Clearwater Paper PESTLE Analysis

Your Competitive Advantage Starts with This Report

Unlock strategic clarity with our Clearwater Paper PESTLE Analysis—3–5 sentence overview revealing how political, economic, social, technological, legal, and environmental forces shape the company’s outlook; buy the full report for actionable insights, editable charts, and data-driven recommendations to inform investments and strategy.

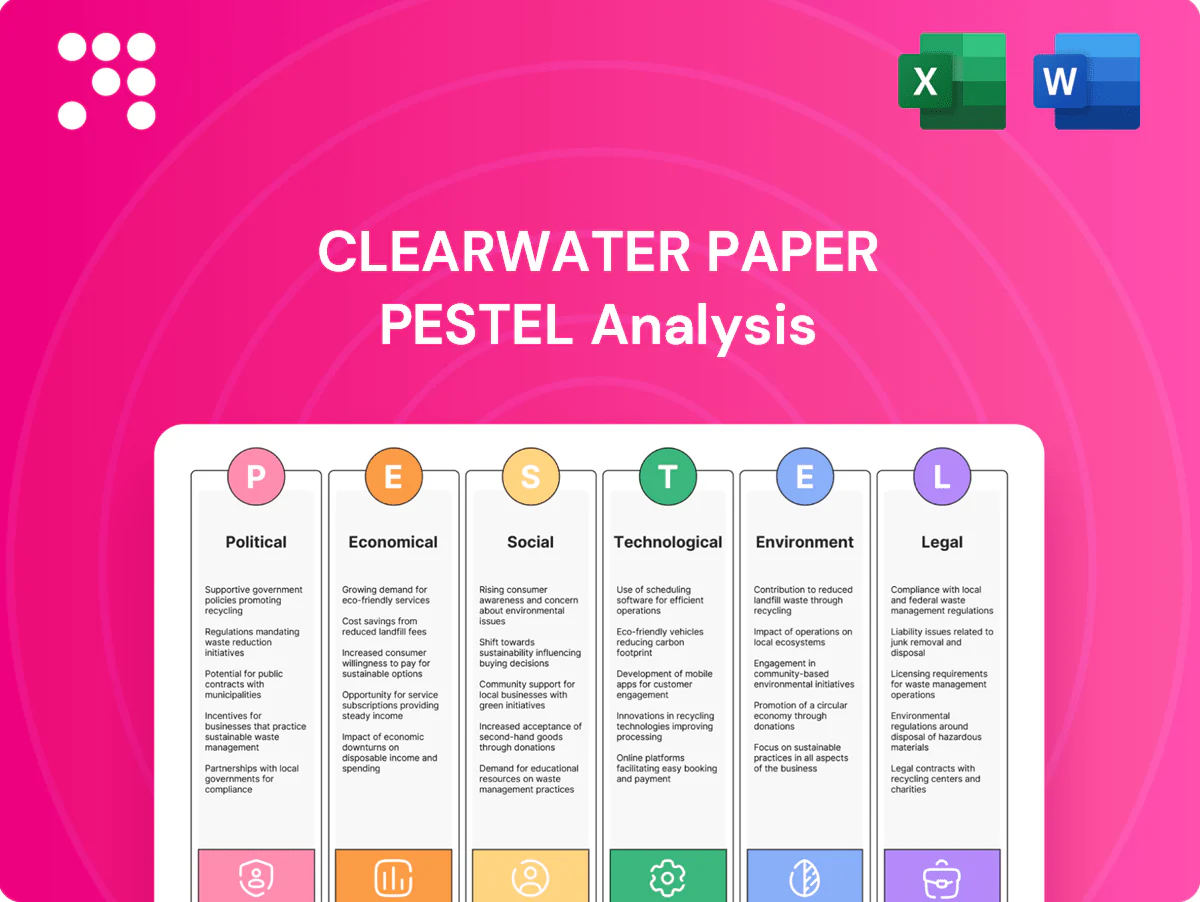

Political factors

Trade policy and tariffs on pulp and paper

Changes in tariffs on pulp, paperboard and converting equipment (historically ranging roughly 2.5–25% across key markets) can quickly alter Clearwater Paper’s input costs and pricing power. Retaliatory trade actions have pressured margins on fixed‑price private‑label contracts during past disputes, compressing EBITDA. Conversely, favorable trade deals have expanded export opportunities for North American paperboard in packaging, supporting volume growth.

