Ciena PESTLE Analysis

Your Shortcut to Market Insight Starts Here

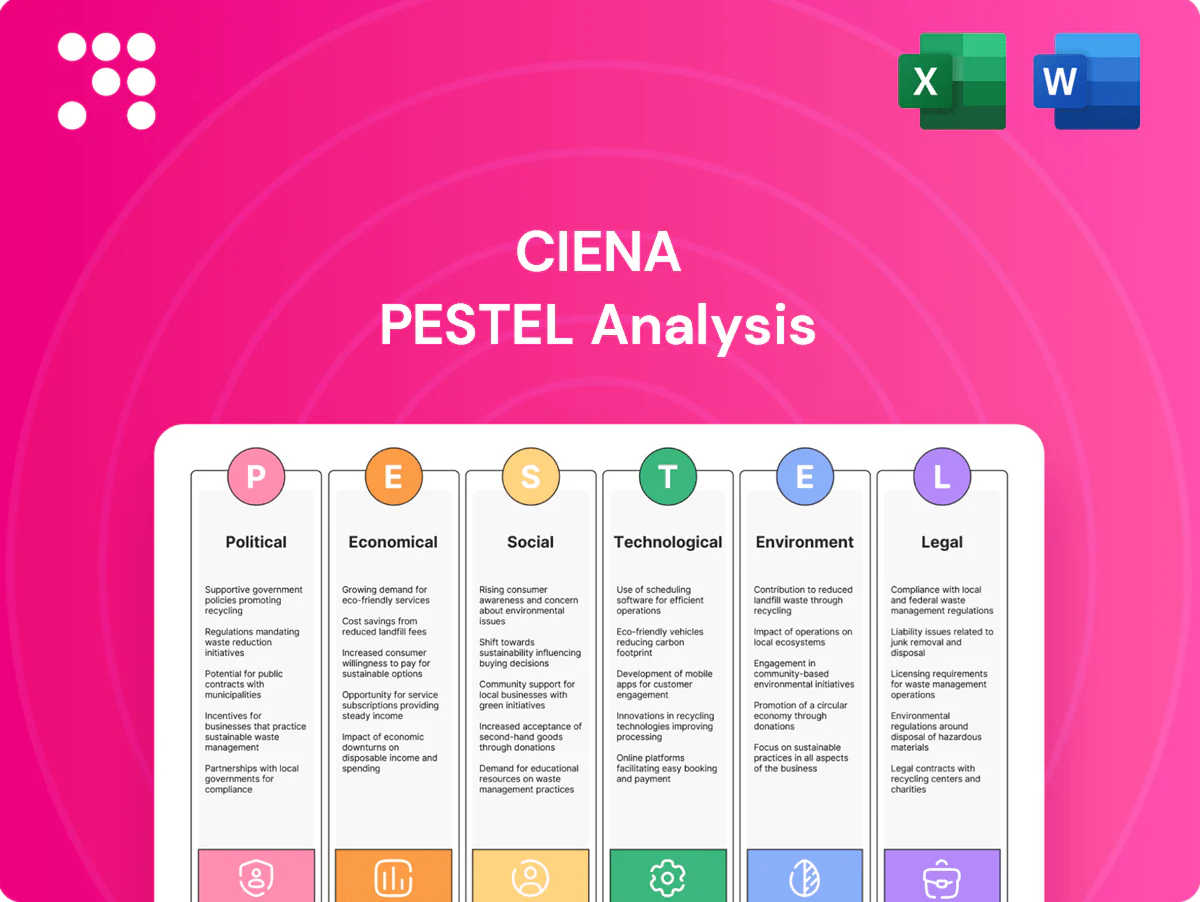

Gain strategic clarity on how political, economic, social, technological, legal and environmental forces are shaping Ciena's trajectory; our PESTLE highlights risks and growth levers investors and strategists need. This concise snapshot reveals critical external trends and competitive implications. Purchase the full, editable PESTLE for a detailed, actionable roadmap you can use immediately.

