Clarus Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

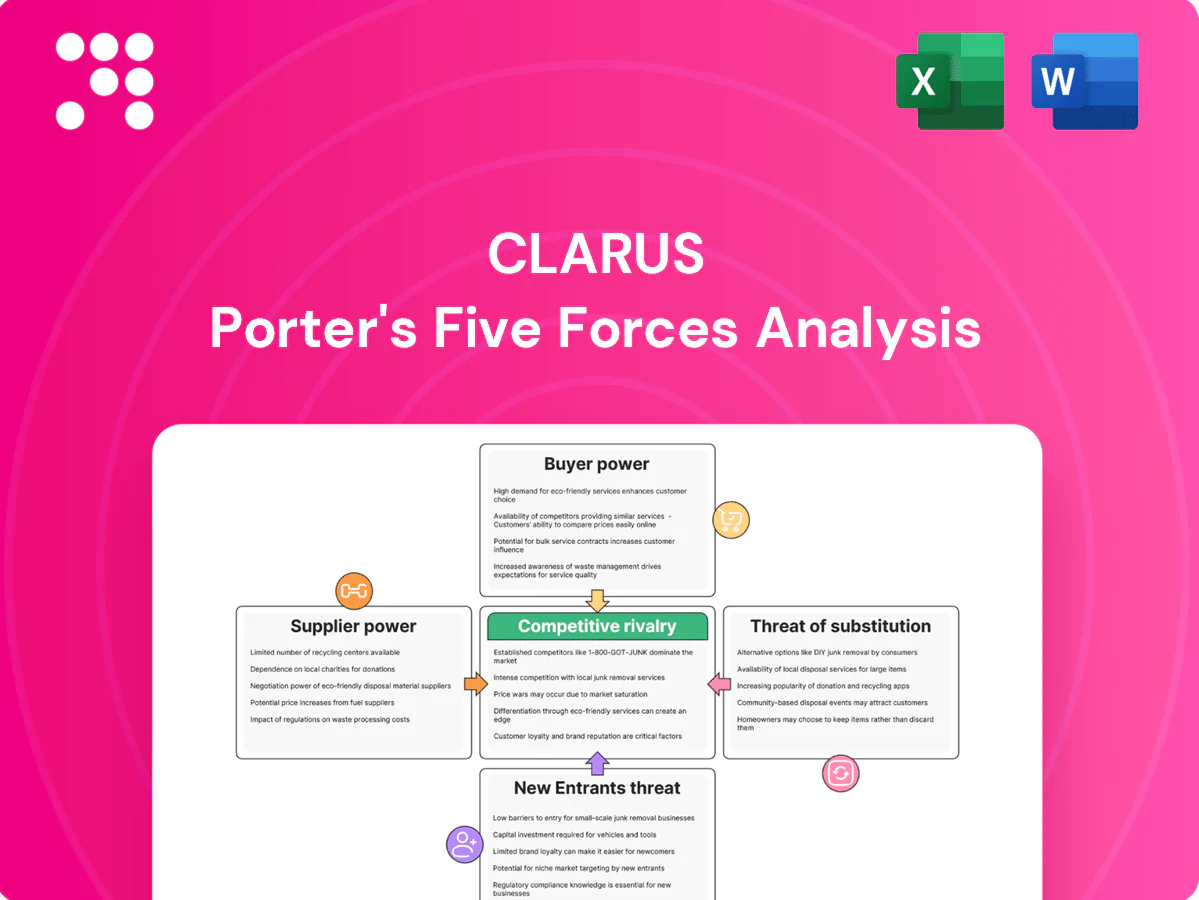

Clarus’s Porter’s Five Forces Analysis highlights competitive intensity, supplier and buyer power, threats from substitutes and new entrants, and the degree of industry rivalry. This snapshot surfaces the principal pressure points and strategic levers affecting Clarus’s market position. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Clarus’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialty raw materials concentration

Clarus relies on high-spec aluminum, carbon composites, performance textiles and precision electronics for safety-critical gear, many of which must meet UIAA and CE certification; qualified suppliers are concentrated, raising supplier leverage and switching costs. Limited alternates inflate price and delivery risk; long-term contracts and dual-sourcing reduce exposure, though qualification timelines commonly run 9–18 months.

