Net Serviços de Comunicação Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

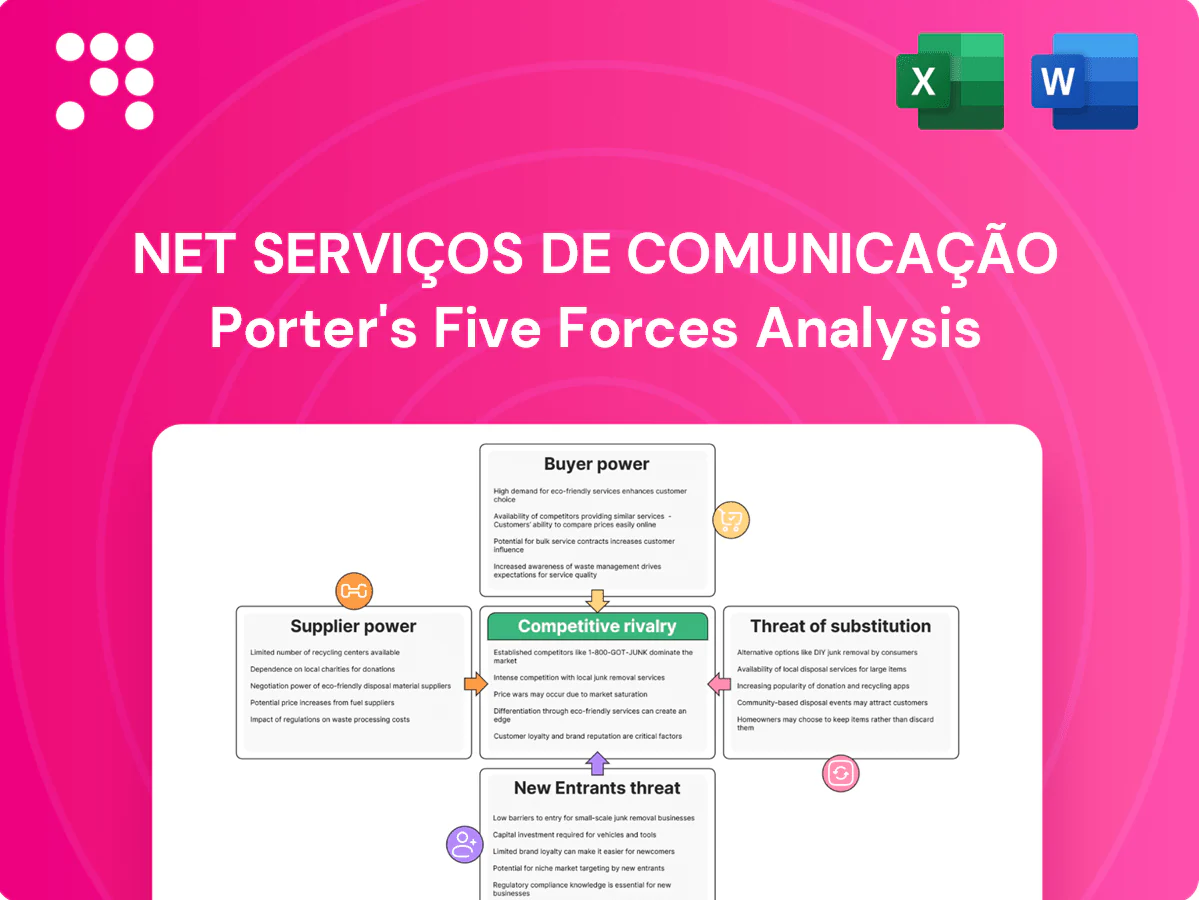

Net Serviços de Comunicação faces strong buyer power and intense rivalry amid growing digital substitutes, while supplier leverage and regulatory barriers produce moderate pressures. New entrants threaten niche digital segments, compressing pricing power. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Net Serviços de Comunicação’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated network vendors

Core RAN and transport gear come from three dominant global vendors—Ericsson, Nokia and Huawei—concentrating supply and raising switching costs; procurement lead times for major RAN orders often extend to 6–12 months, increasing operational risk.

Vendor lock-in reduces Claro’s pricing and roadmap leverage, but multi-vendor deployments and standardized interfaces (e.g., O-RAN initiatives) mitigate dependency and lower marginal switching burden.