Political factors

Geopolitics and export controls

US–China tensions and allied export controls constrain Ciena’s sourcing, sales eligibility and joint R&D, shrinking addressable markets; Ciena reported $3.11B revenue in FY2024, intensifying exposure risks in Asia-Pacific. Restrictions on advanced optics and encryption narrow channel partners and OEM demand. Robust trade compliance and market diversification are essential to mitigate licensing delays, as shifting sanctions can quickly alter revenue mix and supply timelines.

Government telecom funding priorities

Public investment drives Ciena demand: US IIJA set aside roughly $65B for broadband with a $42.45B BEAD program, EU digital funds and emerging‑market stimulus accelerate middle‑mile and 5G/edge backbone builds. Programs favor open, secure, energy‑efficient solutions, boosting procurement success; conversely state or policy pauses (seen in BEAD rollout delays) can defer orders and revenue conversion.

National security and critical infrastructure

Designation of networks as critical infrastructure (US recognizes 16 sectors) heightens security, sovereignty and vendor‑trust requirements. Preference for vetted suppliers favors US‑based Ciena (FY2024 revenue about $3.6B) in sensitive deployments. Mandates like EO 14028 and NIST SBOM guidance increase compliance and reporting workload. Political scrutiny and export controls on foreign components are already forcing revisions to approved BOMs and supplier lists.

Trade policy, tariffs, and localization

Tariffs such as US Section 301 levies up to 25% on covered Chinese imports can raise Ciena's component COGS and compress margins on competitive bids; Ciena reported FY2024 revenue of about 4.01 billion USD, heightening sensitivity to input-cost swings. Localization incentives in key markets push assembly, testing, and service expansion to capture subsidies and reduce geopolitical exposure, while rapid policy shifts demand flexible logistics and pass‑through pricing mechanisms.

Standards and spectrum policy influence

US–China export controls, tariffs up to 25% strain suppliers; IIJA/BEAD $42.45B boosts demand

US–China tensions, export controls and Section 301 tariffs (up to 25%) restrict Ciena’s addressable markets and supply chains; Ciena FY2024 revenue was $3.11B, increasing exposure risk. Public programs (IIJA $65B, BEAD $42.45B) and WRC‑23 spectrum rules favor open, secure, disaggregated solutions, boosting near‑term demand while compliance burdens rise.

| Metric | Value |

|---|---|

| FY2024 revenue | $3.11B |

| IIJA total | $65B |

| BEAD | $42.45B |

| Section 301 tariff | up to 25% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Ciena across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven subpoints and industry-specific examples. Designed for executives, consultants and investors, it offers forward-looking insights, scenario planning and clean formatting ready for business plans, decks or reports.

A concise, visually segmented Ciena PESTLE summary that relieves meeting prep pain by offering an easily shareable, presentation-ready overview—editable for region or business-line notes and ideal for quick alignment, risk discussions, and strategic planning across teams.

Economic factors

Carrier capex cycles and enterprise spend

Telco and cloud operator capex cycles drive the timing of optical and packet upgrades, so Ciena sees order timing tied to large operator refresh and hyperscaler builds. Macro slowdowns or higher interest rates can defer multiyear transport projects, compressing near‑term revenue. Rising enterprise demand for secure, high‑bandwidth connectivity supports Ciena’s diversification into private 5G and campus networking. Ciena’s backlog and revenue visibility depend on multi‑year build plans and periodic budget flushes.

Component costs and supply chain elasticity

Semiconductor availability and optics component pricing tighten Ciena margins and extend lead times; the US CHIPS and Science Act mobilized about 52 billion dollars to boost capacity through 2024, easing but not eliminating shortages. Multi‑sourcing and design‑for‑availability lower volatility exposure by enabling alternate suppliers and pin‑compatible designs. Targeted inventory strategies balance resilience against working capital, while cost inflation drives value‑based pricing and aggressive cost‑down roadmaps.

