductor lead times >20 weeks and node concentration raise delivery and cost risk. TSMC+Samsung held ~70% advanced-node capacity (2023–24), and the optical transceiver market was ~USD 11B in 2024, amplifying supplier pricing power.

| Metric | 2024 Value |

|---|---|

| Lead times | >20 weeks |

| Foundry concentration | TSMC+Samsung ~70% |

| Optical market | ~USD 11B |

| Ciena revenue | ~USD 3.1B |

What is included in the product

Uncovers competitive drivers, buyer and supplier power, threat of substitutes and new entrants, and intensity of rivalry shaping Ciena’s pricing, margins, and strategic positioning, while highlighting disruptive technologies and defenses that protect or threaten its market share.

A concise Porter's Five Forces summary for Ciena—visualize competitive pressures, supplier and buyer leverage, and threat of substitutes to quickly identify strategic pain points and prioritize high-impact responses.

Customers Bargaining Power

Highly concentrated buyers

Large carriers, hyperscalers and governments drive a significant share of Ciena’s business; Ciena reported $3.94 billion revenue in FY2024 with its top customers accounting for roughly 45% of sales, boosting buyer leverage. Their scale and sophisticated procurement teams extract favorable pricing and contractual terms. Competitive RFPs further compress margins and push tougher SLAs. Losing a key account would materially dent growth and cash flow.

Standards-based interoperability

Open standards like Open ROADM and 400/800G enable multi-vendor environments, reducing vendor lock-in and lowering technical switching barriers. Operational integration, end-to-end orchestration and strict service SLAs still anchor provider relationships, slowing churn. Buyers leveraged interoperability in 2024 to extract better commercial terms; Ciena reported roughly $3.3B revenue in FY2024, reflecting intense pricing and design competition.

Long sales cycles and proofs

Extensive 12–24 month lab and field trials typically precede volume awards for Ciena, with buyers using evaluation stages to extract concessions; fiscal 2024 revenue was about $4.08 billion, highlighting the scale behind protracted deals. Multi-year framework agreements lock in price curves, which together cap vendors’ near-term pricing power despite technology leadership.

Total cost and outcomes focus

Customers prioritize lifecycle cost, energy efficiency and automation outcomes; Ciena’s FY2024 revenue of about $3.7B underscores buyer leverage as operators demand proof of throughput gains and opex cuts to justify purchases, plus bundled support and flexible financing—forcing vendors to share efficiency gains through pricing and commercial terms.

- Lifecycle cost focus: proof of opex reduction

- Energy efficiency: lower power-per-bit demanded

- Automation outcomes: faster ROI and operational savings

- Commercials: bundled support and flexible financing

Vendor consolidation pressures

Many operators rationalize supplier counts to 3–5 preferred vendors by 2024 to streamline procurement and operations, making preferred-vendor status a gatekeeper for network RFPs. Consolidation boosts selected vendors’ volume but increases buyer leverage in negotiations. MSAs in 2024 routinely embed price and SLA penalty clauses that compress supplier margins and shift risk back to vendors.

- 3–5 preferred vendors common by 2024

- Preferred-vendor status controls RFP access

- Higher volume per vendor but greater buyer leverage

- MSAs with price/penalty clauses tighten margins

Major buyers drive vendor squeeze: ~45% customer share, tighter pricing and SLAs

Large buyers drive strong leverage: Ciena FY2024 revenue ~$3.94B with top customers ~45% of sales, enabling tougher pricing and SLAs. Open standards and multivendor RFPs lower switching costs, while 12–24 month trials and 3–5 preferred-vendor rationalization maintain procurement control. MSAs with price/SLA penalty clauses are routine, compressing vendor margins.

| Metric | Value |

|---|---|

| FY2024 revenue | $3.94B |

| Top-customer share | ~45% |

| Procurement cycle | 12–24 months |

| Preferred vendors per operator | 3–5 |

Full Version Awaits

Ciena Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Ciena you’ll receive after purchase—complete, professionally formatted, and data-driven. It contains the full competitive assessment, force-by-force evaluation, and strategic implications ready for immediate download. No placeholders or samples: the file displayed is the file you get, ready for use upon payment.