Quality and certification requirements

Black Diamond and Pieps products mandate CE and UIAA certifications and full traceability; suppliers able to document process control and independent testing command pricing power. Any material lapse risks product recalls and reputational damage, eroding buyer leverage. Regular supplier audits and co-engineering arrangements create technical lock-in and multi-year dependency.

Geographic and logistics exposure

Global sourcing from Asia-Pacific and Europe exposes Clarus to freight volatility and geopolitical risk; Suez Canal disruptions can affect roughly 12% of seaborne trade, amplifying supplier leverage.

Tight logistics and scarce carrier capacity shift bargaining power to suppliers holding priority slots; nearshoring offers mitigation but needs multi-year timelines and significant capex.

Maintaining inventory buffers reduces acute supplier leverage but increases carrying costs and working capital demands.

Tooling and co-development lock-in

Proprietary molds, dies and firmware co-developed with suppliers create high switching costs and impede rapid vendor changes; tooling and firmware NRE commonly reach six-figure levels, effectively tying production to specific partners. Those NRE-backed dependencies give suppliers leverage during contract renewals, often enabling price premia, longer lead times and stricter terms. Standardizing components and moving to modular designs reduces lock-in and restores negotiating power.

- Proprietary tooling = high switching cost

- NRE often six-figure+ ties production to partners

- Supplier leverage rises at renewal

- Standardization reduces lock-in

Commodity vs. branded components mix

Concentrated certified suppliers raise costs: 9–18 month quals, six-figure NRE, ~45% chip margins

Suppliers concentrated for certified, safety-critical inputs, raising pricing and switching costs; qualification timelines typically 9–18 months and proprietary NRE often six-figure. Semiconductor and niche module pricing power persists (global semi gross margin ~45% in 2024; MOQs commonly mid-thousands). Freight/geopolitical exposure (Suez ~12% seaborne trade) and scarce carrier capacity further shift leverage to suppliers.

| Supplier Risk | Metric | Value |

|---|---|---|

| Qualification time | Months | 9–18 |

| NRE | USD | Six-figure+ |

| Semiconductor margin (2024) | % | ~45 |

| Suez trade exposure | % seaborne | ~12 |

What is included in the product

Tailored Porter's Five Forces analysis for Clarus that uncovers competitive pressures, supplier and buyer power, threat of substitutes and new entrants, and highlights disruptive trends and strategic levers to protect margins and inform investor or management decision-making.

A single-sheet Clarus Porter’s Five Forces summary that quantifies competitive pressure, creates instant spider/radar visuals, and lets you toggle scenarios—so teams make fast, data-driven strategic decisions without spreadsheet complexity.

Customers Bargaining Power

Channel concentration in specialty retail

Large specialty retailers and distributors (outdoor chains and national sporting goods) aggregate outsized volume, giving them leverage to demand lower prices, extended payment terms, and preferential shelf placement. Losing a major retail account can create material revenue volatility for a supplier like Clarus. Diversifying by region and channel, including direct-to-consumer and international partners, reduces customer concentration risk.

Direct-to-consumer balance

Clarus’s DTC strategy reduces intermediary power and captures retail margin by selling direct to consumers, aligning with a 2024 U.S. trend where e-commerce accounted for roughly 19% of retail sales (U.S. Census Bureau).

However, DTC raises customer expectations for service, fast shipping, and lenient returns, trends reflected in 2024 surveys showing fulfillment and returns as top drivers of online purchase satisfaction.

Price transparency online increases buyer bargaining power, but targeted loyalty programs and personalized offers have proven in 2024 to improve retention and reduce pure price sensitivity among repeat buyers.

