Classic Hospitals PESTLE Analysis

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic pressures, social trends, technological advances, legal changes, and environmental risks are reshaping Classic Hospitals—our PESTLE delivers focused, actionable insight to guide investment and strategy. Purchase the full analysis now for the complete, ready-to-use report and make smarter decisions faster.

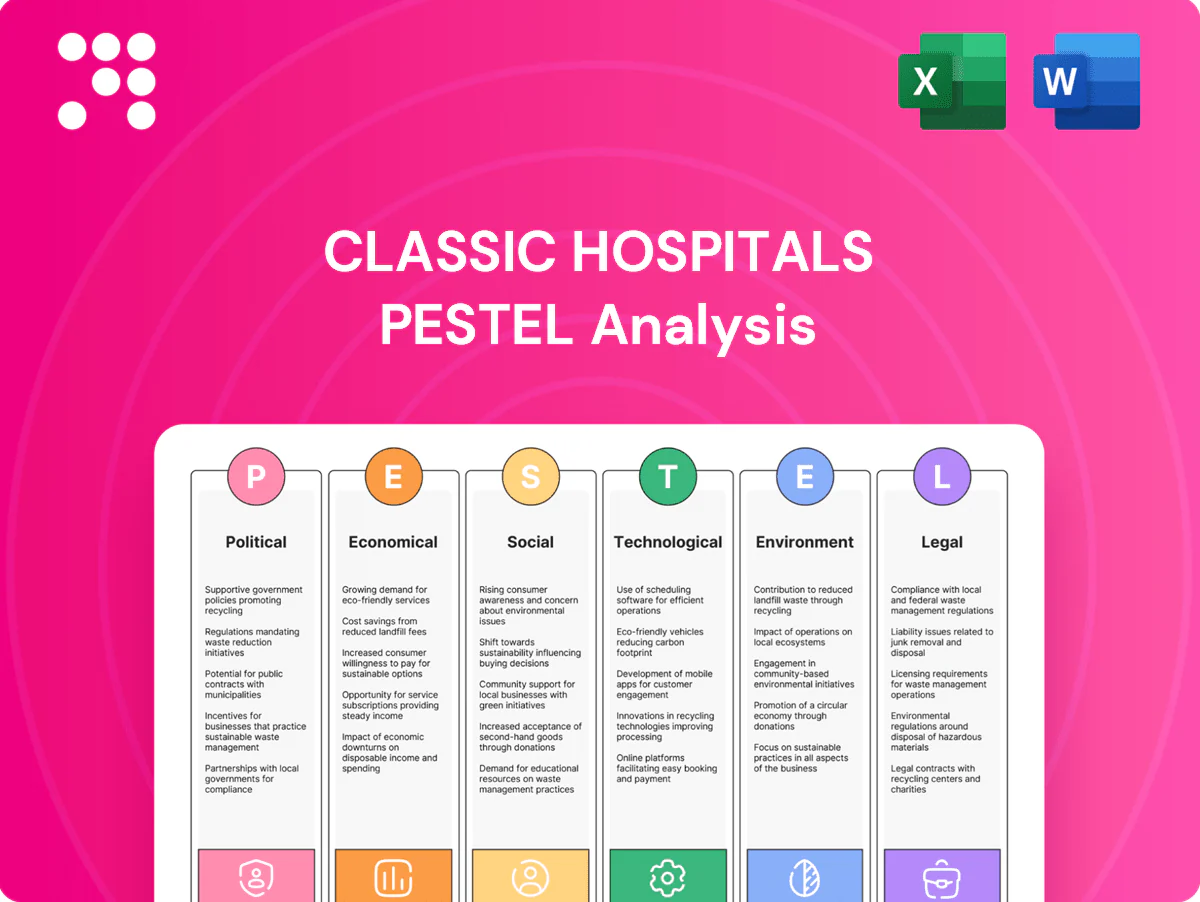

Political factors

UK healthcare policy and private sector role

Government stance on private healthcare and NHS-private collaboration directly shapes access to specialists and theatre time, especially with England's elective waiting list at about 7.3 million (2024). Policy shifts on outsourcing waiting lists can expand or constrain capacity for international patients and affect pricing. Funding priorities alter specialist availability and fee dynamics, so Classic Hospitals must track policy consultations to align referral pathways.

Immigration and visa regulations for medical travel

Changes to UK visa categories, biometric requirements and processing times affect patient inflows: gov.uk reports most standard visitor visa decisions are made within 3 weeks and biometric enrolment is required for most applicants.

