Clear Secure Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

This brief snapshot highlights Clear Secure’s competitive dynamics, market pressures, and strategic advantages, but only scratches the surface; the full Porter's Five Forces Analysis delivers force-by-force ratings, visuals, and actionable implications tailored to Clear Secure. Unlock the complete report to quantify supplier and buyer power, entrant and substitute threats, and competitive rivalry for smarter strategy and investment decisions.

Suppliers Bargaining Power

Specialized biometric hardware vendors

Clear depends on a limited pool of certified biometric device makers for iris/fingerprint scanners and liveness detection, giving suppliers outsized leverage and raising switching costs; certification lead times commonly run 3–12 months and semiconductor lead times have exceeded 20 weeks, amplifying rollout risk. Long-term supply contracts can blunt price pressure but create lock-in, while component shortages or certification changes can disrupt deployments and service levels.

Cloud and security infrastructure providers

Dependence on hyperscalers concentrates supplier power: in 2024 AWS, Azure and GCP together held about 66% of cloud market share, giving pricing leverage. Changes in pricing, egress fees and compliance features can materially compress gross margins for Clear. Multi-cloud deployments (used by ~92% of enterprises in 2024) and in-house optimizations reduce exposure but increase complexity and ops cost. Data residency and strict encryption standards narrow provider choice and raise integration burden.

Identity data, verification, and KYC sources

Feeds from DMVs, the three major credit bureaus (Experian, Equifax, TransUnion), and third-party KYC/AML providers are critical to verification accuracy and fraud prevention. These sources are concentrated and heavily regulated, giving suppliers significant bargaining power. Contractual access terms, per-lookup pricing and usage restrictions materially affect Clear’s unit economics. Any withdrawal of these feeds can materially reduce match rates and degrade customer experience.

Airport and venue infrastructure partners

Access to airport and venue footprints is a quasi-supply input: gatekeeper landlords control placement, exclusivity, and operating windows, raising supplier leverage; limited premium space and narrow operational windows amplify bargaining power. As of 2024 Clear operated in over 60 airports and venues, making co-marketing and revenue-sharing common but creating deeper dependence.

- Gatekeeper landlords: dictate terms, placement, exclusivity

- Scarce premium space: increases landlord leverage

- Co-marketing/revenue share: realigns incentives but heightens dependence

Regulatory bodies and certification authorities

Regulatory bodies such as TSA and DHS and privacy regimes like California CPRA create a supply constraint on Clear by dictating biometric and identity standards; compliance remains mandatory in 2024 and limits rapid capability expansion. Lengthy approval cycles and recurring audits routinely delay deployments and raise compliance costs, sometimes spanning many months for device and workflow certifications. Rule changes force design or workflow redesigns and certification dependency grants implicit bargaining power to regulators and accredited labs.

- Regulators: TSA, DHS, state privacy (CCPA/CPRA) — 2024 enforcement active

- Impact: approval/audit delays extend timelines, increase costs

- Dependency: certified labs/regulators hold implicit bargaining power

Concentrated suppliers hike costs: cloud 66%, venues 60+

Clear faces concentrated supplier power: certified biometric vendors (cert lead 3–12 months, semiconductor lead >20 weeks) and cloud hyperscalers (AWS/Azure/GCP ≈66% market share in 2024) raise costs and switching barriers. DMV/credit bureau feeds and gatekeeper landlords (Clear in 60+ airports/venues in 2024) further constrain pricing and access.

| Supplier | 2024 Metric |

|---|---|

| Hyperscalers | 66% market share |

| Multi-cloud adoption | ~92% enterprises |

| Airport footprint | 60+ sites |

What is included in the product

Analyzes competitive intensity, buyer and supplier power, threat of substitutes, and entry barriers specific to Clear Secure, identifying disruptive forces, pricing pressures, and strategic levers to protect and grow market share—editable for reports.

A concise, one-sheet Porter's Five Forces for Clear Secure that turns complex competitive dynamics into an at-a-glance radar chart—customize pressure levels, swap in your own data, and drop directly into decks for faster, board-ready decisions.

Customers Bargaining Power

Individual subscribers’ price sensitivity

Travelers weigh the CLEAR Plus fee of $189 (2024) against time savings and trip frequency, with frequent flyers more willing to pay while occasional travelers are price-sensitive. Credit-card perks and elite airline status often subsidize or replace CLEAR value, reducing willingness to pay. Churn rises when travel volumes dip or airport wait times compress; intro offers and bundling blunt sensitivity but squeeze ARPU.