Product differentiation and brand loyalty

In climbing and avalanche safety, strong brand trust — driven by proven performance, safety records, and community credibility — materially reduces buyer power as customers prioritize reliability over price; for non-safety items like racks and lifestyle accessories, easier cross-shopping increases buyer leverage, but continuous 2024-era innovation in materials and features sustains willingness to pay among core users.

Price sensitivity and macro cycles

Discretionary outdoor spend shifts with macro cycles: in downturns buyers demand promotions and trade down, raising customer leverage; retailers reported heavier markdown cadence in 2024 as consumers tightened wallets. Seasonality amplifies post-peak discounting, while essential safety SKUs—helmets, harnesses—maintained firmer pricing versus lifestyle items in 2024.

- 2024: elevated markdown cadence; stronger pricing resilience for safety SKUs

- Downturns: higher promotion share and trade-down behavior

- Seasonality: post-peak discount pressure

Information symmetry and reviews

Online reviews, forums, and independent test results arm buyers with data; by 2024 over 70% of purchasers consult reviews before buying, intensifying price and feature bargaining on like-for-like products. Transparent comparisons reward top-performing designs and penalize gaps, while rapid feedback loops—reviews appearing within days—force quicker markdown and warranty decisions.

- Information symmetry: accelerates price sensitivity

- Comparability: amplifies competition on specs/failures

- Transparency: ties sales to measurable performance

- Feedback speed: compresses repricing cycles

DTC, reviews and e-commerce (~19%) shift pricing power from large retailers

Large specialty retailers retain bargaining leverage via volume and shelf placement, creating concentration risk for Clarus; DTC reduces intermediary power and captured margin (U.S. e-commerce ~19% of retail sales in 2024). Online price transparency and reviews (>70% consult reviews before buying in 2024) raise buyer power, though safety SKUs show firmer pricing and loyalty reduces pure price sensitivity.

| Metric | 2024 datapoint |

|---|---|

| E-commerce share | ~19% |

| Review consult rate | >70% |

| Retail markdowns | Elevated cadence |

| Safety SKU pricing | More resilient |

Preview the Actual Deliverable

Clarus Porter's Five Forces Analysis

This preview shows the exact Clarus Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The report delivers a concise industry overview, competitive intensity scoring, and strategic implications across bargaining power, rivalry, entry barriers, substitutes and supplier dynamics. It's fully formatted and ready for immediate use.

A Must-Have Tool for Decision-Makers

Clarus’s Porter’s Five Forces Analysis highlights competitive intensity, supplier and buyer power, threats from substitutes and new entrants, and the degree of industry rivalry. This snapshot surfaces the principal pressure points and strategic levers affecting Clarus’s market position. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Clarus’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialty raw materials concentration

Clarus relies on high-spec aluminum, carbon composites, performance textiles and precision electronics for safety-critical gear, many of which must meet UIAA and CE certification; qualified suppliers are concentrated, raising supplier leverage and switching costs. Limited alternates inflate price and delivery risk; long-term contracts and dual-sourcing reduce exposure, though qualification timelines commonly run 9–18 months.

Quality and certification requirements

Black Diamond and Pieps products mandate CE and UIAA certifications and full traceability; suppliers able to document process control and independent testing command pricing power. Any material lapse risks product recalls and reputational damage, eroding buyer leverage. Regular supplier audits and co-engineering arrangements create technical lock-in and multi-year dependency.

Geographic and logistics exposure

Global sourcing from Asia-Pacific and Europe exposes Clarus to freight volatility and geopolitical risk; Suez Canal disruptions can affect roughly 12% of seaborne trade, amplifying supplier leverage.

Tight logistics and scarce carrier capacity shift bargaining power to suppliers holding priority slots; nearshoring offers mitigation but needs multi-year timelines and significant capex.

Maintaining inventory buffers reduces acute supplier leverage but increases carrying costs and working capital demands.