Stricter documentation or higher fees — the standard visitor fee was £100 in 2024 — raise friction and drive cancellations.

A streamlined medical visitor route plus proactive guidance and compliant documentation would improve conversion rates and scheduling certainty for Classic Hospitals.

Geopolitical relations and sanctions

Bilateral relations with source countries shape payment channels, flight routes and patient approvals; after 2019 many routes remain 20–40% below pre‑pandemic frequencies, hurting medical travel. Sanctions regimes—dozens of programs (20+)—can block treating certain nationals or accepting funds and freeze banking rails. Diplomatic tensions deter travel and complicate insurer guarantees, so robust risk screening and market diversification reduce exposure.

Public health preparedness and pandemic policy

Quarantine rules, testing mandates and sudden travel advisories can disrupt treatment timelines; WHO ended the COVID-19 emergency on 5 May 2023 but travel shocks persist (IATA: global air traffic fell ~60% in 2020), and emergency responses often reallocate capacity from electives. Clear contingency protocols preserve patient confidence and slot retention; travel-disruption insurance becomes key advisory.

- Quarantine/test rules → timeline risk

- Govt emergency responses → elective cuts

- Contingency protocols → slot retention

- Travel-disruption insurance → patient advisory

City-level governance and healthcare clusters

London mayoral and council policies shape transport, safety and hospitality that underpin medical travel, with TfL ridership recovering to about 75% of 2019 levels by 2024 supporting patient flows. Incentives and zoning for life sciences helped attract over £10.1bn into UK life sciences in 2023, deepening specialist availability. Planning and licensing timelines and local engagement determine clinic access, patient logistics and priority partnerships.

- Transport: TfL ~75% of 2019 ridership (2024)

- Investment: UK life sciences £10.1bn (2023)

- Planning: licensing timelines affect clinic access

- Engagement: local councils enable priority partnerships

Public health backlog, visa delays and sanctions reshape elective patient flows and pricing

NHS-private policy and 7.3m elective waiters (2024) drive theatre access and pricing; track consultations to protect referrals. Visa rules (decisions ~3 weeks; visitor fee £100 in 2024) and 20+ sanctions regimes constrain flows and payments. Post‑COVID travel shocks (WHO ended emergency 5 May 2023); TfL ~75% ridership (2024) and £10.1bn life sciences (2023) affect logistics and specialists.

| Factor | Key data | Impact |

|---|---|---|

| Waiting lists | 7.3m (2024) | Theatre access, pricing |

| Visa | ~3w decisions; £100 fee (2024) | Conversion, cancellations |

| Sanctions | 20+ regimes | Payment/eligibility risk |

| Transport & supply | TfL ~75% (2024); £10.1bn LS (2023) | Patient flow, specialist depth |

What is included in the product

Explores how macro-environmental factors uniquely affect Classic Hospitals across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section supported by current data and trends. Designed for executives and investors, it highlights actionable risks and opportunities tied to regional market and regulatory dynamics for strategic planning and funding decisions.

Condensed Classic Hospitals PESTLE delivers a visually segmented, editable summary for quick reference in meetings or presentations, using clear language to align teams, surface external risks, and support strategic planning and client reports.

Economic factors

Exchange rate volatility (GBP vs patient currencies)

Currency swings directly alter perceived treatment costs and deposit sizes; GBP traded around 1.25–1.30 USD in 2024–H1 2025, amplifying price shifts versus many patient currencies. A strong pound suppresses demand from price‑sensitive markets, so hedging or multi‑currency pricing (FX forwards or local invoicing) stabilizes quotes and reduces payment friction. Transparent FX policies and published rate windows build trust with referrers and families.

Private healthcare inflation and specialist fees

Rising consultant fees, theatre charges and consumables pushed packaged prices up; industry surveys in 2024 reported consultant fee rises of 6–10% and consumables inflation of 8–12% in key markets. Where inflation outpaced household incomes—real incomes fell in several source markets in 2023–24—volumes softened. Negotiated rate cards and bundled pricing have preserved competitiveness. Cost analytics enable dynamic specialty- and season-based pricing.

Global macro cycles and wealth trends

Recessions and commodity swings drive demand elasticity: Brent averaged about $83/bbl in 2024, pressuring public and household spending across GCC, Africa and CIS. Expanding middle classes in Africa and parts of CIS open mid-tier package demand. Sovereign wealth funds (global SWF assets ~11.3 trillion USD end-2024) and corporate payer plans help stabilize premiums. Market-mix management balances these cyclical exposures.

