Clariane Porter's Five Forces Analysis

Don't Miss the Bigger Picture

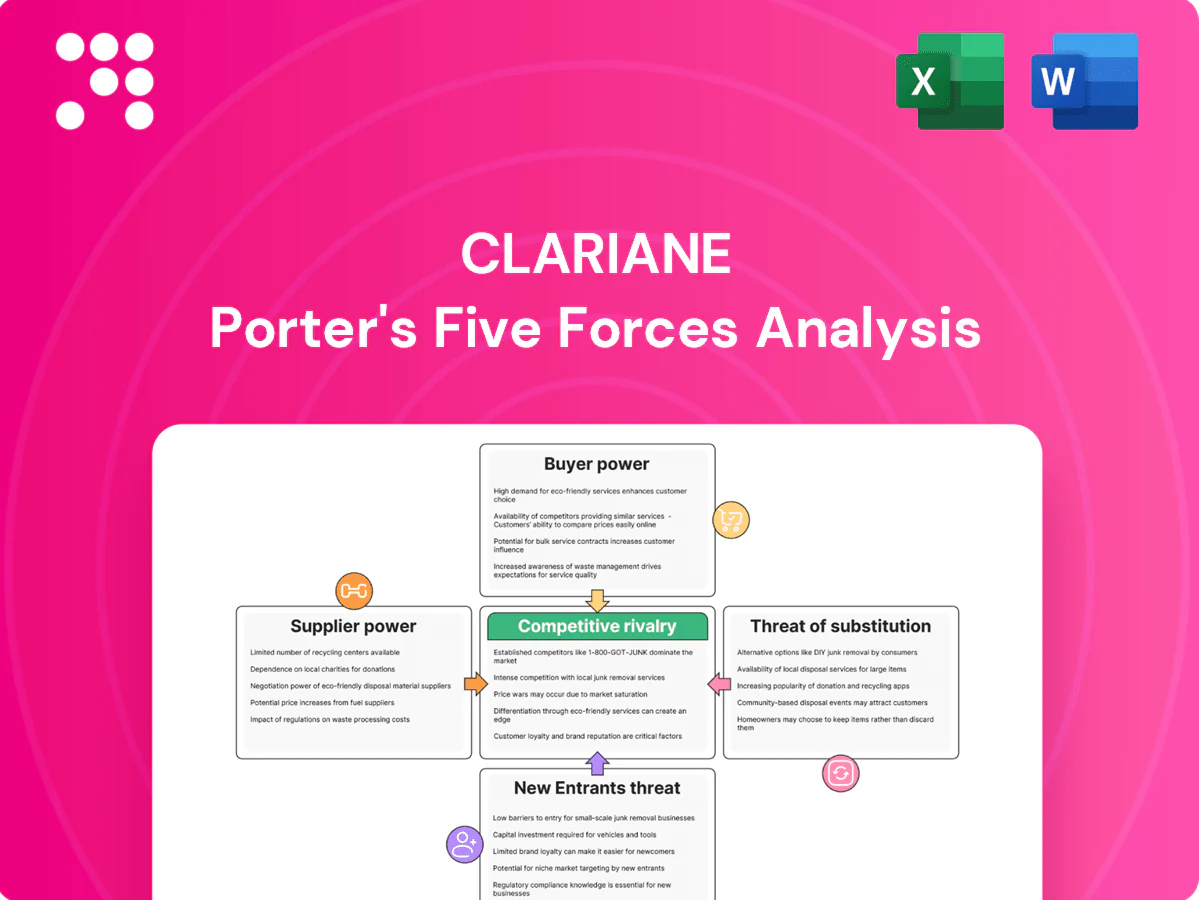

Clariane's Porter’s Five Forces analysis distills competitive pressures—buyer and supplier power, rivalry, substitutes, and entry threats—into clear strategic implications. It highlights where Clariane holds leverage and where external risks could erode margins. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Clariane’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarce skilled caregivers

Registered nurses, aides and therapists face chronic shortages across Europe, with 2024 vacancy rates averaging about 9% and turnover often 15–20%, giving labor suppliers strong leverage over wages and conditions. Clariane must meet statutory staffing ratios (often 1:4–1:8 in acute and elderly care), constraining flexibility in wage negotiations. High unionization and regulatory mandates further amplify supplier power, while turnover drives recruitment and training costs that can add up to roughly 10–15% of annual labor spend.