Forestry and natural resources policy

National and state policies on timber harvesting and public land access directly affect fiber availability and stumpage pricing for Clearwater Paper; the U.S. holds about 487 million acres of timberland (USFS). Incentives for sustainable forestry, including state conservation cost-share programs and federal grant funding, can align with Clearwater Paper’s sourcing and certification goals. Restrictions or permitting delays on federal and state lands can tighten regional supply and elevate procurement costs.

Infrastructure and energy policy

Public investment under the Bipartisan Infrastructure Law (~$1.2 trillion) and ~ $17 billion for ports, plus trucking rules affecting ~70% of freight, directly shape freight reliability for Clearwater Paper's tissue and paperboard distribution. Energy incentives from the Inflation Reduction Act (about $369 billion for clean energy) and industrial power policies influence mill operating costs versus US industrial electricity ~7.5¢/kWh (2024). Accelerating grid decarbonization will likely force mill capex to upgrade boilers, electrification and on-site storage to meet lower-carbon power requirements.

Government procurement and AFH spending

Government procurement standards, such as the EPA Comprehensive Procurement Guidelines covering recycled-content paper, set sustainability and price benchmarks for away-from-home (AFH) tissue purchasing. U.S. federal procurement totaled about $672 billion in FY2023, so shifts in public budgets and policies—particularly in education and healthcare—can materially affect AFH demand volumes. State and municipal preference programs for recycled content are increasingly influencing product mix toward higher recycled fiber content.

- EPA CPG includes recycled-content paper products

- FY2023 U.S. federal procurement ≈ $672 billion

- Education and healthcare budget cycles drive AFH volume variability

Political stability and regional permitting

Local governance and permitting regimes around Clearwater Paper headquarters in Spokane, WA, shape mill upgrades, expansions, and environmental compliance timelines, often dictating phased mitigation and monitoring requirements. Political resistance to industrial projects in sensitive watersheds raises project risk and can delay capital deployment. Cooperative regional incentives and tax abatements can catalyze modernization and help retain manufacturing jobs.

- Permitting impact: extended review timelines increase capex hold-ups

- Political risk: local opposition raises likelihood of project delays

- Incentives: regional packages drive modernization and job retention

Tariffs, procurement & BIL/IRA drive AFH demand, logistics and timber supply

Tariffs (2.5–25%) and trade disputes materially shift input costs and export access; federal procurement (~$672B FY2023) and EPA recycled-content rules drive AFH demand mix. Infrastructure/ports funding (BIL ~$1.2T; ports ~$17B) and IRA (~$369B) affect logistics and mill energy capex; US timberland ≈487M acres impacts fiber supply.

| Factor | 2023–24 Data |

|---|---|

| Federal procurement | $672B FY2023 |

| BIL/ports/IRA | $1.2T / $17B / $369B |

| US timberland | ≈487M acres |

What is included in the product

Explores how macro-environmental factors uniquely affect Clearwater Paper across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—highlighting industry-specific drivers like pulp & paper supply chains, trade policy, and packaging demand. Each section is data‑backed, forward‑looking and formatted for executives, investors, and strategists to identify risks, opportunities and actionable responses.

A concise, visually segmented PESTLE summary of Clearwater Paper that highlights external risks, regulatory and supply-chain factors, and market positioning—easily dropped into presentations, annotated for local context, and shared across teams for quick alignment during planning sessions.

Economic factors

Input cost volatility (pulp, energy, chemicals)

Pulp and energy prices—NBSK pulp around $900/ton in mid-2024 and US industrial electricity about 7 cents/kWh—are major drivers of tissue and paperboard margins, with raw-material swings able to cut margins sharply. Cost spikes can strain fixed-price private-label contracts, compressing gross margin. Clearwater Paper uses hedging programs and supplier diversification to mitigate earnings volatility and manage working capital exposure.

Retailer consolidation and pricing power

Large retailers wield strong pricing and service demands—Walmart alone reported $611.3 billion in FY2024 net sales—pressuring private label margins for suppliers like Clearwater Paper. Volume concentration heightens sensitivity to account wins and losses, making a single retailer shift material to revenue and utilization. Differentiation through consistent quality, verified sustainability credentials, and reliable on-time supply helps defend margins and customer retention.

