Clarus SWOT Analysis

Make Insightful Decisions Backed by Expert Research

Discover how Clarus stacks up across market strengths, competitive threats, and growth levers with our concise SWOT snapshot—then unlock the full analysis for strategic depth. Purchase the complete report to receive a research-backed, editable Word and Excel package. Ideal for investors, advisors, and managers who need actionable, presentation-ready insights.

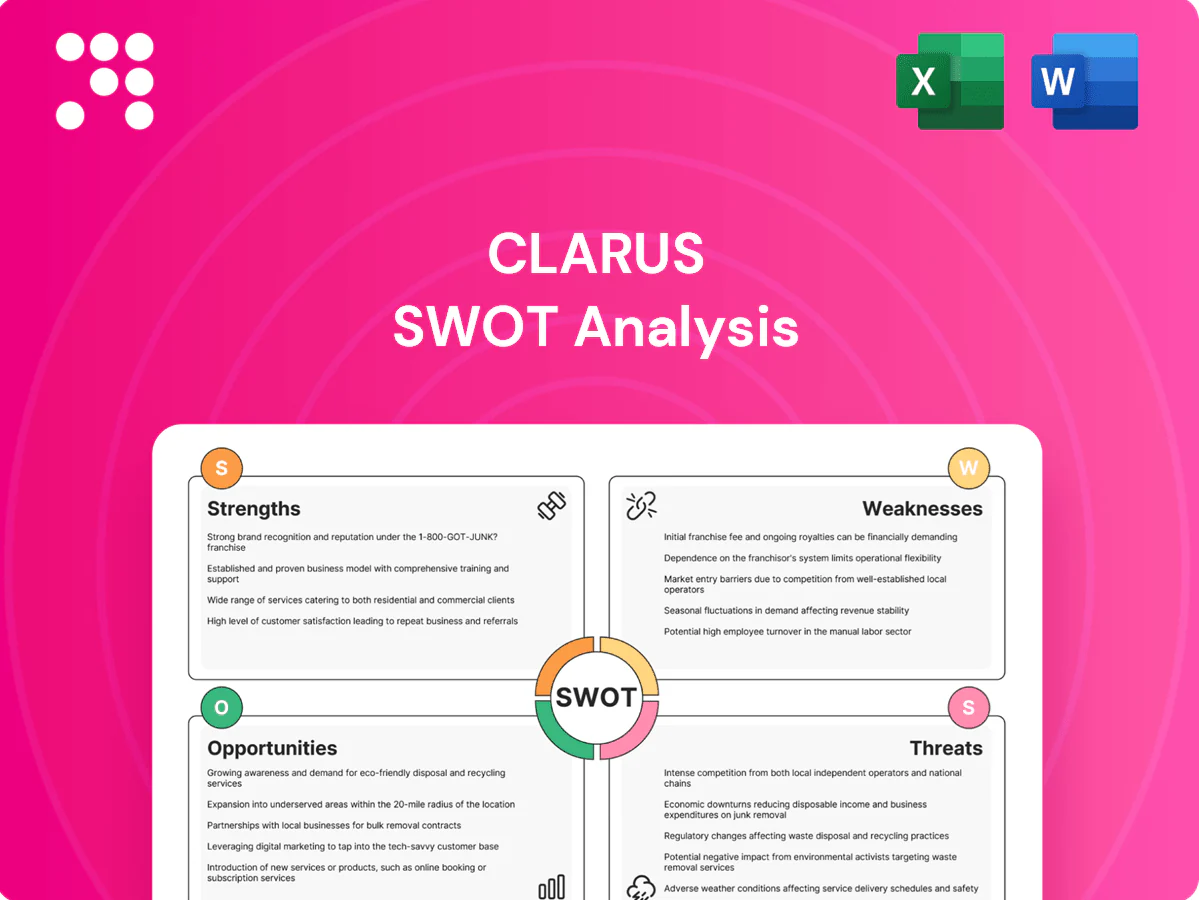

Strengths

Trusted premium brands

Clarus' portfolio of four premium brands — Black Diamond, Pieps, Sierra and Rhino-Rack — carries strong equity and recognition across core outdoor segments. These brands are widely respected for reliability, safety and performance by enthusiasts and professionals, underpinning pricing power and high repeat purchase rates. Black Diamond is a recognized leader in climbing hardgoods and Pieps is a category leader in avalanche safety, reinforcing channel and margin strength.

