Clearwater Paper SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

Clearwater Paper’s SWOT analysis highlights resilient manufacturing capabilities, niche market strength in tissue and pulp, and exposure to commodity cycles and regulatory risk. Discover strategic opportunities and hidden vulnerabilities that could affect valuation and operations. Want the full, editable report with expert insights and Excel tools? Purchase the complete SWOT analysis to plan, pitch, or invest with confidence.

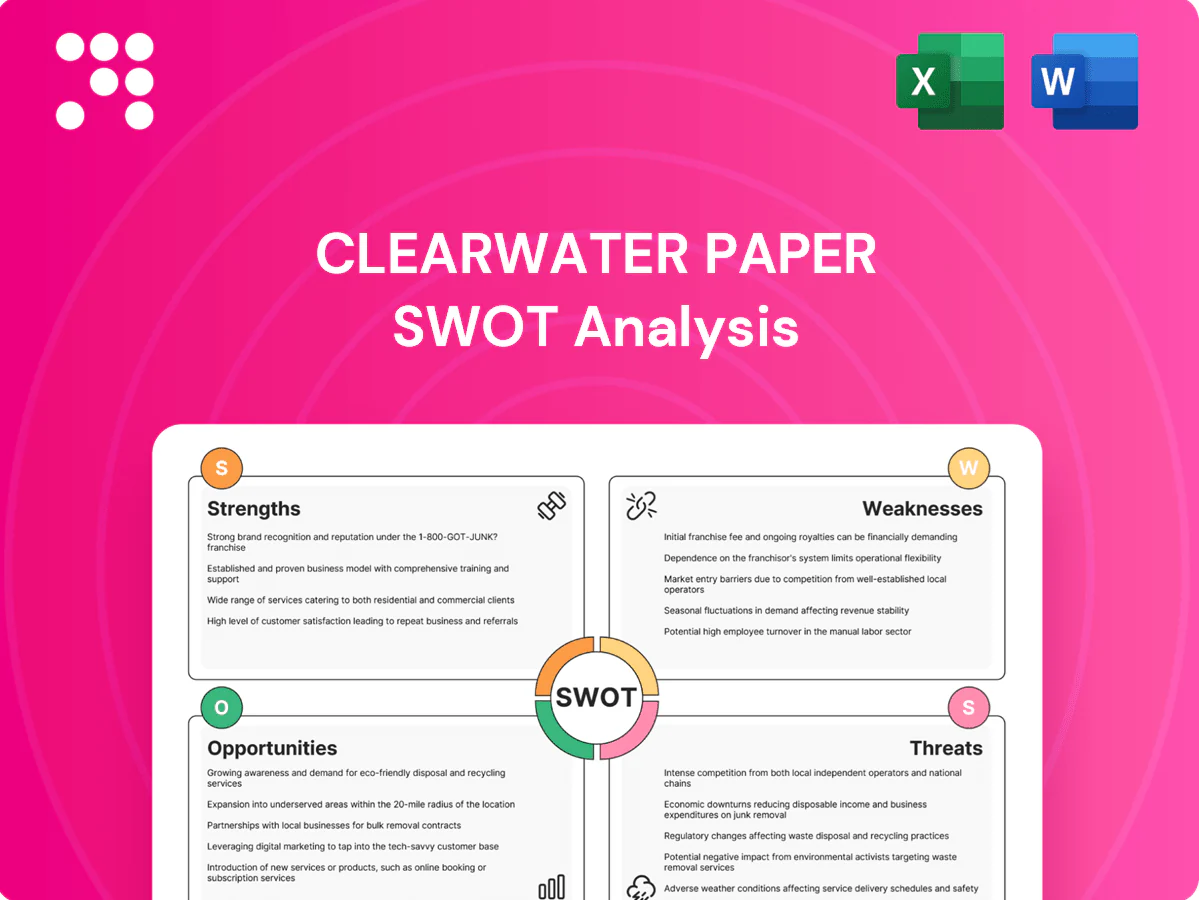

Strengths

Private-label tissue scale with major retailers

Clearwater Paper (NASDAQ: CLW) supplies major retailers and wholesalers, providing channel access and volume stability. Private-label tissue now represents roughly 25% of U.S. retail tissue volume, favoring cost-competitive suppliers like Clearwater. Its scale supports efficient procurement and production, lowering unit costs. Deep retail relationships help secure shelf space and multi-year contracts.

Diversified portfolio: consumer tissue, away-from-home, paperboard

Clearwater Paper’s diversified portfolio spans consumer tissue, away-from-home products and paperboard, smoothing revenue through different demand cycles. Consumer tissue delivers steady, non-discretionary volumes while paperboard captures packaging growth driven by e-commerce and FMCG. Away-from-home channels supply institutional, countercyclical demand streams. This mix reduces reliance on any single revenue source and supports stability in recent years.

Vertical integration in pulp and paperboard

Owning pulp and paperboard assets lowers Clearwater Paper's input risk and strengthens cost control by internalizing raw material supply chains. Vertical integration enables tighter product customization and consistent quality across grades used in consumer and specialty packaging. Internal supply buffers the company against external market shocks and can drive higher operating margins versus pure converters.

