Claranova SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

Claranova's SWOT highlights diversified digital product strengths, recurring-revenue assets, and exposure to competitive platform risks and integration challenges. Our full SWOT unpacks financial context, strategic options, and execution risks with evidence-backed recommendations. Purchase the complete, editable report to plan, pitch, or invest with confidence.

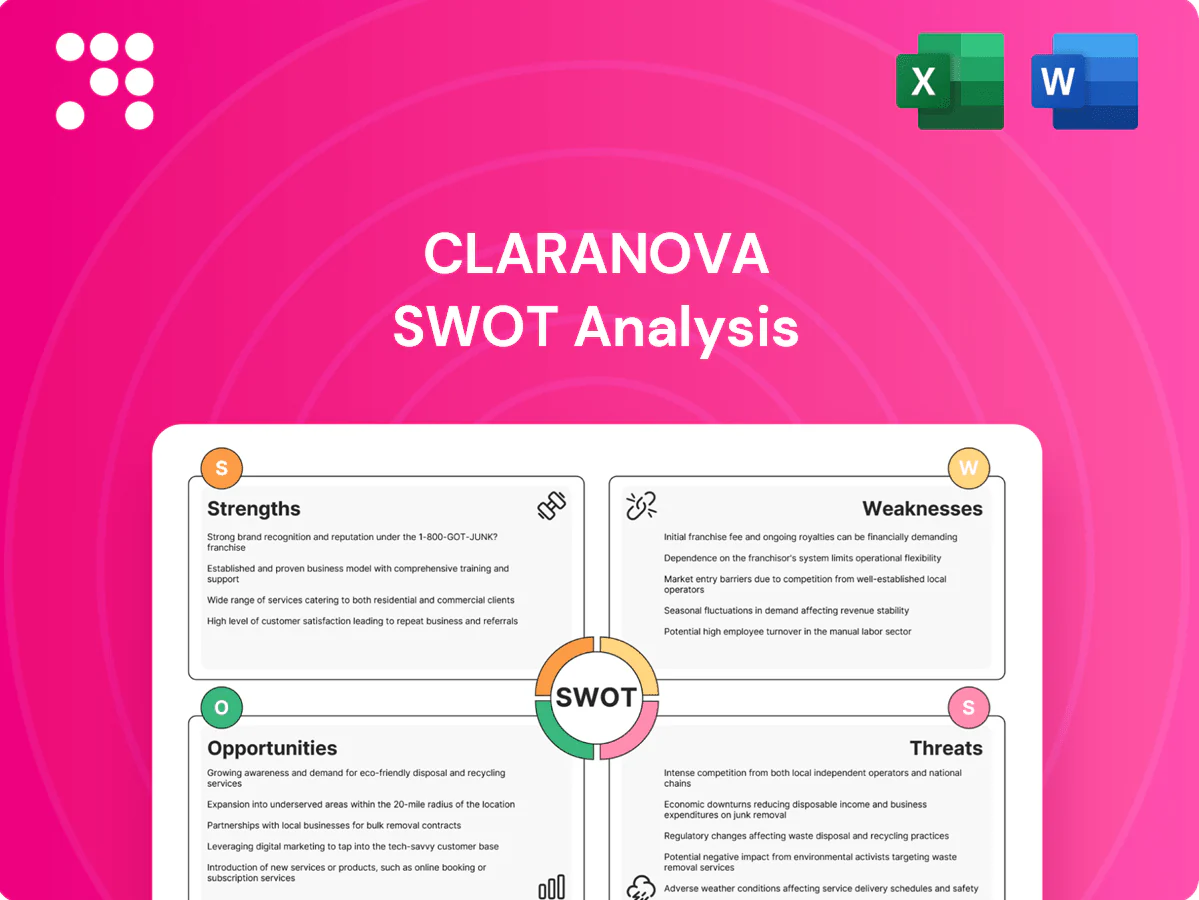

Strengths

Diversified digital portfolio

Claranova, listed on Euronext Paris, runs a diversified digital portfolio across three pillars—personalized e-commerce, software publishing and IoT—spreading revenue risk and enabling cross-selling synergies.

