CJ Cheiljedang PESTLE Analysis

Your Competitive Advantage Starts with This Report

Our PESTLE analysis of CJ Cheiljedang reveals how political regulations, shifting consumer tastes, and technological advances are reshaping its food and biotech strategies. Actionable insights highlight risks and growth levers for investors and strategists. Download the full report for the complete, ready-to-use breakdown.

Political factors

Global trade policy and tariffs

Food and bio-ingredient exports face shifting tariffs, non-tariff barriers and customs rules across the U.S., EU, China and ASEAN, complicating clearance times. South Korea-led FTAs (RCEP ~30% of global GDP, CPTPP ~13% in 2024) and bilateral deals covering over 60% of Korean trade can cut duties on processed foods and amino acids, improving price competitiveness. Rising protectionism and SPS measures in 2023–24 have increased compliance costs and delays. CJ CheilJedang needs agile trade compliance and diversified routing to mitigate shocks.

Geopolitical tensions and supply security

U.S.–China rivalry, Korea–Japan frictions and the Russia–Ukraine war have tightened availability of grain, energy and logistics corridors, with Russia and Ukraine supplying about 15% of global wheat and corn exports pre-2022 and Black Sea shipments collapsing by roughly two-thirds in early 2022. Sanctions and export controls have intermittently stalled bio-inputs and equipment shipments, forcing firms to secure multi-source procurement and strategic inventories. CJ CheilJedang must model shipping-lane disruptions and currency swings (KRW ~1,300 per USD in 2024) in scenario plans to protect margins and continuity.

Food sovereignty and agricultural policy

Host governments in 2024 accelerated food-sovereignty measures—over 50 countries tightened local-production, subsidy and import-license rules for staples and feed—tilting market access for sugar, flour and animal feed toward domestic suppliers. Localization partnerships and in‑market manufacturing by CJ CheilJedang can capture incentives when tied to demonstrable jobs, technology transfer and food‑security contributions, which governments increasingly quantify when awarding quotas and subsidies.

Public health and nutrition agendas

National drives—WHO 30% salt-intake reduction target by 2025 and over 50 countries with sugar taxes by 2024—force CJ CheilJedang to reformulate to cut salt, sugar and industrial trans fats; school-meal standards and labeling scorecards shift SKUs; alignment wins institutional contracts and reputational capital, while non-compliance risks fines and shelf-space loss.

- WHO target: 30% salt reduction by 2025

- 50+ countries with SSB taxes (2024)

- Reformulation required to keep institutional contracts

- Penalties and delisting risk for non-compliance

Industrial and biotech policy support

Many countries court bio-manufacturing via grants, tax credits and infrastructure programs to attract investment. Precision fermentation and green bio-chemicals often qualify for incentives, with over 50 countries now publishing national bioeconomy strategies. Strategic-sector designation can materially lower capex and opex and streamline permitting and workforce development.

- Grants & tax credits

- Precision fermentation eligible

- Lower capex/opex

- Faster permits & training

RCEP, FX strain and SSB taxes push diversified sourcing, reformulation and local production

Trade barriers, shifting tariffs and FTAs (RCEP ~30% global GDP, CPTPP ~13% in 2024) change margins and clearance times; KRW ~1,300/USD (2024) raises FX risk. Geopolitical strains and sanctions disrupt grain and input flows, requiring multi-source procurement and inventory buffers. Food‑sovereignty measures and health regulation (50+ SSB taxes by 2024) push reformulation and local production incentives.

| Issue | 2024/25 data | Action |

|---|---|---|

| FTAs | RCEP ~30% GDP; CPTPP ~13% | Use duty savings, diversify routes |

| FX & supply | KRW ~1,300/USD; Black Sea shocks | Hedge FX; multi-source sourcing |

| Regulation | 50+ SSB taxes; WHO salt target 2025 | Reformulate; localize production |

| Incentives | 50+ national bioeconomy strategies | Access grants, tax credits |

What is included in the product

Provides a concise PESTLE assessment of CJ CheilJedang, examining Political, Economic, Social, Technological, Environmental, and Legal drivers and their specific implications for the company’s food, bio, and biotech businesses. Each section links to current trends and data to help executives and investors identify strategic risks, opportunities, and scenario-ready actions.

