CIMB Group Holdings Porter's Five Forces Analysis

Don't Miss the Bigger Picture

CIMB Group Holdings faces intense competitive rivalry, evolving buyer power, and regulatory-driven barriers that shape profitability, while supplier influence and substitute financial services add strategic pressure. This snapshot highlights key forces but omits force-by-force ratings, visuals, and financial implications. Unlock the full Porter's Five Forces Analysis for a consultant-grade breakdown, Excel/Word deliverables, and actionable insights to inform investment and strategy.

Suppliers Bargaining Power

Concentrated tech and infrastructure vendors

Core banking, cloud, cybersecurity and payments rails are supplied by a concentrated set of global vendors—cloud market shares in 2024: AWS 32%, Microsoft Azure 23%, Google Cloud 11%—giving suppliers pricing and contractual leverage.

Switching core systems is costly and risky, increasing dependency, though CIMB’s regional scale enables multi-vendor strategies and stronger negotiation leverage.

Long-term partnerships can secure volume discounts and co-innovation aligned with bank priorities.

Wholesale funding and interbank providers

CIMB relies on wholesale markets for liquidity and capital flexibility, particularly in wholesale banking, which raises supplier power when funding costs spike in stressed conditions. A strong CASA deposit base and diversified currency access mitigate reliance on interbank providers. Regulatory liquidity buffers—LCR and NSFR mandated at >=100%—reduce vulnerability to market swings.

Talent and specialized skills

Quant, risk, tech, Shariah advisory and ESG specialists remain scarce across ASEAN, with LinkedIn reporting fintech-related skill demand in Southeast Asia up around 40% year-on-year in 2024, giving suppliers clear bargaining power. Wage inflation and poaching by fintechs and global banks have pushed specialist compensation higher, creating notable cost pressure on margins. CIMB’s regional platform, cross-border career mobility and internal rotations help attract and retain specialists. Continuous upskilling programs and targeted employer branding are critical levers to reduce turnover and supplier leverage.

Data, credit bureaus, and payment networks

Access to credit bureaus, alternative data and card/payment schemes is essential for CIMB’s risk models and product economics, with interchange and scheme fees typically ranging 0.1–3% which can materially affect margins. Fee structures and restrictive data licensing raise supplier influence, though CIMB can leverage portfolio scale and route volumes to lower-cost rails. Ongoing open banking and national payment rails are gradually rebalancing power.

- Scale bargaining: route volume to lower-cost networks

- Fee pressure: interchange 0.1–3%

- Data terms: licensing rigidity vs open banking progress

Regulatory capital and compliance inputs

Regulatory capital requirements act as non-negotiable inputs: Basel III mandates a CET1 minimum of 4.5% plus a 2.5% conservation buffer (total 7.0%), making regtech and KYC vendors strategically important and giving them pricing leverage. CIMB mitigates this through shared compliance utilities, automation and strong governance to reduce ad hoc spend and limit vendor lock-in.

Cloud/regtech suppliers gain pricing power; AWS 32%, SEA talent +40%

Suppliers wield moderate-to-high power: cloud (AWS 32%, Azure 23%, GCP 11% in 2024), regtech/KYC and data vendors command pricing and contract leverage, and specialist tech talent demand in SEA rose ~40% y/y in 2024, pressuring wages. CIMB offsets via regional scale, multi-vendor routing, CASA strength and shared compliance utilities; regulatory buffers (LCR/NSFR ≥100%, CET1 ≥7.0%) reduce liquidity supplier risk.

| Metric | Value |

|---|---|

| AWS share (2024) | 32% |

| Interchange fees | 0.1–3% |

| Specialist demand SEA (2024) | +40% y/y |

| CET1 requirement | ≥7.0% |

What is included in the product

Tailored Porter's Five Forces analysis of CIMB Group Holdings uncovering competitive drivers, buyer and supplier influence, entry barriers, substitutes and disruptive threats to its market position. Ideal for strategic planning and investor materials.

A concise Porter's Five Forces one-sheet for CIMB Group — quickly reveals competitive pressures and strategic levers to ease executive decision-making. Swap in current data to model impacts of regulation, new entrants or market shifts and instantly turn insights into board-ready slides.