Geopolitical and Brazilian compliance pressures (import controls, security reviews) further shape vendor choice and bargaining dynamics, often adding regulatory timelines and cost premiums to procurement.

Tower and infrastructure lessors

Dependence on towercos and fiber neutral hosts creates recurring lease obligations, with contract tenors typically 5–10 years and renewal-linked escalators giving suppliers leverage. Site scarcity in dense urban corridors heightens that power. América Móvil’s scale across 18 countries and bulk purchasing secures more favorable terms, while network sharing and small cells partially offset site dependency.

Content and channel rights

Premium TV and sports rights holders exert strong pricing power over pay-TV bundles, with Brazil pay-TV subscribers declining to about 8.2 million in 2024, pressuring operators to absorb higher fees or raise ARPU. Shifts to streaming exclusives push content costs up and can erode bundle differentiation. Claro mitigates by expanding OTT aggregation and cross-bundling across mobile, fixed and TV. Content disputes risk churn and attract ANATEL scrutiny over service quality.

Spectrum and regulatory inputs

Spectrum allocation by ANATEL, with assignment fees and coverage/quality obligations, materially shapes Net Serviços de Comunicação’s cost base and rollout timing. The 2021 5G auction (BRL 47.2 billion awarded) exemplifies state leverage via auction design and limited bands, constraining supplier power despite operator scale. Compliance demands on universal service and quality reduce operational flexibility. A strategic mix of 700 MHz, 3.5 GHz and 26 GHz bands improves capacity and bargaining posture.

- ANATEL fees and rollout obligations increase fixed costs

- 2021 5G auction: BRL 47.2 billion — shows state leverage

- Compliance on quality/universal service limits flexibility

- Low/mid/high band mix strengthens capacity and negotiating power

Handset and device ecosystems

Flagship devices from a few OEMs remain key to 5G uptake and ARPU uplift; global 5G subscriptions surpassed 1.8 billion in 2024, concentrating supplier leverage in device launches and chip supply. Subsidy policies and retail channel availability can rapidly shift bargaining power, while eSIM adoption and open financing increase supplier diversification. Bundled device plans and trade-in programs enhance Net Serviços de Comunicação’s negotiation leverage with OEMs.

- 2024: 1.8 billion 5G subs

- Subsidies/channel sway power

- eSIM + financing diversify sourcing

- Bundles/trade-ins boost leverage

RAN vendor concentration, ANATEL fees and long leases raise costs; 1.8bn 5G subs boost OEM leverage

Three dominant RAN vendors (Ericsson, Nokia, Huawei) and 6–12 month lead times concentrate supplier power; ANATEL spectrum fees and long tower lease tenors (5–10 yrs) add cost rigidity. 2024: 1.8bn 5G subs increase OEM leverage, but América Móvil scale, multi-vendor/O‑RAN and network sharing mitigate switching costs.

| Metric | Value |

|---|---|

| 2021 5G auction | BRL 47.2bn |

| RAN lead times | 6–12 months |

| Tower lease tenor | 5–10 yrs |

| 5G subs (2024) | 1.8bn |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power, threat of substitutes and entry barriers specific to Net Serviços de Comunicação, highlighting disruptive forces and emerging threats to market share and profitability while identifying strategic levers to defend margins and guide growth.

A clear one-sheet Porter's Five Forces for Net Serviços de Comunicação—quickly diagnose competitive pain points, prioritize strategic responses, and slot straight into decks or operational plans.

Customers Bargaining Power

Price-sensitive mass market

Brazilian consumers are value-focused, amplifying price elasticity and promo hunting in a market of ≈230 million mobile lines. Number portability (since 2008) eases switching, heightening buyer power. Prepaid and control plans comprise over half the base, increasing transparency and reducing lock-in. Claro uses bundles and loyalty programs to stabilize ARPU and cut churn.

Enterprise and public sector accounts

Large enterprise and public sector RFPs and multi-year contracts force carriers to offer mid-teens discounts and firm SLAs, compressing margins. Many buyers dual-source across carriers—roughly 30–50% of major accounts—boosting negotiation leverage. Convergence of fixed, mobile, cloud and IoT (enterprise cloud adoption ~80% in 2024) increases deal size but scrutiny. Vertical solutions and managed services shift focus from pure price to value-based contracts.