Concise, visually segmented PESTLE summary for CJ CheilJedang that streamlines external risk assessment and market positioning discussions, easily dropped into presentations or shared across teams for quick alignment and decision-making.

Economic factors

Commodity and energy price volatility

Corn (~$5.50/bu), soy (~$12.50/bu), wheat (~$7/bu), sugar (~16¢/lb) and Brent crude (~$80/bbl in 2024–25) drive CJ CheilJedang’s COGS across food and feed; war, extreme weather and rising biofuel mandates have amplified swings. Hedging, long-term supply contracts and vertical integration help stabilize margins, while ability to pass costs depends on brand strength and retail vs foodservice channel mix.

FX fluctuations and revenue mix

KRW volatility versus the USD (around 1,330 KRW/USD in mid‑2025) and EUR (EUR near 1.09 USD) raises import cost and reduces translated overseas earnings for CJ CheilJedang, especially in raw materials procurement. A diverse geographic footprint (APAC, Americas, Europe) provides a natural hedge by matching revenues to costs regionally. Financial hedges and USD/EUR pricing clauses have been used to protect cash flows, while parity shifts inform plant siting and sourcing decisions.

Consumer demand cycles

Inflationary pressure—South Korea CPI 2024 +2.6% while real wages fell ~0.8%—has trimmed volumes in convenience and premium lines but boosted at-home staples demand. Downtrading fuels private-label gains (share up toward mid-teens in some markets) while value-pack and mid-tier innovation protected CJ CheilJedang’s category share. Price elasticity varies widely by market, requiring localized pricing analytics and SKU-level promotion optimization.

Emerging market growth

Rising incomes in India (population ~1.4 billion) and Southeast Asia (~680 million) expand addressable markets for processed foods and amino acids as IMF 2024 GDP growth estimates show India ~6.8% and ASEAN ~4.5%, raising per‑capita spending power.

Distribution buildout and localized flavors increase penetration; currency and regulatory risks are higher but can be offset by scale economics and volume growth.

Joint ventures and licensing accelerate market entry, reducing capex and regulatory friction while leveraging local know‑how.

- Market size drivers: population and GDP growth

- Opportunities: distribution + localization

- Risks: currency & regulation

- Mitigants: scale economics, joint ventures

Capital costs and capex intensity

Interest rates materially affect returns on new fermentation and processing capacity, altering project IRRs and hurdle rates. Bio plants and cold-chain logistics demand large upfront investment and long payback periods. Access to green finance linked to sustainability KPIs can reduce WACC. Phased capex and brownfield upgrades shorten payback and lower execution risk.

- Interest sensitivity

- High capex intensity

- Green finance upside

- Phased/brownfield advantage

RCEP, FX strain and SSB taxes push diversified sourcing, reformulation and local production

CJ CheilJedang’s margins remain commodity‑sensitive (corn $5.50/bu, soy $12.50, wheat $7, Brent $80/bbl), FX risk (KRW ~1,330/USD mid‑2025) and local inflation (KR CPI 2024 +2.6%, real wages -0.8%) constrain pricing power; India GDP ~6.8% and ASEAN ~4.5% expand demand; higher rates (BOK ~3.5%) raise project IRRs, green finance reduces WACC.