Pharma, medical devices, and consumables

Clinical supplies are highly regulated and quality-critical, giving approved vendors moderate bargaining power; market concentration (top 10 device firms account for roughly 40% of global revenues) limits substitutability. Bulk purchasing and frame agreements can temper prices, but 2021–23 supply shocks and intermittent shortages disrupted operations. Compliance and traceability rules (UDI, serialization) restrict alternative sourcing, while medical input inflation (about 5–7% in 2023–24) pressures margins.

Real estate, utilities, and maintenance

Clariane faces high supplier power in real estate, utilities and maintenance: nursing homes need specialized, code-compliant facilities that tie operators to landlords with long leases (commonly 5–20 years) and retrofits that often exceed $5,000 per bed, limiting relocation flexibility; nationwide occupancy near 78% in 2024 keeps demand for such sites tight. Energy price volatility and spikes in wholesale natural gas/electricity materially raise operating cost exposure, while certified preventive-maintenance vendors command scheduling leverage due to licensing and certification requirements.

IT/EHR and interoperability vendors

Clinical software, EHRs and telecare platforms create high switching costs—integration, training and data migration can run into millions—while the global EHR market was valued at about $35 billion in 2024, reinforcing vendor leverage. Cybersecurity and HIPAA/privacy compliance narrow viable vendors, and mandatory upgrade clauses let vendors push recurring price escalators. Service outages directly harm care quality metrics tied to CMS audits and reimbursements, increasing supplier power.

- Market: ~35B 2024

- Switching cost: often millions

- Compliance: HIPAA narrows vendors

- Upgrades: recurring escalators

- Outages: affect CMS quality/audits

Staffing agencies and temp pools

Agency labor fills clinical gaps but carries a 20–40% premium versus payroll, giving agencies strong spot-market power; US staffing revenue reached about 180 billion in 2024, underscoring scale. Absentee peaks or outbreaks can raise temp demand by 30–50%, pressuring margins if internal hiring pipelines are weak, while tight SLAs limit renegotiation during crises.

- Premiums: 20–40% above payroll

- Market size: ~180 billion (US, 2024)

- Demand spikes: +30–50% in outbreaks

- Risk: margin erosion if internal pipeline weak

- SLA constraint: limited renegotiation in crises

Clinical supplier squeeze: RN vacancy ~9%, agency premiums 20–40%

Supplier power is high: RN vacancies ~9% and turnover 15–20% (2024) push wages and agency premiums 20–40%, eroding margins. Clinical supply concentration (top10 ≈40% revenues) and medical inflation 5–7% (2023–24) limit sourcing flexibility. EHR market ~$35B (2024) and US staffing ~$180B (2024) raise switching and vendor leverage.

| Metric | 2024 |

|---|---|

| RN vacancy | ~9% |

| Turnover | 15–20% |

| Agency premium | 20–40% |

| EHR market | $35B |

| US staffing | $180B |

What is included in the product

Tailored Porter's Five Forces for Clariane that uncovers key drivers of competition, evaluates supplier and buyer power, identifies disruptive substitutes and emerging threats, and assesses entry barriers to clarify pricing influence and profitability.

Clear one-sheet Porter's Five Forces for Clariane—customize pressure levels, swap in your data, and instantly visualize strategic pressure with a spider chart for quick decision-making.

Customers Bargaining Power

Public payers and municipalities

Public payers and municipalities set reference prices via tenders in 2024, concentrating buyer power; OECD data show public financing still dominates health spending (around 70% in many countries), budget cycles and policy shifts reallocate occupancy rates, compliance audits drive contract renewals, and delayed payments (often 60+ days in some markets) strain working capital.

