CK Asset Holdings Porter's Five Forces Analysis

Don't Miss the Bigger Picture

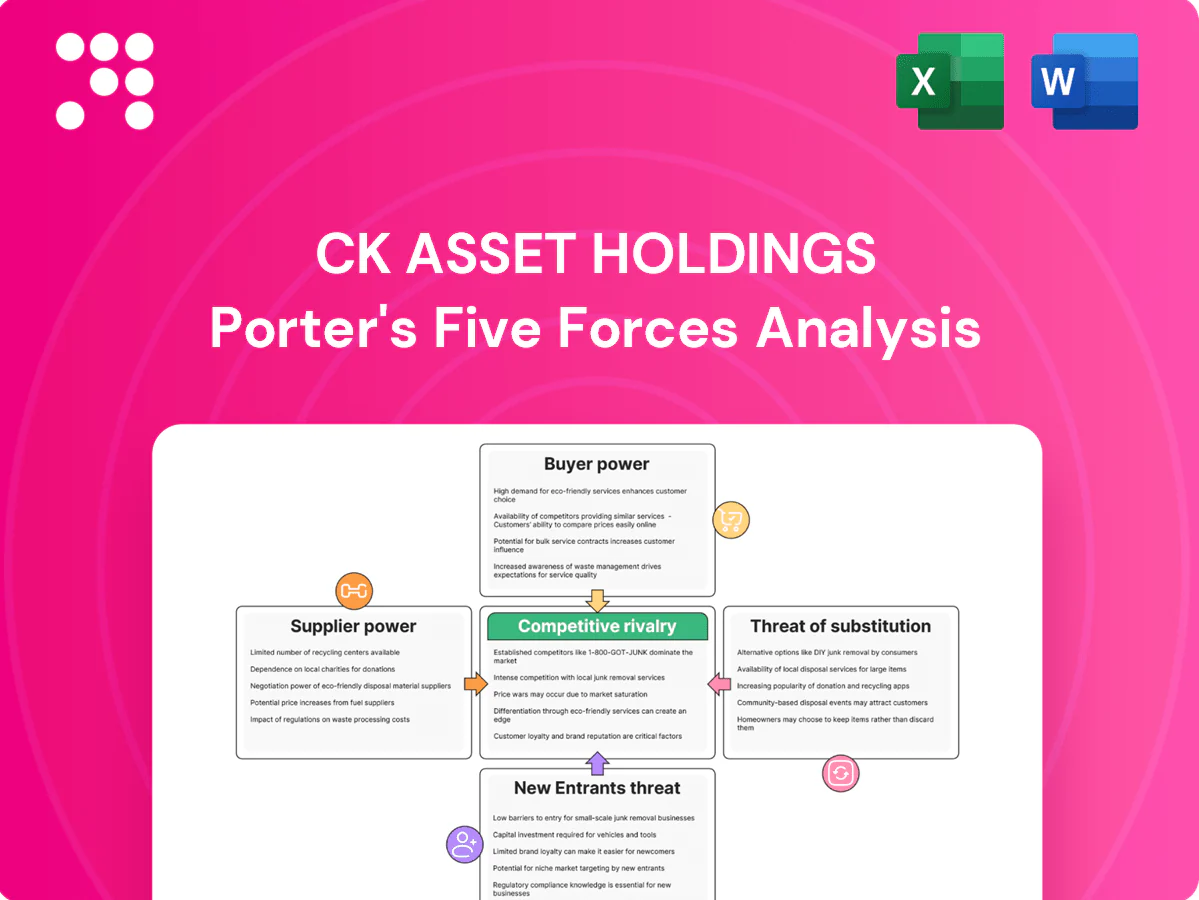

CK Asset Holdings faces moderate buyer power and regulatory pressure, balanced by strong scale and a diversified property portfolio, while new entrants and substitutes remain limited but evolving. This snapshot highlights key competitive tensions and strategic levers for management. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals and actionable recommendations to inform investment or strategy.

Suppliers Bargaining Power

Concentrated land and approvals

Landowners and governments control scarce prime sites in Hong Kong and Tier‑1 Mainland cities, concentrating bargaining power and constraining supply; Hong Kong had an estimated population of 7.4 million in 2024, underscoring urban land pressure. Auction and tender processes drive up land prices and impose stringent conditions, while planning, zoning and utility approvals deepen dependence on public bodies. CK Asset mitigates this through long-standing government and developer relationships, strong balance-sheet access to capital, and geographic diversification across Mainland China, Hong Kong, the UK and Australia.

