CJ Logistics Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

CJ Logistics faces moderate supplier power, intense rivalry among global logistics players, and evolving threats from digital disruptors that reshape pricing and service models. This snapshot highlights key pressures but only scratches the surface. Unlock the full Porter’s Five Forces Analysis to explore CJ Logistics’s competitive dynamics and strategic opportunities in detail.

Suppliers Bargaining Power

Fuel and energy dependency

Jet fuel, diesel and electricity suppliers exert leverage through price volatility—Brent crude averaged about $86/barrel in 2024—pushing carrier surcharges and squeezing margins. Long-term hedging and diversified procurement reduce but do not eliminate exposure, as spikes still force spot premiums. Power utilities at warehouses/hubs command essential inputs and can levy tariff increases. CJ Logistics must pass costs via surcharges or optimize routing and load factors to offset spikes.

Transportation capacity providers

Airlines, ocean carriers, rail operators and port terminals control scarce peak-season slots — utilization often exceeds 85%, pushing spot rates and prioritization fees higher and increasing supplier power. Tight capacity in 2024 kept ocean and air premiums above pre-pandemic levels, while multi-carrier contracts and volume commitments improve access but restrict flexibility. Strategic alliances and guaranteed-space agreements are key countermeasures.

Equipment and technology vendors

Automation OEMs, WMS/TMS and sorting-system vendors create material switching costs—often running $0.5–3.0M per large DC for re‑engineering and integration—strengthening supplier power over CJ Logistics. Proprietary software and multi‑year maintenance contracts commonly add 10–20% of initial CAPEX annually, locking in higher lifecycle costs. Open APIs and modular tech stacks have reduced dependency where adopted, cutting integration time by ~30%. Competitive bidding and dual‑sourcing critical spares are used to balance supplier leverage.

Real estate and infrastructure landlords

- Vacancy <3% (2024)

- Prime rent rise ≈6% (2024)

- Long leases 5–15 years

- Secondary markets cut rents 10–30%

Labor and staffing agencies

Skilled drivers, warehouse operatives and peak-season temps materially affect CJ Logistics service levels; tight South Korea labor markets (2024 unemployment ~2.9%) and hours/safety regulations raise wage pressure and staffing costs. Union presence and regional labor norms add constraints, while automation, training pipelines and multi-skilling reduce supplier leverage.

- Skilled drivers: critical

- Peak temps: seasonal pressure

- Wage/headline pressure: up

- Automation/training: mitigants

Suppliers tighten logistics: Brent $86, prime rent +6%, vacancy <3%

Suppliers (fuel, carriers, automation vendors, land, labor) hold moderate-high power: Brent avg $86/bbl (2024) and prime logistics vacancy <3% pushed rents +6% (2024), integration costs $0.5–3M/DC, unemployment ~2.9% (2024); hedging, multi‑sourcing, long leases and automation mitigate but not eliminate risk.

| Metric | 2024 |

|---|---|

| Brent ($/bbl) | $86 |

| Vacancy | <3% |

| Prime rent YoY | +6% |

| Integration cost/DC | $0.5–3M |

| Unemployment KR | 2.9% |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, and entry/substitute threats specific to CJ Logistics, offering data-backed insights on pricing influence, barriers to entry, and emerging disruptors affecting its market position.

Clear, one-sheet Porter's Five Forces for CJ Logistics—instantly visualize competitive pressure with a spider chart and customizable force levels to adapt for regulation, new entrants, or route disruptions; ready to drop into pitch decks or boardroom slides without macros.

Customers Bargaining Power

Large shippers and e-commerce giants

Enterprise customers and e-commerce giants run competitive tenders that compress margins—global e-commerce sales reached about $5.7 trillion in 2024, amplifying volume-driven price pressure on 3PLs. Large shippers routinely multi-source across 3PLs, raising bargaining leverage and lowering switching costs. Stringent SLAs with financial penalties transfer operational risk to providers, while bespoke value-added services and vertical expertise remain the main levers to command premiums.