Enterprise and venue clients’ negotiating leverage

Airports, airlines and stadiums control lane access and passenger flow, giving them strong negotiating leverage over Clear Secure through gatekeeping and scheduling control. Their multi-year contracts and scale allow them to insist on pricing concessions, strict SLAs, integrations and revenue-sharing arrangements. Competing vendors and public procurement processes amplify bidding pressure and limit Clear’s margin flexibility. This concentration of buyer power raises renewal and pricing risk for Clear.

Multi-homing and switching ease

Buyers can layer CLEAR with TSA PreCheck—CLEAR reported ~15 million users and TSA PreCheck ~12 million members in 2024—so consumers often multi-home rather than substitute entirely. Enterprise clients routinely pilot rival identity providers in parallel, reducing switching friction. Data portability remains limited, but front-end substitution at contract renewal is feasible, weakening vendor lock-in and increasing buyer bargaining power.

Demand concentration at key hubs

Volume is heavily concentrated at major airports and venues, giving a handful of hub accounts outsized influence over Clear Secures utilization and brand visibility; losing a hub materially reduces throughput and public exposure. This concentration strengthens buyers in negotiations over fees and placement, pressuring pricing and concession terms. Expanding into diversified use cases in 2024—stadiums, healthcare, and retail—reduces dependence on a few accounts and eases bargaining leverage.

- Concentration: few hubs drive most usage

- Risk: loss of a hub cuts visibility

- Bargaining: buyers press fees/placements

- Mitigation: diversify to stadiums, healthcare, retail

Security, privacy, and trust requirements

Buyers demand rigorous privacy controls and transparent governance; a 2024 IBM report found the average data breach cost $4.45M, pushing customers to insist on stricter SLAs and audit rights. Any incident shifts leverage to buyers, who may tighten terms or exit, while enterprise risk committees lengthen sales cycles and press for broader indemnities. Strong compliance programs can flip this cost into a competitive selling point.

- Buyer demands: privacy, governance, audit rights

- Post-incident power: stricter terms/exits

- Sales impact: longer cycles, indemnity pressure

- Opportunity: compliance as differentiation

Multi-homing:~15M vs ~12M; breach $4.45M

Customers exert strong bargaining power: fee-sensitive occasional travelers vs loyal frequent flyers (CLEAR Plus $189 in 2024); multi-homing is common (CLEAR ~15M users, TSA PreCheck ~12M in 2024), and major hubs hold outsized leverage. Enterprises demand tight privacy/SLA terms after an average breach cost of $4.45M (2024), extending sales cycles and pressing concessions.