Tooling and co-development lock-in

Proprietary molds, dies and firmware co-developed with suppliers create high switching costs and impede rapid vendor changes; tooling and firmware NRE commonly reach six-figure levels, effectively tying production to specific partners. Those NRE-backed dependencies give suppliers leverage during contract renewals, often enabling price premia, longer lead times and stricter terms. Standardizing components and moving to modular designs reduces lock-in and restores negotiating power.

- Proprietary tooling = high switching cost

- NRE often six-figure+ ties production to partners

- Supplier leverage rises at renewal

- Standardization reduces lock-in

Commodity vs. branded components mix

Concentrated certified suppliers raise costs: 9–18 month quals, six-figure NRE, ~45% chip margins

Suppliers concentrated for certified, safety-critical inputs, raising pricing and switching costs; qualification timelines typically 9–18 months and proprietary NRE often six-figure. Semiconductor and niche module pricing power persists (global semi gross margin ~45% in 2024; MOQs commonly mid-thousands). Freight/geopolitical exposure (Suez ~12% seaborne trade) and scarce carrier capacity further shift leverage to suppliers.

| Supplier Risk | Metric | Value |

|---|---|---|

| Qualification time | Months | 9–18 |

| NRE | USD | Six-figure+ |

| Semiconductor margin (2024) | % | ~45 |

| Suez trade exposure | % seaborne | ~12 |

What is included in the product

Tailored Porter's Five Forces analysis for Clarus that uncovers competitive pressures, supplier and buyer power, threat of substitutes and new entrants, and highlights disruptive trends and strategic levers to protect margins and inform investor or management decision-making.

A single-sheet Clarus Porter’s Five Forces summary that quantifies competitive pressure, creates instant spider/radar visuals, and lets you toggle scenarios—so teams make fast, data-driven strategic decisions without spreadsheet complexity.

Customers Bargaining Power

Channel concentration in specialty retail

Large specialty retailers and distributors (outdoor chains and national sporting goods) aggregate outsized volume, giving them leverage to demand lower prices, extended payment terms, and preferential shelf placement. Losing a major retail account can create material revenue volatility for a supplier like Clarus. Diversifying by region and channel, including direct-to-consumer and international partners, reduces customer concentration risk.

Direct-to-consumer balance

Clarus’s DTC strategy reduces intermediary power and captures retail margin by selling direct to consumers, aligning with a 2024 U.S. trend where e-commerce accounted for roughly 19% of retail sales (U.S. Census Bureau).

However, DTC raises customer expectations for service, fast shipping, and lenient returns, trends reflected in 2024 surveys showing fulfillment and returns as top drivers of online purchase satisfaction.

Price transparency online increases buyer bargaining power, but targeted loyalty programs and personalized offers have proven in 2024 to improve retention and reduce pure price sensitivity among repeat buyers.

Product differentiation and brand loyalty

In climbing and avalanche safety, strong brand trust — driven by proven performance, safety records, and community credibility — materially reduces buyer power as customers prioritize reliability over price; for non-safety items like racks and lifestyle accessories, easier cross-shopping increases buyer leverage, but continuous 2024-era innovation in materials and features sustains willingness to pay among core users.

Price sensitivity and macro cycles

Discretionary outdoor spend shifts with macro cycles: in downturns buyers demand promotions and trade down, raising customer leverage; retailers reported heavier markdown cadence in 2024 as consumers tightened wallets. Seasonality amplifies post-peak discounting, while essential safety SKUs—helmets, harnesses—maintained firmer pricing versus lifestyle items in 2024.

- 2024: elevated markdown cadence; stronger pricing resilience for safety SKUs

- Downturns: higher promotion share and trade-down behavior

- Seasonality: post-peak discount pressure

Information symmetry and reviews

Online reviews, forums, and independent test results arm buyers with data; by 2024 over 70% of purchasers consult reviews before buying, intensifying price and feature bargaining on like-for-like products. Transparent comparisons reward top-performing designs and penalize gaps, while rapid feedback loops—reviews appearing within days—force quicker markdown and warranty decisions.