| Metric | Value |

|---|---|

| Corn | $5.50/bu |

| Brent | $80/bbl |

| KRW/USD | ~1,330 |

| KR CPI 2024 | +2.6% |

| India GDP (IMF 2024) | 6.8% |

| BOK rate | ~3.5% |

Same Document Delivered

CJ Cheiljedang PESTLE Analysis

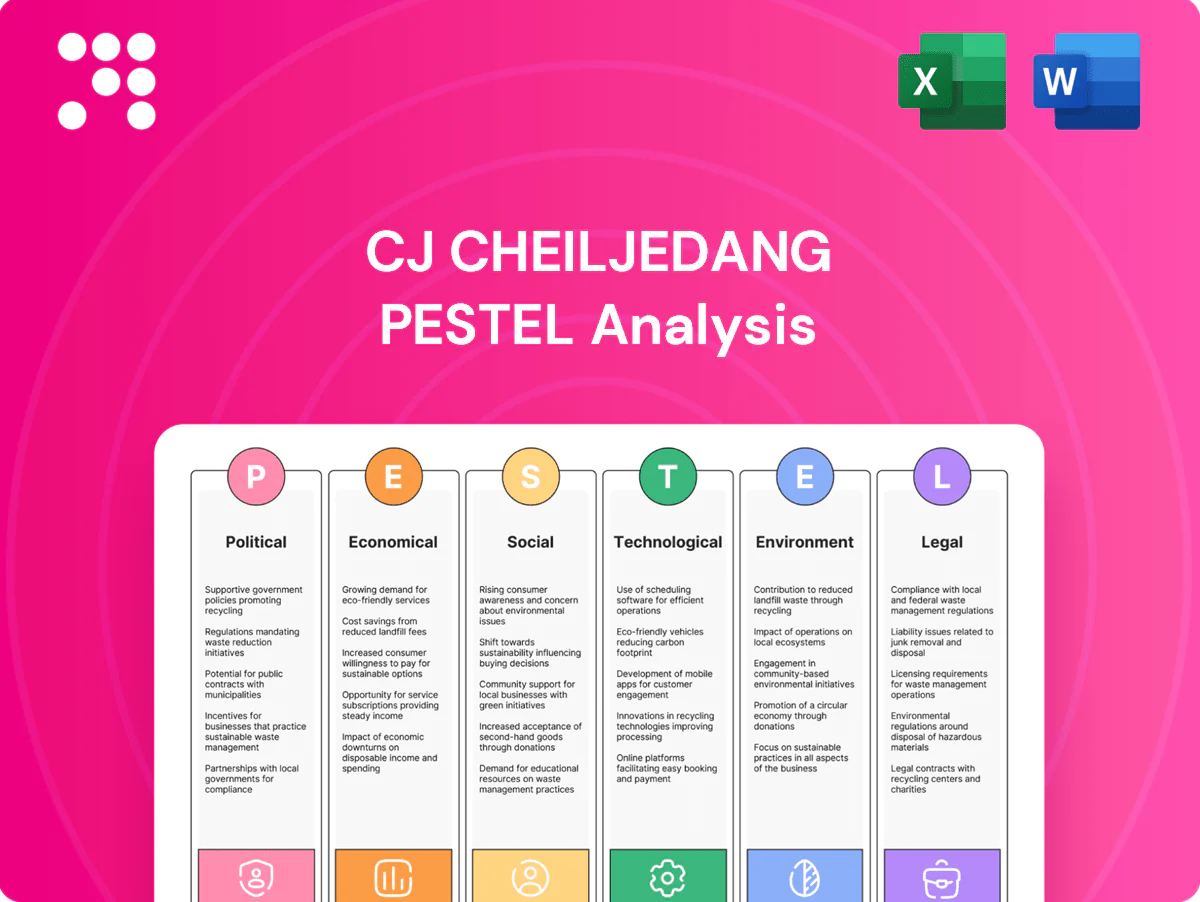

The preview shown here is the exact CJ Cheiljedang PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It covers political, economic, social, technological, legal, and environmental factors with clear headings and actionable insights. No placeholders or teasers; this is the final, downloadable file you’ll get immediately after checkout.

Your Competitive Advantage Starts with This Report

Our PESTLE analysis of CJ Cheiljedang reveals how political regulations, shifting consumer tastes, and technological advances are reshaping its food and biotech strategies. Actionable insights highlight risks and growth levers for investors and strategists. Download the full report for the complete, ready-to-use breakdown.