Don't Miss the Bigger Picture

Ciena’s Porter's Five Forces snapshot highlights strong supplier power, intense rivalry, moderate buyer leverage, low threat of substitutes, and meaningful barriers to entry. These forces shape margins and strategic choices across optical networking and services. This brief teaser only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ciena’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated component sources

Ciena depends on a narrow supplier base for coherent DSPs, high-end optics and specialty semiconductors, which increases supplier leverage during tight cycles or process-node transitions. In 2024 semiconductor lead times remained elevated at 20+ weeks, amplifying risk to Ciena’s delivery cadence and cost structure. Dual-sourcing is feasible for some legacy parts but not for bleeding-edge components, so any disruption can ripple through margins and backlog.

Advanced manufacturing dependence

Critical ASICs and modules for Ciena rely on advanced foundries and contract manufacturers; TSMC and Samsung together controlled roughly 70% of advanced-node capacity through 2023–2024, concentrating supplier power. Capacity constraints or node migrations have repeatedly shifted pricing leverage to suppliers, raising component costs. Long qualification cycles, typically 12–18 months, make rapid switching difficult. This dependence can compress Ciena margins during supply imbalances.

Proprietary IP in optics

Key Ciena modules embed supplier-owned IP in lasers, modulators and pluggables, and the global optical transceiver market was roughly USD 11B in 2024, concentrating bargaining power with incumbents. Proprietary designs limit interchangeability and can raise switching costs, with IP holders able to command premiums often in the 10–30% range for newest performance tiers. Ciena reduces exposure through in-house optics design and close co-development with key suppliers to retain margin and roadmap control.

Logistics and materials sensitivity

Specialty optical materials and global logistics raise cost and availability risk for Ciena; in 2024 supply-chain fragility contributed to longer lead times for tunable lasers and photonic components. Geopolitical export controls on advanced optics and semiconductors further constrain sourcing. Buffer inventory reduces stockouts but ties up working capital against Ciena’s ~3.1B 2024 revenue, boosting supplier leverage when their chains are compliant and resilient.

- Materials sensitivity: high

- Geopolitics/export controls: constrained

- Inventory trade-off: working capital impact

- Supplier strength: firms with resilient, compliant chains

Software and tooling reliance

Development tools, firmware, and testing platforms for Ciena often originate from niche vendors, creating dependency that lets suppliers dictate licensing and support terms which can delay delivery schedules and maintenance windows.

Deep integration into Ciena’s optical hardware and network OS raises switching friction, increasing migration costs and time; vendors with unique testbeds or firmware expertise can command higher fees and stricter SLAs.

Supply risk: >20-week lead times, TSMC+Samsung ~70% share, optical ~USD 11B

Ciena faces high supplier leverage due to narrow sources for DSPs, optics and specialty semiconductors; 2024 semiconductor lead times >20 weeks and node concentration raise delivery and cost risk. TSMC+Samsung held ~70% advanced-node capacity (2023–24), and the optical transceiver market was ~USD 11B in 2024, amplifying supplier pricing power.

| Metric | 2024 Value |

|---|---|

| Lead times | >20 weeks |

| Foundry concentration | TSMC+Samsung ~70% |

| Optical market | ~USD 11B |

| Ciena revenue | ~USD 3.1B |

What is included in the product

Uncovers competitive drivers, buyer and supplier power, threat of substitutes and new entrants, and intensity of rivalry shaping Ciena’s pricing, margins, and strategic positioning, while highlighting disruptive technologies and defenses that protect or threaten its market share.

A concise Porter's Five Forces summary for Ciena—visualize competitive pressures, supplier and buyer leverage, and threat of substitutes to quickly identify strategic pain points and prioritize high-impact responses.

Customers Bargaining Power

Highly concentrated buyers

Large carriers, hyperscalers and governments drive a significant share of Ciena’s business; Ciena reported $3.94 billion revenue in FY2024 with its top customers accounting for roughly 45% of sales, boosting buyer leverage. Their scale and sophisticated procurement teams extract favorable pricing and contractual terms. Competitive RFPs further compress margins and push tougher SLAs. Losing a key account would materially dent growth and cash flow.

Standards-based interoperability

Open standards like Open ROADM and 400/800G enable multi-vendor environments, reducing vendor lock-in and lowering technical switching barriers. Operational integration, end-to-end orchestration and strict service SLAs still anchor provider relationships, slowing churn. Buyers leveraged interoperability in 2024 to extract better commercial terms; Ciena reported roughly $3.3B revenue in FY2024, reflecting intense pricing and design competition.

Long sales cycles and proofs

Extensive 12–24 month lab and field trials typically precede volume awards for Ciena, with buyers using evaluation stages to extract concessions; fiscal 2024 revenue was about $4.08 billion, highlighting the scale behind protracted deals. Multi-year framework agreements lock in price curves, which together cap vendors’ near-term pricing power despite technology leadership.