Innovation and technical expertise

Consistent R&D in safety gear, hardgoods and rack systems drives products designed for rigorous use cases, supported by deep engineering teams and continuous athlete feedback loops that accelerate iterative improvements and shorten time-to-upgrade. This innovation creates clear differentiation, limits commoditization, and is validated through IP filings and compliance with industry certifications such as CE, ISO and relevant ASTM standards.

Diversified outdoor portfolio

Clarus spans climbing, skiing, hunting and vehicle-based adventure, balancing seasonal demand and enabling cross-selling between hardgoods and accessories (e.g., packs, lighting, and apparel), which raises average order value and customer lifetime value. Multiple end uses reduce reliance on any single sport trend, and diversified wholesale, DTC and international channels provide resilience across cycles and regions.

Omnichannel distribution reach

Clarus leverages omnichannel distribution across specialty retail, big-box, e-commerce and DTC, increasing product visibility and customer access in core outdoor and consumer markets. DTC sales provide rich first-party data that informs design cycles and inventory allocation, tightening sell-through. Strategic retail and distributor partnerships extend international shelf space and local market reach.

- Channels: specialty, big-box, e-commerce, DTC

- Data: DTC feedback drives design & inventory

- Scale: partnerships expand international presence

Strong community engagement

Clarus maintains authentic ties to core users through athletes, guides, and branded events, turning firsthand field feedback into rapid product refinements and vocal advocacy. Community input directly shapes product fit, driving retention in niche, mission-driven segments and reducing formal R&D cycles. User-generated content from ambassadors and customers provides sustained, low-cost marketing and credibility.

- authentic ambassador network

- community-driven product fit

- UGC as low-cost marketing

- high loyalty in niche segments

Four premium outdoor brands: certified gear, omnichannel reach and elite customer loyalty

Clarus' four premium brands deliver strong category equity across climbing, skiing, hunting and vehicle-based adventure. Omnichannel reach—specialty, big-box, e-commerce and DTC—supports visibility and first-party data. Robust R&D, CE/ISO/ASTM-aligned safety certifications and an active ambassador network drive product differentiation and high loyalty.

| Metric | Value |

|---|---|

| Brands | 4 |

| Core segments | Climbing, Skiing, Hunting, Vehicle-adventure |

| Channels | Specialty, Big-box, E-commerce, DTC |

| Certifications | CE, ISO, ASTM |

What is included in the product

Provides a strategic overview of Clarus’s internal strengths and weaknesses and external opportunities and threats, analyzing competitive position, growth drivers, operational gaps, and market risks to inform strategic decision-making.

Provides a ready-to-use visual SWOT matrix that accelerates strategic alignment, reduces time spent consolidating insights across teams, and simplifies stakeholder-ready reporting.

Weaknesses

Seasonality exposure

Clarus faces concentrated sales in winter sports and peak adventure seasons, with holiday/peak retail periods often representing roughly 20% of annual category sales (NRF). This seasonality complicates forecasting and raises inventory risk outside peak windows, increasing markdowns and potential write-downs. Cash flow swings track weather-dependent demand, and heavy discounting to clear seasonal stock can compress margins materially.

Supply chain complexity

Multi-material, safety-critical manufacturing at Clarus requires stringent QA and traceability across metal, polymer and textile supply lines, raising inspection and compliance steps. This complexity makes Clarus vulnerable to component delays and rising logistics costs, which pressured operations during 2023–24 when global freight rates and port congestion spiked. Coordinating across multiple brands and geographies strains planning and increases variability in lead times. Higher inventory and longer receivable cycles have elevated working capital needs, reflected in year-end 2024 net sales of $341.5 million.