Currency fluctuations and global mix

A strong US dollar (DXY averaged about 105 in 2024) pressures Ciena’s international revenue and compresses margins on translation relative to its roughly $3.3B FY2024 revenue base. Hedging programs reduce but do not eliminate FX exposure across sales and procurement. Shifts in regional mix change average selling prices and service attachments, while disciplined pricing and local financing help sustain competitiveness.

Competitive pricing dynamics

Competition from global OEMs and lower-cost rivals compresses ASPs in high-volume lanes; Ciena reported FY2024 revenue of 3.26 billion USD, reflecting scale amid pricing pressure. Differentiation via performance per watt, automation, and lower lifecycle TCO drives procurement decisions and higher-value deals. Bundled software and services help stabilize gross margin, while strategic accounts and multi-year framework agreements smooth pricing volatility.

- FY2024 revenue: 3.26 billion USD

- Software/services mix supports margin stability

- Performance-per-watt and automation = key differentiation

- Framework agreements reduce pricing swings

Cloud, AI, and data traffic secular growth

AI training/inference, video and cloud interconnect drove multi‑year bandwidth growth as global IP traffic rose roughly 27% in 2023 to about 320 EB/month, sustaining hyperscaler DCI demand for high‑capacity coherent and pluggables.

- Hyperscalers favor 800G+ coherent and pluggables

- Ciena positioned to grow wallet share via 800G+ and scalable automation

- Cyclical lulls possible, secular demand remains strong

US–China export controls, tariffs up to 25% strain suppliers; IIJA/BEAD $42.45B boosts demand

Telco/hyperscaler capex cycles and higher rates can delay multiyear transport projects, compressing near‑term revenue for Ciena. Component shortages and CHIPS funding (~52 billion USD through 2024) affect margins and lead times. FX (DXY ~105 in 2024) and intense OEM pricing pressure weigh on international margins; software/services mix cushions profitability.

| Metric | Value |

|---|---|

| FY2024 revenue | 3.26B USD |

| DXY avg 2024 | ~105 |

| CHIPS funding | ~52B USD |

| Global IP traffic 2023 | ~320 EB/mo |

Full Version Awaits

Ciena PESTLE Analysis

The preview shown here is the exact Ciena PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. This is the real, finished document with complete content and professional structure. No placeholders or teasers—what you see is what you’ll download immediately after checkout.

Your Shortcut to Market Insight Starts Here

Gain strategic clarity on how political, economic, social, technological, legal and environmental forces are shaping Ciena's trajectory; our PESTLE highlights risks and growth levers investors and strategists need. This concise snapshot reveals critical external trends and competitive implications. Purchase the full, editable PESTLE for a detailed, actionable roadmap you can use immediately.

Political factors

Geopolitics and export controls

US–China tensions and allied export controls constrain Ciena’s sourcing, sales eligibility and joint R&D, shrinking addressable markets; Ciena reported $3.11B revenue in FY2024, intensifying exposure risks in Asia-Pacific. Restrictions on advanced optics and encryption narrow channel partners and OEM demand. Robust trade compliance and market diversification are essential to mitigate licensing delays, as shifting sanctions can quickly alter revenue mix and supply timelines.

Government telecom funding priorities

Public investment drives Ciena demand: US IIJA set aside roughly $65B for broadband with a $42.45B BEAD program, EU digital funds and emerging‑market stimulus accelerate middle‑mile and 5G/edge backbone builds. Programs favor open, secure, energy‑efficient solutions, boosting procurement success; conversely state or policy pauses (seen in BEAD rollout delays) can defer orders and revenue conversion.

National security and critical infrastructure

Designation of networks as critical infrastructure (US recognizes 16 sectors) heightens security, sovereignty and vendor‑trust requirements. Preference for vetted suppliers favors US‑based Ciena (FY2024 revenue about $3.6B) in sensitive deployments. Mandates like EO 14028 and NIST SBOM guidance increase compliance and reporting workload. Political scrutiny and export controls on foreign components are already forcing revisions to approved BOMs and supplier lists.