Families with price–quality trade-offs

Private-pay families compare care outcomes, amenities and proximity and exert selective power, with 87% of consumers consulting online reviews (BrightLocal 2024) making facilities highly review-sensitive. Transparency and published incident reports raise price–quality sensitivity, while roughly 50% of admissions are urgent or post-acute, limiting negotiation at point of need. Location constraints further reduce bargaining leverage; ancillary services (therapy, private rooms, extras) remain discretionary levers that can add 5–10% to facility revenue.

Insurers and managed care

Insurers push bundled rates and outcome-linked payments, compressing provider margins as Medicare Advantage enrollment topped 30 million in 2024 (over 50% of beneficiaries), increasing payer leverage. Network inclusion drives volumes but often at 15–30% discounted rates, shifting revenue mix toward lower-margin cases. Data sharing and KPI commitments transfer financial risk to providers, with HRRP-style readmission penalties up to 3% and contract renegotiations tied to readmission and functional improvement metrics.

High switching frictions

Once admitted, residents face emotional, medical, and logistical barriers to switch, reducing ongoing buyer power; care continuity and specialized needs create lock-in, while 2024 US nursing home occupancy hovered around 81%, underscoring fewer open beds and higher switching frictions. Pre-admission choice and waiting lists keep headline pricing under pressure, but discharge risk rises quickly if published quality scores fall.

- Lock-in: clinical needs and continuity

- Market pressure: waiting lists limit price hikes

- Risk: quality declines raise discharge probability

Occupancy-driven leverage

Reputation events—positive or negative—can rapidly move occupancy and flip pricing power within weeks.

- Occupancy dip → discounts

- Capacity constraint → waiting lists

- Seasonality → negotiation windows

- Reputation → rapid occupancy shifts

Mixed buyer power: public payers dominate, insurers and families shape pricing and reputation

Buyers exert mixed power: public payers (≈70% health financing) and insurers (Medicare Advantage 30M in 2024) push prices and outcomes, while private families (87% consult online reviews) drive reputation sensitivity. Occupancy (US nursing homes ~81% in 2024) and urgent admissions limit switching, but local dips prompt rapid discounting.

| Metric | 2024 |

|---|---|

| Public financing | ~70% |

| Medicare Advantage | 30M enrollees |

| Online review consult | 87% |

| NH occupancy (US) | ~81% |

What You See Is What You Get

Clariane Porter's Five Forces Analysis

This Clariane Porter's Five Forces Analysis preview is the exact, fully formatted document you’ll receive after purchase. It contains the complete assessment and conclusions—no placeholders or samples. You’ll get instant access to this identical file, ready to download and use.

Don't Miss the Bigger Picture

Clariane's Porter’s Five Forces analysis distills competitive pressures—buyer and supplier power, rivalry, substitutes, and entry threats—into clear strategic implications. It highlights where Clariane holds leverage and where external risks could erode margins. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Clariane’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarce skilled caregivers

Registered nurses, aides and therapists face chronic shortages across Europe, with 2024 vacancy rates averaging about 9% and turnover often 15–20%, giving labor suppliers strong leverage over wages and conditions. Clariane must meet statutory staffing ratios (often 1:4–1:8 in acute and elderly care), constraining flexibility in wage negotiations. High unionization and regulatory mandates further amplify supplier power, while turnover drives recruitment and training costs that can add up to roughly 10–15% of annual labor spend.

Pharma, medical devices, and consumables

Clinical supplies are highly regulated and quality-critical, giving approved vendors moderate bargaining power; market concentration (top 10 device firms account for roughly 40% of global revenues) limits substitutability. Bulk purchasing and frame agreements can temper prices, but 2021–23 supply shocks and intermittent shortages disrupted operations. Compliance and traceability rules (UDI, serialization) restrict alternative sourcing, while medical input inflation (about 5–7% in 2023–24) pressures margins.

Real estate, utilities, and maintenance

Clariane faces high supplier power in real estate, utilities and maintenance: nursing homes need specialized, code-compliant facilities that tie operators to landlords with long leases (commonly 5–20 years) and retrofits that often exceed $5,000 per bed, limiting relocation flexibility; nationwide occupancy near 78% in 2024 keeps demand for such sites tight. Energy price volatility and spikes in wholesale natural gas/electricity materially raise operating cost exposure, while certified preventive-maintenance vendors command scheduling leverage due to licensing and certification requirements.