- Information symmetry: accelerates price sensitivity

- Comparability: amplifies competition on specs/failures

- Transparency: ties sales to measurable performance

- Feedback speed: compresses repricing cycles

DTC, reviews and e-commerce (~19%) shift pricing power from large retailers

Large specialty retailers retain bargaining leverage via volume and shelf placement, creating concentration risk for Clarus; DTC reduces intermediary power and captured margin (U.S. e-commerce ~19% of retail sales in 2024). Online price transparency and reviews (>70% consult reviews before buying in 2024) raise buyer power, though safety SKUs show firmer pricing and loyalty reduces pure price sensitivity.

| Metric | 2024 datapoint |

|---|---|

| E-commerce share | ~19% |

| Review consult rate | >70% |

| Retail markdowns | Elevated cadence |

| Safety SKU pricing | More resilient |

Preview the Actual Deliverable

Clarus Porter's Five Forces Analysis

This preview shows the exact Clarus Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The report delivers a concise industry overview, competitive intensity scoring, and strategic implications across bargaining power, rivalry, entry barriers, substitutes and supplier dynamics. It's fully formatted and ready for immediate use.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Clarus’s Porter’s Five Forces Analysis highlights competitive intensity, supplier and buyer power, threats from substitutes and new entrants, and the degree of industry rivalry. This snapshot surfaces the principal pressure points and strategic levers affecting Clarus’s market position. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Clarus’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialty raw materials concentration

Clarus relies on high-spec aluminum, carbon composites, performance textiles and precision electronics for safety-critical gear, many of which must meet UIAA and CE certification; qualified suppliers are concentrated, raising supplier leverage and switching costs. Limited alternates inflate price and delivery risk; long-term contracts and dual-sourcing reduce exposure, though qualification timelines commonly run 9–18 months.

Quality and certification requirements

Black Diamond and Pieps products mandate CE and UIAA certifications and full traceability; suppliers able to document process control and independent testing command pricing power. Any material lapse risks product recalls and reputational damage, eroding buyer leverage. Regular supplier audits and co-engineering arrangements create technical lock-in and multi-year dependency.

Geographic and logistics exposure

Global sourcing from Asia-Pacific and Europe exposes Clarus to freight volatility and geopolitical risk; Suez Canal disruptions can affect roughly 12% of seaborne trade, amplifying supplier leverage.

Tight logistics and scarce carrier capacity shift bargaining power to suppliers holding priority slots; nearshoring offers mitigation but needs multi-year timelines and significant capex.

Maintaining inventory buffers reduces acute supplier leverage but increases carrying costs and working capital demands.

Tooling and co-development lock-in

Proprietary molds, dies and firmware co-developed with suppliers create high switching costs and impede rapid vendor changes; tooling and firmware NRE commonly reach six-figure levels, effectively tying production to specific partners. Those NRE-backed dependencies give suppliers leverage during contract renewals, often enabling price premia, longer lead times and stricter terms. Standardizing components and moving to modular designs reduces lock-in and restores negotiating power.

- Proprietary tooling = high switching cost

- NRE often six-figure+ ties production to partners

- Supplier leverage rises at renewal

- Standardization reduces lock-in

Commodity vs. branded components mix

Concentrated certified suppliers raise costs: 9–18 month quals, six-figure NRE, ~45% chip margins

Suppliers concentrated for certified, safety-critical inputs, raising pricing and switching costs; qualification timelines typically 9–18 months and proprietary NRE often six-figure. Semiconductor and niche module pricing power persists (global semi gross margin ~45% in 2024; MOQs commonly mid-thousands). Freight/geopolitical exposure (Suez ~12% seaborne trade) and scarce carrier capacity further shift leverage to suppliers.

| Supplier Risk | Metric | Value |

|---|---|---|

| Qualification time | Months | 9–18 |

| NRE | USD | Six-figure+ |

| Semiconductor margin (2024) | % | ~45 |

| Suez trade exposure | % seaborne | ~12 |

What is included in the product

Tailored Porter's Five Forces analysis for Clarus that uncovers competitive pressures, supplier and buyer power, threat of substitutes and new entrants, and highlights disruptive trends and strategic levers to protect margins and inform investor or management decision-making.

