City Union Bank Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

City Union Bank’s Porter’s Five Forces snapshot highlights moderate bargaining power of borrowers, intense rivalry among private and regional banks, and emerging fintech substitution risks that could compress margins. Regulatory oversight and concentrated deposit bases shape strategic priorities and capital allocation. This brief only scratches the surface—unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy implications.

Suppliers Bargaining Power

Depositors as primary funders

Retail and corporate depositors supply the low-cost funds that underpin City Union Bank’s loan growth and margins, though their rate sensitivity can force the bank to raise cost of funds if competitors hike deposit rates. Granular CASA and term deposits lower concentration risk and stabilize funding. Deposit insurance covers deposits up to ₹5 lakh, and strong brand trust further moderates depositor bargaining power.

Wholesale funding and interbank lines

Refinance from institutions and interbank borrowings are often costlier and more volatile than retail deposits, and in 2024 liquidity repricing episodes pushed spreads and covenant demands higher during stress.

Technology and fintech vendors

Critical core-banking, cybersecurity, and digital platforms for City Union Bank are supplied by a concentrated vendor set, creating leverage as many contracts run 3–5 years and migrations typically take months to over a year.

High switching costs, integration complexity, regulatory compliance, and SLAs amplify supplier bargaining power, and long-term contracts can lock in pricing and service levels.

Adopting multi-vendor architectures and selective in-house development has lowered dependence and procurement risk while enabling negotiation of better terms.

Payment networks and infrastructure

Skilled talent and compliance expertise

Skilled risk, credit, tech and regulatory talent are scarce and mobile, raising wage bargaining power and pushing attrition in banking tech roles by about 12% in 2024; retention is therefore crucial for City Union Bank to protect asset quality and digital delivery against poaching by larger private banks and well-funded fintechs.

- Retention: key to asset quality

- Competition: private banks, fintechs

- Training pipelines mitigate risk

- ESOPs lower turnover

Retail CASA cushions banks; rate-sensitive flows and vendor/talent squeeze raise funding costs

Retail deposits (granular CASA, ₹5 lakh deposit insurance) temper depositor power, though rate-sensitive flows can raise cost of funds. Institutional/refinance channels are costlier and volatile; 2024 liquidity repricing tightened spreads. Concentrated IT/payment vendors, 3–5yr contracts and ~210,000 ATMs/UPI >100 billion txns in 2024 increase supplier leverage. Talent attrition ~12% in 2024 raises wage pressure.

| Supplier | Impact | 2024 metric |

|---|---|---|

| Depositors | Low-cost funding | ₹5 lakh insurance |

| Payment networks | Fee rules | UPI >100bn txns |

| Vendors/talent | Leverage | Attrition ~12% |

What is included in the product

Uncovers competitive drivers, customer and supplier power, entry barriers, substitutes and rival intensity specific to City Union Bank, with strategic implications for pricing, growth and risk mitigation.