Customers Bargaining Power

Price-sensitive retail customers

Price-sensitive retail customers compare rates, fees and rewards across banks and fintechs, driving pricing pressure; digital channels have lowered switching costs and raised expectations. CIMB counters with bundled products, loyalty ecosystems and a competitive CASA ratio (32.4% in 2024) to protect margins. Enhanced UX and convenience via mobile and omnichannel services help dampen pure price competition.

SMEs demand tailored credit and cash management

SMEs increasingly demand flexible lending, fast onboarding and integrated payments, giving them negotiation leverage as many maintain relationships with 2–3 banks to optimize pricing and limits. CIMB’s SME platforms and relationship managers can create stickiness via advisory and ecosystem tools, while data-driven underwriting in 2024 has cut time-to-cash from weeks to days for many clients, improving retention.

Large corporates and institutions

Large corporates run competitive RFPs and mandate syndicates that compress fees, while cross-border treasury, trade and DCM needs push them toward banks with regional reach. CIMB’s ASEAN network across 15 countries and full-service Islamic banking (CIMB Islamic since 2003) strengthens its negotiating position. Combining balance-sheet capacity with advisory services deepens share of wallet and helps retain mandates.

Affluent and wealth clients

Affluent clients haggle over pricing, product access and service tiers and will migrate to global private banks if perceived value falls; CIMB counters with differentiated Shariah-compliant wealth offerings, structured solutions and omnichannel advisory to retain clients.

- Focus: Shariah-compliant wealth

- Retention: bespoke portfolios & performance reporting

- Risk: migration to global private banks

Digital-first expectations

Customers now expect instant, 24/7, low-friction services with super-apps as the benchmark, and poor UX quickly triggers switching; CIMB’s investments in mobile, APIs and personalization have measurably reduced buyer power by raising satisfaction and retention. Continuous CX iteration remains necessary to sustain this advantage as competitors emulate digital features and lower switching costs.

- Digital-first expectations

- Low-friction service = higher retention

- CIMB mobile/API investments reduce buyer power

- Ongoing CX iteration required

Retail price pressure, faster SME lending, ASEAN reach and CX drive 2024 banking outcomes

Price-sensitive retail customers force pricing pressure; CIMB defends with bundled products, loyalty and a CASA ratio of 32.4% in 2024.

SMEs demand fast, flexible lending; CIMB’s SME platforms cut time-to-cash from weeks to days in 2024, improving retention.

Large corporates run competitive RFPs; CIMB’s ASEAN network across 15 countries and Islamic banking strengthen mandates.

Digital-first expectations mean CX and APIs remain critical to limit buyer power.