Brands PlanetArt, Avanquest and myDevices serve both consumer and B2B segments, balancing demand cycles and broadening addressable markets.

This multi-pillar model delivers resilience and optionality for capital allocation across the group.

Strong PlanetArt brand reach

PlanetArt leverages broad consumer awareness in photo printing and personalized gifts through scalable, mobile-first funnels that drive high repeat purchase behavior and seasonal peak volumes, boosting customer lifetime value. Variable-cost manufacturing networks enable agile fulfillment and margin management across peaks. This brand reach underpins Claranova’s direct-to-consumer growth strategy.

Avanquest recurring software revenues

Avanquest’s subscription-based utilities, PDF, security and productivity tools deliver predictable recurring cash flows through multi-month and annual plans. Direct-to-consumer distribution via owned channels and app stores reduces reliance on third-party partners and preserves margins. Data-driven marketing and CRM optimize conversion, upsell and retention economics, improving customer lifetime value and payback periods.

IoT platform capabilities

myDevices provides device management, data visualization and rapid deployment for SMB and enterprise use cases, accelerating time-to-value for vertical solutions; the global installed base of IoT endpoints is expected to reach about 29.4 billion devices by 2025, enlarging platform demand. Partnerships with hardware and connectivity providers broaden Claranova’s addressable markets and speed go-to-market for bundled offers.

- Device mgmt, visualization, rapid deployment

- Speeds vertical time-to-value

- Addresses ~29.4B IoT endpoints (2025)

- Hardware/connectivity partnerships expand market

Global footprint and scalability

Claranova leverages digital delivery and a distributed logistics network to serve customers globally, enabling rapid market access while maintaining localized fulfillment. Its modular platforms allow fast rollout of new SKUs and geographies with limited incremental overhead. Centralized technology and marketing stacks concentrate fixed costs, improving unit economics as volume scales; Claranova is publicly listed on Euronext Paris.

- Global digital delivery + distributed logistics

- Modular platforms for rapid SKU/geography launches

- Centralized tech & marketing — better unit economics at scale

- Publicly listed on Euronext Paris

Three digital pillars diversify revenue, enable cross-selling and target 29.4 billion IoT endpoints

Claranova operates three complementary digital pillars—PlanetArt, Avanquest and myDevices—diversifying revenue and enabling cross-selling while listed on Euronext Paris.

PlanetArt’s mobile-first, variable-cost fulfillment model drives high repeat purchases and seasonal scale; Avanquest delivers recurring subscription cash flows via owned channels.

myDevices’ IoT platform and hardware partnerships accelerate SMB/enterprise deployments, tapping a projected 29.4 billion global IoT endpoints by 2025.

| Metric | Fact |

|---|---|

| Global IoT endpoints (2025) | 29.4 billion |

What is included in the product

Provides a concise SWOT analysis of Claranova, outlining its internal strengths and weaknesses and external opportunities and threats to assess strategic positioning, growth drivers, and key risks.

Provides a concise SWOT matrix for Claranova to quickly identify strategic strengths, weaknesses, opportunities and threats, easing prioritization of product and market pain points. Ideal for executives needing a clear snapshot to align fast, actionable responses.

Weaknesses

Exposure to seasonality

PlanetArt demand concentrates around holidays, creating revenue volatility and operational strain as order volume can spike sharply in Nov–Dec; Adobe’s Digital Economy Index shows the US holiday period can drive roughly 30% of annual online sales. Inventory and fulfillment capacity must ramp, pressuring costs and reducing margin during peaks. Cash flow timing from concentrated seasonal sales complicates working capital and liquidity planning.

Competitive intensity

Photo-gifts, consumer software and IoT all sit in crowded markets with heavy price-based competition that pressures margins. Customer acquisition costs have risen as ad platforms compress ROI, increasing payback periods and churn risk for subscription products. The global IoT market exceeded $1.1 trillion in 2023, underscoring intense entrant activity and the need to continually reinforce differentiation to defend share.

