City Union Bank SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

City Union Bank's SWOT highlights resilient regional banking strengths, niche retail franchise, and prudent asset quality, alongside competition, regulatory headwinds, and digital transformation needs. Want the full story behind its strengths, risks, and growth drivers? Purchase the complete SWOT analysis to gain a professionally written, editable report ideal for investors and strategists.

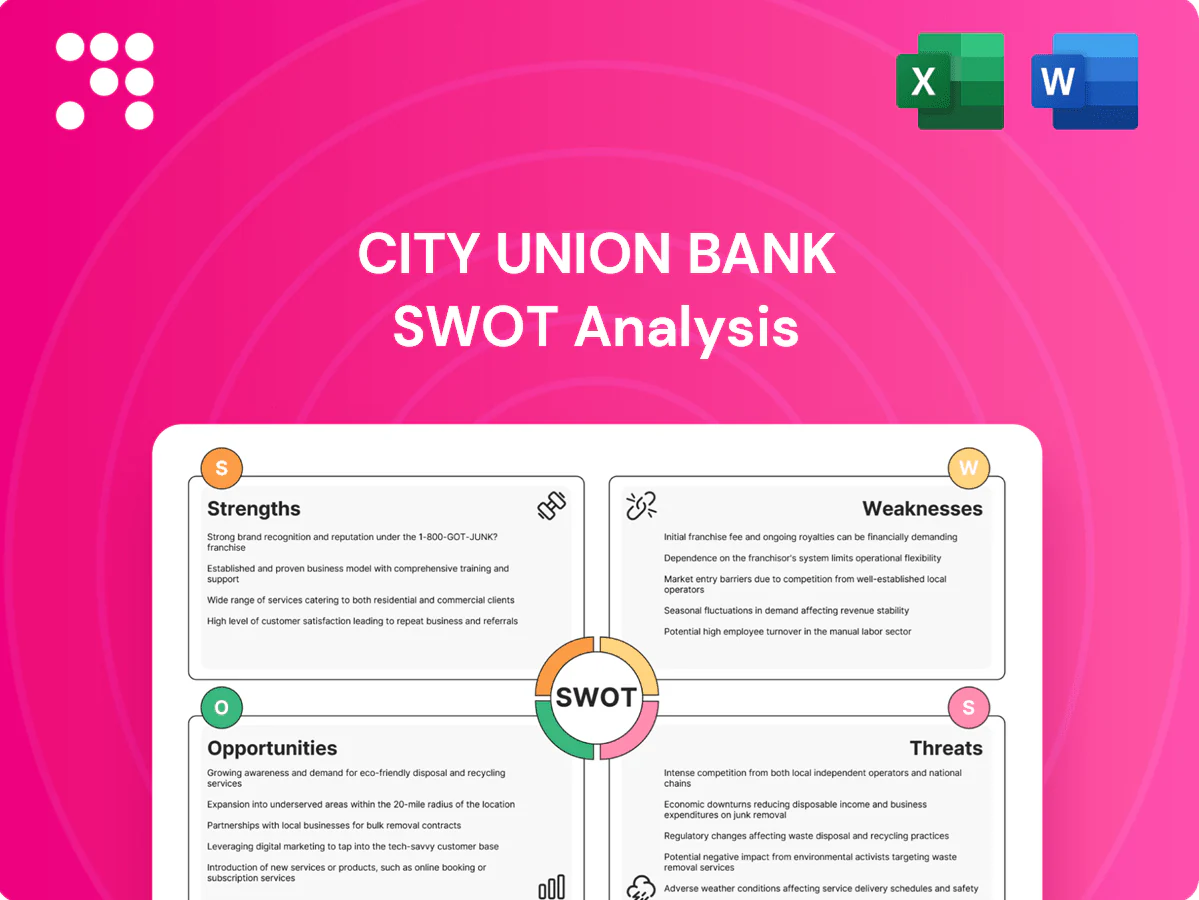

Strengths

Diverse product suite

City Union Bank, founded in 1904, offers deposits and loans across retail, agri and corporate segments alongside FX and transaction services, creating a full-service portfolio that drives multiple revenue streams and customer stickiness. Robust cross-sell opportunities raise customer lifetime value, while the mix of fee and interest income enhances resilience against cyclical credit shocks.