Total cost and outcomes focus

Customers prioritize lifecycle cost, energy efficiency and automation outcomes; Ciena’s FY2024 revenue of about $3.7B underscores buyer leverage as operators demand proof of throughput gains and opex cuts to justify purchases, plus bundled support and flexible financing—forcing vendors to share efficiency gains through pricing and commercial terms.

- Lifecycle cost focus: proof of opex reduction

- Energy efficiency: lower power-per-bit demanded

- Automation outcomes: faster ROI and operational savings

- Commercials: bundled support and flexible financing

Vendor consolidation pressures

Many operators rationalize supplier counts to 3–5 preferred vendors by 2024 to streamline procurement and operations, making preferred-vendor status a gatekeeper for network RFPs. Consolidation boosts selected vendors’ volume but increases buyer leverage in negotiations. MSAs in 2024 routinely embed price and SLA penalty clauses that compress supplier margins and shift risk back to vendors.

- 3–5 preferred vendors common by 2024

- Preferred-vendor status controls RFP access

- Higher volume per vendor but greater buyer leverage

- MSAs with price/penalty clauses tighten margins

Major buyers drive vendor squeeze: ~45% customer share, tighter pricing and SLAs

Large buyers drive strong leverage: Ciena FY2024 revenue ~$3.94B with top customers ~45% of sales, enabling tougher pricing and SLAs. Open standards and multivendor RFPs lower switching costs, while 12–24 month trials and 3–5 preferred-vendor rationalization maintain procurement control. MSAs with price/SLA penalty clauses are routine, compressing vendor margins.

| Metric | Value |

|---|---|

| FY2024 revenue | $3.94B |

| Top-customer share | ~45% |

| Procurement cycle | 12–24 months |

| Preferred vendors per operator | 3–5 |

Full Version Awaits

Ciena Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Ciena you’ll receive after purchase—complete, professionally formatted, and data-driven. It contains the full competitive assessment, force-by-force evaluation, and strategic implications ready for immediate download. No placeholders or samples: the file displayed is the file you get, ready for use upon payment.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Ciena’s Porter's Five Forces snapshot highlights strong supplier power, intense rivalry, moderate buyer leverage, low threat of substitutes, and meaningful barriers to entry. These forces shape margins and strategic choices across optical networking and services. This brief teaser only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ciena’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated component sources

Ciena depends on a narrow supplier base for coherent DSPs, high-end optics and specialty semiconductors, which increases supplier leverage during tight cycles or process-node transitions. In 2024 semiconductor lead times remained elevated at 20+ weeks, amplifying risk to Ciena’s delivery cadence and cost structure. Dual-sourcing is feasible for some legacy parts but not for bleeding-edge components, so any disruption can ripple through margins and backlog.

Advanced manufacturing dependence

Critical ASICs and modules for Ciena rely on advanced foundries and contract manufacturers; TSMC and Samsung together controlled roughly 70% of advanced-node capacity through 2023–2024, concentrating supplier power. Capacity constraints or node migrations have repeatedly shifted pricing leverage to suppliers, raising component costs. Long qualification cycles, typically 12–18 months, make rapid switching difficult. This dependence can compress Ciena margins during supply imbalances.

Proprietary IP in optics

Key Ciena modules embed supplier-owned IP in lasers, modulators and pluggables, and the global optical transceiver market was roughly USD 11B in 2024, concentrating bargaining power with incumbents. Proprietary designs limit interchangeability and can raise switching costs, with IP holders able to command premiums often in the 10–30% range for newest performance tiers. Ciena reduces exposure through in-house optics design and close co-development with key suppliers to retain margin and roadmap control.

Logistics and materials sensitivity

Specialty optical materials and global logistics raise cost and availability risk for Ciena; in 2024 supply-chain fragility contributed to longer lead times for tunable lasers and photonic components. Geopolitical export controls on advanced optics and semiconductors further constrain sourcing. Buffer inventory reduces stockouts but ties up working capital against Ciena’s ~3.1B 2024 revenue, boosting supplier leverage when their chains are compliant and resilient.

- Materials sensitivity: high

- Geopolitics/export controls: constrained

- Inventory trade-off: working capital impact

- Supplier strength: firms with resilient, compliant chains

Software and tooling reliance

Development tools, firmware, and testing platforms for Ciena often originate from niche vendors, creating dependency that lets suppliers dictate licensing and support terms which can delay delivery schedules and maintenance windows.