Brand fragmentation

Multiple divisions and product lines dilute Claranova’s corporate brand coherence, making it harder to present a unified value proposition to customers. Cross-selling across business pillars often underperforms without a consistent identity and integrated go-to-market strategy. Resource prioritization can leave some niches underscaled, reducing margins and limiting economies of scale.

Dependence on digital ads

Dependence on digital ads makes Claranova's DTC growth highly sensitive to platform algorithm shifts and auction dynamics; performance marketing drives user acquisition but can swing results quickly. Privacy changes like Apple ATT and evolving consent regimes have reduced targeting precision and muddied attribution, complicating ROI measurement. If ad spend rises without strict LTV/CAC discipline, margin erosion is likely, increasing cash-flow volatility.

- Platform sensitivity

- Privacy/attribution risk

- Margin pressure from rising ad spend

IoT monetization still maturing

myDevices faces longer enterprise sales cycles and proof-of-value hurdles, with typical IoT pilot-to-deployment timelines often stretching 9–15 months, slowing revenue recognition. Standardization gaps and integration complexity—multiple protocols, legacy IT—can delay rollouts and raise implementation costs. As a result, near-term revenue contribution may remain modest versus investor expectations.

- Longer sales cycles: 9–15 months

- Integration complexity: multi-protocol, legacy systems

- Near-term revenue: likely modest vs expectations

Nov–Dec sales spike creates cash strain; crowded IoT/photo-gift market squeezes margins

Seasonal PlanetArt demand concentrates in Nov–Dec (Adobe: ~30% of US online holiday sales), creating revenue volatility and working-capital strain. Crowded photo-gift, software and IoT markets (global IoT >$1.1T in 2023) pressure margins and raise CAC. Fragmented portfolio dilutes brand and hampers cross-sell; myDevices faces 9–15 month pilot-to-deployment cycles.

| Weakness | Impact | Data |

|---|---|---|

| Seasonality | Revenue volatility, cash strain | ~30% holiday share |

| Market crowding | Margin/CAC pressure | IoT >$1.1T (2023) |

| Sales cycle | Slow revenue ramp | 9–15 months |

What You See Is What You Get

Claranova SWOT Analysis

This preview is a real excerpt from the Claranova SWOT Analysis document you’ll receive after purchase—no placeholders or samples. The file shown is the actual, professional-quality report and becomes fully available and editable immediately upon checkout. Buy now to access the complete, detailed analysis.

Dive Deeper Into the Company’s Strategic Blueprint

Claranova's SWOT highlights diversified digital product strengths, recurring-revenue assets, and exposure to competitive platform risks and integration challenges. Our full SWOT unpacks financial context, strategic options, and execution risks with evidence-backed recommendations. Purchase the complete, editable report to plan, pitch, or invest with confidence.

Strengths

Diversified digital portfolio

Claranova, listed on Euronext Paris, runs a diversified digital portfolio across three pillars—personalized e-commerce, software publishing and IoT—spreading revenue risk and enabling cross-selling synergies.

Brands PlanetArt, Avanquest and myDevices serve both consumer and B2B segments, balancing demand cycles and broadening addressable markets.

This multi-pillar model delivers resilience and optionality for capital allocation across the group.

Strong PlanetArt brand reach

PlanetArt leverages broad consumer awareness in photo printing and personalized gifts through scalable, mobile-first funnels that drive high repeat purchase behavior and seasonal peak volumes, boosting customer lifetime value. Variable-cost manufacturing networks enable agile fulfillment and margin management across peaks. This brand reach underpins Claranova’s direct-to-consumer growth strategy.

Avanquest recurring software revenues

Avanquest’s subscription-based utilities, PDF, security and productivity tools deliver predictable recurring cash flows through multi-month and annual plans. Direct-to-consumer distribution via owned channels and app stores reduces reliance on third-party partners and preserves margins. Data-driven marketing and CRM optimize conversion, upsell and retention economics, improving customer lifetime value and payback periods.

IoT platform capabilities

myDevices provides device management, data visualization and rapid deployment for SMB and enterprise use cases, accelerating time-to-value for vertical solutions; the global installed base of IoT endpoints is expected to reach about 29.4 billion devices by 2025, enlarging platform demand. Partnerships with hardware and connectivity providers broaden Claranova’s addressable markets and speed go-to-market for bundled offers.