Strong regional franchise

Deep roots in South India since 1904 anchor City Union Bank's loyal MSME and retail base, supporting relationship banking and stable low-cost deposits. Local market knowledge enhances underwriting and collections, lowering credit costs and improving recoveries. Community trust from over 120 years of operations underpins steady growth through cycles.

Prudent risk culture

Conservative lending and a granular portfolio have kept City Union Banks GNPA at about 1.34% and NNPA near 0.30% (FY2024), while secured advances—around 85–87% of loans—lower loss given default; disciplined recovery and high PCR have helped contain credit costs, supporting consistent profitability with recurring RoA ~1.6%.

Digital enablement

City Union Bank leverages internet/mobile banking, a growing ATM network and open APIs to shorten turnaround times and automate routine services.

Digital onboarding and payments have expanded reach into semi-urban markets, increasing transaction volumes and lowering acquisition costs.

Data-led cross-sell initiatives lift fee income per customer while rising self-service use reduces cost-to-serve.

- APIs: faster service delivery

- Onboarding: wider reach, lower CAC

- Cross-sell: higher fees/customer

- Self-service: reduced cost-to-serve

SME and agri expertise

City Union Bank’s deep specialization in MSME and agriculture lending creates a durable niche, with tailored loan products and faster credit decisions attracting higher-quality borrowers and repeat business.

Collateral-backed structures and focused risk underwriting reduce portfolio volatility, while long-standing ecosystem relationships with traders, input suppliers and local businesses strengthen customer retention and cross-sell opportunities.

- SME/MSME focus

- Tailored products & fast decisions

- Collateral-backed risk mitigation

- Ecosystem-driven retention

Diversified retail, MSME & corporate lender; GNPA 1.34%, RoA ~1.6%

City Union Bank combines diversified retail, MSME and corporate lending with fee income and digital channels, driving customer stickiness and cross-sell. Conservative underwriting yields GNPA ~1.34% and NNPA ~0.30% (FY2024) with secured advances ~85–87%, supporting recurring RoA ~1.6%. Deep South India franchise and API-led digital services lower acquisition and servicing costs while boosting recoveries.

| Metric | Value | Period |

|---|---|---|

| GNPA | 1.34% | FY2024 |

| NNPA | 0.30% | FY2024 |

| Secured advances | 85–87% | FY2024 |

| RoA | ~1.6% | FY2024 |

What is included in the product

Delivers a strategic overview of City Union Bank’s internal strengths and weaknesses and examines external opportunities and threats shaping its competitive position and growth prospects.

Delivers a concise City Union Bank SWOT matrix for quick strategic alignment, easing stakeholder briefings and enabling fast, editable updates to reflect shifting market priorities.

Weaknesses

Geographic concentration

City Union Bank remains heavily concentrated in Tamil Nadu and the broader southern region, exposing it to heightened regional risk; local economic slowdowns or sectoral shocks can disproportionately dent growth and credit quality. Diversification across India is still a work-in-progress, with branch expansion beyond core markets progressing slowly relative to peers. This geographic skew constrains balance-sheet resilience and revenue diversification.

Scale limitations

City Union Bank's smaller balance sheet (≈₹1.1 lakh crore assets FY24) versus SBI/ICICI (≈₹70–80 lakh crore) reduces pricing power on deposits and loans, compressing spreads. Higher unit costs from 1,500+ branches push cost-to-income toward 48–52%, pressuring margins. Limited capital expenditure restricts investments in AI and real-time payments, and brand scale makes attracting senior fintech talent harder against larger banks.

Legacy processes

Operational workflows at City Union Bank still retain manual dependencies, causing inefficiencies and higher processing costs. Integration challenges across legacy systems slow product launches and limit API-driven partnerships. Rigidity in processes raises turnaround times for loan disbursals and account services. Customer experience trails digital-first competitors, impacting retention among younger segments.

Fee income depth

City Union Bank's revenue mix is heavily skewed to interest income, with non‑interest fee lines contributing under one-quarter of total income in FY2024, limiting potential ROA uplift. Limited penetration in wealth, payments and FX fees caps fee growth, while volatile credit costs have outsized impact on profits. Diversifying non‑interest streams is essential.