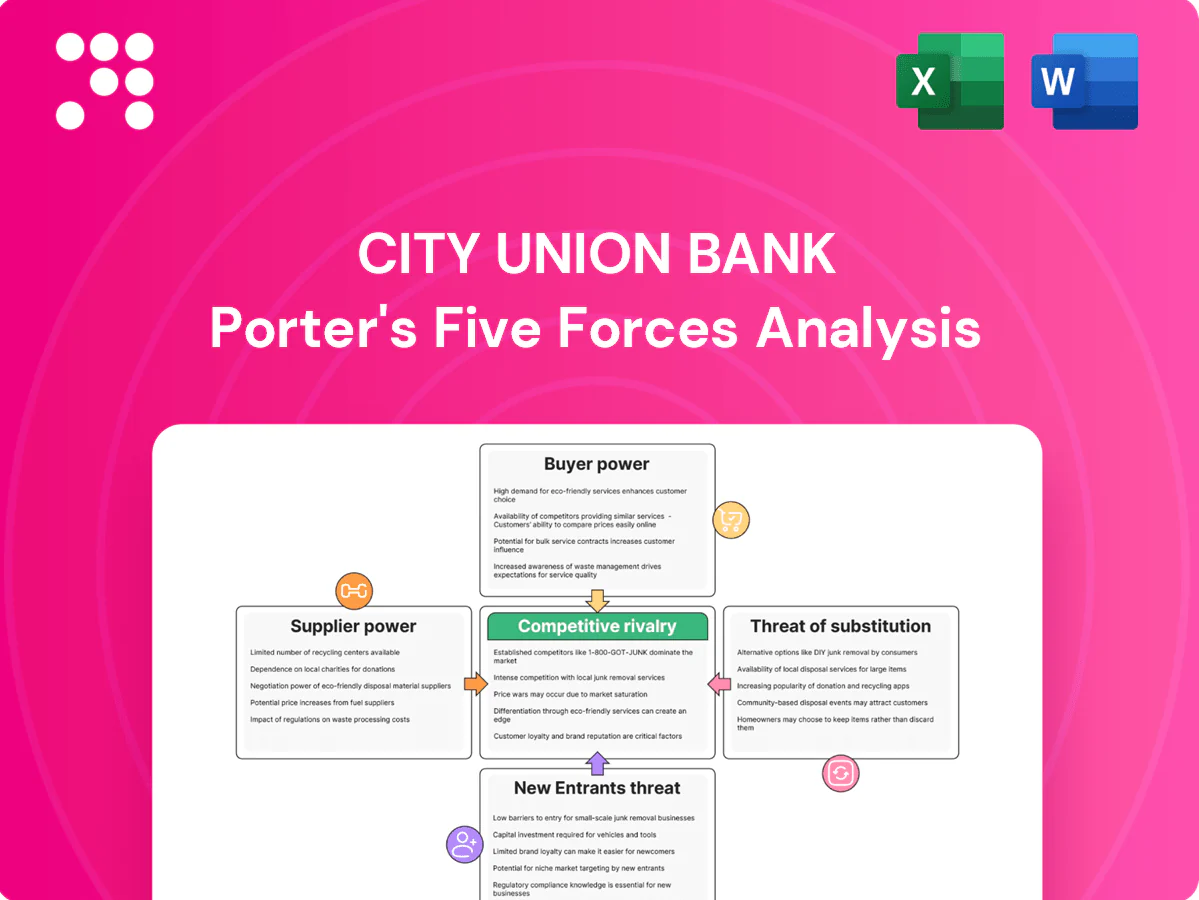

Compact one-sheet Porter's Five Forces for City Union Bank — customizable pressure levels with a spider chart, deck-ready layout, swap in your data, no macros, fits Excel dashboards or Word reports.

Customers Bargaining Power

Price-sensitive retail depositors

Price-sensitive retail depositors increasingly shop rates via comparison apps and portals, and the surge in UPI—monthly volumes exceeded 10 billion by 2023 and rose further into 2024—plus streamlined digital onboarding sharply lowers switching friction. To defend balances City Union Bank must trade higher term-deposit pricing against CASA acquisition economics; its brand trust and service quality can reduce pure price bargaining and help retain core low-cost liabilities.

SME and corporate borrowers

SME and corporate borrowers exert strong bargaining power, negotiating spreads, fees and covenants based on credit profile and collateral; competing banks and NBFCs in 2024 continued offering tailored structures and faster turnaround, increasing pressure. Relationship banking and bundled treasury and payment services at City Union Bank help mitigate price sensitivity, but concentration risk in marquee accounts elevates buyer leverage.

Digital-first users

Digital-first users expect seamless 24/7 mobile and internet banking with industry-level uptime near 99.9%; even short outages drive rapid churn. Transparent fee and feature comparisons and public reviews amplify customer bargaining power. Continuous feature rollout and reliability are key to retention in India’s high-volume digital ecosystem—UPI processed over 10 billion transactions in a month in 2024 (NPCI).

Rural and agricultural customers

Rural borrowers choose City Union Bank mainly for credit access, faster turnaround and doorstep service; Kisan Credit Card lending in India topped about Rs 11 lakh crore by 2024, with a 2% interest subvention capping banks’ pricing flexibility. Informal moneylenders still compete at 24–36% APR, but CUB’s 800+ branches and field officers reduce customer bargaining power through proximity and service convenience.

- Credit access: high demand for KCC and microloans

- Pricing cap: 2% subvention limits rate hikes

- Alternatives: informal lenders (24–36% APR)

- Proximity: 800+ branches + field staff lower buyer power

Fee-based service seekers

Fee-based forex, trade, wealth and payments customers increasingly shop on fees and SLAs; competing platforms in 2024 processed over 70 billion UPI transactions and offer flat pricing and plug-in integrations, raising switching pressure on City Union Bank. Volume discounts and bundled pricing drive retention, while superior advisory quality and execution speed can offset pure price comparisons.