| Metric | 2024 |

|---|---|

| CLEAR users | ~15M |

| TSA PreCheck members | ~12M |

| CLEAR Plus fee | $189 |

| Avg breach cost | $4.45M |

What You See Is What You Get

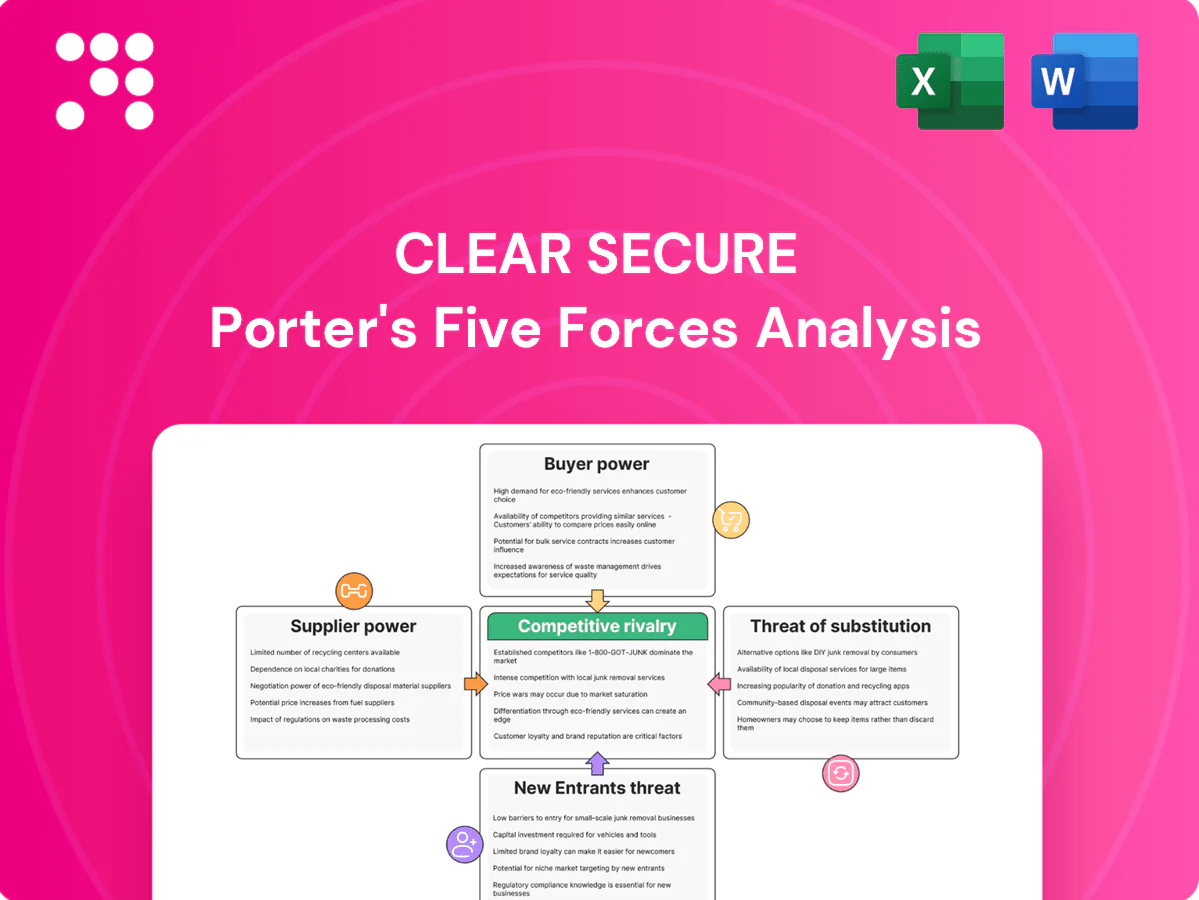

Clear Secure Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Clear Secure you’ll receive immediately after purchase—no placeholders, edits, or missing sections. The file is fully formatted, professionally written, and ready for download and use the moment you buy. What you see here is the complete deliverable, instantly accessible upon payment.

A Must-Have Tool for Decision-Makers

This brief snapshot highlights Clear Secure’s competitive dynamics, market pressures, and strategic advantages, but only scratches the surface; the full Porter's Five Forces Analysis delivers force-by-force ratings, visuals, and actionable implications tailored to Clear Secure. Unlock the complete report to quantify supplier and buyer power, entrant and substitute threats, and competitive rivalry for smarter strategy and investment decisions.

Suppliers Bargaining Power

Specialized biometric hardware vendors

Clear depends on a limited pool of certified biometric device makers for iris/fingerprint scanners and liveness detection, giving suppliers outsized leverage and raising switching costs; certification lead times commonly run 3–12 months and semiconductor lead times have exceeded 20 weeks, amplifying rollout risk. Long-term supply contracts can blunt price pressure but create lock-in, while component shortages or certification changes can disrupt deployments and service levels.

Cloud and security infrastructure providers

Dependence on hyperscalers concentrates supplier power: in 2024 AWS, Azure and GCP together held about 66% of cloud market share, giving pricing leverage. Changes in pricing, egress fees and compliance features can materially compress gross margins for Clear. Multi-cloud deployments (used by ~92% of enterprises in 2024) and in-house optimizations reduce exposure but increase complexity and ops cost. Data residency and strict encryption standards narrow provider choice and raise integration burden.

Identity data, verification, and KYC sources

Feeds from DMVs, the three major credit bureaus (Experian, Equifax, TransUnion), and third-party KYC/AML providers are critical to verification accuracy and fraud prevention. These sources are concentrated and heavily regulated, giving suppliers significant bargaining power. Contractual access terms, per-lookup pricing and usage restrictions materially affect Clear’s unit economics. Any withdrawal of these feeds can materially reduce match rates and degrade customer experience.

Airport and venue infrastructure partners

Access to airport and venue footprints is a quasi-supply input: gatekeeper landlords control placement, exclusivity, and operating windows, raising supplier leverage; limited premium space and narrow operational windows amplify bargaining power. As of 2024 Clear operated in over 60 airports and venues, making co-marketing and revenue-sharing common but creating deeper dependence.