IT/EHR and interoperability vendors

Clinical software, EHRs and telecare platforms create high switching costs—integration, training and data migration can run into millions—while the global EHR market was valued at about $35 billion in 2024, reinforcing vendor leverage. Cybersecurity and HIPAA/privacy compliance narrow viable vendors, and mandatory upgrade clauses let vendors push recurring price escalators. Service outages directly harm care quality metrics tied to CMS audits and reimbursements, increasing supplier power.

- Market: ~35B 2024

- Switching cost: often millions

- Compliance: HIPAA narrows vendors

- Upgrades: recurring escalators

- Outages: affect CMS quality/audits

Staffing agencies and temp pools

Agency labor fills clinical gaps but carries a 20–40% premium versus payroll, giving agencies strong spot-market power; US staffing revenue reached about 180 billion in 2024, underscoring scale. Absentee peaks or outbreaks can raise temp demand by 30–50%, pressuring margins if internal hiring pipelines are weak, while tight SLAs limit renegotiation during crises.

- Premiums: 20–40% above payroll

- Market size: ~180 billion (US, 2024)

- Demand spikes: +30–50% in outbreaks

- Risk: margin erosion if internal pipeline weak

- SLA constraint: limited renegotiation in crises

Clinical supplier squeeze: RN vacancy ~9%, agency premiums 20–40%

Supplier power is high: RN vacancies ~9% and turnover 15–20% (2024) push wages and agency premiums 20–40%, eroding margins. Clinical supply concentration (top10 ≈40% revenues) and medical inflation 5–7% (2023–24) limit sourcing flexibility. EHR market ~$35B (2024) and US staffing ~$180B (2024) raise switching and vendor leverage.

| Metric | 2024 |

|---|---|

| RN vacancy | ~9% |

| Turnover | 15–20% |

| Agency premium | 20–40% |

| EHR market | $35B |

| US staffing | $180B |

What is included in the product

Tailored Porter's Five Forces for Clariane that uncovers key drivers of competition, evaluates supplier and buyer power, identifies disruptive substitutes and emerging threats, and assesses entry barriers to clarify pricing influence and profitability.

Clear one-sheet Porter's Five Forces for Clariane—customize pressure levels, swap in your data, and instantly visualize strategic pressure with a spider chart for quick decision-making.

Customers Bargaining Power

Public payers and municipalities

Public payers and municipalities set reference prices via tenders in 2024, concentrating buyer power; OECD data show public financing still dominates health spending (around 70% in many countries), budget cycles and policy shifts reallocate occupancy rates, compliance audits drive contract renewals, and delayed payments (often 60+ days in some markets) strain working capital.

Families with price–quality trade-offs

Private-pay families compare care outcomes, amenities and proximity and exert selective power, with 87% of consumers consulting online reviews (BrightLocal 2024) making facilities highly review-sensitive. Transparency and published incident reports raise price–quality sensitivity, while roughly 50% of admissions are urgent or post-acute, limiting negotiation at point of need. Location constraints further reduce bargaining leverage; ancillary services (therapy, private rooms, extras) remain discretionary levers that can add 5–10% to facility revenue.

Insurers and managed care

Insurers push bundled rates and outcome-linked payments, compressing provider margins as Medicare Advantage enrollment topped 30 million in 2024 (over 50% of beneficiaries), increasing payer leverage. Network inclusion drives volumes but often at 15–30% discounted rates, shifting revenue mix toward lower-margin cases. Data sharing and KPI commitments transfer financial risk to providers, with HRRP-style readmission penalties up to 3% and contract renegotiations tied to readmission and functional improvement metrics.

High switching frictions

Once admitted, residents face emotional, medical, and logistical barriers to switch, reducing ongoing buyer power; care continuity and specialized needs create lock-in, while 2024 US nursing home occupancy hovered around 81%, underscoring fewer open beds and higher switching frictions. Pre-admission choice and waiting lists keep headline pricing under pressure, but discharge risk rises quickly if published quality scores fall.