- Fees/SLA-driven

- Flat-price competitors

- Volume discounts matter

- Advisory/speed offsets price

UPI boom and KCC caps boost customer bargaining power, press bank spreads

Customers wield rising bargaining power as price-sensitive retail users and digital-first clients (UPI >10 billion monthly txns in 2024) switch quickly; SME/corporate borrowers press spreads and covenants amid NBFC competition. Rural clients rely on proximity (City Union Bank 800+ branches) but KCC exposure (≈Rs 11 lakh crore by 2024) and 2% subvention cap limit pricing flexibility.

| Metric | Value | Source |

|---|---|---|

| UPI monthly txns | >10 billion | NPCI 2024 |

| CUB branches | 800+ | CUB 2024 |

| KCC outstanding | ≈Rs 11 lakh crore | RBI/2024 |

| Expected uptime | ~99.9% | Industry 2024 |

Full Version Awaits

City Union Bank Porter's Five Forces Analysis

This preview shows the exact City Union Bank Porter's Five Forces analysis you'll receive—no placeholders or mockups. The full document is professionally written, fully formatted and ready for immediate download upon purchase. What you see here is precisely the deliverable you'll get after payment.

Go Beyond the Preview—Access the Full Strategic Report

City Union Bank’s Porter’s Five Forces snapshot highlights moderate bargaining power of borrowers, intense rivalry among private and regional banks, and emerging fintech substitution risks that could compress margins. Regulatory oversight and concentrated deposit bases shape strategic priorities and capital allocation. This brief only scratches the surface—unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy implications.

Suppliers Bargaining Power

Depositors as primary funders

Retail and corporate depositors supply the low-cost funds that underpin City Union Bank’s loan growth and margins, though their rate sensitivity can force the bank to raise cost of funds if competitors hike deposit rates. Granular CASA and term deposits lower concentration risk and stabilize funding. Deposit insurance covers deposits up to ₹5 lakh, and strong brand trust further moderates depositor bargaining power.

Wholesale funding and interbank lines

Refinance from institutions and interbank borrowings are often costlier and more volatile than retail deposits, and in 2024 liquidity repricing episodes pushed spreads and covenant demands higher during stress.

Technology and fintech vendors

Critical core-banking, cybersecurity, and digital platforms for City Union Bank are supplied by a concentrated vendor set, creating leverage as many contracts run 3–5 years and migrations typically take months to over a year.

High switching costs, integration complexity, regulatory compliance, and SLAs amplify supplier bargaining power, and long-term contracts can lock in pricing and service levels.

Adopting multi-vendor architectures and selective in-house development has lowered dependence and procurement risk while enabling negotiation of better terms.

Payment networks and infrastructure

Skilled talent and compliance expertise

Skilled risk, credit, tech and regulatory talent are scarce and mobile, raising wage bargaining power and pushing attrition in banking tech roles by about 12% in 2024; retention is therefore crucial for City Union Bank to protect asset quality and digital delivery against poaching by larger private banks and well-funded fintechs.

- Retention: key to asset quality

- Competition: private banks, fintechs

- Training pipelines mitigate risk

- ESOPs lower turnover

Retail CASA cushions banks; rate-sensitive flows and vendor/talent squeeze raise funding costs

Retail deposits (granular CASA, ₹5 lakh deposit insurance) temper depositor power, though rate-sensitive flows can raise cost of funds. Institutional/refinance channels are costlier and volatile; 2024 liquidity repricing tightened spreads. Concentrated IT/payment vendors, 3–5yr contracts and ~210,000 ATMs/UPI >100 billion txns in 2024 increase supplier leverage. Talent attrition ~12% in 2024 raises wage pressure.

| Supplier | Impact | 2024 metric |

|---|---|---|

| Depositors | Low-cost funding | ₹5 lakh insurance |

| Payment networks | Fee rules | UPI >100bn txns |

| Vendors/talent | Leverage | Attrition ~12% |

What is included in the product

Uncovers competitive drivers, customer and supplier power, entry barriers, substitutes and rival intensity specific to City Union Bank, with strategic implications for pricing, growth and risk mitigation.

Compact one-sheet Porter's Five Forces for City Union Bank — customizable pressure levels with a spider chart, deck-ready layout, swap in your data, no macros, fits Excel dashboards or Word reports.

Customers Bargaining Power

Price-sensitive retail depositors

Price-sensitive retail depositors increasingly shop rates via comparison apps and portals, and the surge in UPI—monthly volumes exceeded 10 billion by 2023 and rose further into 2024—plus streamlined digital onboarding sharply lowers switching friction. To defend balances City Union Bank must trade higher term-deposit pricing against CASA acquisition economics; its brand trust and service quality can reduce pure price bargaining and help retain core low-cost liabilities.