Price transparency and benchmarking

Market indices and digital platforms make rates comparable across providers; Xeneta's 2024 index showed global ocean spot rates about 50% below 2021 peaks. Buyers leverage benchmarks to negotiate margins, forcing carriers like CJ Logistics to justify spreads versus market rates. Detailed KPIs enable performance-based pricing pressure as shippers tie SLAs to OTIF and dwell times. Differentiated tech analytics and outcomes-based contracts reduce pure price focus.

Switching costs and integration

IT integration, co-designed processes and bespoke facility setups with CJ Logistics create meaningful switching friction by tying clients into shared systems across CJ’s network in over 40 countries, yet the rise of standardized APIs and common data formats is lowering technical barriers. Contractual exit clauses and phased transitions (commonly 3–5 year migration windows) still enable savvy buyers to switch. Deep integration and co-investment by customers increase long-term stickiness.

Service criticality and reliability

Time-sensitive sectors demand OTIF near 98% and damage rates below 0.5% in 2024, raising buyer expectations; missed SLAs trigger chargebacks often equivalent to 1–3% of shipment value and incur reputational costs that strengthen customer bargaining power. Redundant networks and resilient planning are essential to defend pricing, while proven performance supports long-term renewals.

- OTIF target 98%

- Damage rate <0.5%

- Chargebacks 1–3% of shipment value

- Redundancy = pricing defense

Demand cyclicality and volume volatility

Demand cyclicality forces CJ Logistics into flexible capacity commitments as peak seasons and promotional spikes can raise handling volumes by up to 30%, enabling buyers to demand surge handling without proportional price increases; forecast accuracy and collaborative planning therefore materially influence contract terms and penalty clauses. Dynamic pricing and capacity reservation models are increasingly used to balance buyer leverage versus carrier cost recovery.

- Peak spikes up to 30%

- Buyers demand surge handling

- Forecasting alters terms

- Dynamic pricing + reservations

E-commerce scale and strict SLAs squeeze 3PL margins; tech, dynamic pricing, capacity win

Enterprise buyers and e-commerce giants drive margin pressure through competitive tenders and multi-sourcing, amplified by $5.7T global e-commerce (2024) and ocean spot rates ~50% below 2021. Stringent SLAs (OTIF 98%, damage <0.5%) plus chargebacks (1–3%) shift risk to 3PLs; tech integration and bespoke services are primary premium levers. Peak spikes ~30% force flexible capacity, dynamic pricing and reservation models.