- Gatekeeper landlords: dictate terms, placement, exclusivity

- Scarce premium space: increases landlord leverage

- Co-marketing/revenue share: realigns incentives but heightens dependence

Regulatory bodies and certification authorities

Regulatory bodies such as TSA and DHS and privacy regimes like California CPRA create a supply constraint on Clear by dictating biometric and identity standards; compliance remains mandatory in 2024 and limits rapid capability expansion. Lengthy approval cycles and recurring audits routinely delay deployments and raise compliance costs, sometimes spanning many months for device and workflow certifications. Rule changes force design or workflow redesigns and certification dependency grants implicit bargaining power to regulators and accredited labs.

- Regulators: TSA, DHS, state privacy (CCPA/CPRA) — 2024 enforcement active

- Impact: approval/audit delays extend timelines, increase costs

- Dependency: certified labs/regulators hold implicit bargaining power

Concentrated suppliers hike costs: cloud 66%, venues 60+

Clear faces concentrated supplier power: certified biometric vendors (cert lead 3–12 months, semiconductor lead >20 weeks) and cloud hyperscalers (AWS/Azure/GCP ≈66% market share in 2024) raise costs and switching barriers. DMV/credit bureau feeds and gatekeeper landlords (Clear in 60+ airports/venues in 2024) further constrain pricing and access.

| Supplier | 2024 Metric |

|---|---|

| Hyperscalers | 66% market share |

| Multi-cloud adoption | ~92% enterprises |

| Airport footprint | 60+ sites |

What is included in the product

Analyzes competitive intensity, buyer and supplier power, threat of substitutes, and entry barriers specific to Clear Secure, identifying disruptive forces, pricing pressures, and strategic levers to protect and grow market share—editable for reports.

A concise, one-sheet Porter's Five Forces for Clear Secure that turns complex competitive dynamics into an at-a-glance radar chart—customize pressure levels, swap in your own data, and drop directly into decks for faster, board-ready decisions.

Customers Bargaining Power

Individual subscribers’ price sensitivity

Travelers weigh the CLEAR Plus fee of $189 (2024) against time savings and trip frequency, with frequent flyers more willing to pay while occasional travelers are price-sensitive. Credit-card perks and elite airline status often subsidize or replace CLEAR value, reducing willingness to pay. Churn rises when travel volumes dip or airport wait times compress; intro offers and bundling blunt sensitivity but squeeze ARPU.

Enterprise and venue clients’ negotiating leverage

Airports, airlines and stadiums control lane access and passenger flow, giving them strong negotiating leverage over Clear Secure through gatekeeping and scheduling control. Their multi-year contracts and scale allow them to insist on pricing concessions, strict SLAs, integrations and revenue-sharing arrangements. Competing vendors and public procurement processes amplify bidding pressure and limit Clear’s margin flexibility. This concentration of buyer power raises renewal and pricing risk for Clear.

Multi-homing and switching ease

Buyers can layer CLEAR with TSA PreCheck—CLEAR reported ~15 million users and TSA PreCheck ~12 million members in 2024—so consumers often multi-home rather than substitute entirely. Enterprise clients routinely pilot rival identity providers in parallel, reducing switching friction. Data portability remains limited, but front-end substitution at contract renewal is feasible, weakening vendor lock-in and increasing buyer bargaining power.

Demand concentration at key hubs

Volume is heavily concentrated at major airports and venues, giving a handful of hub accounts outsized influence over Clear Secures utilization and brand visibility; losing a hub materially reduces throughput and public exposure. This concentration strengthens buyers in negotiations over fees and placement, pressuring pricing and concession terms. Expanding into diversified use cases in 2024—stadiums, healthcare, and retail—reduces dependence on a few accounts and eases bargaining leverage.

- Concentration: few hubs drive most usage

- Risk: loss of a hub cuts visibility

- Bargaining: buyers press fees/placements

- Mitigation: diversify to stadiums, healthcare, retail

Security, privacy, and trust requirements

Buyers demand rigorous privacy controls and transparent governance; a 2024 IBM report found the average data breach cost $4.45M, pushing customers to insist on stricter SLAs and audit rights. Any incident shifts leverage to buyers, who may tighten terms or exit, while enterprise risk committees lengthen sales cycles and press for broader indemnities. Strong compliance programs can flip this cost into a competitive selling point.