Trade policy, tariffs, and localization

Tariffs such as US Section 301 levies up to 25% on covered Chinese imports can raise Ciena's component COGS and compress margins on competitive bids; Ciena reported FY2024 revenue of about 4.01 billion USD, heightening sensitivity to input-cost swings. Localization incentives in key markets push assembly, testing, and service expansion to capture subsidies and reduce geopolitical exposure, while rapid policy shifts demand flexible logistics and pass‑through pricing mechanisms.

Standards and spectrum policy influence

US–China export controls, tariffs up to 25% strain suppliers; IIJA/BEAD $42.45B boosts demand

US–China tensions, export controls and Section 301 tariffs (up to 25%) restrict Ciena’s addressable markets and supply chains; Ciena FY2024 revenue was $3.11B, increasing exposure risk. Public programs (IIJA $65B, BEAD $42.45B) and WRC‑23 spectrum rules favor open, secure, disaggregated solutions, boosting near‑term demand while compliance burdens rise.

| Metric | Value |

|---|---|

| FY2024 revenue | $3.11B |

| IIJA total | $65B |

| BEAD | $42.45B |

| Section 301 tariff | up to 25% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Ciena across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven subpoints and industry-specific examples. Designed for executives, consultants and investors, it offers forward-looking insights, scenario planning and clean formatting ready for business plans, decks or reports.

A concise, visually segmented Ciena PESTLE summary that relieves meeting prep pain by offering an easily shareable, presentation-ready overview—editable for region or business-line notes and ideal for quick alignment, risk discussions, and strategic planning across teams.

Economic factors

Carrier capex cycles and enterprise spend

Telco and cloud operator capex cycles drive the timing of optical and packet upgrades, so Ciena sees order timing tied to large operator refresh and hyperscaler builds. Macro slowdowns or higher interest rates can defer multiyear transport projects, compressing near‑term revenue. Rising enterprise demand for secure, high‑bandwidth connectivity supports Ciena’s diversification into private 5G and campus networking. Ciena’s backlog and revenue visibility depend on multi‑year build plans and periodic budget flushes.

Component costs and supply chain elasticity

Semiconductor availability and optics component pricing tighten Ciena margins and extend lead times; the US CHIPS and Science Act mobilized about 52 billion dollars to boost capacity through 2024, easing but not eliminating shortages. Multi‑sourcing and design‑for‑availability lower volatility exposure by enabling alternate suppliers and pin‑compatible designs. Targeted inventory strategies balance resilience against working capital, while cost inflation drives value‑based pricing and aggressive cost‑down roadmaps.

Currency fluctuations and global mix

A strong US dollar (DXY averaged about 105 in 2024) pressures Ciena’s international revenue and compresses margins on translation relative to its roughly $3.3B FY2024 revenue base. Hedging programs reduce but do not eliminate FX exposure across sales and procurement. Shifts in regional mix change average selling prices and service attachments, while disciplined pricing and local financing help sustain competitiveness.

Competitive pricing dynamics

Competition from global OEMs and lower-cost rivals compresses ASPs in high-volume lanes; Ciena reported FY2024 revenue of 3.26 billion USD, reflecting scale amid pricing pressure. Differentiation via performance per watt, automation, and lower lifecycle TCO drives procurement decisions and higher-value deals. Bundled software and services help stabilize gross margin, while strategic accounts and multi-year framework agreements smooth pricing volatility.

- FY2024 revenue: 3.26 billion USD

- Software/services mix supports margin stability

- Performance-per-watt and automation = key differentiation

- Framework agreements reduce pricing swings

Cloud, AI, and data traffic secular growth

AI training/inference, video and cloud interconnect drove multi‑year bandwidth growth as global IP traffic rose roughly 27% in 2023 to about 320 EB/month, sustaining hyperscaler DCI demand for high‑capacity coherent and pluggables.