| Metric | Value |

|---|---|

| Global e‑commerce (2024) | $5.7T |

| Ocean spot vs 2021 | -50% |

| OTIF target | 98% |

| Damage rate | <0.5% |

| Chargebacks | 1–3% |

| Peak spikes | ~30% |

Preview the Actual Deliverable

CJ Logistics Porter's Five Forces Analysis

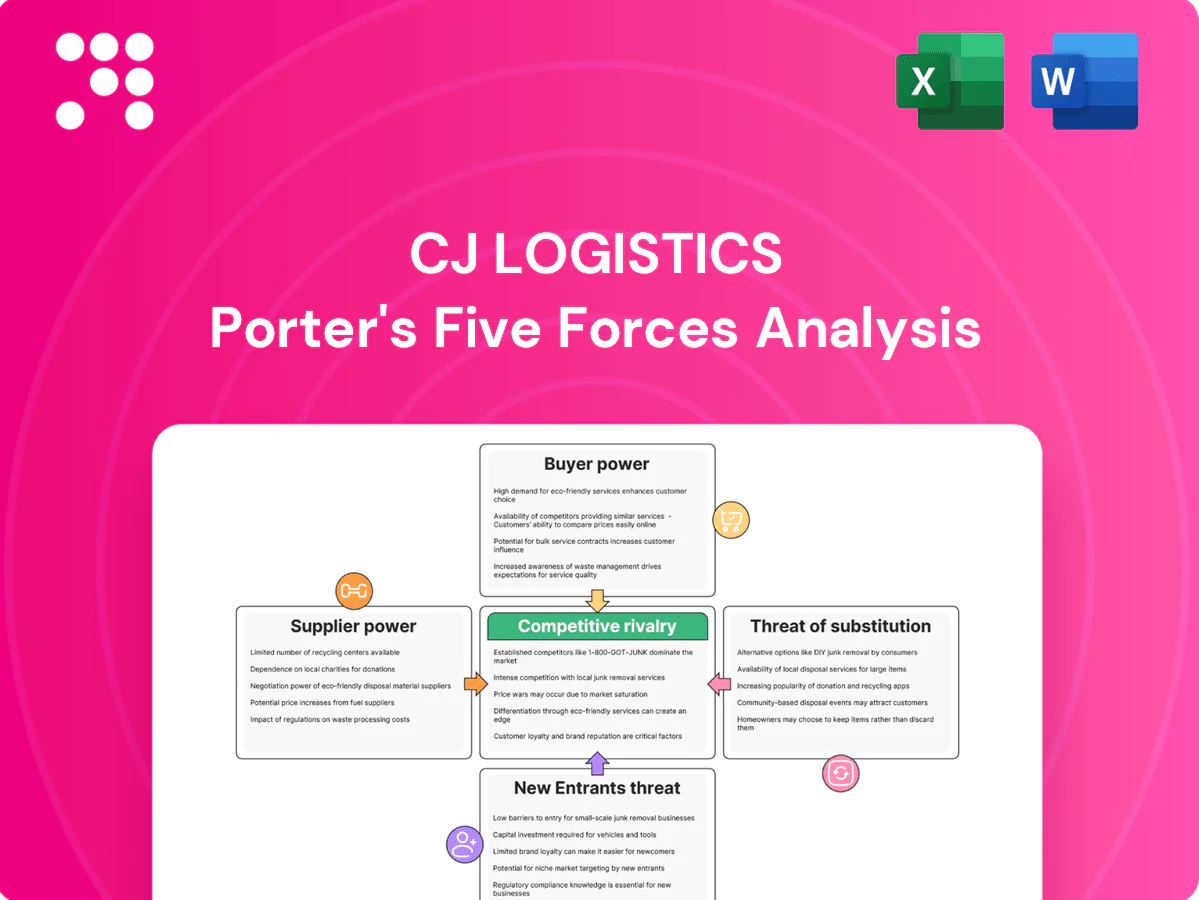

This preview shows the actual CJ Logistics Porter’s Five Forces analysis you’ll receive—fully formatted, comprehensive, and ready for immediate use. No samples or placeholders; the document here is identical to the file delivered after purchase. It contains in-depth evaluation of competitive rivalry, buyer and supplier power, and threats from entrants and substitutes.

Go Beyond the Preview—Access the Full Strategic Report

CJ Logistics faces moderate supplier power, intense rivalry among global logistics players, and evolving threats from digital disruptors that reshape pricing and service models. This snapshot highlights key pressures but only scratches the surface. Unlock the full Porter’s Five Forces Analysis to explore CJ Logistics’s competitive dynamics and strategic opportunities in detail.

Suppliers Bargaining Power

Fuel and energy dependency

Jet fuel, diesel and electricity suppliers exert leverage through price volatility—Brent crude averaged about $86/barrel in 2024—pushing carrier surcharges and squeezing margins. Long-term hedging and diversified procurement reduce but do not eliminate exposure, as spikes still force spot premiums. Power utilities at warehouses/hubs command essential inputs and can levy tariff increases. CJ Logistics must pass costs via surcharges or optimize routing and load factors to offset spikes.

Transportation capacity providers

Airlines, ocean carriers, rail operators and port terminals control scarce peak-season slots — utilization often exceeds 85%, pushing spot rates and prioritization fees higher and increasing supplier power. Tight capacity in 2024 kept ocean and air premiums above pre-pandemic levels, while multi-carrier contracts and volume commitments improve access but restrict flexibility. Strategic alliances and guaranteed-space agreements are key countermeasures.

Equipment and technology vendors

Automation OEMs, WMS/TMS and sorting-system vendors create material switching costs—often running $0.5–3.0M per large DC for re‑engineering and integration—strengthening supplier power over CJ Logistics. Proprietary software and multi‑year maintenance contracts commonly add 10–20% of initial CAPEX annually, locking in higher lifecycle costs. Open APIs and modular tech stacks have reduced dependency where adopted, cutting integration time by ~30%. Competitive bidding and dual‑sourcing critical spares are used to balance supplier leverage.

