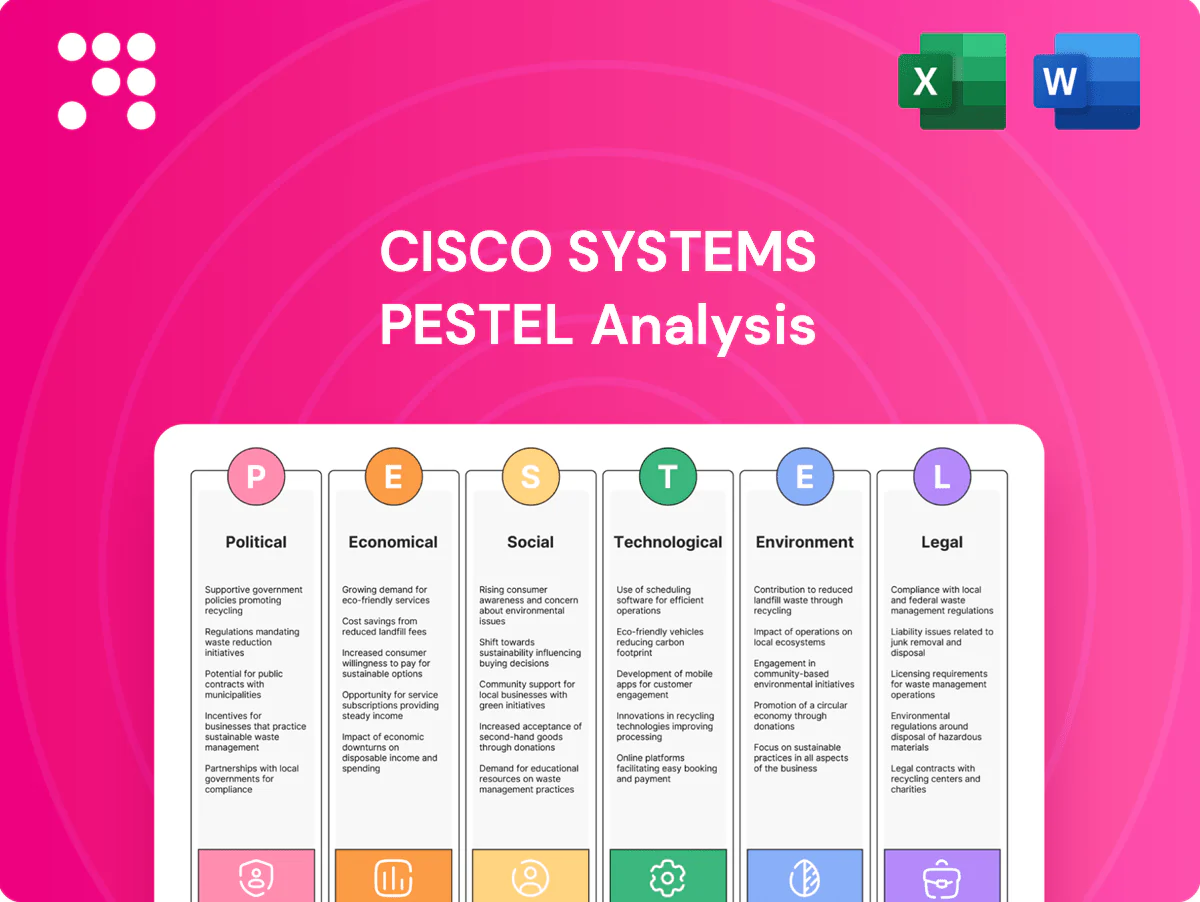

Cisco Systems PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Uncover how political shifts, economic cycles, and rapid tech innovation are reshaping Cisco Systems with our concise PESTLE snapshot—perfect for investors and strategists. Gain actionable insight to de-risk decisions and spot growth vectors. Purchase the full PESTLE for the complete, ready-to-use analysis now.

Political factors

Geopolitics and export controls

US–China tensions and stepped-up export controls (notably Oct 2022 and subsequent 2023–24 measures on advanced chips and encryption) constrain Cisco’s market access for high-end networking and security gear. Restrictions on certain semiconductors and crypto tech force shipment delays and product redesigns, raising lead times and costs. Cisco, with FY2024 revenue of about $60.8B, must segment product roadmaps and supply lines by jurisdiction, affecting pricing and competitive dynamics.