- Device mgmt, visualization, rapid deployment

- Speeds vertical time-to-value

- Addresses ~29.4B IoT endpoints (2025)

- Hardware/connectivity partnerships expand market

Global footprint and scalability

Claranova leverages digital delivery and a distributed logistics network to serve customers globally, enabling rapid market access while maintaining localized fulfillment. Its modular platforms allow fast rollout of new SKUs and geographies with limited incremental overhead. Centralized technology and marketing stacks concentrate fixed costs, improving unit economics as volume scales; Claranova is publicly listed on Euronext Paris.

- Global digital delivery + distributed logistics

- Modular platforms for rapid SKU/geography launches

- Centralized tech & marketing — better unit economics at scale

- Publicly listed on Euronext Paris

Three digital pillars diversify revenue, enable cross-selling and target 29.4 billion IoT endpoints

Claranova operates three complementary digital pillars—PlanetArt, Avanquest and myDevices—diversifying revenue and enabling cross-selling while listed on Euronext Paris.

PlanetArt’s mobile-first, variable-cost fulfillment model drives high repeat purchases and seasonal scale; Avanquest delivers recurring subscription cash flows via owned channels.

myDevices’ IoT platform and hardware partnerships accelerate SMB/enterprise deployments, tapping a projected 29.4 billion global IoT endpoints by 2025.

| Metric | Fact |

|---|---|

| Global IoT endpoints (2025) | 29.4 billion |

What is included in the product

Provides a concise SWOT analysis of Claranova, outlining its internal strengths and weaknesses and external opportunities and threats to assess strategic positioning, growth drivers, and key risks.

Provides a concise SWOT matrix for Claranova to quickly identify strategic strengths, weaknesses, opportunities and threats, easing prioritization of product and market pain points. Ideal for executives needing a clear snapshot to align fast, actionable responses.

Weaknesses

Exposure to seasonality

PlanetArt demand concentrates around holidays, creating revenue volatility and operational strain as order volume can spike sharply in Nov–Dec; Adobe’s Digital Economy Index shows the US holiday period can drive roughly 30% of annual online sales. Inventory and fulfillment capacity must ramp, pressuring costs and reducing margin during peaks. Cash flow timing from concentrated seasonal sales complicates working capital and liquidity planning.

Competitive intensity

Photo-gifts, consumer software and IoT all sit in crowded markets with heavy price-based competition that pressures margins. Customer acquisition costs have risen as ad platforms compress ROI, increasing payback periods and churn risk for subscription products. The global IoT market exceeded $1.1 trillion in 2023, underscoring intense entrant activity and the need to continually reinforce differentiation to defend share.

Brand fragmentation

Multiple divisions and product lines dilute Claranova’s corporate brand coherence, making it harder to present a unified value proposition to customers. Cross-selling across business pillars often underperforms without a consistent identity and integrated go-to-market strategy. Resource prioritization can leave some niches underscaled, reducing margins and limiting economies of scale.

Dependence on digital ads

Dependence on digital ads makes Claranova's DTC growth highly sensitive to platform algorithm shifts and auction dynamics; performance marketing drives user acquisition but can swing results quickly. Privacy changes like Apple ATT and evolving consent regimes have reduced targeting precision and muddied attribution, complicating ROI measurement. If ad spend rises without strict LTV/CAC discipline, margin erosion is likely, increasing cash-flow volatility.

- Platform sensitivity

- Privacy/attribution risk

- Margin pressure from rising ad spend

IoT monetization still maturing

myDevices faces longer enterprise sales cycles and proof-of-value hurdles, with typical IoT pilot-to-deployment timelines often stretching 9–15 months, slowing revenue recognition. Standardization gaps and integration complexity—multiple protocols, legacy IT—can delay rollouts and raise implementation costs. As a result, near-term revenue contribution may remain modest versus investor expectations.