Real estate and infrastructure landlords

- Vacancy <3% (2024)

- Prime rent rise ≈6% (2024)

- Long leases 5–15 years

- Secondary markets cut rents 10–30%

Labor and staffing agencies

Skilled drivers, warehouse operatives and peak-season temps materially affect CJ Logistics service levels; tight South Korea labor markets (2024 unemployment ~2.9%) and hours/safety regulations raise wage pressure and staffing costs. Union presence and regional labor norms add constraints, while automation, training pipelines and multi-skilling reduce supplier leverage.

- Skilled drivers: critical

- Peak temps: seasonal pressure

- Wage/headline pressure: up

- Automation/training: mitigants

Suppliers tighten logistics: Brent $86, prime rent +6%, vacancy <3%

Suppliers (fuel, carriers, automation vendors, land, labor) hold moderate-high power: Brent avg $86/bbl (2024) and prime logistics vacancy <3% pushed rents +6% (2024), integration costs $0.5–3M/DC, unemployment ~2.9% (2024); hedging, multi‑sourcing, long leases and automation mitigate but not eliminate risk.

| Metric | 2024 |

|---|---|

| Brent ($/bbl) | $86 |

| Vacancy | <3% |

| Prime rent YoY | +6% |

| Integration cost/DC | $0.5–3M |

| Unemployment KR | 2.9% |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, and entry/substitute threats specific to CJ Logistics, offering data-backed insights on pricing influence, barriers to entry, and emerging disruptors affecting its market position.

Clear, one-sheet Porter's Five Forces for CJ Logistics—instantly visualize competitive pressure with a spider chart and customizable force levels to adapt for regulation, new entrants, or route disruptions; ready to drop into pitch decks or boardroom slides without macros.

Customers Bargaining Power

Large shippers and e-commerce giants

Enterprise customers and e-commerce giants run competitive tenders that compress margins—global e-commerce sales reached about $5.7 trillion in 2024, amplifying volume-driven price pressure on 3PLs. Large shippers routinely multi-source across 3PLs, raising bargaining leverage and lowering switching costs. Stringent SLAs with financial penalties transfer operational risk to providers, while bespoke value-added services and vertical expertise remain the main levers to command premiums.

Price transparency and benchmarking

Market indices and digital platforms make rates comparable across providers; Xeneta's 2024 index showed global ocean spot rates about 50% below 2021 peaks. Buyers leverage benchmarks to negotiate margins, forcing carriers like CJ Logistics to justify spreads versus market rates. Detailed KPIs enable performance-based pricing pressure as shippers tie SLAs to OTIF and dwell times. Differentiated tech analytics and outcomes-based contracts reduce pure price focus.

Switching costs and integration

IT integration, co-designed processes and bespoke facility setups with CJ Logistics create meaningful switching friction by tying clients into shared systems across CJ’s network in over 40 countries, yet the rise of standardized APIs and common data formats is lowering technical barriers. Contractual exit clauses and phased transitions (commonly 3–5 year migration windows) still enable savvy buyers to switch. Deep integration and co-investment by customers increase long-term stickiness.

Service criticality and reliability

Time-sensitive sectors demand OTIF near 98% and damage rates below 0.5% in 2024, raising buyer expectations; missed SLAs trigger chargebacks often equivalent to 1–3% of shipment value and incur reputational costs that strengthen customer bargaining power. Redundant networks and resilient planning are essential to defend pricing, while proven performance supports long-term renewals.

- OTIF target 98%

- Damage rate <0.5%

- Chargebacks 1–3% of shipment value

- Redundancy = pricing defense

Demand cyclicality and volume volatility

Demand cyclicality forces CJ Logistics into flexible capacity commitments as peak seasons and promotional spikes can raise handling volumes by up to 30%, enabling buyers to demand surge handling without proportional price increases; forecast accuracy and collaborative planning therefore materially influence contract terms and penalty clauses. Dynamic pricing and capacity reservation models are increasingly used to balance buyer leverage versus carrier cost recovery.