Political factors

Global trade policy and tariffs

Food and bio-ingredient exports face shifting tariffs, non-tariff barriers and customs rules across the U.S., EU, China and ASEAN, complicating clearance times. South Korea-led FTAs (RCEP ~30% of global GDP, CPTPP ~13% in 2024) and bilateral deals covering over 60% of Korean trade can cut duties on processed foods and amino acids, improving price competitiveness. Rising protectionism and SPS measures in 2023–24 have increased compliance costs and delays. CJ CheilJedang needs agile trade compliance and diversified routing to mitigate shocks.

Geopolitical tensions and supply security

U.S.–China rivalry, Korea–Japan frictions and the Russia–Ukraine war have tightened availability of grain, energy and logistics corridors, with Russia and Ukraine supplying about 15% of global wheat and corn exports pre-2022 and Black Sea shipments collapsing by roughly two-thirds in early 2022. Sanctions and export controls have intermittently stalled bio-inputs and equipment shipments, forcing firms to secure multi-source procurement and strategic inventories. CJ CheilJedang must model shipping-lane disruptions and currency swings (KRW ~1,300 per USD in 2024) in scenario plans to protect margins and continuity.

Food sovereignty and agricultural policy

Host governments in 2024 accelerated food-sovereignty measures—over 50 countries tightened local-production, subsidy and import-license rules for staples and feed—tilting market access for sugar, flour and animal feed toward domestic suppliers. Localization partnerships and in‑market manufacturing by CJ CheilJedang can capture incentives when tied to demonstrable jobs, technology transfer and food‑security contributions, which governments increasingly quantify when awarding quotas and subsidies.

Public health and nutrition agendas

National drives—WHO 30% salt-intake reduction target by 2025 and over 50 countries with sugar taxes by 2024—force CJ CheilJedang to reformulate to cut salt, sugar and industrial trans fats; school-meal standards and labeling scorecards shift SKUs; alignment wins institutional contracts and reputational capital, while non-compliance risks fines and shelf-space loss.

- WHO target: 30% salt reduction by 2025

- 50+ countries with SSB taxes (2024)

- Reformulation required to keep institutional contracts

- Penalties and delisting risk for non-compliance

Industrial and biotech policy support

Many countries court bio-manufacturing via grants, tax credits and infrastructure programs to attract investment. Precision fermentation and green bio-chemicals often qualify for incentives, with over 50 countries now publishing national bioeconomy strategies. Strategic-sector designation can materially lower capex and opex and streamline permitting and workforce development.

- Grants & tax credits

- Precision fermentation eligible

- Lower capex/opex

- Faster permits & training

RCEP, FX strain and SSB taxes push diversified sourcing, reformulation and local production

Trade barriers, shifting tariffs and FTAs (RCEP ~30% global GDP, CPTPP ~13% in 2024) change margins and clearance times; KRW ~1,300/USD (2024) raises FX risk. Geopolitical strains and sanctions disrupt grain and input flows, requiring multi-source procurement and inventory buffers. Food‑sovereignty measures and health regulation (50+ SSB taxes by 2024) push reformulation and local production incentives.

| Issue | 2024/25 data | Action |

|---|---|---|

| FTAs | RCEP ~30% GDP; CPTPP ~13% | Use duty savings, diversify routes |

| FX & supply | KRW ~1,300/USD; Black Sea shocks | Hedge FX; multi-source sourcing |

| Regulation | 50+ SSB taxes; WHO salt target 2025 | Reformulate; localize production |

| Incentives | 50+ national bioeconomy strategies | Access grants, tax credits |

What is included in the product

Provides a concise PESTLE assessment of CJ CheilJedang, examining Political, Economic, Social, Technological, Environmental, and Legal drivers and their specific implications for the company’s food, bio, and biotech businesses. Each section links to current trends and data to help executives and investors identify strategic risks, opportunities, and scenario-ready actions.