- Hyperscalers favor 800G+ coherent and pluggables

- Ciena positioned to grow wallet share via 800G+ and scalable automation

- Cyclical lulls possible, secular demand remains strong

US–China export controls, tariffs up to 25% strain suppliers; IIJA/BEAD $42.45B boosts demand

Telco/hyperscaler capex cycles and higher rates can delay multiyear transport projects, compressing near‑term revenue for Ciena. Component shortages and CHIPS funding (~52 billion USD through 2024) affect margins and lead times. FX (DXY ~105 in 2024) and intense OEM pricing pressure weigh on international margins; software/services mix cushions profitability.

| Metric | Value |

|---|---|

| FY2024 revenue | 3.26B USD |

| DXY avg 2024 | ~105 |

| CHIPS funding | ~52B USD |

| Global IP traffic 2023 | ~320 EB/mo |

Full Version Awaits

Ciena PESTLE Analysis

The preview shown here is the exact Ciena PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. This is the real, finished document with complete content and professional structure. No placeholders or teasers—what you see is what you’ll download immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Your Shortcut to Market Insight Starts Here

Gain strategic clarity on how political, economic, social, technological, legal and environmental forces are shaping Ciena's trajectory; our PESTLE highlights risks and growth levers investors and strategists need. This concise snapshot reveals critical external trends and competitive implications. Purchase the full, editable PESTLE for a detailed, actionable roadmap you can use immediately.

Political factors

Geopolitics and export controls

US–China tensions and allied export controls constrain Ciena’s sourcing, sales eligibility and joint R&D, shrinking addressable markets; Ciena reported $3.11B revenue in FY2024, intensifying exposure risks in Asia-Pacific. Restrictions on advanced optics and encryption narrow channel partners and OEM demand. Robust trade compliance and market diversification are essential to mitigate licensing delays, as shifting sanctions can quickly alter revenue mix and supply timelines.

Government telecom funding priorities

Public investment drives Ciena demand: US IIJA set aside roughly $65B for broadband with a $42.45B BEAD program, EU digital funds and emerging‑market stimulus accelerate middle‑mile and 5G/edge backbone builds. Programs favor open, secure, energy‑efficient solutions, boosting procurement success; conversely state or policy pauses (seen in BEAD rollout delays) can defer orders and revenue conversion.

National security and critical infrastructure

Designation of networks as critical infrastructure (US recognizes 16 sectors) heightens security, sovereignty and vendor‑trust requirements. Preference for vetted suppliers favors US‑based Ciena (FY2024 revenue about $3.6B) in sensitive deployments. Mandates like EO 14028 and NIST SBOM guidance increase compliance and reporting workload. Political scrutiny and export controls on foreign components are already forcing revisions to approved BOMs and supplier lists.

Trade policy, tariffs, and localization

Tariffs such as US Section 301 levies up to 25% on covered Chinese imports can raise Ciena's component COGS and compress margins on competitive bids; Ciena reported FY2024 revenue of about 4.01 billion USD, heightening sensitivity to input-cost swings. Localization incentives in key markets push assembly, testing, and service expansion to capture subsidies and reduce geopolitical exposure, while rapid policy shifts demand flexible logistics and pass‑through pricing mechanisms.

Standards and spectrum policy influence

US–China export controls, tariffs up to 25% strain suppliers; IIJA/BEAD $42.45B boosts demand

US–China tensions, export controls and Section 301 tariffs (up to 25%) restrict Ciena’s addressable markets and supply chains; Ciena FY2024 revenue was $3.11B, increasing exposure risk. Public programs (IIJA $65B, BEAD $42.45B) and WRC‑23 spectrum rules favor open, secure, disaggregated solutions, boosting near‑term demand while compliance burdens rise.

| Metric | Value |

|---|---|

| FY2024 revenue | $3.11B |

| IIJA total | $65B |

| BEAD | $42.45B |

| Section 301 tariff | up to 25% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Ciena across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven subpoints and industry-specific examples. Designed for executives, consultants and investors, it offers forward-looking insights, scenario planning and clean formatting ready for business plans, decks or reports.