- Revenue mix: interest‑dominant (FY2024)

- Low wealth/payments/FX fee penetration

- Volatile credit costs amplify profit swings

- Priority: expand non‑interest income

Brand visibility

- Limited national recognition

- ~860 branches (Mar 2024)

- Acquisition costs +≈20% outside core

- Requires multi-year trust investment

Regional bank faces scale limits, margin pressure from high costs and low fee income

City Union Bank is regionally concentrated in Tamil Nadu, limiting diversification and exposing it to local downturns. A smaller balance sheet (~₹1.1 lakh crore FY24) and ~860 branches reduce pricing power and scale benefits. Cost-to-income (~48–52%) and non‑interest income under 25% constrain margins and fee diversification.

| Metric | Value (FY24) |

|---|---|

| Assets | ≈₹1.1 lakh crore |

| Branches | ≈860 |

| Non‑interest income | <25% |

| Cost-to-income | ≈48–52% |

Preview Before You Purchase

City Union Bank SWOT Analysis

This is the actual City Union Bank SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; purchase unlocks the complete, editable version. Buy now to access the full, detailed analysis.

Dive Deeper Into the Company’s Strategic Blueprint

City Union Bank's SWOT highlights resilient regional banking strengths, niche retail franchise, and prudent asset quality, alongside competition, regulatory headwinds, and digital transformation needs. Want the full story behind its strengths, risks, and growth drivers? Purchase the complete SWOT analysis to gain a professionally written, editable report ideal for investors and strategists.

Strengths

Diverse product suite

City Union Bank, founded in 1904, offers deposits and loans across retail, agri and corporate segments alongside FX and transaction services, creating a full-service portfolio that drives multiple revenue streams and customer stickiness. Robust cross-sell opportunities raise customer lifetime value, while the mix of fee and interest income enhances resilience against cyclical credit shocks.

Strong regional franchise

Deep roots in South India since 1904 anchor City Union Bank's loyal MSME and retail base, supporting relationship banking and stable low-cost deposits. Local market knowledge enhances underwriting and collections, lowering credit costs and improving recoveries. Community trust from over 120 years of operations underpins steady growth through cycles.

Prudent risk culture

Conservative lending and a granular portfolio have kept City Union Banks GNPA at about 1.34% and NNPA near 0.30% (FY2024), while secured advances—around 85–87% of loans—lower loss given default; disciplined recovery and high PCR have helped contain credit costs, supporting consistent profitability with recurring RoA ~1.6%.

Digital enablement

City Union Bank leverages internet/mobile banking, a growing ATM network and open APIs to shorten turnaround times and automate routine services.

Digital onboarding and payments have expanded reach into semi-urban markets, increasing transaction volumes and lowering acquisition costs.

Data-led cross-sell initiatives lift fee income per customer while rising self-service use reduces cost-to-serve.

- APIs: faster service delivery

- Onboarding: wider reach, lower CAC

- Cross-sell: higher fees/customer

- Self-service: reduced cost-to-serve

SME and agri expertise

City Union Bank’s deep specialization in MSME and agriculture lending creates a durable niche, with tailored loan products and faster credit decisions attracting higher-quality borrowers and repeat business.

Collateral-backed structures and focused risk underwriting reduce portfolio volatility, while long-standing ecosystem relationships with traders, input suppliers and local businesses strengthen customer retention and cross-sell opportunities.

- SME/MSME focus

- Tailored products & fast decisions

- Collateral-backed risk mitigation

- Ecosystem-driven retention

Diversified retail, MSME & corporate lender; GNPA 1.34%, RoA ~1.6%

City Union Bank combines diversified retail, MSME and corporate lending with fee income and digital channels, driving customer stickiness and cross-sell. Conservative underwriting yields GNPA ~1.34% and NNPA ~0.30% (FY2024) with secured advances ~85–87%, supporting recurring RoA ~1.6%. Deep South India franchise and API-led digital services lower acquisition and servicing costs while boosting recoveries.

| Metric | Value | Period |

|---|---|---|

| GNPA | 1.34% | FY2024 |

| NNPA | 0.30% | FY2024 |

| Secured advances | 85–87% | FY2024 |

| RoA | ~1.6% | FY2024 |

What is included in the product

Delivers a strategic overview of City Union Bank’s internal strengths and weaknesses and examines external opportunities and threats shaping its competitive position and growth prospects.

Delivers a concise City Union Bank SWOT matrix for quick strategic alignment, easing stakeholder briefings and enabling fast, editable updates to reflect shifting market priorities.