- Buyer demands: privacy, governance, audit rights

- Post-incident power: stricter terms/exits

- Sales impact: longer cycles, indemnity pressure

- Opportunity: compliance as differentiation

Multi-homing:~15M vs ~12M; breach $4.45M

Customers exert strong bargaining power: fee-sensitive occasional travelers vs loyal frequent flyers (CLEAR Plus $189 in 2024); multi-homing is common (CLEAR ~15M users, TSA PreCheck ~12M in 2024), and major hubs hold outsized leverage. Enterprises demand tight privacy/SLA terms after an average breach cost of $4.45M (2024), extending sales cycles and pressing concessions.

| Metric | 2024 |

|---|---|

| CLEAR users | ~15M |

| TSA PreCheck members | ~12M |

| CLEAR Plus fee | $189 |

| Avg breach cost | $4.45M |

What You See Is What You Get

Clear Secure Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Clear Secure you’ll receive immediately after purchase—no placeholders, edits, or missing sections. The file is fully formatted, professionally written, and ready for download and use the moment you buy. What you see here is the complete deliverable, instantly accessible upon payment.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

This brief snapshot highlights Clear Secure’s competitive dynamics, market pressures, and strategic advantages, but only scratches the surface; the full Porter's Five Forces Analysis delivers force-by-force ratings, visuals, and actionable implications tailored to Clear Secure. Unlock the complete report to quantify supplier and buyer power, entrant and substitute threats, and competitive rivalry for smarter strategy and investment decisions.

Suppliers Bargaining Power

Specialized biometric hardware vendors

Clear depends on a limited pool of certified biometric device makers for iris/fingerprint scanners and liveness detection, giving suppliers outsized leverage and raising switching costs; certification lead times commonly run 3–12 months and semiconductor lead times have exceeded 20 weeks, amplifying rollout risk. Long-term supply contracts can blunt price pressure but create lock-in, while component shortages or certification changes can disrupt deployments and service levels.

Cloud and security infrastructure providers

Dependence on hyperscalers concentrates supplier power: in 2024 AWS, Azure and GCP together held about 66% of cloud market share, giving pricing leverage. Changes in pricing, egress fees and compliance features can materially compress gross margins for Clear. Multi-cloud deployments (used by ~92% of enterprises in 2024) and in-house optimizations reduce exposure but increase complexity and ops cost. Data residency and strict encryption standards narrow provider choice and raise integration burden.

Identity data, verification, and KYC sources

Feeds from DMVs, the three major credit bureaus (Experian, Equifax, TransUnion), and third-party KYC/AML providers are critical to verification accuracy and fraud prevention. These sources are concentrated and heavily regulated, giving suppliers significant bargaining power. Contractual access terms, per-lookup pricing and usage restrictions materially affect Clear’s unit economics. Any withdrawal of these feeds can materially reduce match rates and degrade customer experience.

Airport and venue infrastructure partners

Access to airport and venue footprints is a quasi-supply input: gatekeeper landlords control placement, exclusivity, and operating windows, raising supplier leverage; limited premium space and narrow operational windows amplify bargaining power. As of 2024 Clear operated in over 60 airports and venues, making co-marketing and revenue-sharing common but creating deeper dependence.

- Gatekeeper landlords: dictate terms, placement, exclusivity

- Scarce premium space: increases landlord leverage

- Co-marketing/revenue share: realigns incentives but heightens dependence

Regulatory bodies and certification authorities

Regulatory bodies such as TSA and DHS and privacy regimes like California CPRA create a supply constraint on Clear by dictating biometric and identity standards; compliance remains mandatory in 2024 and limits rapid capability expansion. Lengthy approval cycles and recurring audits routinely delay deployments and raise compliance costs, sometimes spanning many months for device and workflow certifications. Rule changes force design or workflow redesigns and certification dependency grants implicit bargaining power to regulators and accredited labs.