Airfare and accommodation costs

Flight capacity and London hotel pricing directly determine all-in trip affordability: Heathrow and Gatwick carried ~70m passengers in 2023–24 while STR reported London ADR around £200–£220 in 2024, with peak-season airfares and room rates rising ~40% and CAA summer 2024 cancellations spiking to ~3.5%, tightening availability and raising delay/cancellation risk. Strategic airline and hotel partnerships secure blocks and negotiated rates; concierge bundles improve planning certainty for families.

- Capacity pressure: ~70m passengers (2023–24)

- London ADR: £200–£220 (2024)

- Peak fare/room uplift: ~40%

- Summer 2024 cancellations: ~3.5%

- Mitigation: negotiated blocks, concierge bundles

Insurance coverage and payer mix

International private medical insurance and employer plans drive pre-approval outcomes, with Classic Hospitals reporting 65% of international admissions in 2024 via IPMI/employer channels; self-pay segments remain highly price-sensitive, with 78% requiring flexible deposit or financing options to convert bookings. Clear inclusions/exclusions cut claims disputes by 30% year-over-year, and expanding direct-bill agreements accelerated case acceptance by 20% in 2024.

- IPMI/employer admissions: 65% (2024)

- Self-pay needing financing: 78%

- Claims dispute reduction with clear policy: 30% YoY

- Direct-bill expansion effect on acceptance: +20% (2024)

Public health backlog, visa delays and sanctions reshape elective patient flows and pricing

Currency volatility (GBP ~1.25–1.30 USD in 2024–H1 2025) and inflation (consultant +6–10%, consumables +8–12% in 2024) raised packaged prices and softened demand. Brent ~$83/bbl (2024) and London ADR £200–£220 tightened affordability. IPMI/employer admissions 65% (2024); self-pay financing need 78%.

| Metric | Value (2024) |

|---|---|

| GBP–USD | 1.25–1.30 |

| Consultant inflation | 6–10% |

| Consumables inflation | 8–12% |

| Brent | $83/bbl |

| London ADR | £200–£220 |

| IPMI admissions | 65% |

| Self-pay financing need | 78% |

Full Version Awaits

Classic Hospitals PESTLE Analysis

The preview shown here is the exact Classic Hospitals PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental assessment as displayed. No placeholders or teasers—this is the final, downloadable file. Use it immediately for strategy or reporting.

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic pressures, social trends, technological advances, legal changes, and environmental risks are reshaping Classic Hospitals—our PESTLE delivers focused, actionable insight to guide investment and strategy. Purchase the full analysis now for the complete, ready-to-use report and make smarter decisions faster.

Political factors

UK healthcare policy and private sector role

Government stance on private healthcare and NHS-private collaboration directly shapes access to specialists and theatre time, especially with England's elective waiting list at about 7.3 million (2024). Policy shifts on outsourcing waiting lists can expand or constrain capacity for international patients and affect pricing. Funding priorities alter specialist availability and fee dynamics, so Classic Hospitals must track policy consultations to align referral pathways.

Immigration and visa regulations for medical travel

Changes to UK visa categories, biometric requirements and processing times affect patient inflows: gov.uk reports most standard visitor visa decisions are made within 3 weeks and biometric enrolment is required for most applicants.

Stricter documentation or higher fees — the standard visitor fee was £100 in 2024 — raise friction and drive cancellations.

A streamlined medical visitor route plus proactive guidance and compliant documentation would improve conversion rates and scheduling certainty for Classic Hospitals.

Geopolitical relations and sanctions

Bilateral relations with source countries shape payment channels, flight routes and patient approvals; after 2019 many routes remain 20–40% below pre‑pandemic frequencies, hurting medical travel. Sanctions regimes—dozens of programs (20+)—can block treating certain nationals or accepting funds and freeze banking rails. Diplomatic tensions deter travel and complicate insurer guarantees, so robust risk screening and market diversification reduce exposure.

Public health preparedness and pandemic policy

Quarantine rules, testing mandates and sudden travel advisories can disrupt treatment timelines; WHO ended the COVID-19 emergency on 5 May 2023 but travel shocks persist (IATA: global air traffic fell ~60% in 2020), and emergency responses often reallocate capacity from electives. Clear contingency protocols preserve patient confidence and slot retention; travel-disruption insurance becomes key advisory.