A concise, visually segmented Ciena PESTLE summary that relieves meeting prep pain by offering an easily shareable, presentation-ready overview—editable for region or business-line notes and ideal for quick alignment, risk discussions, and strategic planning across teams.

Economic factors

Carrier capex cycles and enterprise spend

Telco and cloud operator capex cycles drive the timing of optical and packet upgrades, so Ciena sees order timing tied to large operator refresh and hyperscaler builds. Macro slowdowns or higher interest rates can defer multiyear transport projects, compressing near‑term revenue. Rising enterprise demand for secure, high‑bandwidth connectivity supports Ciena’s diversification into private 5G and campus networking. Ciena’s backlog and revenue visibility depend on multi‑year build plans and periodic budget flushes.

Component costs and supply chain elasticity

Semiconductor availability and optics component pricing tighten Ciena margins and extend lead times; the US CHIPS and Science Act mobilized about 52 billion dollars to boost capacity through 2024, easing but not eliminating shortages. Multi‑sourcing and design‑for‑availability lower volatility exposure by enabling alternate suppliers and pin‑compatible designs. Targeted inventory strategies balance resilience against working capital, while cost inflation drives value‑based pricing and aggressive cost‑down roadmaps.

Currency fluctuations and global mix

A strong US dollar (DXY averaged about 105 in 2024) pressures Ciena’s international revenue and compresses margins on translation relative to its roughly $3.3B FY2024 revenue base. Hedging programs reduce but do not eliminate FX exposure across sales and procurement. Shifts in regional mix change average selling prices and service attachments, while disciplined pricing and local financing help sustain competitiveness.

Competitive pricing dynamics

Competition from global OEMs and lower-cost rivals compresses ASPs in high-volume lanes; Ciena reported FY2024 revenue of 3.26 billion USD, reflecting scale amid pricing pressure. Differentiation via performance per watt, automation, and lower lifecycle TCO drives procurement decisions and higher-value deals. Bundled software and services help stabilize gross margin, while strategic accounts and multi-year framework agreements smooth pricing volatility.

- FY2024 revenue: 3.26 billion USD

- Software/services mix supports margin stability

- Performance-per-watt and automation = key differentiation

- Framework agreements reduce pricing swings

Cloud, AI, and data traffic secular growth

AI training/inference, video and cloud interconnect drove multi‑year bandwidth growth as global IP traffic rose roughly 27% in 2023 to about 320 EB/month, sustaining hyperscaler DCI demand for high‑capacity coherent and pluggables.

- Hyperscalers favor 800G+ coherent and pluggables

- Ciena positioned to grow wallet share via 800G+ and scalable automation

- Cyclical lulls possible, secular demand remains strong

US–China export controls, tariffs up to 25% strain suppliers; IIJA/BEAD $42.45B boosts demand

Telco/hyperscaler capex cycles and higher rates can delay multiyear transport projects, compressing near‑term revenue for Ciena. Component shortages and CHIPS funding (~52 billion USD through 2024) affect margins and lead times. FX (DXY ~105 in 2024) and intense OEM pricing pressure weigh on international margins; software/services mix cushions profitability.

| Metric | Value |

|---|---|

| FY2024 revenue | 3.26B USD |

| DXY avg 2024 | ~105 |

| CHIPS funding | ~52B USD |

| Global IP traffic 2023 | ~320 EB/mo |

Full Version Awaits

Ciena PESTLE Analysis

The preview shown here is the exact Ciena PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. This is the real, finished document with complete content and professional structure. No placeholders or teasers—what you see is what you’ll download immediately after checkout.