Digital comparison and omnichannel

Online comparators and social media make pricing and quality highly visible, driving customer scrutiny in 2024 and contributing to an industry churn around 3.5% in Brazil. Self-service portability accelerates switching if perceived value drops, shortening retention windows. Claro’s apps and analytics enable targeted retention offers and personalized bundles to reduce churn. Transparent fees and simpler plan architecture can materially dampen buyer bargaining power.

Quality-of-service expectations

Latency, coverage and streaming performance now drive perceived value for Net Serviços: in 2024 5G and FTTH rollouts have doubled peak speeds versus 4G, and sub-30ms latency in urban cells is a customer expectation. A 10-point NPS decline in dense markets correlates with materially higher churn. Service credits and proactive care cut dissatisfaction and blunt customer bargaining power.

- Latency: sub-30ms expected

- Coverage: 5G+FTTH uplift = ~2x peak speeds

- Retention: service credits reduce churn pressure

Bundle stickiness vs flexibility

Quad-play bundles raise switching costs by combining broadband, TV, mobile and fixed voice on one bill, anchoring ARPU and reducing churn; in 2024 over 40% of Brazilian households still take multi-service packs. Month-to-month OTT options, however, grew among new TV subscribers in 2024, increasing flexibility for content-only users. Modular add-ons, family plans, contract benefits and device financing further balance retention and choice.

- bundle_retention: higher ARPU, lower churn

- ott_flex: >40% new TV subs chose month-to-month in 2024

- modular_addons: targeted upsell potential

- contracts_devices: anchor via financing and benefits

Brazil buyers drive bargaining: ≈230M, churn ~3.5%

Brazilian buyers exert strong price and switch power: ≈230M mobile lines, churn ~3.5% (2024), enterprise dual-sourcing 30–50% and >40% new TV subs chose month-to-month in 2024; QoS (sub-30ms, 2x peak speeds via 5G/FTTH) and bundles (40%+ multi-service households) moderate bargaining via retention and value plays.

| Metric | 2024 |

|---|---|

| Mobile lines | ≈230M |

| Churn | ~3.5% |

| Enterprise dual-source | 30–50% |

| New TV OTT month-to-month | >40% |

What You See Is What You Get

Net Serviços de Comunicação Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Net Serviços de Comunicação you'll receive after purchase—fully formatted, final and ready to use. The assessment covers supplier power, buyer power, competitive rivalry, threat of substitutes and barriers to entry with actionable insights. No samples or placeholders; purchase grants immediate download of this identical file.

Go Beyond the Preview—Access the Full Strategic Report

Net Serviços de Comunicação faces strong buyer power and intense rivalry amid growing digital substitutes, while supplier leverage and regulatory barriers produce moderate pressures. New entrants threaten niche digital segments, compressing pricing power. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Net Serviços de Comunicação’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated network vendors

Core RAN and transport gear come from three dominant global vendors—Ericsson, Nokia and Huawei—concentrating supply and raising switching costs; procurement lead times for major RAN orders often extend to 6–12 months, increasing operational risk.

Vendor lock-in reduces Claro’s pricing and roadmap leverage, but multi-vendor deployments and standardized interfaces (e.g., O-RAN initiatives) mitigate dependency and lower marginal switching burden.

Geopolitical and Brazilian compliance pressures (import controls, security reviews) further shape vendor choice and bargaining dynamics, often adding regulatory timelines and cost premiums to procurement.

Tower and infrastructure lessors

Dependence on towercos and fiber neutral hosts creates recurring lease obligations, with contract tenors typically 5–10 years and renewal-linked escalators giving suppliers leverage. Site scarcity in dense urban corridors heightens that power. América Móvil’s scale across 18 countries and bulk purchasing secures more favorable terms, while network sharing and small cells partially offset site dependency.

Content and channel rights

Premium TV and sports rights holders exert strong pricing power over pay-TV bundles, with Brazil pay-TV subscribers declining to about 8.2 million in 2024, pressuring operators to absorb higher fees or raise ARPU. Shifts to streaming exclusives push content costs up and can erode bundle differentiation. Claro mitigates by expanding OTT aggregation and cross-bundling across mobile, fixed and TV. Content disputes risk churn and attract ANATEL scrutiny over service quality.