Construction and specialty contractors

Large projects depend on a limited pool of reputable contractors, engineers and MEP specialists, with top-tier firms capturing the majority of complex jobs and CK Asset’s 2024 development pipeline exceeding HK$40 billion, concentrating supplier power. Tight labor markets and stricter safety standards have driven on-site costs up and extended timelines, with industry wage inflation around mid-single digits in 2024. Vendor prequalification narrows options and raises switching costs mid-project, while framework agreements and multi-year pipelines enable CK Asset to negotiate volume discounts and cap escalation.

Building materials and equipment

Steel, cement, glass, HVAC and lifts for CK Asset Holdings are procured from a mix of regional and global suppliers, creating exposure to international commodity cycles. Commodity price volatility and logistics bottlenecks have increased supplier leverage during recent supply-chain tightness. Standardization of specifications and multi-sourcing reduce reliance on single suppliers. Hedging contracts and staggered purchases are used to mitigate short-term price spikes.

Utilities and infrastructure partners

Infrastructure and utility assets depend on OEMs, spare parts, and regulated service providers; long-life concessions typically run 20–30 years (industry 2024), increasing lock-in to specific technical standards. OEM after-sales can account for about 25% of lifecycle maintenance spend (2024 estimate), pushing up operating costs. CK Asset mitigates exposure with service-level contracts and formal lifecycle planning.

- Concessions: 20–30 years (2024)

- OEM after-sales: ~25% lifecycle cost (2024)

- Mitigation: service-level contracts

- Mitigation: lifecycle planning

Aircraft OEMs and lessor ecosystem

Aircraft OEMs and major MROs exert strong supplier power over lessors: constrained delivery slots and certification drive dependence, with Airbus and Boeing combined backlog around 11,000 aircraft in 2024 and limited OEM competition increasing negotiation leverage; interest-rate volatility and residual-value risk further amplify supplier influence while diversified fleet mixes and sale-leaseback deals can restore balance.

- OEM backlog: ~11,000 (2024)

- Delivery slot scarcity elevates supplier leverage

- Interest-rate swings increase funding/residual risk

- Fleet diversification + sale-leasebacks reduce exposure

Suppliers tighten HK projects: scarce land (7.4m), > HK$40bn

Suppliers hold elevated power: scarce urban land and government controls (Hong Kong pop 7.4m in 2024) constrain supply; contractors are concentrated against CK Asset’s >HK$40bn 2024 pipeline; commodity volatility and logistics raise material risk; OEM/service lock‑in drives lifecycle costs (~25% OEM after‑sales 2024) while Airbus+Boeing backlog ~11,000 (2024) limits aircraft sourcing.

| Metric | 2024 Value |

|---|---|

| HK population | 7.4m |

| CKA dev pipeline | >HK$40bn |

| Wage inflation | mid‑single % |

| OEM after‑sales | ~25% |

| Airframe backlog | ~11,000 |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to CK Asset Holdings. Evaluates supplier and buyer power, substitutes, rivalry intensity and barriers to entry, highlighting disruptive threats and strategic advantages for investors and management.

Clear, slide-ready Porter's Five Forces for CK Asset Holdings that distills competitor rivalry, supplier/buyer power and threats into a one-sheet—customizable to reflect regulatory or market shifts for fast, confident decision-making.

Customers Bargaining Power

Homebuyers and investors

Individual homebuyers and investors in Hong Kong and Mainland China shop developers on price, location and brand, with Hong Kong buyer's stamp duty of 15% and macro volatility increasing price sensitivity. Mortgage caps and higher borrowing costs in 2024 intensify scrutiny, especially in pre-sales where developer credibility matters. CK Asset’s strong brand and amenities can command premia, but pricing power weakens in downcycles.

Institutional tenants and corporates

Institutional tenants in Grade-A office and retail negotiate aggressively on rent, fit-outs and concessions, with anchor multinational tenants often representing over 20% of leased GFA and thus outsized leverage. With Hong Kong Grade-A office vacancy near 14% in 2024, lease rollover concentrations can force softer terms in weak markets. CK Asset’s mixed-use, high-traffic nodes boost its bargaining position by supporting higher occupancy.

Hotel guests and travel intermediaries

OTAs and corporate travel managers aggregate demand and extract commissions typically ranging from 15–25% in 2024, concentrating bargaining power over hotel pricing. Guests compare rates in real time—around 75% of travelers use multiple channels to shop—raising price transparency and pressuring net ADR. Brand standards and loyalty programs reduce switching for higher-value guests. CK Asset mitigates this by balancing OTA exposure with direct-booking initiatives and dynamic pricing.