Niche scale versus giants

Narrow specialty focus leaves Clarus outspent by broader lifestyle giants on marketing, weakening brand visibility and customer reach. Retailers and suppliers favor scale, reducing Claruss bargaining power on shelf space and input costs. Global rollout of new lines is constrained by limited distribution networks and capital. Technical SKUs incur higher per-unit production costs versus mass-market items.

Integration and portfolio focus

Execution risk arises from managing distinct brand identities and strategies, raising the chance of inconsistent market positioning and diluted marketing ROI; resources can be stretched across categories, constraining innovation and margin improvement. Aligning IT, ERP and demand planning across brands increases operational complexity and error risk, while M&A or divestiture activity can distract management and disrupt integration timelines.

- brand-fragmentation

- resource-dilution

- IT/ERP-complexity

- M&A-distraction

Margin sensitivity

Margin sensitivity: Clarus faces exposure to raw-material, freight and currency swings; global container rates fell roughly 70% from 2022 peaks to 2024 but raw-material volatility persists, pressuring input costs. Technical safety products require rigorous testing and certification, raising per-SKU OPEX. Promotional pressure in competitive channels and adverse mix shifts toward lower-margin SKUs compress gross margins.

- raw-material/freight/currency risk

- high testing/certification costs

- promotional channel pressure

- mix shift to low-margin SKUs

Seasonal, safety-critical production drives inventory and cash-flow swings; holiday ≈ 20%

Clarus is highly seasonal — holiday/peak periods drive ~20% of annual category sales, creating inventory, cash‑flow swings and markdown risk; 2024 net sales were $341.5M. Multi‑material, safety‑critical manufacturing increases QA, lead‑time variability and working‑capital needs. Limited marketing scale and distribution vs. lifestyle peers and raw‑material/freight volatility (container rates down ~70% 2022–24) compress margins.

| Weakness | Metric | 2024 |

|---|---|---|

| Seasonality | Holiday share | ~20% |

| Scale | Net sales | $341.5M |

| Freight volatility | Container rate change | -70% vs 2022 |

What You See Is What You Get

Clarus SWOT Analysis

This is the actual Clarus SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the complete structure, findings, and recommendations. Purchase unlocks the editable, full-resolution version ready for download and use.

Make Insightful Decisions Backed by Expert Research

Discover how Clarus stacks up across market strengths, competitive threats, and growth levers with our concise SWOT snapshot—then unlock the full analysis for strategic depth. Purchase the complete report to receive a research-backed, editable Word and Excel package. Ideal for investors, advisors, and managers who need actionable, presentation-ready insights.

Strengths

Trusted premium brands

Clarus' portfolio of four premium brands — Black Diamond, Pieps, Sierra and Rhino-Rack — carries strong equity and recognition across core outdoor segments. These brands are widely respected for reliability, safety and performance by enthusiasts and professionals, underpinning pricing power and high repeat purchase rates. Black Diamond is a recognized leader in climbing hardgoods and Pieps is a category leader in avalanche safety, reinforcing channel and margin strength.

Innovation and technical expertise

Consistent R&D in safety gear, hardgoods and rack systems drives products designed for rigorous use cases, supported by deep engineering teams and continuous athlete feedback loops that accelerate iterative improvements and shorten time-to-upgrade. This innovation creates clear differentiation, limits commoditization, and is validated through IP filings and compliance with industry certifications such as CE, ISO and relevant ASTM standards.

Diversified outdoor portfolio

Clarus spans climbing, skiing, hunting and vehicle-based adventure, balancing seasonal demand and enabling cross-selling between hardgoods and accessories (e.g., packs, lighting, and apparel), which raises average order value and customer lifetime value. Multiple end uses reduce reliance on any single sport trend, and diversified wholesale, DTC and international channels provide resilience across cycles and regions.