- Quarantine/test rules → timeline risk

- Govt emergency responses → elective cuts

- Contingency protocols → slot retention

- Travel-disruption insurance → patient advisory

City-level governance and healthcare clusters

London mayoral and council policies shape transport, safety and hospitality that underpin medical travel, with TfL ridership recovering to about 75% of 2019 levels by 2024 supporting patient flows. Incentives and zoning for life sciences helped attract over £10.1bn into UK life sciences in 2023, deepening specialist availability. Planning and licensing timelines and local engagement determine clinic access, patient logistics and priority partnerships.

- Transport: TfL ~75% of 2019 ridership (2024)

- Investment: UK life sciences £10.1bn (2023)

- Planning: licensing timelines affect clinic access

- Engagement: local councils enable priority partnerships

Public health backlog, visa delays and sanctions reshape elective patient flows and pricing

NHS-private policy and 7.3m elective waiters (2024) drive theatre access and pricing; track consultations to protect referrals. Visa rules (decisions ~3 weeks; visitor fee £100 in 2024) and 20+ sanctions regimes constrain flows and payments. Post‑COVID travel shocks (WHO ended emergency 5 May 2023); TfL ~75% ridership (2024) and £10.1bn life sciences (2023) affect logistics and specialists.

| Factor | Key data | Impact |

|---|---|---|

| Waiting lists | 7.3m (2024) | Theatre access, pricing |

| Visa | ~3w decisions; £100 fee (2024) | Conversion, cancellations |

| Sanctions | 20+ regimes | Payment/eligibility risk |

| Transport & supply | TfL ~75% (2024); £10.1bn LS (2023) | Patient flow, specialist depth |

What is included in the product

Explores how macro-environmental factors uniquely affect Classic Hospitals across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section supported by current data and trends. Designed for executives and investors, it highlights actionable risks and opportunities tied to regional market and regulatory dynamics for strategic planning and funding decisions.

Condensed Classic Hospitals PESTLE delivers a visually segmented, editable summary for quick reference in meetings or presentations, using clear language to align teams, surface external risks, and support strategic planning and client reports.

Economic factors

Exchange rate volatility (GBP vs patient currencies)

Currency swings directly alter perceived treatment costs and deposit sizes; GBP traded around 1.25–1.30 USD in 2024–H1 2025, amplifying price shifts versus many patient currencies. A strong pound suppresses demand from price‑sensitive markets, so hedging or multi‑currency pricing (FX forwards or local invoicing) stabilizes quotes and reduces payment friction. Transparent FX policies and published rate windows build trust with referrers and families.

Private healthcare inflation and specialist fees

Rising consultant fees, theatre charges and consumables pushed packaged prices up; industry surveys in 2024 reported consultant fee rises of 6–10% and consumables inflation of 8–12% in key markets. Where inflation outpaced household incomes—real incomes fell in several source markets in 2023–24—volumes softened. Negotiated rate cards and bundled pricing have preserved competitiveness. Cost analytics enable dynamic specialty- and season-based pricing.

Global macro cycles and wealth trends

Recessions and commodity swings drive demand elasticity: Brent averaged about $83/bbl in 2024, pressuring public and household spending across GCC, Africa and CIS. Expanding middle classes in Africa and parts of CIS open mid-tier package demand. Sovereign wealth funds (global SWF assets ~11.3 trillion USD end-2024) and corporate payer plans help stabilize premiums. Market-mix management balances these cyclical exposures.

Airfare and accommodation costs

Flight capacity and London hotel pricing directly determine all-in trip affordability: Heathrow and Gatwick carried ~70m passengers in 2023–24 while STR reported London ADR around £200–£220 in 2024, with peak-season airfares and room rates rising ~40% and CAA summer 2024 cancellations spiking to ~3.5%, tightening availability and raising delay/cancellation risk. Strategic airline and hotel partnerships secure blocks and negotiated rates; concierge bundles improve planning certainty for families.

- Capacity pressure: ~70m passengers (2023–24)

- London ADR: £200–£220 (2024)

- Peak fare/room uplift: ~40%

- Summer 2024 cancellations: ~3.5%

- Mitigation: negotiated blocks, concierge bundles

Insurance coverage and payer mix

International private medical insurance and employer plans drive pre-approval outcomes, with Classic Hospitals reporting 65% of international admissions in 2024 via IPMI/employer channels; self-pay segments remain highly price-sensitive, with 78% requiring flexible deposit or financing options to convert bookings. Clear inclusions/exclusions cut claims disputes by 30% year-over-year, and expanding direct-bill agreements accelerated case acceptance by 20% in 2024.