Consumer trade-down and private label penetration

In downturns consumers trade down to value, lifting private-label tissue demand as seen during 2020–2023 when private-label penetration surged versus pre-pandemic levels per IRI/NielsenIQ trends. In expansions branded share historically reclaims ground, pressuring private-label volumes and margin. Elastic merchandising and targeted promotions have proven to stabilize Clearwater Paper throughput and mix by smoothing SKU velocity and reducing promotional lift volatility.

Freight and logistics costs

Rising freight costs—U.S. diesel averaged $3.97/gal in 2024 (EIA)—plus persistent driver shortfalls (industry estimates in the tens of thousands) and network congestion materially raise delivered cost; tissue's low density amplifies per-unit freight, increasing sensitivity to transportation price swings, making optimized plant-to-customer routing essential to preserve Clearwater Paper's competitiveness.

- Diesel: $3.97/gal (2024, EIA)

- Driver shortage: tens of thousands (ATA estimates)

- Low-density tissue → higher freight per unit

- Routing optimization preserves margins

FX and export competitiveness in paperboard

Currency moves directly affect competitiveness of U.S.-made paperboard; a stronger dollar in 2024 (US Dollar Index averaged about 104) dampened price competitiveness and weighed on export volumes and margins. Clearwater Paper offsets FX exposure through hedging programs and a regional sales mix that emphasizes North American packaging, helping stabilize net realizations. Continued dollar strength into 2025 would likely pressure export pricing unless offset by cost or mix improvements.

- DXY 2024 average ~104

- Hedging and regional mix reduce FX volatility impact

- Strong dollar → downward pressure on export volumes/pricing

Tariffs, procurement & BIL/IRA drive AFH demand, logistics and timber supply

Pulp (NBSK ~$900/ton mid‑2024), energy (~$0.07/kWh) and freight ($3.97/gal diesel) drive margin volatility; hedging and supplier mix partly mitigate swings. Large retailers (Walmart $611.3B FY2024) and concentrated volumes increase pricing risk. Strong dollar (DXY ~104) pressures exports and realizations.

| Metric | 2024 |

|---|---|

| NBSK pulp | $900/ton |

| Electricity | $0.07/kWh |

| Diesel | $3.97/gal |

| DXY | ~104 |

| Walmart sales | $611.3B |

Preview Before You Purchase

Clearwater Paper PESTLE Analysis

The Clearwater Paper PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are the same file you’ll download immediately after payment. No placeholders or teasers—this is the real, final version of the report.

Your Competitive Advantage Starts with This Report

Unlock strategic clarity with our Clearwater Paper PESTLE Analysis—3–5 sentence overview revealing how political, economic, social, technological, legal, and environmental forces shape the company’s outlook; buy the full report for actionable insights, editable charts, and data-driven recommendations to inform investments and strategy.

Political factors

Trade policy and tariffs on pulp and paper

Changes in tariffs on pulp, paperboard and converting equipment (historically ranging roughly 2.5–25% across key markets) can quickly alter Clearwater Paper’s input costs and pricing power. Retaliatory trade actions have pressured margins on fixed‑price private‑label contracts during past disputes, compressing EBITDA. Conversely, favorable trade deals have expanded export opportunities for North American paperboard in packaging, supporting volume growth.

Forestry and natural resources policy

National and state policies on timber harvesting and public land access directly affect fiber availability and stumpage pricing for Clearwater Paper; the U.S. holds about 487 million acres of timberland (USFS). Incentives for sustainable forestry, including state conservation cost-share programs and federal grant funding, can align with Clearwater Paper’s sourcing and certification goals. Restrictions or permitting delays on federal and state lands can tighten regional supply and elevate procurement costs.

Infrastructure and energy policy

Public investment under the Bipartisan Infrastructure Law (~$1.2 trillion) and ~ $17 billion for ports, plus trucking rules affecting ~70% of freight, directly shape freight reliability for Clearwater Paper's tissue and paperboard distribution. Energy incentives from the Inflation Reduction Act (about $369 billion for clean energy) and industrial power policies influence mill operating costs versus US industrial electricity ~7.5¢/kWh (2024). Accelerating grid decarbonization will likely force mill capex to upgrade boilers, electrification and on-site storage to meet lower-carbon power requirements.