Deep integration into Ciena’s optical hardware and network OS raises switching friction, increasing migration costs and time; vendors with unique testbeds or firmware expertise can command higher fees and stricter SLAs.

Supply risk: >20-week lead times, TSMC+Samsung ~70% share, optical ~USD 11B

Ciena faces high supplier leverage due to narrow sources for DSPs, optics and specialty semiconductors; 2024 semiconductor lead times >20 weeks and node concentration raise delivery and cost risk. TSMC+Samsung held ~70% advanced-node capacity (2023–24), and the optical transceiver market was ~USD 11B in 2024, amplifying supplier pricing power.

| Metric | 2024 Value |

|---|---|

| Lead times | >20 weeks |

| Foundry concentration | TSMC+Samsung ~70% |

| Optical market | ~USD 11B |

| Ciena revenue | ~USD 3.1B |

What is included in the product

Uncovers competitive drivers, buyer and supplier power, threat of substitutes and new entrants, and intensity of rivalry shaping Ciena’s pricing, margins, and strategic positioning, while highlighting disruptive technologies and defenses that protect or threaten its market share.

A concise Porter's Five Forces summary for Ciena—visualize competitive pressures, supplier and buyer leverage, and threat of substitutes to quickly identify strategic pain points and prioritize high-impact responses.

Customers Bargaining Power

Highly concentrated buyers

Large carriers, hyperscalers and governments drive a significant share of Ciena’s business; Ciena reported $3.94 billion revenue in FY2024 with its top customers accounting for roughly 45% of sales, boosting buyer leverage. Their scale and sophisticated procurement teams extract favorable pricing and contractual terms. Competitive RFPs further compress margins and push tougher SLAs. Losing a key account would materially dent growth and cash flow.

Standards-based interoperability

Open standards like Open ROADM and 400/800G enable multi-vendor environments, reducing vendor lock-in and lowering technical switching barriers. Operational integration, end-to-end orchestration and strict service SLAs still anchor provider relationships, slowing churn. Buyers leveraged interoperability in 2024 to extract better commercial terms; Ciena reported roughly $3.3B revenue in FY2024, reflecting intense pricing and design competition.

Long sales cycles and proofs

Extensive 12–24 month lab and field trials typically precede volume awards for Ciena, with buyers using evaluation stages to extract concessions; fiscal 2024 revenue was about $4.08 billion, highlighting the scale behind protracted deals. Multi-year framework agreements lock in price curves, which together cap vendors’ near-term pricing power despite technology leadership.

Total cost and outcomes focus

Customers prioritize lifecycle cost, energy efficiency and automation outcomes; Ciena’s FY2024 revenue of about $3.7B underscores buyer leverage as operators demand proof of throughput gains and opex cuts to justify purchases, plus bundled support and flexible financing—forcing vendors to share efficiency gains through pricing and commercial terms.

- Lifecycle cost focus: proof of opex reduction

- Energy efficiency: lower power-per-bit demanded

- Automation outcomes: faster ROI and operational savings

- Commercials: bundled support and flexible financing

Vendor consolidation pressures

Many operators rationalize supplier counts to 3–5 preferred vendors by 2024 to streamline procurement and operations, making preferred-vendor status a gatekeeper for network RFPs. Consolidation boosts selected vendors’ volume but increases buyer leverage in negotiations. MSAs in 2024 routinely embed price and SLA penalty clauses that compress supplier margins and shift risk back to vendors.

- 3–5 preferred vendors common by 2024

- Preferred-vendor status controls RFP access

- Higher volume per vendor but greater buyer leverage

- MSAs with price/penalty clauses tighten margins

Major buyers drive vendor squeeze: ~45% customer share, tighter pricing and SLAs

Large buyers drive strong leverage: Ciena FY2024 revenue ~$3.94B with top customers ~45% of sales, enabling tougher pricing and SLAs. Open standards and multivendor RFPs lower switching costs, while 12–24 month trials and 3–5 preferred-vendor rationalization maintain procurement control. MSAs with price/SLA penalty clauses are routine, compressing vendor margins.

| Metric | Value |

|---|---|

| FY2024 revenue | $3.94B |

| Top-customer share | ~45% |

| Procurement cycle | 12–24 months |

| Preferred vendors per operator | 3–5 |

Full Version Awaits

Ciena Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Ciena you’ll receive after purchase—complete, professionally formatted, and data-driven. It contains the full competitive assessment, force-by-force evaluation, and strategic implications ready for immediate download. No placeholders or samples: the file displayed is the file you get, ready for use upon payment.