Public sector procurement

Public sector procurement drives demand for secure networking, cloud connectivity and zero-trust, aligning with Cisco’s offerings as governments increase IT modernization; Cisco reported fiscal 2024 revenue of about $57.8 billion, with public sector a material vertical. Multi-year government contracts offer revenue visibility but necessitate strict compliance and certifications. Fiscal cycles and elections shift priorities, while defense, critical infrastructure and education remain strategic buys.

Localization and national champions

Many governments push local manufacturing, data residency and national tech champions, with over 50 countries having data-localization measures by 2024; Cisco, which reported $58.3B revenue in FY2024, may need JVs, local partners or in-country assembly to win tenders. Preference policies can tilt procurement toward domestic vendors, raising implementation costs but opening protected markets.

Sanctions and entity lists

Sanctions regimes can abruptly bar sales to named entities or regions, forcing Cisco to reroute business and comply with export controls; OFAC civil penalties can reach roughly 336,922 USD per violation, with criminal exposure higher. Effective compliance requires customer screening, license management and auditable controls; breaches risk heavy fines and reputational damage. Product portfolio mix and channel policies must be rapidly adjusted to remain compliant and preserve revenue.

- Immediate sales restrictions to listed entities

- Mandatory screening & license workflows

- Audit trails to avoid ~336,922 USD penalties

- Rapid channel/portfolio reconfiguration

Standards and multilateral bodies

Cisco is an active contributor to IETF, IEEE and 3GPP, influencing interoperability and adoption; IETF had over 9,000 RFCs by 2024 and 3GPP Release 18 (5G‑Advanced) work was ongoing in 2024–25, affecting product roadmaps. Fragmentation of standards across geopolitical blocs raises engineering complexity, while standards leadership preserves backward compatibility and market access and can yield de facto advantages.

- Interoperability: IETF/IEEE/3GPP influence

- Complexity: fragmentation across blocs

- Access: standards participation protects market entry

- Advantage: leadership creates de facto market benefits

Export controls, localization & standards reshape secure networking supply chains

US–China export controls (2022–24) limit high-end sales, forcing redesigns and segmented supply chains; Cisco FY2024 revenue ≈ $58.3B. Governments drive secure networking demand via multi-year contracts but require localization and compliance amid >50 data‑localization laws by 2024. Sanctions/OFAC risk (~336,922 USD civil penalty per violation) mandate strict screening. Standards role (IETF >9,000 RFCs; 3GPP R18 ongoing) shapes roadmaps.

| Metric | Value |

|---|---|

| FY2024 revenue | $58.3B |

| Data‑localization laws (by 2024) | >50 countries |

| OFAC civil penalty (approx) | $336,922 |

| IETF RFCs (by 2024) | >9,000 |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely affect Cisco Systems, with data-backed trends and regional industry context; designed to reveal threats and opportunities for executives, consultants, and investors and to support scenario planning, strategy design, and inclusion in business plans or investor materials.

Relieves meeting-prep pain by providing a concise, visually segmented Cisco PESTLE summary that highlights external risks and opportunities, is editable for regional or business-line notes, and can be dropped into presentations or shared across teams for quick alignment.

Economic factors

IT spending cycles

Enterprise capex and opex shift with macro growth, inflation and confidence—hardware refreshes are often deferred in downturns while security and cloud connectivity stay more resilient. Cisco’s recurring software and services, exceeding $20B in FY2024, help smooth revenue volatility; a vertical mix across service providers, public sector and cloud customers diversifies demand.

Interest rates and financing

Higher interest rates — US federal funds at about 5.25–5.50% in mid‑2025 — raise the total cost of ownership for financed Cisco deals and squeeze partner working capital, slowing deal flow. Customer purchase decision cycles lengthen as corporate hurdle rates rise, delaying refreshes and cloud migrations. Cisco Capital can unlock sales by offering financing but increases Cisco’s credit exposure; subsequent rate cuts have historically unlocked deferred projects and upgrades.