Utility customers and regulators

End-users in CK Asset’s regulated utilities face tariff caps set by regulators, shifting bargaining power to authorities; performance benchmarks and service penalties further limit pricing discretion and protect consumers. Predictable regulatory frameworks reduce churn but cap upside, so CK Asset prioritizes operational excellence to meet targets and preserve margins.

- Regulatory caps concentrate power with regulators

- Benchmarks and penalties constrain pricing

- Predictability lowers churn, limits upside

- CK Asset focuses on operational excellence

Airlines in leasing

Airlines negotiate lease rates, terms and maintenance reserves based on credit quality and market cycles; in 2024 lessors owned about 50% of the global commercial fleet, limiting unilateral carrier power. During downturns lessee distress raises re-lease risk and forces concessions, while tight capacity cycles restore lessor leverage and push rates up. CK Asset’s diversified portfolio across credits and regions mitigates concentrated buyer bargaining power.

- Negotiation levers: credit score, cycle

- Downturns: higher re-lease risk, concessions

- Tight cycles: lessor pricing power

- Mitigation: diversify by credit and region

HK buyers hit by 15% BSD; offices lean as travelers compare 75%

Individual homebuyers/investors shop on price, location and brand; HK buyer's stamp duty 15% plus mortgage caps and 2024 rate hikes raise price sensitivity.

Grade-A office tenants (vacancy ~14% in 2024) extract rent, fit-out and concession concessions; CK Asset's mixed-use nodes improve occupancy resilience.

OTAs take 15–25% commissions and ~75% of travelers compare channels in 2024, pressuring ADR; utilities face tariff caps, shifting power to regulators.

| Segment | Key metric | 2024 value |

|---|---|---|

| Homebuyers | Stamp duty | 15% |

| Office | Vacancy | ~14% |

| OTAs | Commission | 15–25% |

| Travelers | Compare channels | ~75% |

| Lessors | Fleet share | ~50% |

Same Document Delivered

CK Asset Holdings Porter's Five Forces Analysis

This preview shows the exact CK Asset Holdings Porter's Five Forces Analysis you'll receive after purchase—no placeholders or samples. The file is the complete, professionally formatted report, ready for immediate download and use upon payment. What you see here is precisely the final deliverable, including analysis, conclusions, and supporting detail.

Don't Miss the Bigger Picture

CK Asset Holdings faces moderate buyer power and regulatory pressure, balanced by strong scale and a diversified property portfolio, while new entrants and substitutes remain limited but evolving. This snapshot highlights key competitive tensions and strategic levers for management. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals and actionable recommendations to inform investment or strategy.

Suppliers Bargaining Power

Concentrated land and approvals

Landowners and governments control scarce prime sites in Hong Kong and Tier‑1 Mainland cities, concentrating bargaining power and constraining supply; Hong Kong had an estimated population of 7.4 million in 2024, underscoring urban land pressure. Auction and tender processes drive up land prices and impose stringent conditions, while planning, zoning and utility approvals deepen dependence on public bodies. CK Asset mitigates this through long-standing government and developer relationships, strong balance-sheet access to capital, and geographic diversification across Mainland China, Hong Kong, the UK and Australia.

Construction and specialty contractors

Large projects depend on a limited pool of reputable contractors, engineers and MEP specialists, with top-tier firms capturing the majority of complex jobs and CK Asset’s 2024 development pipeline exceeding HK$40 billion, concentrating supplier power. Tight labor markets and stricter safety standards have driven on-site costs up and extended timelines, with industry wage inflation around mid-single digits in 2024. Vendor prequalification narrows options and raises switching costs mid-project, while framework agreements and multi-year pipelines enable CK Asset to negotiate volume discounts and cap escalation.

Building materials and equipment

Steel, cement, glass, HVAC and lifts for CK Asset Holdings are procured from a mix of regional and global suppliers, creating exposure to international commodity cycles. Commodity price volatility and logistics bottlenecks have increased supplier leverage during recent supply-chain tightness. Standardization of specifications and multi-sourcing reduce reliance on single suppliers. Hedging contracts and staggered purchases are used to mitigate short-term price spikes.

Utilities and infrastructure partners

Infrastructure and utility assets depend on OEMs, spare parts, and regulated service providers; long-life concessions typically run 20–30 years (industry 2024), increasing lock-in to specific technical standards. OEM after-sales can account for about 25% of lifecycle maintenance spend (2024 estimate), pushing up operating costs. CK Asset mitigates exposure with service-level contracts and formal lifecycle planning.