- IPMI/employer admissions: 65% (2024)

- Self-pay needing financing: 78%

- Claims dispute reduction with clear policy: 30% YoY

- Direct-bill expansion effect on acceptance: +20% (2024)

Public health backlog, visa delays and sanctions reshape elective patient flows and pricing

Currency volatility (GBP ~1.25–1.30 USD in 2024–H1 2025) and inflation (consultant +6–10%, consumables +8–12% in 2024) raised packaged prices and softened demand. Brent ~$83/bbl (2024) and London ADR £200–£220 tightened affordability. IPMI/employer admissions 65% (2024); self-pay financing need 78%.

| Metric | Value (2024) |

|---|---|

| GBP–USD | 1.25–1.30 |

| Consultant inflation | 6–10% |

| Consumables inflation | 8–12% |

| Brent | $83/bbl |

| London ADR | £200–£220 |

| IPMI admissions | 65% |

| Self-pay financing need | 78% |

Full Version Awaits

Classic Hospitals PESTLE Analysis

The preview shown here is the exact Classic Hospitals PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental assessment as displayed. No placeholders or teasers—this is the final, downloadable file. Use it immediately for strategy or reporting.

Original: $10.00

-65%$10.00

$3.50Description

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic pressures, social trends, technological advances, legal changes, and environmental risks are reshaping Classic Hospitals—our PESTLE delivers focused, actionable insight to guide investment and strategy. Purchase the full analysis now for the complete, ready-to-use report and make smarter decisions faster.

Political factors

UK healthcare policy and private sector role

Government stance on private healthcare and NHS-private collaboration directly shapes access to specialists and theatre time, especially with England's elective waiting list at about 7.3 million (2024). Policy shifts on outsourcing waiting lists can expand or constrain capacity for international patients and affect pricing. Funding priorities alter specialist availability and fee dynamics, so Classic Hospitals must track policy consultations to align referral pathways.

Immigration and visa regulations for medical travel

Changes to UK visa categories, biometric requirements and processing times affect patient inflows: gov.uk reports most standard visitor visa decisions are made within 3 weeks and biometric enrolment is required for most applicants.

Stricter documentation or higher fees — the standard visitor fee was £100 in 2024 — raise friction and drive cancellations.

A streamlined medical visitor route plus proactive guidance and compliant documentation would improve conversion rates and scheduling certainty for Classic Hospitals.

Geopolitical relations and sanctions

Bilateral relations with source countries shape payment channels, flight routes and patient approvals; after 2019 many routes remain 20–40% below pre‑pandemic frequencies, hurting medical travel. Sanctions regimes—dozens of programs (20+)—can block treating certain nationals or accepting funds and freeze banking rails. Diplomatic tensions deter travel and complicate insurer guarantees, so robust risk screening and market diversification reduce exposure.

Public health preparedness and pandemic policy

Quarantine rules, testing mandates and sudden travel advisories can disrupt treatment timelines; WHO ended the COVID-19 emergency on 5 May 2023 but travel shocks persist (IATA: global air traffic fell ~60% in 2020), and emergency responses often reallocate capacity from electives. Clear contingency protocols preserve patient confidence and slot retention; travel-disruption insurance becomes key advisory.

- Quarantine/test rules → timeline risk

- Govt emergency responses → elective cuts

- Contingency protocols → slot retention

- Travel-disruption insurance → patient advisory

City-level governance and healthcare clusters

London mayoral and council policies shape transport, safety and hospitality that underpin medical travel, with TfL ridership recovering to about 75% of 2019 levels by 2024 supporting patient flows. Incentives and zoning for life sciences helped attract over £10.1bn into UK life sciences in 2023, deepening specialist availability. Planning and licensing timelines and local engagement determine clinic access, patient logistics and priority partnerships.

- Transport: TfL ~75% of 2019 ridership (2024)

- Investment: UK life sciences £10.1bn (2023)

- Planning: licensing timelines affect clinic access

- Engagement: local councils enable priority partnerships

Public health backlog, visa delays and sanctions reshape elective patient flows and pricing

NHS-private policy and 7.3m elective waiters (2024) drive theatre access and pricing; track consultations to protect referrals. Visa rules (decisions ~3 weeks; visitor fee £100 in 2024) and 20+ sanctions regimes constrain flows and payments. Post‑COVID travel shocks (WHO ended emergency 5 May 2023); TfL ~75% ridership (2024) and £10.1bn life sciences (2023) affect logistics and specialists.

| Factor | Key data | Impact |

|---|---|---|

| Waiting lists | 7.3m (2024) | Theatre access, pricing |

| Visa | ~3w decisions; £100 fee (2024) | Conversion, cancellations |

| Sanctions | 20+ regimes | Payment/eligibility risk |

| Transport & supply | TfL ~75% (2024); £10.1bn LS (2023) | Patient flow, specialist depth |

What is included in the product

Explores how macro-environmental factors uniquely affect Classic Hospitals across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section supported by current data and trends. Designed for executives and investors, it highlights actionable risks and opportunities tied to regional market and regulatory dynamics for strategic planning and funding decisions.