Concise, visually segmented PESTLE summary for CJ CheilJedang that streamlines external risk assessment and market positioning discussions, easily dropped into presentations or shared across teams for quick alignment and decision-making.

Economic factors

Commodity and energy price volatility

Corn (~$5.50/bu), soy (~$12.50/bu), wheat (~$7/bu), sugar (~16¢/lb) and Brent crude (~$80/bbl in 2024–25) drive CJ CheilJedang’s COGS across food and feed; war, extreme weather and rising biofuel mandates have amplified swings. Hedging, long-term supply contracts and vertical integration help stabilize margins, while ability to pass costs depends on brand strength and retail vs foodservice channel mix.

FX fluctuations and revenue mix

KRW volatility versus the USD (around 1,330 KRW/USD in mid‑2025) and EUR (EUR near 1.09 USD) raises import cost and reduces translated overseas earnings for CJ CheilJedang, especially in raw materials procurement. A diverse geographic footprint (APAC, Americas, Europe) provides a natural hedge by matching revenues to costs regionally. Financial hedges and USD/EUR pricing clauses have been used to protect cash flows, while parity shifts inform plant siting and sourcing decisions.

Consumer demand cycles

Inflationary pressure—South Korea CPI 2024 +2.6% while real wages fell ~0.8%—has trimmed volumes in convenience and premium lines but boosted at-home staples demand. Downtrading fuels private-label gains (share up toward mid-teens in some markets) while value-pack and mid-tier innovation protected CJ CheilJedang’s category share. Price elasticity varies widely by market, requiring localized pricing analytics and SKU-level promotion optimization.

Emerging market growth

Rising incomes in India (population ~1.4 billion) and Southeast Asia (~680 million) expand addressable markets for processed foods and amino acids as IMF 2024 GDP growth estimates show India ~6.8% and ASEAN ~4.5%, raising per‑capita spending power.

Distribution buildout and localized flavors increase penetration; currency and regulatory risks are higher but can be offset by scale economics and volume growth.

Joint ventures and licensing accelerate market entry, reducing capex and regulatory friction while leveraging local know‑how.

- Market size drivers: population and GDP growth

- Opportunities: distribution + localization

- Risks: currency & regulation

- Mitigants: scale economics, joint ventures

Capital costs and capex intensity

Interest rates materially affect returns on new fermentation and processing capacity, altering project IRRs and hurdle rates. Bio plants and cold-chain logistics demand large upfront investment and long payback periods. Access to green finance linked to sustainability KPIs can reduce WACC. Phased capex and brownfield upgrades shorten payback and lower execution risk.

- Interest sensitivity

- High capex intensity

- Green finance upside

- Phased/brownfield advantage

RCEP, FX strain and SSB taxes push diversified sourcing, reformulation and local production

CJ CheilJedang’s margins remain commodity‑sensitive (corn $5.50/bu, soy $12.50, wheat $7, Brent $80/bbl), FX risk (KRW ~1,330/USD mid‑2025) and local inflation (KR CPI 2024 +2.6%, real wages -0.8%) constrain pricing power; India GDP ~6.8% and ASEAN ~4.5% expand demand; higher rates (BOK ~3.5%) raise project IRRs, green finance reduces WACC.

| Metric | Value |

|---|---|

| Corn | $5.50/bu |

| Brent | $80/bbl |

| KRW/USD | ~1,330 |

| KR CPI 2024 | +2.6% |

| India GDP (IMF 2024) | 6.8% |

| BOK rate | ~3.5% |

Same Document Delivered

CJ Cheiljedang PESTLE Analysis

The preview shown here is the exact CJ Cheiljedang PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It covers political, economic, social, technological, legal, and environmental factors with clear headings and actionable insights. No placeholders or teasers; this is the final, downloadable file you’ll get immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Your Competitive Advantage Starts with This Report

Our PESTLE analysis of CJ Cheiljedang reveals how political regulations, shifting consumer tastes, and technological advances are reshaping its food and biotech strategies. Actionable insights highlight risks and growth levers for investors and strategists. Download the full report for the complete, ready-to-use breakdown.