| Segment | Metric (2024) |

|---|---|

| Retail | CASA 32.4% |

| SME | Time-to-cash: weeks→days |

| Corporate | ASEAN network: 15 countries |

Preview Before You Purchase

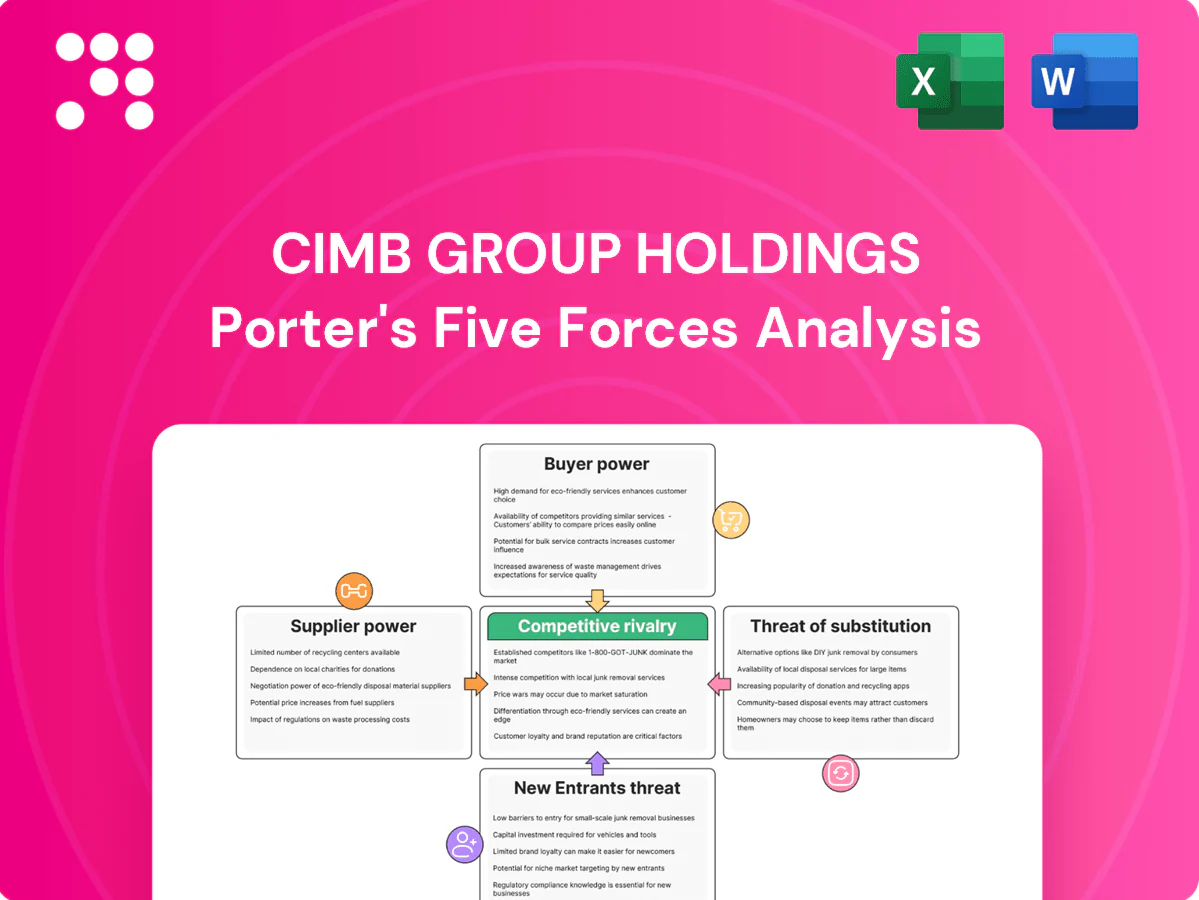

CIMB Group Holdings Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of CIMB Group Holdings you'll receive—fully formatted and ready for use. It covers competitive rivalry, supplier and buyer power, and the threats of new entrants and substitutes with data-driven insights and strategic implications. No placeholders or mockups; completing your purchase grants immediate access to this identical file.

Don't Miss the Bigger Picture

CIMB Group Holdings faces intense competitive rivalry, evolving buyer power, and regulatory-driven barriers that shape profitability, while supplier influence and substitute financial services add strategic pressure. This snapshot highlights key forces but omits force-by-force ratings, visuals, and financial implications. Unlock the full Porter's Five Forces Analysis for a consultant-grade breakdown, Excel/Word deliverables, and actionable insights to inform investment and strategy.

Suppliers Bargaining Power

Concentrated tech and infrastructure vendors

Core banking, cloud, cybersecurity and payments rails are supplied by a concentrated set of global vendors—cloud market shares in 2024: AWS 32%, Microsoft Azure 23%, Google Cloud 11%—giving suppliers pricing and contractual leverage.

Switching core systems is costly and risky, increasing dependency, though CIMB’s regional scale enables multi-vendor strategies and stronger negotiation leverage.

Long-term partnerships can secure volume discounts and co-innovation aligned with bank priorities.

Wholesale funding and interbank providers

CIMB relies on wholesale markets for liquidity and capital flexibility, particularly in wholesale banking, which raises supplier power when funding costs spike in stressed conditions. A strong CASA deposit base and diversified currency access mitigate reliance on interbank providers. Regulatory liquidity buffers—LCR and NSFR mandated at >=100%—reduce vulnerability to market swings.

Talent and specialized skills

Quant, risk, tech, Shariah advisory and ESG specialists remain scarce across ASEAN, with LinkedIn reporting fintech-related skill demand in Southeast Asia up around 40% year-on-year in 2024, giving suppliers clear bargaining power. Wage inflation and poaching by fintechs and global banks have pushed specialist compensation higher, creating notable cost pressure on margins. CIMB’s regional platform, cross-border career mobility and internal rotations help attract and retain specialists. Continuous upskilling programs and targeted employer branding are critical levers to reduce turnover and supplier leverage.