- Lock-in: clinical needs and continuity

- Market pressure: waiting lists limit price hikes

- Risk: quality declines raise discharge probability

Occupancy-driven leverage

Reputation events—positive or negative—can rapidly move occupancy and flip pricing power within weeks.

- Occupancy dip → discounts

- Capacity constraint → waiting lists

- Seasonality → negotiation windows

- Reputation → rapid occupancy shifts

Mixed buyer power: public payers dominate, insurers and families shape pricing and reputation

Buyers exert mixed power: public payers (≈70% health financing) and insurers (Medicare Advantage 30M in 2024) push prices and outcomes, while private families (87% consult online reviews) drive reputation sensitivity. Occupancy (US nursing homes ~81% in 2024) and urgent admissions limit switching, but local dips prompt rapid discounting.

| Metric | 2024 |

|---|---|

| Public financing | ~70% |

| Medicare Advantage | 30M enrollees |

| Online review consult | 87% |

| NH occupancy (US) | ~81% |

What You See Is What You Get

Clariane Porter's Five Forces Analysis

This Clariane Porter's Five Forces Analysis preview is the exact, fully formatted document you’ll receive after purchase. It contains the complete assessment and conclusions—no placeholders or samples. You’ll get instant access to this identical file, ready to download and use.

Description

Don't Miss the Bigger Picture

Clariane's Porter’s Five Forces analysis distills competitive pressures—buyer and supplier power, rivalry, substitutes, and entry threats—into clear strategic implications. It highlights where Clariane holds leverage and where external risks could erode margins. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Clariane’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarce skilled caregivers

Registered nurses, aides and therapists face chronic shortages across Europe, with 2024 vacancy rates averaging about 9% and turnover often 15–20%, giving labor suppliers strong leverage over wages and conditions. Clariane must meet statutory staffing ratios (often 1:4–1:8 in acute and elderly care), constraining flexibility in wage negotiations. High unionization and regulatory mandates further amplify supplier power, while turnover drives recruitment and training costs that can add up to roughly 10–15% of annual labor spend.

Pharma, medical devices, and consumables

Clinical supplies are highly regulated and quality-critical, giving approved vendors moderate bargaining power; market concentration (top 10 device firms account for roughly 40% of global revenues) limits substitutability. Bulk purchasing and frame agreements can temper prices, but 2021–23 supply shocks and intermittent shortages disrupted operations. Compliance and traceability rules (UDI, serialization) restrict alternative sourcing, while medical input inflation (about 5–7% in 2023–24) pressures margins.

Real estate, utilities, and maintenance

Clariane faces high supplier power in real estate, utilities and maintenance: nursing homes need specialized, code-compliant facilities that tie operators to landlords with long leases (commonly 5–20 years) and retrofits that often exceed $5,000 per bed, limiting relocation flexibility; nationwide occupancy near 78% in 2024 keeps demand for such sites tight. Energy price volatility and spikes in wholesale natural gas/electricity materially raise operating cost exposure, while certified preventive-maintenance vendors command scheduling leverage due to licensing and certification requirements.

IT/EHR and interoperability vendors

Clinical software, EHRs and telecare platforms create high switching costs—integration, training and data migration can run into millions—while the global EHR market was valued at about $35 billion in 2024, reinforcing vendor leverage. Cybersecurity and HIPAA/privacy compliance narrow viable vendors, and mandatory upgrade clauses let vendors push recurring price escalators. Service outages directly harm care quality metrics tied to CMS audits and reimbursements, increasing supplier power.

- Market: ~35B 2024

- Switching cost: often millions

- Compliance: HIPAA narrows vendors

- Upgrades: recurring escalators

- Outages: affect CMS quality/audits

Staffing agencies and temp pools

Agency labor fills clinical gaps but carries a 20–40% premium versus payroll, giving agencies strong spot-market power; US staffing revenue reached about 180 billion in 2024, underscoring scale. Absentee peaks or outbreaks can raise temp demand by 30–50%, pressuring margins if internal hiring pipelines are weak, while tight SLAs limit renegotiation during crises.