Weaknesses

Geographic concentration

City Union Bank remains heavily concentrated in Tamil Nadu and the broader southern region, exposing it to heightened regional risk; local economic slowdowns or sectoral shocks can disproportionately dent growth and credit quality. Diversification across India is still a work-in-progress, with branch expansion beyond core markets progressing slowly relative to peers. This geographic skew constrains balance-sheet resilience and revenue diversification.

Scale limitations

City Union Bank's smaller balance sheet (≈₹1.1 lakh crore assets FY24) versus SBI/ICICI (≈₹70–80 lakh crore) reduces pricing power on deposits and loans, compressing spreads. Higher unit costs from 1,500+ branches push cost-to-income toward 48–52%, pressuring margins. Limited capital expenditure restricts investments in AI and real-time payments, and brand scale makes attracting senior fintech talent harder against larger banks.

Legacy processes

Operational workflows at City Union Bank still retain manual dependencies, causing inefficiencies and higher processing costs. Integration challenges across legacy systems slow product launches and limit API-driven partnerships. Rigidity in processes raises turnaround times for loan disbursals and account services. Customer experience trails digital-first competitors, impacting retention among younger segments.

Fee income depth

City Union Bank's revenue mix is heavily skewed to interest income, with non‑interest fee lines contributing under one-quarter of total income in FY2024, limiting potential ROA uplift. Limited penetration in wealth, payments and FX fees caps fee growth, while volatile credit costs have outsized impact on profits. Diversifying non‑interest streams is essential.

- Revenue mix: interest‑dominant (FY2024)

- Low wealth/payments/FX fee penetration

- Volatile credit costs amplify profit swings

- Priority: expand non‑interest income

Brand visibility

- Limited national recognition

- ~860 branches (Mar 2024)

- Acquisition costs +≈20% outside core

- Requires multi-year trust investment

Regional bank faces scale limits, margin pressure from high costs and low fee income

City Union Bank is regionally concentrated in Tamil Nadu, limiting diversification and exposing it to local downturns. A smaller balance sheet (~₹1.1 lakh crore FY24) and ~860 branches reduce pricing power and scale benefits. Cost-to-income (~48–52%) and non‑interest income under 25% constrain margins and fee diversification.

| Metric | Value (FY24) |

|---|---|

| Assets | ≈₹1.1 lakh crore |

| Branches | ≈860 |

| Non‑interest income | <25% |

| Cost-to-income | ≈48–52% |

Preview Before You Purchase

City Union Bank SWOT Analysis

This is the actual City Union Bank SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; purchase unlocks the complete, editable version. Buy now to access the full, detailed analysis.

Description

Dive Deeper Into the Company’s Strategic Blueprint

City Union Bank's SWOT highlights resilient regional banking strengths, niche retail franchise, and prudent asset quality, alongside competition, regulatory headwinds, and digital transformation needs. Want the full story behind its strengths, risks, and growth drivers? Purchase the complete SWOT analysis to gain a professionally written, editable report ideal for investors and strategists.

Strengths

Diverse product suite

City Union Bank, founded in 1904, offers deposits and loans across retail, agri and corporate segments alongside FX and transaction services, creating a full-service portfolio that drives multiple revenue streams and customer stickiness. Robust cross-sell opportunities raise customer lifetime value, while the mix of fee and interest income enhances resilience against cyclical credit shocks.

Strong regional franchise

Deep roots in South India since 1904 anchor City Union Bank's loyal MSME and retail base, supporting relationship banking and stable low-cost deposits. Local market knowledge enhances underwriting and collections, lowering credit costs and improving recoveries. Community trust from over 120 years of operations underpins steady growth through cycles.

Prudent risk culture

Conservative lending and a granular portfolio have kept City Union Banks GNPA at about 1.34% and NNPA near 0.30% (FY2024), while secured advances—around 85–87% of loans—lower loss given default; disciplined recovery and high PCR have helped contain credit costs, supporting consistent profitability with recurring RoA ~1.6%.

Digital enablement

City Union Bank leverages internet/mobile banking, a growing ATM network and open APIs to shorten turnaround times and automate routine services.

Digital onboarding and payments have expanded reach into semi-urban markets, increasing transaction volumes and lowering acquisition costs.

Data-led cross-sell initiatives lift fee income per customer while rising self-service use reduces cost-to-serve.