FX and global footprint

A strong US dollar (DXY near 106 in mid-2025) compresses Cisco’s international revenue translation and forces tougher local pricing in key markets. Hedging programs reduce reported volatility but do not restore bid competitiveness in local-currency tenders. Local pricing, channel incentives and promotions are used to soften demand elasticity. Supply and service costs also rise when currencies weaken versus the dollar.

Supply chain and components

Semiconductor availability and logistics costs materially affect Ciscos bookings-to-revenue conversion; industry semiconductor lead times averaged about 20 weeks in 2024, extending conversion cycles. Diversified sourcing and design-for-availability have reduced node-specific disruption and improved fulfillment resilience. Inventory optimization balances demand uncertainty with delivery SLAs while cost inflation pressures margins and forces selective list-price increases.

- Semiconductor lead times: ~20 weeks (2024)

- Diversified sourcing lowers single-vendor risk

- Inventory optimization aligns safety stock with SLAs

- Cost inflation compresses gross margins, prompting pricing actions

Cloud and subscription mix

Cisco's shift to cloud and subscription offerings alters revenue recognition and compresses near-term product margins while boosting recurring revenue visibility, requiring a land-and-expand sales motion to drive renewals and upsells across security, observability, and collaboration bundles that raise ARPU.

- Recurring revenue improves predictability and valuation multiples

- Bundles increase ARPU and customer stickiness

- Land-and-expand is critical for growth

- Partner comp must shift to subscription economics

Export controls, localization & standards reshape secure networking supply chains

Enterprise capex sensitivity, higher rates (Fed funds ~5.25–5.50% mid‑2025) and strong dollar (DXY ~106) compress international revenues; recurring software/services (>20B FY2024) smooth volatility. Semiconductor lead times (~20 weeks in 2024) and rising logistics inflate costs and delay bookings-to-revenue. Cisco Capital offsets some cycle weakness but raises credit exposure.

| Metric | Value |

|---|---|

| FY2024 recurring rev | >$20B |

| Total rev FY2024 | $57.6B |

| Fed funds (mid‑2025) | 5.25–5.50% |

| DXY (mid‑2025) | ~106 |

| Semiconductor lead times (2024) | ~20 wks |

Preview the Actual Deliverable

Cisco Systems PESTLE Analysis

This Cisco Systems PESTLE Analysis preview is the exact, fully formatted document you’ll receive after purchase—no placeholders or surprises. The content, structure, and layout shown here are identical to the downloadable file delivered immediately upon payment. Use it as-is for strategic planning, presentations, or research.

Make Smarter Strategic Decisions with a Complete PESTEL View

Uncover how political shifts, economic cycles, and rapid tech innovation are reshaping Cisco Systems with our concise PESTLE snapshot—perfect for investors and strategists. Gain actionable insight to de-risk decisions and spot growth vectors. Purchase the full PESTLE for the complete, ready-to-use analysis now.

Political factors

Geopolitics and export controls

US–China tensions and stepped-up export controls (notably Oct 2022 and subsequent 2023–24 measures on advanced chips and encryption) constrain Cisco’s market access for high-end networking and security gear. Restrictions on certain semiconductors and crypto tech force shipment delays and product redesigns, raising lead times and costs. Cisco, with FY2024 revenue of about $60.8B, must segment product roadmaps and supply lines by jurisdiction, affecting pricing and competitive dynamics.

Public sector procurement

Public sector procurement drives demand for secure networking, cloud connectivity and zero-trust, aligning with Cisco’s offerings as governments increase IT modernization; Cisco reported fiscal 2024 revenue of about $57.8 billion, with public sector a material vertical. Multi-year government contracts offer revenue visibility but necessitate strict compliance and certifications. Fiscal cycles and elections shift priorities, while defense, critical infrastructure and education remain strategic buys.

Localization and national champions

Many governments push local manufacturing, data residency and national tech champions, with over 50 countries having data-localization measures by 2024; Cisco, which reported $58.3B revenue in FY2024, may need JVs, local partners or in-country assembly to win tenders. Preference policies can tilt procurement toward domestic vendors, raising implementation costs but opening protected markets.

Sanctions and entity lists

Sanctions regimes can abruptly bar sales to named entities or regions, forcing Cisco to reroute business and comply with export controls; OFAC civil penalties can reach roughly 336,922 USD per violation, with criminal exposure higher. Effective compliance requires customer screening, license management and auditable controls; breaches risk heavy fines and reputational damage. Product portfolio mix and channel policies must be rapidly adjusted to remain compliant and preserve revenue.