- Longer sales cycles: 9–15 months

- Integration complexity: multi-protocol, legacy systems

- Near-term revenue: likely modest vs expectations

Nov–Dec sales spike creates cash strain; crowded IoT/photo-gift market squeezes margins

Seasonal PlanetArt demand concentrates in Nov–Dec (Adobe: ~30% of US online holiday sales), creating revenue volatility and working-capital strain. Crowded photo-gift, software and IoT markets (global IoT >$1.1T in 2023) pressure margins and raise CAC. Fragmented portfolio dilutes brand and hampers cross-sell; myDevices faces 9–15 month pilot-to-deployment cycles.

| Weakness | Impact | Data |

|---|---|---|

| Seasonality | Revenue volatility, cash strain | ~30% holiday share |

| Market crowding | Margin/CAC pressure | IoT >$1.1T (2023) |

| Sales cycle | Slow revenue ramp | 9–15 months |

What You See Is What You Get

Claranova SWOT Analysis

This preview is a real excerpt from the Claranova SWOT Analysis document you’ll receive after purchase—no placeholders or samples. The file shown is the actual, professional-quality report and becomes fully available and editable immediately upon checkout. Buy now to access the complete, detailed analysis.

Original: $10.00

-65%$10.00

$3.50Description

Dive Deeper Into the Company’s Strategic Blueprint

Claranova's SWOT highlights diversified digital product strengths, recurring-revenue assets, and exposure to competitive platform risks and integration challenges. Our full SWOT unpacks financial context, strategic options, and execution risks with evidence-backed recommendations. Purchase the complete, editable report to plan, pitch, or invest with confidence.

Strengths

Diversified digital portfolio

Claranova, listed on Euronext Paris, runs a diversified digital portfolio across three pillars—personalized e-commerce, software publishing and IoT—spreading revenue risk and enabling cross-selling synergies.

Brands PlanetArt, Avanquest and myDevices serve both consumer and B2B segments, balancing demand cycles and broadening addressable markets.

This multi-pillar model delivers resilience and optionality for capital allocation across the group.

Strong PlanetArt brand reach

PlanetArt leverages broad consumer awareness in photo printing and personalized gifts through scalable, mobile-first funnels that drive high repeat purchase behavior and seasonal peak volumes, boosting customer lifetime value. Variable-cost manufacturing networks enable agile fulfillment and margin management across peaks. This brand reach underpins Claranova’s direct-to-consumer growth strategy.

Avanquest recurring software revenues

Avanquest’s subscription-based utilities, PDF, security and productivity tools deliver predictable recurring cash flows through multi-month and annual plans. Direct-to-consumer distribution via owned channels and app stores reduces reliance on third-party partners and preserves margins. Data-driven marketing and CRM optimize conversion, upsell and retention economics, improving customer lifetime value and payback periods.

IoT platform capabilities

myDevices provides device management, data visualization and rapid deployment for SMB and enterprise use cases, accelerating time-to-value for vertical solutions; the global installed base of IoT endpoints is expected to reach about 29.4 billion devices by 2025, enlarging platform demand. Partnerships with hardware and connectivity providers broaden Claranova’s addressable markets and speed go-to-market for bundled offers.

- Device mgmt, visualization, rapid deployment

- Speeds vertical time-to-value

- Addresses ~29.4B IoT endpoints (2025)

- Hardware/connectivity partnerships expand market

Global footprint and scalability

Claranova leverages digital delivery and a distributed logistics network to serve customers globally, enabling rapid market access while maintaining localized fulfillment. Its modular platforms allow fast rollout of new SKUs and geographies with limited incremental overhead. Centralized technology and marketing stacks concentrate fixed costs, improving unit economics as volume scales; Claranova is publicly listed on Euronext Paris.

- Global digital delivery + distributed logistics

- Modular platforms for rapid SKU/geography launches

- Centralized tech & marketing — better unit economics at scale

- Publicly listed on Euronext Paris

Three digital pillars diversify revenue, enable cross-selling and target 29.4 billion IoT endpoints

Claranova operates three complementary digital pillars—PlanetArt, Avanquest and myDevices—diversifying revenue and enabling cross-selling while listed on Euronext Paris.