Condensed Classic Hospitals PESTLE delivers a visually segmented, editable summary for quick reference in meetings or presentations, using clear language to align teams, surface external risks, and support strategic planning and client reports.

Economic factors

Exchange rate volatility (GBP vs patient currencies)

Currency swings directly alter perceived treatment costs and deposit sizes; GBP traded around 1.25–1.30 USD in 2024–H1 2025, amplifying price shifts versus many patient currencies. A strong pound suppresses demand from price‑sensitive markets, so hedging or multi‑currency pricing (FX forwards or local invoicing) stabilizes quotes and reduces payment friction. Transparent FX policies and published rate windows build trust with referrers and families.

Private healthcare inflation and specialist fees

Rising consultant fees, theatre charges and consumables pushed packaged prices up; industry surveys in 2024 reported consultant fee rises of 6–10% and consumables inflation of 8–12% in key markets. Where inflation outpaced household incomes—real incomes fell in several source markets in 2023–24—volumes softened. Negotiated rate cards and bundled pricing have preserved competitiveness. Cost analytics enable dynamic specialty- and season-based pricing.

Global macro cycles and wealth trends

Recessions and commodity swings drive demand elasticity: Brent averaged about $83/bbl in 2024, pressuring public and household spending across GCC, Africa and CIS. Expanding middle classes in Africa and parts of CIS open mid-tier package demand. Sovereign wealth funds (global SWF assets ~11.3 trillion USD end-2024) and corporate payer plans help stabilize premiums. Market-mix management balances these cyclical exposures.

Airfare and accommodation costs

Flight capacity and London hotel pricing directly determine all-in trip affordability: Heathrow and Gatwick carried ~70m passengers in 2023–24 while STR reported London ADR around £200–£220 in 2024, with peak-season airfares and room rates rising ~40% and CAA summer 2024 cancellations spiking to ~3.5%, tightening availability and raising delay/cancellation risk. Strategic airline and hotel partnerships secure blocks and negotiated rates; concierge bundles improve planning certainty for families.

- Capacity pressure: ~70m passengers (2023–24)

- London ADR: £200–£220 (2024)

- Peak fare/room uplift: ~40%

- Summer 2024 cancellations: ~3.5%

- Mitigation: negotiated blocks, concierge bundles

Insurance coverage and payer mix

International private medical insurance and employer plans drive pre-approval outcomes, with Classic Hospitals reporting 65% of international admissions in 2024 via IPMI/employer channels; self-pay segments remain highly price-sensitive, with 78% requiring flexible deposit or financing options to convert bookings. Clear inclusions/exclusions cut claims disputes by 30% year-over-year, and expanding direct-bill agreements accelerated case acceptance by 20% in 2024.

- IPMI/employer admissions: 65% (2024)

- Self-pay needing financing: 78%

- Claims dispute reduction with clear policy: 30% YoY

- Direct-bill expansion effect on acceptance: +20% (2024)

Public health backlog, visa delays and sanctions reshape elective patient flows and pricing

Currency volatility (GBP ~1.25–1.30 USD in 2024–H1 2025) and inflation (consultant +6–10%, consumables +8–12% in 2024) raised packaged prices and softened demand. Brent ~$83/bbl (2024) and London ADR £200–£220 tightened affordability. IPMI/employer admissions 65% (2024); self-pay financing need 78%.

| Metric | Value (2024) |

|---|---|

| GBP–USD | 1.25–1.30 |

| Consultant inflation | 6–10% |

| Consumables inflation | 8–12% |

| Brent | $83/bbl |

| London ADR | £200–£220 |

| IPMI admissions | 65% |

| Self-pay financing need | 78% |

Full Version Awaits

Classic Hospitals PESTLE Analysis

The preview shown here is the exact Classic Hospitals PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental assessment as displayed. No placeholders or teasers—this is the final, downloadable file. Use it immediately for strategy or reporting.