Government procurement and AFH spending

Government procurement standards, such as the EPA Comprehensive Procurement Guidelines covering recycled-content paper, set sustainability and price benchmarks for away-from-home (AFH) tissue purchasing. U.S. federal procurement totaled about $672 billion in FY2023, so shifts in public budgets and policies—particularly in education and healthcare—can materially affect AFH demand volumes. State and municipal preference programs for recycled content are increasingly influencing product mix toward higher recycled fiber content.

- EPA CPG includes recycled-content paper products

- FY2023 U.S. federal procurement ≈ $672 billion

- Education and healthcare budget cycles drive AFH volume variability

Political stability and regional permitting

Local governance and permitting regimes around Clearwater Paper headquarters in Spokane, WA, shape mill upgrades, expansions, and environmental compliance timelines, often dictating phased mitigation and monitoring requirements. Political resistance to industrial projects in sensitive watersheds raises project risk and can delay capital deployment. Cooperative regional incentives and tax abatements can catalyze modernization and help retain manufacturing jobs.

- Permitting impact: extended review timelines increase capex hold-ups

- Political risk: local opposition raises likelihood of project delays

- Incentives: regional packages drive modernization and job retention

Tariffs, procurement & BIL/IRA drive AFH demand, logistics and timber supply

Tariffs (2.5–25%) and trade disputes materially shift input costs and export access; federal procurement (~$672B FY2023) and EPA recycled-content rules drive AFH demand mix. Infrastructure/ports funding (BIL ~$1.2T; ports ~$17B) and IRA (~$369B) affect logistics and mill energy capex; US timberland ≈487M acres impacts fiber supply.

| Factor | 2023–24 Data |

|---|---|

| Federal procurement | $672B FY2023 |

| BIL/ports/IRA | $1.2T / $17B / $369B |

| US timberland | ≈487M acres |

What is included in the product

Explores how macro-environmental factors uniquely affect Clearwater Paper across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—highlighting industry-specific drivers like pulp & paper supply chains, trade policy, and packaging demand. Each section is data‑backed, forward‑looking and formatted for executives, investors, and strategists to identify risks, opportunities and actionable responses.

A concise, visually segmented PESTLE summary of Clearwater Paper that highlights external risks, regulatory and supply-chain factors, and market positioning—easily dropped into presentations, annotated for local context, and shared across teams for quick alignment during planning sessions.

Economic factors

Input cost volatility (pulp, energy, chemicals)

Pulp and energy prices—NBSK pulp around $900/ton in mid-2024 and US industrial electricity about 7 cents/kWh—are major drivers of tissue and paperboard margins, with raw-material swings able to cut margins sharply. Cost spikes can strain fixed-price private-label contracts, compressing gross margin. Clearwater Paper uses hedging programs and supplier diversification to mitigate earnings volatility and manage working capital exposure.

Retailer consolidation and pricing power

Large retailers wield strong pricing and service demands—Walmart alone reported $611.3 billion in FY2024 net sales—pressuring private label margins for suppliers like Clearwater Paper. Volume concentration heightens sensitivity to account wins and losses, making a single retailer shift material to revenue and utilization. Differentiation through consistent quality, verified sustainability credentials, and reliable on-time supply helps defend margins and customer retention.

Consumer trade-down and private label penetration

In downturns consumers trade down to value, lifting private-label tissue demand as seen during 2020–2023 when private-label penetration surged versus pre-pandemic levels per IRI/NielsenIQ trends. In expansions branded share historically reclaims ground, pressuring private-label volumes and margin. Elastic merchandising and targeted promotions have proven to stabilize Clearwater Paper throughput and mix by smoothing SKU velocity and reducing promotional lift volatility.

Freight and logistics costs

Rising freight costs—U.S. diesel averaged $3.97/gal in 2024 (EIA)—plus persistent driver shortfalls (industry estimates in the tens of thousands) and network congestion materially raise delivered cost; tissue's low density amplifies per-unit freight, increasing sensitivity to transportation price swings, making optimized plant-to-customer routing essential to preserve Clearwater Paper's competitiveness.

- Diesel: $3.97/gal (2024, EIA)

- Driver shortage: tens of thousands (ATA estimates)

- Low-density tissue → higher freight per unit

- Routing optimization preserves margins

FX and export competitiveness in paperboard

Currency moves directly affect competitiveness of U.S.-made paperboard; a stronger dollar in 2024 (US Dollar Index averaged about 104) dampened price competitiveness and weighed on export volumes and margins. Clearwater Paper offsets FX exposure through hedging programs and a regional sales mix that emphasizes North American packaging, helping stabilize net realizations. Continued dollar strength into 2025 would likely pressure export pricing unless offset by cost or mix improvements.