Spectrum and regulatory inputs

Spectrum allocation by ANATEL, with assignment fees and coverage/quality obligations, materially shapes Net Serviços de Comunicação’s cost base and rollout timing. The 2021 5G auction (BRL 47.2 billion awarded) exemplifies state leverage via auction design and limited bands, constraining supplier power despite operator scale. Compliance demands on universal service and quality reduce operational flexibility. A strategic mix of 700 MHz, 3.5 GHz and 26 GHz bands improves capacity and bargaining posture.

- ANATEL fees and rollout obligations increase fixed costs

- 2021 5G auction: BRL 47.2 billion — shows state leverage

- Compliance on quality/universal service limits flexibility

- Low/mid/high band mix strengthens capacity and negotiating power

Handset and device ecosystems

Flagship devices from a few OEMs remain key to 5G uptake and ARPU uplift; global 5G subscriptions surpassed 1.8 billion in 2024, concentrating supplier leverage in device launches and chip supply. Subsidy policies and retail channel availability can rapidly shift bargaining power, while eSIM adoption and open financing increase supplier diversification. Bundled device plans and trade-in programs enhance Net Serviços de Comunicação’s negotiation leverage with OEMs.

- 2024: 1.8 billion 5G subs

- Subsidies/channel sway power

- eSIM + financing diversify sourcing

- Bundles/trade-ins boost leverage

RAN vendor concentration, ANATEL fees and long leases raise costs; 1.8bn 5G subs boost OEM leverage

Three dominant RAN vendors (Ericsson, Nokia, Huawei) and 6–12 month lead times concentrate supplier power; ANATEL spectrum fees and long tower lease tenors (5–10 yrs) add cost rigidity. 2024: 1.8bn 5G subs increase OEM leverage, but América Móvil scale, multi-vendor/O‑RAN and network sharing mitigate switching costs.

| Metric | Value |

|---|---|

| 2021 5G auction | BRL 47.2bn |

| RAN lead times | 6–12 months |

| Tower lease tenor | 5–10 yrs |

| 5G subs (2024) | 1.8bn |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power, threat of substitutes and entry barriers specific to Net Serviços de Comunicação, highlighting disruptive forces and emerging threats to market share and profitability while identifying strategic levers to defend margins and guide growth.

A clear one-sheet Porter's Five Forces for Net Serviços de Comunicação—quickly diagnose competitive pain points, prioritize strategic responses, and slot straight into decks or operational plans.

Customers Bargaining Power

Price-sensitive mass market

Brazilian consumers are value-focused, amplifying price elasticity and promo hunting in a market of ≈230 million mobile lines. Number portability (since 2008) eases switching, heightening buyer power. Prepaid and control plans comprise over half the base, increasing transparency and reducing lock-in. Claro uses bundles and loyalty programs to stabilize ARPU and cut churn.

Enterprise and public sector accounts

Large enterprise and public sector RFPs and multi-year contracts force carriers to offer mid-teens discounts and firm SLAs, compressing margins. Many buyers dual-source across carriers—roughly 30–50% of major accounts—boosting negotiation leverage. Convergence of fixed, mobile, cloud and IoT (enterprise cloud adoption ~80% in 2024) increases deal size but scrutiny. Vertical solutions and managed services shift focus from pure price to value-based contracts.

Digital comparison and omnichannel

Online comparators and social media make pricing and quality highly visible, driving customer scrutiny in 2024 and contributing to an industry churn around 3.5% in Brazil. Self-service portability accelerates switching if perceived value drops, shortening retention windows. Claro’s apps and analytics enable targeted retention offers and personalized bundles to reduce churn. Transparent fees and simpler plan architecture can materially dampen buyer bargaining power.

Quality-of-service expectations

Latency, coverage and streaming performance now drive perceived value for Net Serviços: in 2024 5G and FTTH rollouts have doubled peak speeds versus 4G, and sub-30ms latency in urban cells is a customer expectation. A 10-point NPS decline in dense markets correlates with materially higher churn. Service credits and proactive care cut dissatisfaction and blunt customer bargaining power.

- Latency: sub-30ms expected

- Coverage: 5G+FTTH uplift = ~2x peak speeds

- Retention: service credits reduce churn pressure

Bundle stickiness vs flexibility

Quad-play bundles raise switching costs by combining broadband, TV, mobile and fixed voice on one bill, anchoring ARPU and reducing churn; in 2024 over 40% of Brazilian households still take multi-service packs. Month-to-month OTT options, however, grew among new TV subscribers in 2024, increasing flexibility for content-only users. Modular add-ons, family plans, contract benefits and device financing further balance retention and choice.