- APIs: faster service delivery

- Onboarding: wider reach, lower CAC

- Cross-sell: higher fees/customer

- Self-service: reduced cost-to-serve

SME and agri expertise

City Union Bank’s deep specialization in MSME and agriculture lending creates a durable niche, with tailored loan products and faster credit decisions attracting higher-quality borrowers and repeat business.

Collateral-backed structures and focused risk underwriting reduce portfolio volatility, while long-standing ecosystem relationships with traders, input suppliers and local businesses strengthen customer retention and cross-sell opportunities.

- SME/MSME focus

- Tailored products & fast decisions

- Collateral-backed risk mitigation

- Ecosystem-driven retention

Diversified retail, MSME & corporate lender; GNPA 1.34%, RoA ~1.6%

City Union Bank combines diversified retail, MSME and corporate lending with fee income and digital channels, driving customer stickiness and cross-sell. Conservative underwriting yields GNPA ~1.34% and NNPA ~0.30% (FY2024) with secured advances ~85–87%, supporting recurring RoA ~1.6%. Deep South India franchise and API-led digital services lower acquisition and servicing costs while boosting recoveries.

| Metric | Value | Period |

|---|---|---|

| GNPA | 1.34% | FY2024 |

| NNPA | 0.30% | FY2024 |

| Secured advances | 85–87% | FY2024 |

| RoA | ~1.6% | FY2024 |

What is included in the product

Delivers a strategic overview of City Union Bank’s internal strengths and weaknesses and examines external opportunities and threats shaping its competitive position and growth prospects.

Delivers a concise City Union Bank SWOT matrix for quick strategic alignment, easing stakeholder briefings and enabling fast, editable updates to reflect shifting market priorities.

Weaknesses

Geographic concentration

City Union Bank remains heavily concentrated in Tamil Nadu and the broader southern region, exposing it to heightened regional risk; local economic slowdowns or sectoral shocks can disproportionately dent growth and credit quality. Diversification across India is still a work-in-progress, with branch expansion beyond core markets progressing slowly relative to peers. This geographic skew constrains balance-sheet resilience and revenue diversification.

Scale limitations

City Union Bank's smaller balance sheet (≈₹1.1 lakh crore assets FY24) versus SBI/ICICI (≈₹70–80 lakh crore) reduces pricing power on deposits and loans, compressing spreads. Higher unit costs from 1,500+ branches push cost-to-income toward 48–52%, pressuring margins. Limited capital expenditure restricts investments in AI and real-time payments, and brand scale makes attracting senior fintech talent harder against larger banks.

Legacy processes

Operational workflows at City Union Bank still retain manual dependencies, causing inefficiencies and higher processing costs. Integration challenges across legacy systems slow product launches and limit API-driven partnerships. Rigidity in processes raises turnaround times for loan disbursals and account services. Customer experience trails digital-first competitors, impacting retention among younger segments.

Fee income depth

City Union Bank's revenue mix is heavily skewed to interest income, with non‑interest fee lines contributing under one-quarter of total income in FY2024, limiting potential ROA uplift. Limited penetration in wealth, payments and FX fees caps fee growth, while volatile credit costs have outsized impact on profits. Diversifying non‑interest streams is essential.

- Revenue mix: interest‑dominant (FY2024)

- Low wealth/payments/FX fee penetration

- Volatile credit costs amplify profit swings

- Priority: expand non‑interest income

Brand visibility

- Limited national recognition

- ~860 branches (Mar 2024)

- Acquisition costs +≈20% outside core

- Requires multi-year trust investment

Regional bank faces scale limits, margin pressure from high costs and low fee income

City Union Bank is regionally concentrated in Tamil Nadu, limiting diversification and exposing it to local downturns. A smaller balance sheet (~₹1.1 lakh crore FY24) and ~860 branches reduce pricing power and scale benefits. Cost-to-income (~48–52%) and non‑interest income under 25% constrain margins and fee diversification.

| Metric | Value (FY24) |

|---|---|

| Assets | ≈₹1.1 lakh crore |

| Branches | ≈860 |

| Non‑interest income | <25% |

| Cost-to-income | ≈48–52% |

Preview Before You Purchase

City Union Bank SWOT Analysis

This is the actual City Union Bank SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; purchase unlocks the complete, editable version. Buy now to access the full, detailed analysis.