Omnichannel distribution reach

Clarus leverages omnichannel distribution across specialty retail, big-box, e-commerce and DTC, increasing product visibility and customer access in core outdoor and consumer markets. DTC sales provide rich first-party data that informs design cycles and inventory allocation, tightening sell-through. Strategic retail and distributor partnerships extend international shelf space and local market reach.

- Channels: specialty, big-box, e-commerce, DTC

- Data: DTC feedback drives design & inventory

- Scale: partnerships expand international presence

Strong community engagement

Clarus maintains authentic ties to core users through athletes, guides, and branded events, turning firsthand field feedback into rapid product refinements and vocal advocacy. Community input directly shapes product fit, driving retention in niche, mission-driven segments and reducing formal R&D cycles. User-generated content from ambassadors and customers provides sustained, low-cost marketing and credibility.

- authentic ambassador network

- community-driven product fit

- UGC as low-cost marketing

- high loyalty in niche segments

Four premium outdoor brands: certified gear, omnichannel reach and elite customer loyalty

Clarus' four premium brands deliver strong category equity across climbing, skiing, hunting and vehicle-based adventure. Omnichannel reach—specialty, big-box, e-commerce and DTC—supports visibility and first-party data. Robust R&D, CE/ISO/ASTM-aligned safety certifications and an active ambassador network drive product differentiation and high loyalty.

| Metric | Value |

|---|---|

| Brands | 4 |

| Core segments | Climbing, Skiing, Hunting, Vehicle-adventure |

| Channels | Specialty, Big-box, E-commerce, DTC |

| Certifications | CE, ISO, ASTM |

What is included in the product

Provides a strategic overview of Clarus’s internal strengths and weaknesses and external opportunities and threats, analyzing competitive position, growth drivers, operational gaps, and market risks to inform strategic decision-making.

Provides a ready-to-use visual SWOT matrix that accelerates strategic alignment, reduces time spent consolidating insights across teams, and simplifies stakeholder-ready reporting.

Weaknesses

Seasonality exposure

Clarus faces concentrated sales in winter sports and peak adventure seasons, with holiday/peak retail periods often representing roughly 20% of annual category sales (NRF). This seasonality complicates forecasting and raises inventory risk outside peak windows, increasing markdowns and potential write-downs. Cash flow swings track weather-dependent demand, and heavy discounting to clear seasonal stock can compress margins materially.

Supply chain complexity

Multi-material, safety-critical manufacturing at Clarus requires stringent QA and traceability across metal, polymer and textile supply lines, raising inspection and compliance steps. This complexity makes Clarus vulnerable to component delays and rising logistics costs, which pressured operations during 2023–24 when global freight rates and port congestion spiked. Coordinating across multiple brands and geographies strains planning and increases variability in lead times. Higher inventory and longer receivable cycles have elevated working capital needs, reflected in year-end 2024 net sales of $341.5 million.

Niche scale versus giants

Narrow specialty focus leaves Clarus outspent by broader lifestyle giants on marketing, weakening brand visibility and customer reach. Retailers and suppliers favor scale, reducing Claruss bargaining power on shelf space and input costs. Global rollout of new lines is constrained by limited distribution networks and capital. Technical SKUs incur higher per-unit production costs versus mass-market items.

Integration and portfolio focus

Execution risk arises from managing distinct brand identities and strategies, raising the chance of inconsistent market positioning and diluted marketing ROI; resources can be stretched across categories, constraining innovation and margin improvement. Aligning IT, ERP and demand planning across brands increases operational complexity and error risk, while M&A or divestiture activity can distract management and disrupt integration timelines.

- brand-fragmentation

- resource-dilution

- IT/ERP-complexity

- M&A-distraction

Margin sensitivity

Margin sensitivity: Clarus faces exposure to raw-material, freight and currency swings; global container rates fell roughly 70% from 2022 peaks to 2024 but raw-material volatility persists, pressuring input costs. Technical safety products require rigorous testing and certification, raising per-SKU OPEX. Promotional pressure in competitive channels and adverse mix shifts toward lower-margin SKUs compress gross margins.