Political factors

Global trade policy and tariffs

Food and bio-ingredient exports face shifting tariffs, non-tariff barriers and customs rules across the U.S., EU, China and ASEAN, complicating clearance times. South Korea-led FTAs (RCEP ~30% of global GDP, CPTPP ~13% in 2024) and bilateral deals covering over 60% of Korean trade can cut duties on processed foods and amino acids, improving price competitiveness. Rising protectionism and SPS measures in 2023–24 have increased compliance costs and delays. CJ CheilJedang needs agile trade compliance and diversified routing to mitigate shocks.

Geopolitical tensions and supply security

U.S.–China rivalry, Korea–Japan frictions and the Russia–Ukraine war have tightened availability of grain, energy and logistics corridors, with Russia and Ukraine supplying about 15% of global wheat and corn exports pre-2022 and Black Sea shipments collapsing by roughly two-thirds in early 2022. Sanctions and export controls have intermittently stalled bio-inputs and equipment shipments, forcing firms to secure multi-source procurement and strategic inventories. CJ CheilJedang must model shipping-lane disruptions and currency swings (KRW ~1,300 per USD in 2024) in scenario plans to protect margins and continuity.

Food sovereignty and agricultural policy

Host governments in 2024 accelerated food-sovereignty measures—over 50 countries tightened local-production, subsidy and import-license rules for staples and feed—tilting market access for sugar, flour and animal feed toward domestic suppliers. Localization partnerships and in‑market manufacturing by CJ CheilJedang can capture incentives when tied to demonstrable jobs, technology transfer and food‑security contributions, which governments increasingly quantify when awarding quotas and subsidies.

Public health and nutrition agendas

National drives—WHO 30% salt-intake reduction target by 2025 and over 50 countries with sugar taxes by 2024—force CJ CheilJedang to reformulate to cut salt, sugar and industrial trans fats; school-meal standards and labeling scorecards shift SKUs; alignment wins institutional contracts and reputational capital, while non-compliance risks fines and shelf-space loss.

- WHO target: 30% salt reduction by 2025

- 50+ countries with SSB taxes (2024)

- Reformulation required to keep institutional contracts

- Penalties and delisting risk for non-compliance

Industrial and biotech policy support

Many countries court bio-manufacturing via grants, tax credits and infrastructure programs to attract investment. Precision fermentation and green bio-chemicals often qualify for incentives, with over 50 countries now publishing national bioeconomy strategies. Strategic-sector designation can materially lower capex and opex and streamline permitting and workforce development.

- Grants & tax credits

- Precision fermentation eligible

- Lower capex/opex

- Faster permits & training

RCEP, FX strain and SSB taxes push diversified sourcing, reformulation and local production

Trade barriers, shifting tariffs and FTAs (RCEP ~30% global GDP, CPTPP ~13% in 2024) change margins and clearance times; KRW ~1,300/USD (2024) raises FX risk. Geopolitical strains and sanctions disrupt grain and input flows, requiring multi-source procurement and inventory buffers. Food‑sovereignty measures and health regulation (50+ SSB taxes by 2024) push reformulation and local production incentives.

| Issue | 2024/25 data | Action |

|---|---|---|

| FTAs | RCEP ~30% GDP; CPTPP ~13% | Use duty savings, diversify routes |

| FX & supply | KRW ~1,300/USD; Black Sea shocks | Hedge FX; multi-source sourcing |

| Regulation | 50+ SSB taxes; WHO salt target 2025 | Reformulate; localize production |

| Incentives | 50+ national bioeconomy strategies | Access grants, tax credits |

What is included in the product

Provides a concise PESTLE assessment of CJ CheilJedang, examining Political, Economic, Social, Technological, Environmental, and Legal drivers and their specific implications for the company’s food, bio, and biotech businesses. Each section links to current trends and data to help executives and investors identify strategic risks, opportunities, and scenario-ready actions.