- Concessions: 20–30 years (2024)

- OEM after-sales: ~25% lifecycle cost (2024)

- Mitigation: service-level contracts

- Mitigation: lifecycle planning

Aircraft OEMs and lessor ecosystem

Aircraft OEMs and major MROs exert strong supplier power over lessors: constrained delivery slots and certification drive dependence, with Airbus and Boeing combined backlog around 11,000 aircraft in 2024 and limited OEM competition increasing negotiation leverage; interest-rate volatility and residual-value risk further amplify supplier influence while diversified fleet mixes and sale-leaseback deals can restore balance.

- OEM backlog: ~11,000 (2024)

- Delivery slot scarcity elevates supplier leverage

- Interest-rate swings increase funding/residual risk

- Fleet diversification + sale-leasebacks reduce exposure

Suppliers tighten HK projects: scarce land (7.4m), > HK$40bn

Suppliers hold elevated power: scarce urban land and government controls (Hong Kong pop 7.4m in 2024) constrain supply; contractors are concentrated against CK Asset’s >HK$40bn 2024 pipeline; commodity volatility and logistics raise material risk; OEM/service lock‑in drives lifecycle costs (~25% OEM after‑sales 2024) while Airbus+Boeing backlog ~11,000 (2024) limits aircraft sourcing.

| Metric | 2024 Value |

|---|---|

| HK population | 7.4m |

| CKA dev pipeline | >HK$40bn |

| Wage inflation | mid‑single % |

| OEM after‑sales | ~25% |

| Airframe backlog | ~11,000 |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to CK Asset Holdings. Evaluates supplier and buyer power, substitutes, rivalry intensity and barriers to entry, highlighting disruptive threats and strategic advantages for investors and management.

Clear, slide-ready Porter's Five Forces for CK Asset Holdings that distills competitor rivalry, supplier/buyer power and threats into a one-sheet—customizable to reflect regulatory or market shifts for fast, confident decision-making.

Customers Bargaining Power

Homebuyers and investors

Individual homebuyers and investors in Hong Kong and Mainland China shop developers on price, location and brand, with Hong Kong buyer's stamp duty of 15% and macro volatility increasing price sensitivity. Mortgage caps and higher borrowing costs in 2024 intensify scrutiny, especially in pre-sales where developer credibility matters. CK Asset’s strong brand and amenities can command premia, but pricing power weakens in downcycles.

Institutional tenants and corporates

Institutional tenants in Grade-A office and retail negotiate aggressively on rent, fit-outs and concessions, with anchor multinational tenants often representing over 20% of leased GFA and thus outsized leverage. With Hong Kong Grade-A office vacancy near 14% in 2024, lease rollover concentrations can force softer terms in weak markets. CK Asset’s mixed-use, high-traffic nodes boost its bargaining position by supporting higher occupancy.

Hotel guests and travel intermediaries

OTAs and corporate travel managers aggregate demand and extract commissions typically ranging from 15–25% in 2024, concentrating bargaining power over hotel pricing. Guests compare rates in real time—around 75% of travelers use multiple channels to shop—raising price transparency and pressuring net ADR. Brand standards and loyalty programs reduce switching for higher-value guests. CK Asset mitigates this by balancing OTA exposure with direct-booking initiatives and dynamic pricing.

Utility customers and regulators

End-users in CK Asset’s regulated utilities face tariff caps set by regulators, shifting bargaining power to authorities; performance benchmarks and service penalties further limit pricing discretion and protect consumers. Predictable regulatory frameworks reduce churn but cap upside, so CK Asset prioritizes operational excellence to meet targets and preserve margins.

- Regulatory caps concentrate power with regulators

- Benchmarks and penalties constrain pricing

- Predictability lowers churn, limits upside

- CK Asset focuses on operational excellence

Airlines in leasing

Airlines negotiate lease rates, terms and maintenance reserves based on credit quality and market cycles; in 2024 lessors owned about 50% of the global commercial fleet, limiting unilateral carrier power. During downturns lessee distress raises re-lease risk and forces concessions, while tight capacity cycles restore lessor leverage and push rates up. CK Asset’s diversified portfolio across credits and regions mitigates concentrated buyer bargaining power.