Data, credit bureaus, and payment networks

Access to credit bureaus, alternative data and card/payment schemes is essential for CIMB’s risk models and product economics, with interchange and scheme fees typically ranging 0.1–3% which can materially affect margins. Fee structures and restrictive data licensing raise supplier influence, though CIMB can leverage portfolio scale and route volumes to lower-cost rails. Ongoing open banking and national payment rails are gradually rebalancing power.

- Scale bargaining: route volume to lower-cost networks

- Fee pressure: interchange 0.1–3%

- Data terms: licensing rigidity vs open banking progress

Regulatory capital and compliance inputs

Regulatory capital requirements act as non-negotiable inputs: Basel III mandates a CET1 minimum of 4.5% plus a 2.5% conservation buffer (total 7.0%), making regtech and KYC vendors strategically important and giving them pricing leverage. CIMB mitigates this through shared compliance utilities, automation and strong governance to reduce ad hoc spend and limit vendor lock-in.

Cloud/regtech suppliers gain pricing power; AWS 32%, SEA talent +40%

Suppliers wield moderate-to-high power: cloud (AWS 32%, Azure 23%, GCP 11% in 2024), regtech/KYC and data vendors command pricing and contract leverage, and specialist tech talent demand in SEA rose ~40% y/y in 2024, pressuring wages. CIMB offsets via regional scale, multi-vendor routing, CASA strength and shared compliance utilities; regulatory buffers (LCR/NSFR ≥100%, CET1 ≥7.0%) reduce liquidity supplier risk.

| Metric | Value |

|---|---|

| AWS share (2024) | 32% |

| Interchange fees | 0.1–3% |

| Specialist demand SEA (2024) | +40% y/y |

| CET1 requirement | ≥7.0% |

What is included in the product

Tailored Porter's Five Forces analysis of CIMB Group Holdings uncovering competitive drivers, buyer and supplier influence, entry barriers, substitutes and disruptive threats to its market position. Ideal for strategic planning and investor materials.

A concise Porter's Five Forces one-sheet for CIMB Group — quickly reveals competitive pressures and strategic levers to ease executive decision-making. Swap in current data to model impacts of regulation, new entrants or market shifts and instantly turn insights into board-ready slides.

Customers Bargaining Power

Price-sensitive retail customers

Price-sensitive retail customers compare rates, fees and rewards across banks and fintechs, driving pricing pressure; digital channels have lowered switching costs and raised expectations. CIMB counters with bundled products, loyalty ecosystems and a competitive CASA ratio (32.4% in 2024) to protect margins. Enhanced UX and convenience via mobile and omnichannel services help dampen pure price competition.

SMEs demand tailored credit and cash management

SMEs increasingly demand flexible lending, fast onboarding and integrated payments, giving them negotiation leverage as many maintain relationships with 2–3 banks to optimize pricing and limits. CIMB’s SME platforms and relationship managers can create stickiness via advisory and ecosystem tools, while data-driven underwriting in 2024 has cut time-to-cash from weeks to days for many clients, improving retention.

Large corporates and institutions

Large corporates run competitive RFPs and mandate syndicates that compress fees, while cross-border treasury, trade and DCM needs push them toward banks with regional reach. CIMB’s ASEAN network across 15 countries and full-service Islamic banking (CIMB Islamic since 2003) strengthens its negotiating position. Combining balance-sheet capacity with advisory services deepens share of wallet and helps retain mandates.

Affluent and wealth clients

Affluent clients haggle over pricing, product access and service tiers and will migrate to global private banks if perceived value falls; CIMB counters with differentiated Shariah-compliant wealth offerings, structured solutions and omnichannel advisory to retain clients.

- Focus: Shariah-compliant wealth

- Retention: bespoke portfolios & performance reporting

- Risk: migration to global private banks

Digital-first expectations

Customers now expect instant, 24/7, low-friction services with super-apps as the benchmark, and poor UX quickly triggers switching; CIMB’s investments in mobile, APIs and personalization have measurably reduced buyer power by raising satisfaction and retention. Continuous CX iteration remains necessary to sustain this advantage as competitors emulate digital features and lower switching costs.