Concise, visually segmented PESTLE summary for CJ CheilJedang that streamlines external risk assessment and market positioning discussions, easily dropped into presentations or shared across teams for quick alignment and decision-making.

Economic factors

Commodity and energy price volatility

Corn (~$5.50/bu), soy (~$12.50/bu), wheat (~$7/bu), sugar (~16¢/lb) and Brent crude (~$80/bbl in 2024–25) drive CJ CheilJedang’s COGS across food and feed; war, extreme weather and rising biofuel mandates have amplified swings. Hedging, long-term supply contracts and vertical integration help stabilize margins, while ability to pass costs depends on brand strength and retail vs foodservice channel mix.

FX fluctuations and revenue mix

KRW volatility versus the USD (around 1,330 KRW/USD in mid‑2025) and EUR (EUR near 1.09 USD) raises import cost and reduces translated overseas earnings for CJ CheilJedang, especially in raw materials procurement. A diverse geographic footprint (APAC, Americas, Europe) provides a natural hedge by matching revenues to costs regionally. Financial hedges and USD/EUR pricing clauses have been used to protect cash flows, while parity shifts inform plant siting and sourcing decisions.

Consumer demand cycles

Inflationary pressure—South Korea CPI 2024 +2.6% while real wages fell ~0.8%—has trimmed volumes in convenience and premium lines but boosted at-home staples demand. Downtrading fuels private-label gains (share up toward mid-teens in some markets) while value-pack and mid-tier innovation protected CJ CheilJedang’s category share. Price elasticity varies widely by market, requiring localized pricing analytics and SKU-level promotion optimization.

Emerging market growth

Rising incomes in India (population ~1.4 billion) and Southeast Asia (~680 million) expand addressable markets for processed foods and amino acids as IMF 2024 GDP growth estimates show India ~6.8% and ASEAN ~4.5%, raising per‑capita spending power.

Distribution buildout and localized flavors increase penetration; currency and regulatory risks are higher but can be offset by scale economics and volume growth.

Joint ventures and licensing accelerate market entry, reducing capex and regulatory friction while leveraging local know‑how.

- Market size drivers: population and GDP growth

- Opportunities: distribution + localization

- Risks: currency & regulation

- Mitigants: scale economics, joint ventures

Capital costs and capex intensity

Interest rates materially affect returns on new fermentation and processing capacity, altering project IRRs and hurdle rates. Bio plants and cold-chain logistics demand large upfront investment and long payback periods. Access to green finance linked to sustainability KPIs can reduce WACC. Phased capex and brownfield upgrades shorten payback and lower execution risk.

- Interest sensitivity

- High capex intensity

- Green finance upside

- Phased/brownfield advantage

RCEP, FX strain and SSB taxes push diversified sourcing, reformulation and local production

CJ CheilJedang’s margins remain commodity‑sensitive (corn $5.50/bu, soy $12.50, wheat $7, Brent $80/bbl), FX risk (KRW ~1,330/USD mid‑2025) and local inflation (KR CPI 2024 +2.6%, real wages -0.8%) constrain pricing power; India GDP ~6.8% and ASEAN ~4.5% expand demand; higher rates (BOK ~3.5%) raise project IRRs, green finance reduces WACC.

| Metric | Value |

|---|---|

| Corn | $5.50/bu |

| Brent | $80/bbl |

| KRW/USD | ~1,330 |

| KR CPI 2024 | +2.6% |

| India GDP (IMF 2024) | 6.8% |

| BOK rate | ~3.5% |

Same Document Delivered

CJ Cheiljedang PESTLE Analysis

The preview shown here is the exact CJ Cheiljedang PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It covers political, economic, social, technological, legal, and environmental factors with clear headings and actionable insights. No placeholders or teasers; this is the final, downloadable file you’ll get immediately after checkout.