- Regulators: TSA, DHS, state privacy (CCPA/CPRA) — 2024 enforcement active

- Impact: approval/audit delays extend timelines, increase costs

- Dependency: certified labs/regulators hold implicit bargaining power

Concentrated suppliers hike costs: cloud 66%, venues 60+

Clear faces concentrated supplier power: certified biometric vendors (cert lead 3–12 months, semiconductor lead >20 weeks) and cloud hyperscalers (AWS/Azure/GCP ≈66% market share in 2024) raise costs and switching barriers. DMV/credit bureau feeds and gatekeeper landlords (Clear in 60+ airports/venues in 2024) further constrain pricing and access.

| Supplier | 2024 Metric |

|---|---|

| Hyperscalers | 66% market share |

| Multi-cloud adoption | ~92% enterprises |

| Airport footprint | 60+ sites |

What is included in the product

Analyzes competitive intensity, buyer and supplier power, threat of substitutes, and entry barriers specific to Clear Secure, identifying disruptive forces, pricing pressures, and strategic levers to protect and grow market share—editable for reports.

A concise, one-sheet Porter's Five Forces for Clear Secure that turns complex competitive dynamics into an at-a-glance radar chart—customize pressure levels, swap in your own data, and drop directly into decks for faster, board-ready decisions.

Customers Bargaining Power

Individual subscribers’ price sensitivity

Travelers weigh the CLEAR Plus fee of $189 (2024) against time savings and trip frequency, with frequent flyers more willing to pay while occasional travelers are price-sensitive. Credit-card perks and elite airline status often subsidize or replace CLEAR value, reducing willingness to pay. Churn rises when travel volumes dip or airport wait times compress; intro offers and bundling blunt sensitivity but squeeze ARPU.

Enterprise and venue clients’ negotiating leverage

Airports, airlines and stadiums control lane access and passenger flow, giving them strong negotiating leverage over Clear Secure through gatekeeping and scheduling control. Their multi-year contracts and scale allow them to insist on pricing concessions, strict SLAs, integrations and revenue-sharing arrangements. Competing vendors and public procurement processes amplify bidding pressure and limit Clear’s margin flexibility. This concentration of buyer power raises renewal and pricing risk for Clear.

Multi-homing and switching ease

Buyers can layer CLEAR with TSA PreCheck—CLEAR reported ~15 million users and TSA PreCheck ~12 million members in 2024—so consumers often multi-home rather than substitute entirely. Enterprise clients routinely pilot rival identity providers in parallel, reducing switching friction. Data portability remains limited, but front-end substitution at contract renewal is feasible, weakening vendor lock-in and increasing buyer bargaining power.

Demand concentration at key hubs

Volume is heavily concentrated at major airports and venues, giving a handful of hub accounts outsized influence over Clear Secures utilization and brand visibility; losing a hub materially reduces throughput and public exposure. This concentration strengthens buyers in negotiations over fees and placement, pressuring pricing and concession terms. Expanding into diversified use cases in 2024—stadiums, healthcare, and retail—reduces dependence on a few accounts and eases bargaining leverage.

- Concentration: few hubs drive most usage

- Risk: loss of a hub cuts visibility

- Bargaining: buyers press fees/placements

- Mitigation: diversify to stadiums, healthcare, retail

Security, privacy, and trust requirements

Buyers demand rigorous privacy controls and transparent governance; a 2024 IBM report found the average data breach cost $4.45M, pushing customers to insist on stricter SLAs and audit rights. Any incident shifts leverage to buyers, who may tighten terms or exit, while enterprise risk committees lengthen sales cycles and press for broader indemnities. Strong compliance programs can flip this cost into a competitive selling point.

- Buyer demands: privacy, governance, audit rights

- Post-incident power: stricter terms/exits

- Sales impact: longer cycles, indemnity pressure

- Opportunity: compliance as differentiation

Multi-homing:~15M vs ~12M; breach $4.45M

Customers exert strong bargaining power: fee-sensitive occasional travelers vs loyal frequent flyers (CLEAR Plus $189 in 2024); multi-homing is common (CLEAR ~15M users, TSA PreCheck ~12M in 2024), and major hubs hold outsized leverage. Enterprises demand tight privacy/SLA terms after an average breach cost of $4.45M (2024), extending sales cycles and pressing concessions.

| Metric | 2024 |

|---|---|

| CLEAR users | ~15M |

| TSA PreCheck members | ~12M |

| CLEAR Plus fee | $189 |

| Avg breach cost | $4.45M |

What You See Is What You Get

Clear Secure Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Clear Secure you’ll receive immediately after purchase—no placeholders, edits, or missing sections. The file is fully formatted, professionally written, and ready for download and use the moment you buy. What you see here is the complete deliverable, instantly accessible upon payment.