- raw-material/freight/currency risk

- high testing/certification costs

- promotional channel pressure

- mix shift to low-margin SKUs

Seasonal, safety-critical production drives inventory and cash-flow swings; holiday ≈ 20%

Clarus is highly seasonal — holiday/peak periods drive ~20% of annual category sales, creating inventory, cash‑flow swings and markdown risk; 2024 net sales were $341.5M. Multi‑material, safety‑critical manufacturing increases QA, lead‑time variability and working‑capital needs. Limited marketing scale and distribution vs. lifestyle peers and raw‑material/freight volatility (container rates down ~70% 2022–24) compress margins.

| Weakness | Metric | 2024 |

|---|---|---|

| Seasonality | Holiday share | ~20% |

| Scale | Net sales | $341.5M |

| Freight volatility | Container rate change | -70% vs 2022 |

What You See Is What You Get

Clarus SWOT Analysis

This is the actual Clarus SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the complete structure, findings, and recommendations. Purchase unlocks the editable, full-resolution version ready for download and use.

Description

Make Insightful Decisions Backed by Expert Research

Discover how Clarus stacks up across market strengths, competitive threats, and growth levers with our concise SWOT snapshot—then unlock the full analysis for strategic depth. Purchase the complete report to receive a research-backed, editable Word and Excel package. Ideal for investors, advisors, and managers who need actionable, presentation-ready insights.

Strengths

Trusted premium brands

Clarus' portfolio of four premium brands — Black Diamond, Pieps, Sierra and Rhino-Rack — carries strong equity and recognition across core outdoor segments. These brands are widely respected for reliability, safety and performance by enthusiasts and professionals, underpinning pricing power and high repeat purchase rates. Black Diamond is a recognized leader in climbing hardgoods and Pieps is a category leader in avalanche safety, reinforcing channel and margin strength.

Innovation and technical expertise

Consistent R&D in safety gear, hardgoods and rack systems drives products designed for rigorous use cases, supported by deep engineering teams and continuous athlete feedback loops that accelerate iterative improvements and shorten time-to-upgrade. This innovation creates clear differentiation, limits commoditization, and is validated through IP filings and compliance with industry certifications such as CE, ISO and relevant ASTM standards.

Diversified outdoor portfolio

Clarus spans climbing, skiing, hunting and vehicle-based adventure, balancing seasonal demand and enabling cross-selling between hardgoods and accessories (e.g., packs, lighting, and apparel), which raises average order value and customer lifetime value. Multiple end uses reduce reliance on any single sport trend, and diversified wholesale, DTC and international channels provide resilience across cycles and regions.

Omnichannel distribution reach

Clarus leverages omnichannel distribution across specialty retail, big-box, e-commerce and DTC, increasing product visibility and customer access in core outdoor and consumer markets. DTC sales provide rich first-party data that informs design cycles and inventory allocation, tightening sell-through. Strategic retail and distributor partnerships extend international shelf space and local market reach.

- Channels: specialty, big-box, e-commerce, DTC

- Data: DTC feedback drives design & inventory

- Scale: partnerships expand international presence

Strong community engagement

Clarus maintains authentic ties to core users through athletes, guides, and branded events, turning firsthand field feedback into rapid product refinements and vocal advocacy. Community input directly shapes product fit, driving retention in niche, mission-driven segments and reducing formal R&D cycles. User-generated content from ambassadors and customers provides sustained, low-cost marketing and credibility.