- Digital-first expectations

- Low-friction service = higher retention

- CIMB mobile/API investments reduce buyer power

- Ongoing CX iteration required

Retail price pressure, faster SME lending, ASEAN reach and CX drive 2024 banking outcomes

Price-sensitive retail customers force pricing pressure; CIMB defends with bundled products, loyalty and a CASA ratio of 32.4% in 2024.

SMEs demand fast, flexible lending; CIMB’s SME platforms cut time-to-cash from weeks to days in 2024, improving retention.

Large corporates run competitive RFPs; CIMB’s ASEAN network across 15 countries and Islamic banking strengthen mandates.

Digital-first expectations mean CX and APIs remain critical to limit buyer power.

| Segment | Metric (2024) |

|---|---|

| Retail | CASA 32.4% |

| SME | Time-to-cash: weeks→days |

| Corporate | ASEAN network: 15 countries |

Preview Before You Purchase

CIMB Group Holdings Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of CIMB Group Holdings you'll receive—fully formatted and ready for use. It covers competitive rivalry, supplier and buyer power, and the threats of new entrants and substitutes with data-driven insights and strategic implications. No placeholders or mockups; completing your purchase grants immediate access to this identical file.

Description

Don't Miss the Bigger Picture

CIMB Group Holdings faces intense competitive rivalry, evolving buyer power, and regulatory-driven barriers that shape profitability, while supplier influence and substitute financial services add strategic pressure. This snapshot highlights key forces but omits force-by-force ratings, visuals, and financial implications. Unlock the full Porter's Five Forces Analysis for a consultant-grade breakdown, Excel/Word deliverables, and actionable insights to inform investment and strategy.

Suppliers Bargaining Power

Concentrated tech and infrastructure vendors

Core banking, cloud, cybersecurity and payments rails are supplied by a concentrated set of global vendors—cloud market shares in 2024: AWS 32%, Microsoft Azure 23%, Google Cloud 11%—giving suppliers pricing and contractual leverage.

Switching core systems is costly and risky, increasing dependency, though CIMB’s regional scale enables multi-vendor strategies and stronger negotiation leverage.

Long-term partnerships can secure volume discounts and co-innovation aligned with bank priorities.

Wholesale funding and interbank providers

CIMB relies on wholesale markets for liquidity and capital flexibility, particularly in wholesale banking, which raises supplier power when funding costs spike in stressed conditions. A strong CASA deposit base and diversified currency access mitigate reliance on interbank providers. Regulatory liquidity buffers—LCR and NSFR mandated at >=100%—reduce vulnerability to market swings.

Talent and specialized skills

Quant, risk, tech, Shariah advisory and ESG specialists remain scarce across ASEAN, with LinkedIn reporting fintech-related skill demand in Southeast Asia up around 40% year-on-year in 2024, giving suppliers clear bargaining power. Wage inflation and poaching by fintechs and global banks have pushed specialist compensation higher, creating notable cost pressure on margins. CIMB’s regional platform, cross-border career mobility and internal rotations help attract and retain specialists. Continuous upskilling programs and targeted employer branding are critical levers to reduce turnover and supplier leverage.

Data, credit bureaus, and payment networks

Access to credit bureaus, alternative data and card/payment schemes is essential for CIMB’s risk models and product economics, with interchange and scheme fees typically ranging 0.1–3% which can materially affect margins. Fee structures and restrictive data licensing raise supplier influence, though CIMB can leverage portfolio scale and route volumes to lower-cost rails. Ongoing open banking and national payment rails are gradually rebalancing power.

- Scale bargaining: route volume to lower-cost networks

- Fee pressure: interchange 0.1–3%

- Data terms: licensing rigidity vs open banking progress

Regulatory capital and compliance inputs

Regulatory capital requirements act as non-negotiable inputs: Basel III mandates a CET1 minimum of 4.5% plus a 2.5% conservation buffer (total 7.0%), making regtech and KYC vendors strategically important and giving them pricing leverage. CIMB mitigates this through shared compliance utilities, automation and strong governance to reduce ad hoc spend and limit vendor lock-in.