- Peak spikes up to 30%

- Buyers demand surge handling

- Forecasting alters terms

- Dynamic pricing + reservations

E-commerce scale and strict SLAs squeeze 3PL margins; tech, dynamic pricing, capacity win

Enterprise buyers and e-commerce giants drive margin pressure through competitive tenders and multi-sourcing, amplified by $5.7T global e-commerce (2024) and ocean spot rates ~50% below 2021. Stringent SLAs (OTIF 98%, damage <0.5%) plus chargebacks (1–3%) shift risk to 3PLs; tech integration and bespoke services are primary premium levers. Peak spikes ~30% force flexible capacity, dynamic pricing and reservation models.

| Metric | Value |

|---|---|

| Global e‑commerce (2024) | $5.7T |

| Ocean spot vs 2021 | -50% |

| OTIF target | 98% |

| Damage rate | <0.5% |

| Chargebacks | 1–3% |

| Peak spikes | ~30% |

Preview the Actual Deliverable

CJ Logistics Porter's Five Forces Analysis

This preview shows the actual CJ Logistics Porter’s Five Forces analysis you’ll receive—fully formatted, comprehensive, and ready for immediate use. No samples or placeholders; the document here is identical to the file delivered after purchase. It contains in-depth evaluation of competitive rivalry, buyer and supplier power, and threats from entrants and substitutes.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

CJ Logistics faces moderate supplier power, intense rivalry among global logistics players, and evolving threats from digital disruptors that reshape pricing and service models. This snapshot highlights key pressures but only scratches the surface. Unlock the full Porter’s Five Forces Analysis to explore CJ Logistics’s competitive dynamics and strategic opportunities in detail.

Suppliers Bargaining Power

Fuel and energy dependency

Jet fuel, diesel and electricity suppliers exert leverage through price volatility—Brent crude averaged about $86/barrel in 2024—pushing carrier surcharges and squeezing margins. Long-term hedging and diversified procurement reduce but do not eliminate exposure, as spikes still force spot premiums. Power utilities at warehouses/hubs command essential inputs and can levy tariff increases. CJ Logistics must pass costs via surcharges or optimize routing and load factors to offset spikes.

Transportation capacity providers

Airlines, ocean carriers, rail operators and port terminals control scarce peak-season slots — utilization often exceeds 85%, pushing spot rates and prioritization fees higher and increasing supplier power. Tight capacity in 2024 kept ocean and air premiums above pre-pandemic levels, while multi-carrier contracts and volume commitments improve access but restrict flexibility. Strategic alliances and guaranteed-space agreements are key countermeasures.

Equipment and technology vendors

Automation OEMs, WMS/TMS and sorting-system vendors create material switching costs—often running $0.5–3.0M per large DC for re‑engineering and integration—strengthening supplier power over CJ Logistics. Proprietary software and multi‑year maintenance contracts commonly add 10–20% of initial CAPEX annually, locking in higher lifecycle costs. Open APIs and modular tech stacks have reduced dependency where adopted, cutting integration time by ~30%. Competitive bidding and dual‑sourcing critical spares are used to balance supplier leverage.

Real estate and infrastructure landlords

- Vacancy <3% (2024)

- Prime rent rise ≈6% (2024)

- Long leases 5–15 years

- Secondary markets cut rents 10–30%

Labor and staffing agencies

Skilled drivers, warehouse operatives and peak-season temps materially affect CJ Logistics service levels; tight South Korea labor markets (2024 unemployment ~2.9%) and hours/safety regulations raise wage pressure and staffing costs. Union presence and regional labor norms add constraints, while automation, training pipelines and multi-skilling reduce supplier leverage.

- Skilled drivers: critical

- Peak temps: seasonal pressure

- Wage/headline pressure: up

- Automation/training: mitigants

Suppliers tighten logistics: Brent $86, prime rent +6%, vacancy <3%

Suppliers (fuel, carriers, automation vendors, land, labor) hold moderate-high power: Brent avg $86/bbl (2024) and prime logistics vacancy <3% pushed rents +6% (2024), integration costs $0.5–3M/DC, unemployment ~2.9% (2024); hedging, multi‑sourcing, long leases and automation mitigate but not eliminate risk.

| Metric | 2024 |

|---|---|

| Brent ($/bbl) | $86 |

| Vacancy | <3% |

| Prime rent YoY | +6% |

| Integration cost/DC | $0.5–3M |

| Unemployment KR | 2.9% |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, and entry/substitute threats specific to CJ Logistics, offering data-backed insights on pricing influence, barriers to entry, and emerging disruptors affecting its market position.