PlanetArt’s mobile-first, variable-cost fulfillment model drives high repeat purchases and seasonal scale; Avanquest delivers recurring subscription cash flows via owned channels.

myDevices’ IoT platform and hardware partnerships accelerate SMB/enterprise deployments, tapping a projected 29.4 billion global IoT endpoints by 2025.

| Metric | Fact |

|---|---|

| Global IoT endpoints (2025) | 29.4 billion |

What is included in the product

Provides a concise SWOT analysis of Claranova, outlining its internal strengths and weaknesses and external opportunities and threats to assess strategic positioning, growth drivers, and key risks.

Provides a concise SWOT matrix for Claranova to quickly identify strategic strengths, weaknesses, opportunities and threats, easing prioritization of product and market pain points. Ideal for executives needing a clear snapshot to align fast, actionable responses.

Weaknesses

Exposure to seasonality

PlanetArt demand concentrates around holidays, creating revenue volatility and operational strain as order volume can spike sharply in Nov–Dec; Adobe’s Digital Economy Index shows the US holiday period can drive roughly 30% of annual online sales. Inventory and fulfillment capacity must ramp, pressuring costs and reducing margin during peaks. Cash flow timing from concentrated seasonal sales complicates working capital and liquidity planning.

Competitive intensity

Photo-gifts, consumer software and IoT all sit in crowded markets with heavy price-based competition that pressures margins. Customer acquisition costs have risen as ad platforms compress ROI, increasing payback periods and churn risk for subscription products. The global IoT market exceeded $1.1 trillion in 2023, underscoring intense entrant activity and the need to continually reinforce differentiation to defend share.

Brand fragmentation

Multiple divisions and product lines dilute Claranova’s corporate brand coherence, making it harder to present a unified value proposition to customers. Cross-selling across business pillars often underperforms without a consistent identity and integrated go-to-market strategy. Resource prioritization can leave some niches underscaled, reducing margins and limiting economies of scale.

Dependence on digital ads

Dependence on digital ads makes Claranova's DTC growth highly sensitive to platform algorithm shifts and auction dynamics; performance marketing drives user acquisition but can swing results quickly. Privacy changes like Apple ATT and evolving consent regimes have reduced targeting precision and muddied attribution, complicating ROI measurement. If ad spend rises without strict LTV/CAC discipline, margin erosion is likely, increasing cash-flow volatility.

- Platform sensitivity

- Privacy/attribution risk

- Margin pressure from rising ad spend

IoT monetization still maturing

myDevices faces longer enterprise sales cycles and proof-of-value hurdles, with typical IoT pilot-to-deployment timelines often stretching 9–15 months, slowing revenue recognition. Standardization gaps and integration complexity—multiple protocols, legacy IT—can delay rollouts and raise implementation costs. As a result, near-term revenue contribution may remain modest versus investor expectations.

- Longer sales cycles: 9–15 months

- Integration complexity: multi-protocol, legacy systems

- Near-term revenue: likely modest vs expectations

Nov–Dec sales spike creates cash strain; crowded IoT/photo-gift market squeezes margins

Seasonal PlanetArt demand concentrates in Nov–Dec (Adobe: ~30% of US online holiday sales), creating revenue volatility and working-capital strain. Crowded photo-gift, software and IoT markets (global IoT >$1.1T in 2023) pressure margins and raise CAC. Fragmented portfolio dilutes brand and hampers cross-sell; myDevices faces 9–15 month pilot-to-deployment cycles.

| Weakness | Impact | Data |

|---|---|---|

| Seasonality | Revenue volatility, cash strain | ~30% holiday share |

| Market crowding | Margin/CAC pressure | IoT >$1.1T (2023) |

| Sales cycle | Slow revenue ramp | 9–15 months |

What You See Is What You Get

Claranova SWOT Analysis

This preview is a real excerpt from the Claranova SWOT Analysis document you’ll receive after purchase—no placeholders or samples. The file shown is the actual, professional-quality report and becomes fully available and editable immediately upon checkout. Buy now to access the complete, detailed analysis.