- Immediate sales restrictions to listed entities

- Mandatory screening & license workflows

- Audit trails to avoid ~336,922 USD penalties

- Rapid channel/portfolio reconfiguration

Standards and multilateral bodies

Cisco is an active contributor to IETF, IEEE and 3GPP, influencing interoperability and adoption; IETF had over 9,000 RFCs by 2024 and 3GPP Release 18 (5G‑Advanced) work was ongoing in 2024–25, affecting product roadmaps. Fragmentation of standards across geopolitical blocs raises engineering complexity, while standards leadership preserves backward compatibility and market access and can yield de facto advantages.

- Interoperability: IETF/IEEE/3GPP influence

- Complexity: fragmentation across blocs

- Access: standards participation protects market entry

- Advantage: leadership creates de facto market benefits

Export controls, localization & standards reshape secure networking supply chains

US–China export controls (2022–24) limit high-end sales, forcing redesigns and segmented supply chains; Cisco FY2024 revenue ≈ $58.3B. Governments drive secure networking demand via multi-year contracts but require localization and compliance amid >50 data‑localization laws by 2024. Sanctions/OFAC risk (~336,922 USD civil penalty per violation) mandate strict screening. Standards role (IETF >9,000 RFCs; 3GPP R18 ongoing) shapes roadmaps.

| Metric | Value |

|---|---|

| FY2024 revenue | $58.3B |

| Data‑localization laws (by 2024) | >50 countries |

| OFAC civil penalty (approx) | $336,922 |

| IETF RFCs (by 2024) | >9,000 |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely affect Cisco Systems, with data-backed trends and regional industry context; designed to reveal threats and opportunities for executives, consultants, and investors and to support scenario planning, strategy design, and inclusion in business plans or investor materials.

Relieves meeting-prep pain by providing a concise, visually segmented Cisco PESTLE summary that highlights external risks and opportunities, is editable for regional or business-line notes, and can be dropped into presentations or shared across teams for quick alignment.

Economic factors

IT spending cycles

Enterprise capex and opex shift with macro growth, inflation and confidence—hardware refreshes are often deferred in downturns while security and cloud connectivity stay more resilient. Cisco’s recurring software and services, exceeding $20B in FY2024, help smooth revenue volatility; a vertical mix across service providers, public sector and cloud customers diversifies demand.

Interest rates and financing

Higher interest rates — US federal funds at about 5.25–5.50% in mid‑2025 — raise the total cost of ownership for financed Cisco deals and squeeze partner working capital, slowing deal flow. Customer purchase decision cycles lengthen as corporate hurdle rates rise, delaying refreshes and cloud migrations. Cisco Capital can unlock sales by offering financing but increases Cisco’s credit exposure; subsequent rate cuts have historically unlocked deferred projects and upgrades.

FX and global footprint

A strong US dollar (DXY near 106 in mid-2025) compresses Cisco’s international revenue translation and forces tougher local pricing in key markets. Hedging programs reduce reported volatility but do not restore bid competitiveness in local-currency tenders. Local pricing, channel incentives and promotions are used to soften demand elasticity. Supply and service costs also rise when currencies weaken versus the dollar.

Supply chain and components

Semiconductor availability and logistics costs materially affect Ciscos bookings-to-revenue conversion; industry semiconductor lead times averaged about 20 weeks in 2024, extending conversion cycles. Diversified sourcing and design-for-availability have reduced node-specific disruption and improved fulfillment resilience. Inventory optimization balances demand uncertainty with delivery SLAs while cost inflation pressures margins and forces selective list-price increases.

- Semiconductor lead times: ~20 weeks (2024)

- Diversified sourcing lowers single-vendor risk

- Inventory optimization aligns safety stock with SLAs

- Cost inflation compresses gross margins, prompting pricing actions

Cloud and subscription mix

Cisco's shift to cloud and subscription offerings alters revenue recognition and compresses near-term product margins while boosting recurring revenue visibility, requiring a land-and-expand sales motion to drive renewals and upsells across security, observability, and collaboration bundles that raise ARPU.