- authentic ambassador network

- community-driven product fit

- UGC as low-cost marketing

- high loyalty in niche segments

Four premium outdoor brands: certified gear, omnichannel reach and elite customer loyalty

Clarus' four premium brands deliver strong category equity across climbing, skiing, hunting and vehicle-based adventure. Omnichannel reach—specialty, big-box, e-commerce and DTC—supports visibility and first-party data. Robust R&D, CE/ISO/ASTM-aligned safety certifications and an active ambassador network drive product differentiation and high loyalty.

| Metric | Value |

|---|---|

| Brands | 4 |

| Core segments | Climbing, Skiing, Hunting, Vehicle-adventure |

| Channels | Specialty, Big-box, E-commerce, DTC |

| Certifications | CE, ISO, ASTM |

What is included in the product

Provides a strategic overview of Clarus’s internal strengths and weaknesses and external opportunities and threats, analyzing competitive position, growth drivers, operational gaps, and market risks to inform strategic decision-making.

Provides a ready-to-use visual SWOT matrix that accelerates strategic alignment, reduces time spent consolidating insights across teams, and simplifies stakeholder-ready reporting.

Weaknesses

Seasonality exposure

Clarus faces concentrated sales in winter sports and peak adventure seasons, with holiday/peak retail periods often representing roughly 20% of annual category sales (NRF). This seasonality complicates forecasting and raises inventory risk outside peak windows, increasing markdowns and potential write-downs. Cash flow swings track weather-dependent demand, and heavy discounting to clear seasonal stock can compress margins materially.

Supply chain complexity

Multi-material, safety-critical manufacturing at Clarus requires stringent QA and traceability across metal, polymer and textile supply lines, raising inspection and compliance steps. This complexity makes Clarus vulnerable to component delays and rising logistics costs, which pressured operations during 2023–24 when global freight rates and port congestion spiked. Coordinating across multiple brands and geographies strains planning and increases variability in lead times. Higher inventory and longer receivable cycles have elevated working capital needs, reflected in year-end 2024 net sales of $341.5 million.

Niche scale versus giants

Narrow specialty focus leaves Clarus outspent by broader lifestyle giants on marketing, weakening brand visibility and customer reach. Retailers and suppliers favor scale, reducing Claruss bargaining power on shelf space and input costs. Global rollout of new lines is constrained by limited distribution networks and capital. Technical SKUs incur higher per-unit production costs versus mass-market items.

Integration and portfolio focus

Execution risk arises from managing distinct brand identities and strategies, raising the chance of inconsistent market positioning and diluted marketing ROI; resources can be stretched across categories, constraining innovation and margin improvement. Aligning IT, ERP and demand planning across brands increases operational complexity and error risk, while M&A or divestiture activity can distract management and disrupt integration timelines.

- brand-fragmentation

- resource-dilution

- IT/ERP-complexity

- M&A-distraction

Margin sensitivity

Margin sensitivity: Clarus faces exposure to raw-material, freight and currency swings; global container rates fell roughly 70% from 2022 peaks to 2024 but raw-material volatility persists, pressuring input costs. Technical safety products require rigorous testing and certification, raising per-SKU OPEX. Promotional pressure in competitive channels and adverse mix shifts toward lower-margin SKUs compress gross margins.

- raw-material/freight/currency risk

- high testing/certification costs

- promotional channel pressure

- mix shift to low-margin SKUs

Seasonal, safety-critical production drives inventory and cash-flow swings; holiday ≈ 20%

Clarus is highly seasonal — holiday/peak periods drive ~20% of annual category sales, creating inventory, cash‑flow swings and markdown risk; 2024 net sales were $341.5M. Multi‑material, safety‑critical manufacturing increases QA, lead‑time variability and working‑capital needs. Limited marketing scale and distribution vs. lifestyle peers and raw‑material/freight volatility (container rates down ~70% 2022–24) compress margins.

| Weakness | Metric | 2024 |

|---|---|---|

| Seasonality | Holiday share | ~20% |

| Scale | Net sales | $341.5M |

| Freight volatility | Container rate change | -70% vs 2022 |

What You See Is What You Get

Clarus SWOT Analysis

This is the actual Clarus SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the complete structure, findings, and recommendations. Purchase unlocks the editable, full-resolution version ready for download and use.