A single-sheet Clarus Porter’s Five Forces summary that quantifies competitive pressure, creates instant spider/radar visuals, and lets you toggle scenarios—so teams make fast, data-driven strategic decisions without spreadsheet complexity.

Customers Bargaining Power

Channel concentration in specialty retail

Large specialty retailers and distributors (outdoor chains and national sporting goods) aggregate outsized volume, giving them leverage to demand lower prices, extended payment terms, and preferential shelf placement. Losing a major retail account can create material revenue volatility for a supplier like Clarus. Diversifying by region and channel, including direct-to-consumer and international partners, reduces customer concentration risk.

Direct-to-consumer balance

Clarus’s DTC strategy reduces intermediary power and captures retail margin by selling direct to consumers, aligning with a 2024 U.S. trend where e-commerce accounted for roughly 19% of retail sales (U.S. Census Bureau).

However, DTC raises customer expectations for service, fast shipping, and lenient returns, trends reflected in 2024 surveys showing fulfillment and returns as top drivers of online purchase satisfaction.

Price transparency online increases buyer bargaining power, but targeted loyalty programs and personalized offers have proven in 2024 to improve retention and reduce pure price sensitivity among repeat buyers.

Product differentiation and brand loyalty

In climbing and avalanche safety, strong brand trust — driven by proven performance, safety records, and community credibility — materially reduces buyer power as customers prioritize reliability over price; for non-safety items like racks and lifestyle accessories, easier cross-shopping increases buyer leverage, but continuous 2024-era innovation in materials and features sustains willingness to pay among core users.

Price sensitivity and macro cycles

Discretionary outdoor spend shifts with macro cycles: in downturns buyers demand promotions and trade down, raising customer leverage; retailers reported heavier markdown cadence in 2024 as consumers tightened wallets. Seasonality amplifies post-peak discounting, while essential safety SKUs—helmets, harnesses—maintained firmer pricing versus lifestyle items in 2024.

- 2024: elevated markdown cadence; stronger pricing resilience for safety SKUs

- Downturns: higher promotion share and trade-down behavior

- Seasonality: post-peak discount pressure

Information symmetry and reviews

Online reviews, forums, and independent test results arm buyers with data; by 2024 over 70% of purchasers consult reviews before buying, intensifying price and feature bargaining on like-for-like products. Transparent comparisons reward top-performing designs and penalize gaps, while rapid feedback loops—reviews appearing within days—force quicker markdown and warranty decisions.

- Information symmetry: accelerates price sensitivity

- Comparability: amplifies competition on specs/failures

- Transparency: ties sales to measurable performance

- Feedback speed: compresses repricing cycles

DTC, reviews and e-commerce (~19%) shift pricing power from large retailers

Large specialty retailers retain bargaining leverage via volume and shelf placement, creating concentration risk for Clarus; DTC reduces intermediary power and captured margin (U.S. e-commerce ~19% of retail sales in 2024). Online price transparency and reviews (>70% consult reviews before buying in 2024) raise buyer power, though safety SKUs show firmer pricing and loyalty reduces pure price sensitivity.

| Metric | 2024 datapoint |

|---|---|

| E-commerce share | ~19% |

| Review consult rate | >70% |

| Retail markdowns | Elevated cadence |

| Safety SKU pricing | More resilient |

Preview the Actual Deliverable

Clarus Porter's Five Forces Analysis

This preview shows the exact Clarus Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The report delivers a concise industry overview, competitive intensity scoring, and strategic implications across bargaining power, rivalry, entry barriers, substitutes and supplier dynamics. It's fully formatted and ready for immediate use.