Clear, one-sheet Porter's Five Forces for CJ Logistics—instantly visualize competitive pressure with a spider chart and customizable force levels to adapt for regulation, new entrants, or route disruptions; ready to drop into pitch decks or boardroom slides without macros.

Customers Bargaining Power

Large shippers and e-commerce giants

Enterprise customers and e-commerce giants run competitive tenders that compress margins—global e-commerce sales reached about $5.7 trillion in 2024, amplifying volume-driven price pressure on 3PLs. Large shippers routinely multi-source across 3PLs, raising bargaining leverage and lowering switching costs. Stringent SLAs with financial penalties transfer operational risk to providers, while bespoke value-added services and vertical expertise remain the main levers to command premiums.

Price transparency and benchmarking

Market indices and digital platforms make rates comparable across providers; Xeneta's 2024 index showed global ocean spot rates about 50% below 2021 peaks. Buyers leverage benchmarks to negotiate margins, forcing carriers like CJ Logistics to justify spreads versus market rates. Detailed KPIs enable performance-based pricing pressure as shippers tie SLAs to OTIF and dwell times. Differentiated tech analytics and outcomes-based contracts reduce pure price focus.

Switching costs and integration

IT integration, co-designed processes and bespoke facility setups with CJ Logistics create meaningful switching friction by tying clients into shared systems across CJ’s network in over 40 countries, yet the rise of standardized APIs and common data formats is lowering technical barriers. Contractual exit clauses and phased transitions (commonly 3–5 year migration windows) still enable savvy buyers to switch. Deep integration and co-investment by customers increase long-term stickiness.

Service criticality and reliability

Time-sensitive sectors demand OTIF near 98% and damage rates below 0.5% in 2024, raising buyer expectations; missed SLAs trigger chargebacks often equivalent to 1–3% of shipment value and incur reputational costs that strengthen customer bargaining power. Redundant networks and resilient planning are essential to defend pricing, while proven performance supports long-term renewals.

- OTIF target 98%

- Damage rate <0.5%

- Chargebacks 1–3% of shipment value

- Redundancy = pricing defense

Demand cyclicality and volume volatility

Demand cyclicality forces CJ Logistics into flexible capacity commitments as peak seasons and promotional spikes can raise handling volumes by up to 30%, enabling buyers to demand surge handling without proportional price increases; forecast accuracy and collaborative planning therefore materially influence contract terms and penalty clauses. Dynamic pricing and capacity reservation models are increasingly used to balance buyer leverage versus carrier cost recovery.

- Peak spikes up to 30%

- Buyers demand surge handling

- Forecasting alters terms

- Dynamic pricing + reservations

E-commerce scale and strict SLAs squeeze 3PL margins; tech, dynamic pricing, capacity win

Enterprise buyers and e-commerce giants drive margin pressure through competitive tenders and multi-sourcing, amplified by $5.7T global e-commerce (2024) and ocean spot rates ~50% below 2021. Stringent SLAs (OTIF 98%, damage <0.5%) plus chargebacks (1–3%) shift risk to 3PLs; tech integration and bespoke services are primary premium levers. Peak spikes ~30% force flexible capacity, dynamic pricing and reservation models.

| Metric | Value |

|---|---|

| Global e‑commerce (2024) | $5.7T |

| Ocean spot vs 2021 | -50% |

| OTIF target | 98% |

| Damage rate | <0.5% |

| Chargebacks | 1–3% |

| Peak spikes | ~30% |

Preview the Actual Deliverable

CJ Logistics Porter's Five Forces Analysis

This preview shows the actual CJ Logistics Porter’s Five Forces analysis you’ll receive—fully formatted, comprehensive, and ready for immediate use. No samples or placeholders; the document here is identical to the file delivered after purchase. It contains in-depth evaluation of competitive rivalry, buyer and supplier power, and threats from entrants and substitutes.