- Recurring revenue improves predictability and valuation multiples

- Bundles increase ARPU and customer stickiness

- Land-and-expand is critical for growth

- Partner comp must shift to subscription economics

Export controls, localization & standards reshape secure networking supply chains

Enterprise capex sensitivity, higher rates (Fed funds ~5.25–5.50% mid‑2025) and strong dollar (DXY ~106) compress international revenues; recurring software/services (>20B FY2024) smooth volatility. Semiconductor lead times (~20 weeks in 2024) and rising logistics inflate costs and delay bookings-to-revenue. Cisco Capital offsets some cycle weakness but raises credit exposure.

| Metric | Value |

|---|---|

| FY2024 recurring rev | >$20B |

| Total rev FY2024 | $57.6B |

| Fed funds (mid‑2025) | 5.25–5.50% |

| DXY (mid‑2025) | ~106 |

| Semiconductor lead times (2024) | ~20 wks |

Preview the Actual Deliverable

Cisco Systems PESTLE Analysis

This Cisco Systems PESTLE Analysis preview is the exact, fully formatted document you’ll receive after purchase—no placeholders or surprises. The content, structure, and layout shown here are identical to the downloadable file delivered immediately upon payment. Use it as-is for strategic planning, presentations, or research.

Original: $10.00

-65%$10.00

$3.50Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Uncover how political shifts, economic cycles, and rapid tech innovation are reshaping Cisco Systems with our concise PESTLE snapshot—perfect for investors and strategists. Gain actionable insight to de-risk decisions and spot growth vectors. Purchase the full PESTLE for the complete, ready-to-use analysis now.

Political factors

Geopolitics and export controls

US–China tensions and stepped-up export controls (notably Oct 2022 and subsequent 2023–24 measures on advanced chips and encryption) constrain Cisco’s market access for high-end networking and security gear. Restrictions on certain semiconductors and crypto tech force shipment delays and product redesigns, raising lead times and costs. Cisco, with FY2024 revenue of about $60.8B, must segment product roadmaps and supply lines by jurisdiction, affecting pricing and competitive dynamics.

Public sector procurement

Public sector procurement drives demand for secure networking, cloud connectivity and zero-trust, aligning with Cisco’s offerings as governments increase IT modernization; Cisco reported fiscal 2024 revenue of about $57.8 billion, with public sector a material vertical. Multi-year government contracts offer revenue visibility but necessitate strict compliance and certifications. Fiscal cycles and elections shift priorities, while defense, critical infrastructure and education remain strategic buys.

Localization and national champions

Many governments push local manufacturing, data residency and national tech champions, with over 50 countries having data-localization measures by 2024; Cisco, which reported $58.3B revenue in FY2024, may need JVs, local partners or in-country assembly to win tenders. Preference policies can tilt procurement toward domestic vendors, raising implementation costs but opening protected markets.

Sanctions and entity lists

Sanctions regimes can abruptly bar sales to named entities or regions, forcing Cisco to reroute business and comply with export controls; OFAC civil penalties can reach roughly 336,922 USD per violation, with criminal exposure higher. Effective compliance requires customer screening, license management and auditable controls; breaches risk heavy fines and reputational damage. Product portfolio mix and channel policies must be rapidly adjusted to remain compliant and preserve revenue.

- Immediate sales restrictions to listed entities

- Mandatory screening & license workflows

- Audit trails to avoid ~336,922 USD penalties

- Rapid channel/portfolio reconfiguration

Standards and multilateral bodies

Cisco is an active contributor to IETF, IEEE and 3GPP, influencing interoperability and adoption; IETF had over 9,000 RFCs by 2024 and 3GPP Release 18 (5G‑Advanced) work was ongoing in 2024–25, affecting product roadmaps. Fragmentation of standards across geopolitical blocs raises engineering complexity, while standards leadership preserves backward compatibility and market access and can yield de facto advantages.