- bundle_retention: higher ARPU, lower churn

- ott_flex: >40% new TV subs chose month-to-month in 2024

- modular_addons: targeted upsell potential

- contracts_devices: anchor via financing and benefits

Brazil buyers drive bargaining: ≈230M, churn ~3.5%

Brazilian buyers exert strong price and switch power: ≈230M mobile lines, churn ~3.5% (2024), enterprise dual-sourcing 30–50% and >40% new TV subs chose month-to-month in 2024; QoS (sub-30ms, 2x peak speeds via 5G/FTTH) and bundles (40%+ multi-service households) moderate bargaining via retention and value plays.

| Metric | 2024 |

|---|---|

| Mobile lines | ≈230M |

| Churn | ~3.5% |

| Enterprise dual-source | 30–50% |

| New TV OTT month-to-month | >40% |

What You See Is What You Get

Net Serviços de Comunicação Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Net Serviços de Comunicação you'll receive after purchase—fully formatted, final and ready to use. The assessment covers supplier power, buyer power, competitive rivalry, threat of substitutes and barriers to entry with actionable insights. No samples or placeholders; purchase grants immediate download of this identical file.

Description

Go Beyond the Preview—Access the Full Strategic Report

Net Serviços de Comunicação faces strong buyer power and intense rivalry amid growing digital substitutes, while supplier leverage and regulatory barriers produce moderate pressures. New entrants threaten niche digital segments, compressing pricing power. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Net Serviços de Comunicação’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated network vendors

Core RAN and transport gear come from three dominant global vendors—Ericsson, Nokia and Huawei—concentrating supply and raising switching costs; procurement lead times for major RAN orders often extend to 6–12 months, increasing operational risk.

Vendor lock-in reduces Claro’s pricing and roadmap leverage, but multi-vendor deployments and standardized interfaces (e.g., O-RAN initiatives) mitigate dependency and lower marginal switching burden.

Geopolitical and Brazilian compliance pressures (import controls, security reviews) further shape vendor choice and bargaining dynamics, often adding regulatory timelines and cost premiums to procurement.

Tower and infrastructure lessors

Dependence on towercos and fiber neutral hosts creates recurring lease obligations, with contract tenors typically 5–10 years and renewal-linked escalators giving suppliers leverage. Site scarcity in dense urban corridors heightens that power. América Móvil’s scale across 18 countries and bulk purchasing secures more favorable terms, while network sharing and small cells partially offset site dependency.

Content and channel rights

Premium TV and sports rights holders exert strong pricing power over pay-TV bundles, with Brazil pay-TV subscribers declining to about 8.2 million in 2024, pressuring operators to absorb higher fees or raise ARPU. Shifts to streaming exclusives push content costs up and can erode bundle differentiation. Claro mitigates by expanding OTT aggregation and cross-bundling across mobile, fixed and TV. Content disputes risk churn and attract ANATEL scrutiny over service quality.

Spectrum and regulatory inputs

Spectrum allocation by ANATEL, with assignment fees and coverage/quality obligations, materially shapes Net Serviços de Comunicação’s cost base and rollout timing. The 2021 5G auction (BRL 47.2 billion awarded) exemplifies state leverage via auction design and limited bands, constraining supplier power despite operator scale. Compliance demands on universal service and quality reduce operational flexibility. A strategic mix of 700 MHz, 3.5 GHz and 26 GHz bands improves capacity and bargaining posture.

- ANATEL fees and rollout obligations increase fixed costs

- 2021 5G auction: BRL 47.2 billion — shows state leverage

- Compliance on quality/universal service limits flexibility

- Low/mid/high band mix strengthens capacity and negotiating power

Handset and device ecosystems

Flagship devices from a few OEMs remain key to 5G uptake and ARPU uplift; global 5G subscriptions surpassed 1.8 billion in 2024, concentrating supplier leverage in device launches and chip supply. Subsidy policies and retail channel availability can rapidly shift bargaining power, while eSIM adoption and open financing increase supplier diversification. Bundled device plans and trade-in programs enhance Net Serviços de Comunicação’s negotiation leverage with OEMs.