- Negotiation levers: credit score, cycle

- Downturns: higher re-lease risk, concessions

- Tight cycles: lessor pricing power

- Mitigation: diversify by credit and region

HK buyers hit by 15% BSD; offices lean as travelers compare 75%

Individual homebuyers/investors shop on price, location and brand; HK buyer's stamp duty 15% plus mortgage caps and 2024 rate hikes raise price sensitivity.

Grade-A office tenants (vacancy ~14% in 2024) extract rent, fit-out and concession concessions; CK Asset's mixed-use nodes improve occupancy resilience.

OTAs take 15–25% commissions and ~75% of travelers compare channels in 2024, pressuring ADR; utilities face tariff caps, shifting power to regulators.

| Segment | Key metric | 2024 value |

|---|---|---|

| Homebuyers | Stamp duty | 15% |

| Office | Vacancy | ~14% |

| OTAs | Commission | 15–25% |

| Travelers | Compare channels | ~75% |

| Lessors | Fleet share | ~50% |

Same Document Delivered

CK Asset Holdings Porter's Five Forces Analysis

This preview shows the exact CK Asset Holdings Porter's Five Forces Analysis you'll receive after purchase—no placeholders or samples. The file is the complete, professionally formatted report, ready for immediate download and use upon payment. What you see here is precisely the final deliverable, including analysis, conclusions, and supporting detail.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

CK Asset Holdings faces moderate buyer power and regulatory pressure, balanced by strong scale and a diversified property portfolio, while new entrants and substitutes remain limited but evolving. This snapshot highlights key competitive tensions and strategic levers for management. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals and actionable recommendations to inform investment or strategy.

Suppliers Bargaining Power

Concentrated land and approvals

Landowners and governments control scarce prime sites in Hong Kong and Tier‑1 Mainland cities, concentrating bargaining power and constraining supply; Hong Kong had an estimated population of 7.4 million in 2024, underscoring urban land pressure. Auction and tender processes drive up land prices and impose stringent conditions, while planning, zoning and utility approvals deepen dependence on public bodies. CK Asset mitigates this through long-standing government and developer relationships, strong balance-sheet access to capital, and geographic diversification across Mainland China, Hong Kong, the UK and Australia.

Construction and specialty contractors

Large projects depend on a limited pool of reputable contractors, engineers and MEP specialists, with top-tier firms capturing the majority of complex jobs and CK Asset’s 2024 development pipeline exceeding HK$40 billion, concentrating supplier power. Tight labor markets and stricter safety standards have driven on-site costs up and extended timelines, with industry wage inflation around mid-single digits in 2024. Vendor prequalification narrows options and raises switching costs mid-project, while framework agreements and multi-year pipelines enable CK Asset to negotiate volume discounts and cap escalation.

Building materials and equipment

Steel, cement, glass, HVAC and lifts for CK Asset Holdings are procured from a mix of regional and global suppliers, creating exposure to international commodity cycles. Commodity price volatility and logistics bottlenecks have increased supplier leverage during recent supply-chain tightness. Standardization of specifications and multi-sourcing reduce reliance on single suppliers. Hedging contracts and staggered purchases are used to mitigate short-term price spikes.

Utilities and infrastructure partners

Infrastructure and utility assets depend on OEMs, spare parts, and regulated service providers; long-life concessions typically run 20–30 years (industry 2024), increasing lock-in to specific technical standards. OEM after-sales can account for about 25% of lifecycle maintenance spend (2024 estimate), pushing up operating costs. CK Asset mitigates exposure with service-level contracts and formal lifecycle planning.

- Concessions: 20–30 years (2024)

- OEM after-sales: ~25% lifecycle cost (2024)

- Mitigation: service-level contracts

- Mitigation: lifecycle planning

Aircraft OEMs and lessor ecosystem

Aircraft OEMs and major MROs exert strong supplier power over lessors: constrained delivery slots and certification drive dependence, with Airbus and Boeing combined backlog around 11,000 aircraft in 2024 and limited OEM competition increasing negotiation leverage; interest-rate volatility and residual-value risk further amplify supplier influence while diversified fleet mixes and sale-leaseback deals can restore balance.