- DXY 2024 average ~104

- Hedging and regional mix reduce FX volatility impact

- Strong dollar → downward pressure on export volumes/pricing

Tariffs, procurement & BIL/IRA drive AFH demand, logistics and timber supply

Pulp (NBSK ~$900/ton mid‑2024), energy (~$0.07/kWh) and freight ($3.97/gal diesel) drive margin volatility; hedging and supplier mix partly mitigate swings. Large retailers (Walmart $611.3B FY2024) and concentrated volumes increase pricing risk. Strong dollar (DXY ~104) pressures exports and realizations.

| Metric | 2024 |

|---|---|

| NBSK pulp | $900/ton |

| Electricity | $0.07/kWh |

| Diesel | $3.97/gal |

| DXY | ~104 |

| Walmart sales | $611.3B |

Preview Before You Purchase

Clearwater Paper PESTLE Analysis

The Clearwater Paper PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are the same file you’ll download immediately after payment. No placeholders or teasers—this is the real, final version of the report.

Original: $10.00

-65%$10.00

$3.50Description

Your Competitive Advantage Starts with This Report

Unlock strategic clarity with our Clearwater Paper PESTLE Analysis—3–5 sentence overview revealing how political, economic, social, technological, legal, and environmental forces shape the company’s outlook; buy the full report for actionable insights, editable charts, and data-driven recommendations to inform investments and strategy.

Political factors

Trade policy and tariffs on pulp and paper

Changes in tariffs on pulp, paperboard and converting equipment (historically ranging roughly 2.5–25% across key markets) can quickly alter Clearwater Paper’s input costs and pricing power. Retaliatory trade actions have pressured margins on fixed‑price private‑label contracts during past disputes, compressing EBITDA. Conversely, favorable trade deals have expanded export opportunities for North American paperboard in packaging, supporting volume growth.

Forestry and natural resources policy

National and state policies on timber harvesting and public land access directly affect fiber availability and stumpage pricing for Clearwater Paper; the U.S. holds about 487 million acres of timberland (USFS). Incentives for sustainable forestry, including state conservation cost-share programs and federal grant funding, can align with Clearwater Paper’s sourcing and certification goals. Restrictions or permitting delays on federal and state lands can tighten regional supply and elevate procurement costs.

Infrastructure and energy policy

Public investment under the Bipartisan Infrastructure Law (~$1.2 trillion) and ~ $17 billion for ports, plus trucking rules affecting ~70% of freight, directly shape freight reliability for Clearwater Paper's tissue and paperboard distribution. Energy incentives from the Inflation Reduction Act (about $369 billion for clean energy) and industrial power policies influence mill operating costs versus US industrial electricity ~7.5¢/kWh (2024). Accelerating grid decarbonization will likely force mill capex to upgrade boilers, electrification and on-site storage to meet lower-carbon power requirements.

Government procurement and AFH spending

Government procurement standards, such as the EPA Comprehensive Procurement Guidelines covering recycled-content paper, set sustainability and price benchmarks for away-from-home (AFH) tissue purchasing. U.S. federal procurement totaled about $672 billion in FY2023, so shifts in public budgets and policies—particularly in education and healthcare—can materially affect AFH demand volumes. State and municipal preference programs for recycled content are increasingly influencing product mix toward higher recycled fiber content.

- EPA CPG includes recycled-content paper products

- FY2023 U.S. federal procurement ≈ $672 billion

- Education and healthcare budget cycles drive AFH volume variability

Political stability and regional permitting

Local governance and permitting regimes around Clearwater Paper headquarters in Spokane, WA, shape mill upgrades, expansions, and environmental compliance timelines, often dictating phased mitigation and monitoring requirements. Political resistance to industrial projects in sensitive watersheds raises project risk and can delay capital deployment. Cooperative regional incentives and tax abatements can catalyze modernization and help retain manufacturing jobs.