- 2024: 1.8 billion 5G subs

- Subsidies/channel sway power

- eSIM + financing diversify sourcing

- Bundles/trade-ins boost leverage

RAN vendor concentration, ANATEL fees and long leases raise costs; 1.8bn 5G subs boost OEM leverage

Three dominant RAN vendors (Ericsson, Nokia, Huawei) and 6–12 month lead times concentrate supplier power; ANATEL spectrum fees and long tower lease tenors (5–10 yrs) add cost rigidity. 2024: 1.8bn 5G subs increase OEM leverage, but América Móvil scale, multi-vendor/O‑RAN and network sharing mitigate switching costs.

| Metric | Value |

|---|---|

| 2021 5G auction | BRL 47.2bn |

| RAN lead times | 6–12 months |

| Tower lease tenor | 5–10 yrs |

| 5G subs (2024) | 1.8bn |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power, threat of substitutes and entry barriers specific to Net Serviços de Comunicação, highlighting disruptive forces and emerging threats to market share and profitability while identifying strategic levers to defend margins and guide growth.

A clear one-sheet Porter's Five Forces for Net Serviços de Comunicação—quickly diagnose competitive pain points, prioritize strategic responses, and slot straight into decks or operational plans.

Customers Bargaining Power

Price-sensitive mass market

Brazilian consumers are value-focused, amplifying price elasticity and promo hunting in a market of ≈230 million mobile lines. Number portability (since 2008) eases switching, heightening buyer power. Prepaid and control plans comprise over half the base, increasing transparency and reducing lock-in. Claro uses bundles and loyalty programs to stabilize ARPU and cut churn.

Enterprise and public sector accounts

Large enterprise and public sector RFPs and multi-year contracts force carriers to offer mid-teens discounts and firm SLAs, compressing margins. Many buyers dual-source across carriers—roughly 30–50% of major accounts—boosting negotiation leverage. Convergence of fixed, mobile, cloud and IoT (enterprise cloud adoption ~80% in 2024) increases deal size but scrutiny. Vertical solutions and managed services shift focus from pure price to value-based contracts.

Digital comparison and omnichannel

Online comparators and social media make pricing and quality highly visible, driving customer scrutiny in 2024 and contributing to an industry churn around 3.5% in Brazil. Self-service portability accelerates switching if perceived value drops, shortening retention windows. Claro’s apps and analytics enable targeted retention offers and personalized bundles to reduce churn. Transparent fees and simpler plan architecture can materially dampen buyer bargaining power.

Quality-of-service expectations

Latency, coverage and streaming performance now drive perceived value for Net Serviços: in 2024 5G and FTTH rollouts have doubled peak speeds versus 4G, and sub-30ms latency in urban cells is a customer expectation. A 10-point NPS decline in dense markets correlates with materially higher churn. Service credits and proactive care cut dissatisfaction and blunt customer bargaining power.

- Latency: sub-30ms expected

- Coverage: 5G+FTTH uplift = ~2x peak speeds

- Retention: service credits reduce churn pressure

Bundle stickiness vs flexibility

Quad-play bundles raise switching costs by combining broadband, TV, mobile and fixed voice on one bill, anchoring ARPU and reducing churn; in 2024 over 40% of Brazilian households still take multi-service packs. Month-to-month OTT options, however, grew among new TV subscribers in 2024, increasing flexibility for content-only users. Modular add-ons, family plans, contract benefits and device financing further balance retention and choice.

- bundle_retention: higher ARPU, lower churn

- ott_flex: >40% new TV subs chose month-to-month in 2024

- modular_addons: targeted upsell potential

- contracts_devices: anchor via financing and benefits

Brazil buyers drive bargaining: ≈230M, churn ~3.5%

Brazilian buyers exert strong price and switch power: ≈230M mobile lines, churn ~3.5% (2024), enterprise dual-sourcing 30–50% and >40% new TV subs chose month-to-month in 2024; QoS (sub-30ms, 2x peak speeds via 5G/FTTH) and bundles (40%+ multi-service households) moderate bargaining via retention and value plays.

| Metric | 2024 |

|---|---|

| Mobile lines | ≈230M |

| Churn | ~3.5% |

| Enterprise dual-source | 30–50% |

| New TV OTT month-to-month | >40% |

What You See Is What You Get

Net Serviços de Comunicação Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Net Serviços de Comunicação you'll receive after purchase—fully formatted, final and ready to use. The assessment covers supplier power, buyer power, competitive rivalry, threat of substitutes and barriers to entry with actionable insights. No samples or placeholders; purchase grants immediate download of this identical file.