- Interoperability: IETF/IEEE/3GPP influence

- Complexity: fragmentation across blocs

- Access: standards participation protects market entry

- Advantage: leadership creates de facto market benefits

Export controls, localization & standards reshape secure networking supply chains

US–China export controls (2022–24) limit high-end sales, forcing redesigns and segmented supply chains; Cisco FY2024 revenue ≈ $58.3B. Governments drive secure networking demand via multi-year contracts but require localization and compliance amid >50 data‑localization laws by 2024. Sanctions/OFAC risk (~336,922 USD civil penalty per violation) mandate strict screening. Standards role (IETF >9,000 RFCs; 3GPP R18 ongoing) shapes roadmaps.

| Metric | Value |

|---|---|

| FY2024 revenue | $58.3B |

| Data‑localization laws (by 2024) | >50 countries |

| OFAC civil penalty (approx) | $336,922 |

| IETF RFCs (by 2024) | >9,000 |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely affect Cisco Systems, with data-backed trends and regional industry context; designed to reveal threats and opportunities for executives, consultants, and investors and to support scenario planning, strategy design, and inclusion in business plans or investor materials.

Relieves meeting-prep pain by providing a concise, visually segmented Cisco PESTLE summary that highlights external risks and opportunities, is editable for regional or business-line notes, and can be dropped into presentations or shared across teams for quick alignment.

Economic factors

IT spending cycles

Enterprise capex and opex shift with macro growth, inflation and confidence—hardware refreshes are often deferred in downturns while security and cloud connectivity stay more resilient. Cisco’s recurring software and services, exceeding $20B in FY2024, help smooth revenue volatility; a vertical mix across service providers, public sector and cloud customers diversifies demand.

Interest rates and financing

Higher interest rates — US federal funds at about 5.25–5.50% in mid‑2025 — raise the total cost of ownership for financed Cisco deals and squeeze partner working capital, slowing deal flow. Customer purchase decision cycles lengthen as corporate hurdle rates rise, delaying refreshes and cloud migrations. Cisco Capital can unlock sales by offering financing but increases Cisco’s credit exposure; subsequent rate cuts have historically unlocked deferred projects and upgrades.

FX and global footprint

A strong US dollar (DXY near 106 in mid-2025) compresses Cisco’s international revenue translation and forces tougher local pricing in key markets. Hedging programs reduce reported volatility but do not restore bid competitiveness in local-currency tenders. Local pricing, channel incentives and promotions are used to soften demand elasticity. Supply and service costs also rise when currencies weaken versus the dollar.

Supply chain and components

Semiconductor availability and logistics costs materially affect Ciscos bookings-to-revenue conversion; industry semiconductor lead times averaged about 20 weeks in 2024, extending conversion cycles. Diversified sourcing and design-for-availability have reduced node-specific disruption and improved fulfillment resilience. Inventory optimization balances demand uncertainty with delivery SLAs while cost inflation pressures margins and forces selective list-price increases.

- Semiconductor lead times: ~20 weeks (2024)

- Diversified sourcing lowers single-vendor risk

- Inventory optimization aligns safety stock with SLAs

- Cost inflation compresses gross margins, prompting pricing actions

Cloud and subscription mix

Cisco's shift to cloud and subscription offerings alters revenue recognition and compresses near-term product margins while boosting recurring revenue visibility, requiring a land-and-expand sales motion to drive renewals and upsells across security, observability, and collaboration bundles that raise ARPU.

- Recurring revenue improves predictability and valuation multiples

- Bundles increase ARPU and customer stickiness

- Land-and-expand is critical for growth

- Partner comp must shift to subscription economics

Export controls, localization & standards reshape secure networking supply chains

Enterprise capex sensitivity, higher rates (Fed funds ~5.25–5.50% mid‑2025) and strong dollar (DXY ~106) compress international revenues; recurring software/services (>20B FY2024) smooth volatility. Semiconductor lead times (~20 weeks in 2024) and rising logistics inflate costs and delay bookings-to-revenue. Cisco Capital offsets some cycle weakness but raises credit exposure.

| Metric | Value |

|---|---|

| FY2024 recurring rev | >$20B |

| Total rev FY2024 | $57.6B |

| Fed funds (mid‑2025) | 5.25–5.50% |

| DXY (mid‑2025) | ~106 |

| Semiconductor lead times (2024) | ~20 wks |

Preview the Actual Deliverable

Cisco Systems PESTLE Analysis

This Cisco Systems PESTLE Analysis preview is the exact, fully formatted document you’ll receive after purchase—no placeholders or surprises. The content, structure, and layout shown here are identical to the downloadable file delivered immediately upon payment. Use it as-is for strategic planning, presentations, or research.