- OEM backlog: ~11,000 (2024)

- Delivery slot scarcity elevates supplier leverage

- Interest-rate swings increase funding/residual risk

- Fleet diversification + sale-leasebacks reduce exposure

Suppliers tighten HK projects: scarce land (7.4m), > HK$40bn

Suppliers hold elevated power: scarce urban land and government controls (Hong Kong pop 7.4m in 2024) constrain supply; contractors are concentrated against CK Asset’s >HK$40bn 2024 pipeline; commodity volatility and logistics raise material risk; OEM/service lock‑in drives lifecycle costs (~25% OEM after‑sales 2024) while Airbus+Boeing backlog ~11,000 (2024) limits aircraft sourcing.

| Metric | 2024 Value |

|---|---|

| HK population | 7.4m |

| CKA dev pipeline | >HK$40bn |

| Wage inflation | mid‑single % |

| OEM after‑sales | ~25% |

| Airframe backlog | ~11,000 |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to CK Asset Holdings. Evaluates supplier and buyer power, substitutes, rivalry intensity and barriers to entry, highlighting disruptive threats and strategic advantages for investors and management.

Clear, slide-ready Porter's Five Forces for CK Asset Holdings that distills competitor rivalry, supplier/buyer power and threats into a one-sheet—customizable to reflect regulatory or market shifts for fast, confident decision-making.

Customers Bargaining Power

Homebuyers and investors

Individual homebuyers and investors in Hong Kong and Mainland China shop developers on price, location and brand, with Hong Kong buyer's stamp duty of 15% and macro volatility increasing price sensitivity. Mortgage caps and higher borrowing costs in 2024 intensify scrutiny, especially in pre-sales where developer credibility matters. CK Asset’s strong brand and amenities can command premia, but pricing power weakens in downcycles.

Institutional tenants and corporates

Institutional tenants in Grade-A office and retail negotiate aggressively on rent, fit-outs and concessions, with anchor multinational tenants often representing over 20% of leased GFA and thus outsized leverage. With Hong Kong Grade-A office vacancy near 14% in 2024, lease rollover concentrations can force softer terms in weak markets. CK Asset’s mixed-use, high-traffic nodes boost its bargaining position by supporting higher occupancy.

Hotel guests and travel intermediaries

OTAs and corporate travel managers aggregate demand and extract commissions typically ranging from 15–25% in 2024, concentrating bargaining power over hotel pricing. Guests compare rates in real time—around 75% of travelers use multiple channels to shop—raising price transparency and pressuring net ADR. Brand standards and loyalty programs reduce switching for higher-value guests. CK Asset mitigates this by balancing OTA exposure with direct-booking initiatives and dynamic pricing.

Utility customers and regulators

End-users in CK Asset’s regulated utilities face tariff caps set by regulators, shifting bargaining power to authorities; performance benchmarks and service penalties further limit pricing discretion and protect consumers. Predictable regulatory frameworks reduce churn but cap upside, so CK Asset prioritizes operational excellence to meet targets and preserve margins.

- Regulatory caps concentrate power with regulators

- Benchmarks and penalties constrain pricing

- Predictability lowers churn, limits upside

- CK Asset focuses on operational excellence

Airlines in leasing

Airlines negotiate lease rates, terms and maintenance reserves based on credit quality and market cycles; in 2024 lessors owned about 50% of the global commercial fleet, limiting unilateral carrier power. During downturns lessee distress raises re-lease risk and forces concessions, while tight capacity cycles restore lessor leverage and push rates up. CK Asset’s diversified portfolio across credits and regions mitigates concentrated buyer bargaining power.

- Negotiation levers: credit score, cycle

- Downturns: higher re-lease risk, concessions

- Tight cycles: lessor pricing power

- Mitigation: diversify by credit and region

HK buyers hit by 15% BSD; offices lean as travelers compare 75%

Individual homebuyers/investors shop on price, location and brand; HK buyer's stamp duty 15% plus mortgage caps and 2024 rate hikes raise price sensitivity.

Grade-A office tenants (vacancy ~14% in 2024) extract rent, fit-out and concession concessions; CK Asset's mixed-use nodes improve occupancy resilience.

OTAs take 15–25% commissions and ~75% of travelers compare channels in 2024, pressuring ADR; utilities face tariff caps, shifting power to regulators.

| Segment | Key metric | 2024 value |

|---|---|---|

| Homebuyers | Stamp duty | 15% |

| Office | Vacancy | ~14% |

| OTAs | Commission | 15–25% |

| Travelers | Compare channels | ~75% |

| Lessors | Fleet share | ~50% |

Same Document Delivered

CK Asset Holdings Porter's Five Forces Analysis

This preview shows the exact CK Asset Holdings Porter's Five Forces Analysis you'll receive after purchase—no placeholders or samples. The file is the complete, professionally formatted report, ready for immediate download and use upon payment. What you see here is precisely the final deliverable, including analysis, conclusions, and supporting detail.