SME and corporate borrowers

SME and corporate borrowers exert strong bargaining power, negotiating spreads, fees and covenants based on credit profile and collateral; competing banks and NBFCs in 2024 continued offering tailored structures and faster turnaround, increasing pressure. Relationship banking and bundled treasury and payment services at City Union Bank help mitigate price sensitivity, but concentration risk in marquee accounts elevates buyer leverage.

Digital-first users

Digital-first users expect seamless 24/7 mobile and internet banking with industry-level uptime near 99.9%; even short outages drive rapid churn. Transparent fee and feature comparisons and public reviews amplify customer bargaining power. Continuous feature rollout and reliability are key to retention in India’s high-volume digital ecosystem—UPI processed over 10 billion transactions in a month in 2024 (NPCI).

Rural and agricultural customers

Rural borrowers choose City Union Bank mainly for credit access, faster turnaround and doorstep service; Kisan Credit Card lending in India topped about Rs 11 lakh crore by 2024, with a 2% interest subvention capping banks’ pricing flexibility. Informal moneylenders still compete at 24–36% APR, but CUB’s 800+ branches and field officers reduce customer bargaining power through proximity and service convenience.

- Credit access: high demand for KCC and microloans

- Pricing cap: 2% subvention limits rate hikes

- Alternatives: informal lenders (24–36% APR)

- Proximity: 800+ branches + field staff lower buyer power

Fee-based service seekers

Fee-based forex, trade, wealth and payments customers increasingly shop on fees and SLAs; competing platforms in 2024 processed over 70 billion UPI transactions and offer flat pricing and plug-in integrations, raising switching pressure on City Union Bank. Volume discounts and bundled pricing drive retention, while superior advisory quality and execution speed can offset pure price comparisons.

- Fees/SLA-driven

- Flat-price competitors

- Volume discounts matter

- Advisory/speed offsets price

UPI boom and KCC caps boost customer bargaining power, press bank spreads

Customers wield rising bargaining power as price-sensitive retail users and digital-first clients (UPI >10 billion monthly txns in 2024) switch quickly; SME/corporate borrowers press spreads and covenants amid NBFC competition. Rural clients rely on proximity (City Union Bank 800+ branches) but KCC exposure (≈Rs 11 lakh crore by 2024) and 2% subvention cap limit pricing flexibility.

| Metric | Value | Source |

|---|---|---|

| UPI monthly txns | >10 billion | NPCI 2024 |

| CUB branches | 800+ | CUB 2024 |

| KCC outstanding | ≈Rs 11 lakh crore | RBI/2024 |

| Expected uptime | ~99.9% | Industry 2024 |

Full Version Awaits

City Union Bank Porter's Five Forces Analysis

This preview shows the exact City Union Bank Porter's Five Forces analysis you'll receive—no placeholders or mockups. The full document is professionally written, fully formatted and ready for immediate download upon purchase. What you see here is precisely the deliverable you'll get after payment.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

City Union Bank’s Porter’s Five Forces snapshot highlights moderate bargaining power of borrowers, intense rivalry among private and regional banks, and emerging fintech substitution risks that could compress margins. Regulatory oversight and concentrated deposit bases shape strategic priorities and capital allocation. This brief only scratches the surface—unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy implications.

Suppliers Bargaining Power

Depositors as primary funders

Retail and corporate depositors supply the low-cost funds that underpin City Union Bank’s loan growth and margins, though their rate sensitivity can force the bank to raise cost of funds if competitors hike deposit rates. Granular CASA and term deposits lower concentration risk and stabilize funding. Deposit insurance covers deposits up to ₹5 lakh, and strong brand trust further moderates depositor bargaining power.

Wholesale funding and interbank lines

Refinance from institutions and interbank borrowings are often costlier and more volatile than retail deposits, and in 2024 liquidity repricing episodes pushed spreads and covenant demands higher during stress.

Technology and fintech vendors

Critical core-banking, cybersecurity, and digital platforms for City Union Bank are supplied by a concentrated vendor set, creating leverage as many contracts run 3–5 years and migrations typically take months to over a year.

High switching costs, integration complexity, regulatory compliance, and SLAs amplify supplier bargaining power, and long-term contracts can lock in pricing and service levels.

Adopting multi-vendor architectures and selective in-house development has lowered dependence and procurement risk while enabling negotiation of better terms.

Payment networks and infrastructure

Skilled talent and compliance expertise

Skilled risk, credit, tech and regulatory talent are scarce and mobile, raising wage bargaining power and pushing attrition in banking tech roles by about 12% in 2024; retention is therefore crucial for City Union Bank to protect asset quality and digital delivery against poaching by larger private banks and well-funded fintechs.