- Permitting impact: extended review timelines increase capex hold-ups

- Political risk: local opposition raises likelihood of project delays

- Incentives: regional packages drive modernization and job retention

Tariffs, procurement & BIL/IRA drive AFH demand, logistics and timber supply

Tariffs (2.5–25%) and trade disputes materially shift input costs and export access; federal procurement (~$672B FY2023) and EPA recycled-content rules drive AFH demand mix. Infrastructure/ports funding (BIL ~$1.2T; ports ~$17B) and IRA (~$369B) affect logistics and mill energy capex; US timberland ≈487M acres impacts fiber supply.

| Factor | 2023–24 Data |

|---|---|

| Federal procurement | $672B FY2023 |

| BIL/ports/IRA | $1.2T / $17B / $369B |

| US timberland | ≈487M acres |

What is included in the product

Explores how macro-environmental factors uniquely affect Clearwater Paper across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—highlighting industry-specific drivers like pulp & paper supply chains, trade policy, and packaging demand. Each section is data‑backed, forward‑looking and formatted for executives, investors, and strategists to identify risks, opportunities and actionable responses.

A concise, visually segmented PESTLE summary of Clearwater Paper that highlights external risks, regulatory and supply-chain factors, and market positioning—easily dropped into presentations, annotated for local context, and shared across teams for quick alignment during planning sessions.

Economic factors

Input cost volatility (pulp, energy, chemicals)

Pulp and energy prices—NBSK pulp around $900/ton in mid-2024 and US industrial electricity about 7 cents/kWh—are major drivers of tissue and paperboard margins, with raw-material swings able to cut margins sharply. Cost spikes can strain fixed-price private-label contracts, compressing gross margin. Clearwater Paper uses hedging programs and supplier diversification to mitigate earnings volatility and manage working capital exposure.

Retailer consolidation and pricing power

Large retailers wield strong pricing and service demands—Walmart alone reported $611.3 billion in FY2024 net sales—pressuring private label margins for suppliers like Clearwater Paper. Volume concentration heightens sensitivity to account wins and losses, making a single retailer shift material to revenue and utilization. Differentiation through consistent quality, verified sustainability credentials, and reliable on-time supply helps defend margins and customer retention.

Consumer trade-down and private label penetration

In downturns consumers trade down to value, lifting private-label tissue demand as seen during 2020–2023 when private-label penetration surged versus pre-pandemic levels per IRI/NielsenIQ trends. In expansions branded share historically reclaims ground, pressuring private-label volumes and margin. Elastic merchandising and targeted promotions have proven to stabilize Clearwater Paper throughput and mix by smoothing SKU velocity and reducing promotional lift volatility.

Freight and logistics costs

Rising freight costs—U.S. diesel averaged $3.97/gal in 2024 (EIA)—plus persistent driver shortfalls (industry estimates in the tens of thousands) and network congestion materially raise delivered cost; tissue's low density amplifies per-unit freight, increasing sensitivity to transportation price swings, making optimized plant-to-customer routing essential to preserve Clearwater Paper's competitiveness.

- Diesel: $3.97/gal (2024, EIA)

- Driver shortage: tens of thousands (ATA estimates)

- Low-density tissue → higher freight per unit

- Routing optimization preserves margins

FX and export competitiveness in paperboard

Currency moves directly affect competitiveness of U.S.-made paperboard; a stronger dollar in 2024 (US Dollar Index averaged about 104) dampened price competitiveness and weighed on export volumes and margins. Clearwater Paper offsets FX exposure through hedging programs and a regional sales mix that emphasizes North American packaging, helping stabilize net realizations. Continued dollar strength into 2025 would likely pressure export pricing unless offset by cost or mix improvements.

- DXY 2024 average ~104

- Hedging and regional mix reduce FX volatility impact

- Strong dollar → downward pressure on export volumes/pricing

Tariffs, procurement & BIL/IRA drive AFH demand, logistics and timber supply

Pulp (NBSK ~$900/ton mid‑2024), energy (~$0.07/kWh) and freight ($3.97/gal diesel) drive margin volatility; hedging and supplier mix partly mitigate swings. Large retailers (Walmart $611.3B FY2024) and concentrated volumes increase pricing risk. Strong dollar (DXY ~104) pressures exports and realizations.

| Metric | 2024 |

|---|---|

| NBSK pulp | $900/ton |

| Electricity | $0.07/kWh |

| Diesel | $3.97/gal |

| DXY | ~104 |

| Walmart sales | $611.3B |

Preview Before You Purchase

Clearwater Paper PESTLE Analysis

The Clearwater Paper PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are the same file you’ll download immediately after payment. No placeholders or teasers—this is the real, final version of the report.