- Premiums: 20–40% above payroll

- Market size: ~180 billion (US, 2024)

- Demand spikes: +30–50% in outbreaks

- Risk: margin erosion if internal pipeline weak

- SLA constraint: limited renegotiation in crises

Clinical supplier squeeze: RN vacancy ~9%, agency premiums 20–40%

Supplier power is high: RN vacancies ~9% and turnover 15–20% (2024) push wages and agency premiums 20–40%, eroding margins. Clinical supply concentration (top10 ≈40% revenues) and medical inflation 5–7% (2023–24) limit sourcing flexibility. EHR market ~$35B (2024) and US staffing ~$180B (2024) raise switching and vendor leverage.

| Metric | 2024 |

|---|---|

| RN vacancy | ~9% |

| Turnover | 15–20% |

| Agency premium | 20–40% |

| EHR market | $35B |

| US staffing | $180B |

What is included in the product

Tailored Porter's Five Forces for Clariane that uncovers key drivers of competition, evaluates supplier and buyer power, identifies disruptive substitutes and emerging threats, and assesses entry barriers to clarify pricing influence and profitability.

Clear one-sheet Porter's Five Forces for Clariane—customize pressure levels, swap in your data, and instantly visualize strategic pressure with a spider chart for quick decision-making.

Customers Bargaining Power

Public payers and municipalities

Public payers and municipalities set reference prices via tenders in 2024, concentrating buyer power; OECD data show public financing still dominates health spending (around 70% in many countries), budget cycles and policy shifts reallocate occupancy rates, compliance audits drive contract renewals, and delayed payments (often 60+ days in some markets) strain working capital.

Families with price–quality trade-offs

Private-pay families compare care outcomes, amenities and proximity and exert selective power, with 87% of consumers consulting online reviews (BrightLocal 2024) making facilities highly review-sensitive. Transparency and published incident reports raise price–quality sensitivity, while roughly 50% of admissions are urgent or post-acute, limiting negotiation at point of need. Location constraints further reduce bargaining leverage; ancillary services (therapy, private rooms, extras) remain discretionary levers that can add 5–10% to facility revenue.

Insurers and managed care

Insurers push bundled rates and outcome-linked payments, compressing provider margins as Medicare Advantage enrollment topped 30 million in 2024 (over 50% of beneficiaries), increasing payer leverage. Network inclusion drives volumes but often at 15–30% discounted rates, shifting revenue mix toward lower-margin cases. Data sharing and KPI commitments transfer financial risk to providers, with HRRP-style readmission penalties up to 3% and contract renegotiations tied to readmission and functional improvement metrics.

High switching frictions

Once admitted, residents face emotional, medical, and logistical barriers to switch, reducing ongoing buyer power; care continuity and specialized needs create lock-in, while 2024 US nursing home occupancy hovered around 81%, underscoring fewer open beds and higher switching frictions. Pre-admission choice and waiting lists keep headline pricing under pressure, but discharge risk rises quickly if published quality scores fall.

- Lock-in: clinical needs and continuity

- Market pressure: waiting lists limit price hikes

- Risk: quality declines raise discharge probability

Occupancy-driven leverage

Reputation events—positive or negative—can rapidly move occupancy and flip pricing power within weeks.

- Occupancy dip → discounts

- Capacity constraint → waiting lists

- Seasonality → negotiation windows

- Reputation → rapid occupancy shifts

Mixed buyer power: public payers dominate, insurers and families shape pricing and reputation

Buyers exert mixed power: public payers (≈70% health financing) and insurers (Medicare Advantage 30M in 2024) push prices and outcomes, while private families (87% consult online reviews) drive reputation sensitivity. Occupancy (US nursing homes ~81% in 2024) and urgent admissions limit switching, but local dips prompt rapid discounting.

| Metric | 2024 |

|---|---|

| Public financing | ~70% |

| Medicare Advantage | 30M enrollees |

| Online review consult | 87% |

| NH occupancy (US) | ~81% |

What You See Is What You Get

Clariane Porter's Five Forces Analysis

This Clariane Porter's Five Forces Analysis preview is the exact, fully formatted document you’ll receive after purchase. It contains the complete assessment and conclusions—no placeholders or samples. You’ll get instant access to this identical file, ready to download and use.