- Retention: key to asset quality

- Competition: private banks, fintechs

- Training pipelines mitigate risk

- ESOPs lower turnover

Retail CASA cushions banks; rate-sensitive flows and vendor/talent squeeze raise funding costs

Retail deposits (granular CASA, ₹5 lakh deposit insurance) temper depositor power, though rate-sensitive flows can raise cost of funds. Institutional/refinance channels are costlier and volatile; 2024 liquidity repricing tightened spreads. Concentrated IT/payment vendors, 3–5yr contracts and ~210,000 ATMs/UPI >100 billion txns in 2024 increase supplier leverage. Talent attrition ~12% in 2024 raises wage pressure.

| Supplier | Impact | 2024 metric |

|---|---|---|

| Depositors | Low-cost funding | ₹5 lakh insurance |

| Payment networks | Fee rules | UPI >100bn txns |

| Vendors/talent | Leverage | Attrition ~12% |

What is included in the product

Uncovers competitive drivers, customer and supplier power, entry barriers, substitutes and rival intensity specific to City Union Bank, with strategic implications for pricing, growth and risk mitigation.

Compact one-sheet Porter's Five Forces for City Union Bank — customizable pressure levels with a spider chart, deck-ready layout, swap in your data, no macros, fits Excel dashboards or Word reports.

Customers Bargaining Power

Price-sensitive retail depositors

Price-sensitive retail depositors increasingly shop rates via comparison apps and portals, and the surge in UPI—monthly volumes exceeded 10 billion by 2023 and rose further into 2024—plus streamlined digital onboarding sharply lowers switching friction. To defend balances City Union Bank must trade higher term-deposit pricing against CASA acquisition economics; its brand trust and service quality can reduce pure price bargaining and help retain core low-cost liabilities.

SME and corporate borrowers

SME and corporate borrowers exert strong bargaining power, negotiating spreads, fees and covenants based on credit profile and collateral; competing banks and NBFCs in 2024 continued offering tailored structures and faster turnaround, increasing pressure. Relationship banking and bundled treasury and payment services at City Union Bank help mitigate price sensitivity, but concentration risk in marquee accounts elevates buyer leverage.

Digital-first users

Digital-first users expect seamless 24/7 mobile and internet banking with industry-level uptime near 99.9%; even short outages drive rapid churn. Transparent fee and feature comparisons and public reviews amplify customer bargaining power. Continuous feature rollout and reliability are key to retention in India’s high-volume digital ecosystem—UPI processed over 10 billion transactions in a month in 2024 (NPCI).

Rural and agricultural customers

Rural borrowers choose City Union Bank mainly for credit access, faster turnaround and doorstep service; Kisan Credit Card lending in India topped about Rs 11 lakh crore by 2024, with a 2% interest subvention capping banks’ pricing flexibility. Informal moneylenders still compete at 24–36% APR, but CUB’s 800+ branches and field officers reduce customer bargaining power through proximity and service convenience.

- Credit access: high demand for KCC and microloans

- Pricing cap: 2% subvention limits rate hikes

- Alternatives: informal lenders (24–36% APR)

- Proximity: 800+ branches + field staff lower buyer power

Fee-based service seekers

Fee-based forex, trade, wealth and payments customers increasingly shop on fees and SLAs; competing platforms in 2024 processed over 70 billion UPI transactions and offer flat pricing and plug-in integrations, raising switching pressure on City Union Bank. Volume discounts and bundled pricing drive retention, while superior advisory quality and execution speed can offset pure price comparisons.

- Fees/SLA-driven

- Flat-price competitors

- Volume discounts matter

- Advisory/speed offsets price

UPI boom and KCC caps boost customer bargaining power, press bank spreads

Customers wield rising bargaining power as price-sensitive retail users and digital-first clients (UPI >10 billion monthly txns in 2024) switch quickly; SME/corporate borrowers press spreads and covenants amid NBFC competition. Rural clients rely on proximity (City Union Bank 800+ branches) but KCC exposure (≈Rs 11 lakh crore by 2024) and 2% subvention cap limit pricing flexibility.

| Metric | Value | Source |

|---|---|---|

| UPI monthly txns | >10 billion | NPCI 2024 |

| CUB branches | 800+ | CUB 2024 |

| KCC outstanding | ≈Rs 11 lakh crore | RBI/2024 |

| Expected uptime | ~99.9% | Industry 2024 |

Full Version Awaits

City Union Bank Porter's Five Forces Analysis

This preview shows the exact City Union Bank Porter's Five Forces analysis you'll receive—no placeholders or mockups. The full document is professionally written, fully formatted and ready for immediate download upon purchase. What you see here is precisely the deliverable you'll get after payment.