Cloud/regtech suppliers gain pricing power; AWS 32%, SEA talent +40%

Suppliers wield moderate-to-high power: cloud (AWS 32%, Azure 23%, GCP 11% in 2024), regtech/KYC and data vendors command pricing and contract leverage, and specialist tech talent demand in SEA rose ~40% y/y in 2024, pressuring wages. CIMB offsets via regional scale, multi-vendor routing, CASA strength and shared compliance utilities; regulatory buffers (LCR/NSFR ≥100%, CET1 ≥7.0%) reduce liquidity supplier risk.

| Metric | Value |

|---|---|

| AWS share (2024) | 32% |

| Interchange fees | 0.1–3% |

| Specialist demand SEA (2024) | +40% y/y |

| CET1 requirement | ≥7.0% |

What is included in the product

Tailored Porter's Five Forces analysis of CIMB Group Holdings uncovering competitive drivers, buyer and supplier influence, entry barriers, substitutes and disruptive threats to its market position. Ideal for strategic planning and investor materials.

A concise Porter's Five Forces one-sheet for CIMB Group — quickly reveals competitive pressures and strategic levers to ease executive decision-making. Swap in current data to model impacts of regulation, new entrants or market shifts and instantly turn insights into board-ready slides.

Customers Bargaining Power

Price-sensitive retail customers

Price-sensitive retail customers compare rates, fees and rewards across banks and fintechs, driving pricing pressure; digital channels have lowered switching costs and raised expectations. CIMB counters with bundled products, loyalty ecosystems and a competitive CASA ratio (32.4% in 2024) to protect margins. Enhanced UX and convenience via mobile and omnichannel services help dampen pure price competition.

SMEs demand tailored credit and cash management

SMEs increasingly demand flexible lending, fast onboarding and integrated payments, giving them negotiation leverage as many maintain relationships with 2–3 banks to optimize pricing and limits. CIMB’s SME platforms and relationship managers can create stickiness via advisory and ecosystem tools, while data-driven underwriting in 2024 has cut time-to-cash from weeks to days for many clients, improving retention.

Large corporates and institutions

Large corporates run competitive RFPs and mandate syndicates that compress fees, while cross-border treasury, trade and DCM needs push them toward banks with regional reach. CIMB’s ASEAN network across 15 countries and full-service Islamic banking (CIMB Islamic since 2003) strengthens its negotiating position. Combining balance-sheet capacity with advisory services deepens share of wallet and helps retain mandates.

Affluent and wealth clients

Affluent clients haggle over pricing, product access and service tiers and will migrate to global private banks if perceived value falls; CIMB counters with differentiated Shariah-compliant wealth offerings, structured solutions and omnichannel advisory to retain clients.

- Focus: Shariah-compliant wealth

- Retention: bespoke portfolios & performance reporting

- Risk: migration to global private banks

Digital-first expectations

Customers now expect instant, 24/7, low-friction services with super-apps as the benchmark, and poor UX quickly triggers switching; CIMB’s investments in mobile, APIs and personalization have measurably reduced buyer power by raising satisfaction and retention. Continuous CX iteration remains necessary to sustain this advantage as competitors emulate digital features and lower switching costs.

- Digital-first expectations

- Low-friction service = higher retention

- CIMB mobile/API investments reduce buyer power

- Ongoing CX iteration required

Retail price pressure, faster SME lending, ASEAN reach and CX drive 2024 banking outcomes

Price-sensitive retail customers force pricing pressure; CIMB defends with bundled products, loyalty and a CASA ratio of 32.4% in 2024.

SMEs demand fast, flexible lending; CIMB’s SME platforms cut time-to-cash from weeks to days in 2024, improving retention.

Large corporates run competitive RFPs; CIMB’s ASEAN network across 15 countries and Islamic banking strengthen mandates.

Digital-first expectations mean CX and APIs remain critical to limit buyer power.

| Segment | Metric (2024) |

|---|---|

| Retail | CASA 32.4% |

| SME | Time-to-cash: weeks→days |

| Corporate | ASEAN network: 15 countries |

Preview Before You Purchase

CIMB Group Holdings Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of CIMB Group Holdings you'll receive—fully formatted and ready for use. It covers competitive rivalry, supplier and buyer power, and the threats of new entrants and substitutes with data-driven insights and strategic implications. No placeholders or mockups; completing your purchase grants immediate access to this identical file.