Sustainability positioning and fiber stewardship

Clearwater Paper’s sustainability positioning and fiber stewardship align with major retailer ESG mandates and supported its competitive stance in 2024; the company reported roughly $1.2 billion in net sales in 2024 and leverages certifications and responsible sourcing to capture price premiums and win bids. Eco-friendly tissue and recyclable paperboard meet rising consumer demand and strengthen RFP differentiation for long-term contracts.

Reliable supply chain and operational know-how

Clearwater Paper's reliable supply chain and process expertise underpin on-time delivery to big-box and wholesale partners, supporting repeat business and smoother new product introductions; the company reported over $1.8 billion in net sales in FY2024, reflecting strong market traction and operational continuity.

- On-time delivery to big-box/wholesale

- Converting and board production expertise

- Supply reliability builds trust

- Enables faster new product introductions

25% private-label, vertical integration & ESG drive stable margins and $1.83B sales

Clearwater Paper supplies major retailers with strong private-label exposure (≈25% U.S. retail tissue), driving stable volumes and channel access. Scale and vertical integration (own pulp/board) lower input risk and unit costs, supporting margins. Robust ESG certifications and recyclable offerings won RFPs and price premiums; FY2024 net sales ≈ $1.83B, with reliable on-time delivery to big-box partners.

| Metric | Value (2024) |

|---|---|

| Net sales | $1.83B |

| Private-label share | ≈25% |

| Vertical integration | Pulp, paperboard |

| ESG | Certifications driving premiums |

What is included in the product

Provides a concise SWOT overview of Clearwater Paper’s internal strengths and weaknesses and external opportunities and threats, highlighting competitive position, growth drivers, operational gaps, and market risks shaping its strategic outlook.

Delivers a concise SWOT matrix for Clearwater Paper to align strategy quickly; editable format enables rapid updates and seamless integration into reports and presentations for stakeholder decision-making.

Weaknesses

Exposure to commodity pulp and energy volatility

Exposure to commodity pulp and energy volatility can swing Clearwater Paper margins rapidly; pulp prices doubled in 2021–22 and remained elevated into 2024, compressing gross margins. Even with pulp and paperboard integration, market pricing feeds through to profitability. Hedging programs only partially offset short, sharp spikes. Volatility complicates pricing and inventory decisions and raises working-capital risk.

Limited brand equity versus national brands

Clearwater Paper's heavy reliance on private-label production means revenue is tied to retailer brands rather than its own, limiting consumer pull and reducing pricing power; private-label grocery penetration rose to about 17.5% in the US in 2024 (NielsenIQ), highlighting competitive pressure on branded premium pricing.

As a result, differentiation depends mainly on cost efficiency and service reliability instead of marketing-led brand equity, compressing margins when input costs rise.

Switching risk is elevated if large retail customers re-bid contracts or shift volumes to lower-cost suppliers, creating revenue volatility and contract renegotiation exposure.

Capital-intensive mills and maintenance needs

Paper and tissue assets demand ongoing capex—Clearwater Paper spent about $75 million in 2024 on maintenance and upgrades—yet planned downtime for rollovers can interrupt deliveries and service levels. High fixed costs in milling and converting raise operating leverage, making earnings highly volume-sensitive. Several plants date decades old and typically trail best-in-class efficiency and yield metrics.

Cyclicality in paperboard and printing-related demand

Cyclicality in paperboard and printing-related demand exposes Clearwater Paper to economic swings: packaging paperboard volumes often track GDP and retail activity, while printing-grade papers face secular decline from digital substitution, pressuring volumes and prices. During downturns mix shifts toward lower-margin packaging or reduced printing runs can compress operating margins and EBITDA, and variable end-market recovery timing makes segment forecasting more difficult.

- Exposure: paperboard tied to cyclical packaging demand

- Secular risk: printing volumes decline with digital substitution

- Margin risk: adverse mix shifts compress margins in downturns

- Forecasting: greater volatility across segments complicates planning

Customer concentration and retailer bargaining power

Large national retailers exert strong bargaining power, pressuring price and terms and compressing margins; Clearwater Paper cites customer concentration risk in its 2024 Form 10-K. Losing a key account would materially reduce volumes and utilization, amplifying fixed-cost exposure. Frequent resets in private-label contracts limit pricing power and can cap margin expansion despite cost initiatives.

- Customer concentration: 2024 Form 10-K flagged material exposure

- Retailer bargaining: aggressive price/terms negotiations

- Key-account risk: disproportionate volume impact if lost

- Private-label pricing: frequent resets cap margins

Pulp surge, weak pricing and $75M capex squeeze margins; customer risk

Volatile pulp/energy costs (pulp ~100% rise in 2021–22; remained elevated into 2024) compress margins; heavy private-label exposure limits pricing power; 2024 capex ~75 million USD raises fixed-cost and downtime risk; 2024 Form 10-K flags material customer concentration, increasing switching and volume risk.

| Metric | 2024 |

|---|---|

| Pulp price change | ~+100% (2021–22, elevated into 2024) |

| Private-label exposure | US PL penetration ~17.5% |

| Capex | ~$75M |

| Customer risk | Material concentration (10‑K) |

Preview Before You Purchase

Clearwater Paper SWOT Analysis

This is a real excerpt from the complete Clearwater Paper SWOT Analysis you'll receive upon purchase. The preview below is taken directly from the full report, professional and structured. Buy now to unlock the entire, editable document for immediate download.

Elevate Your Analysis with the Complete SWOT Report

Clearwater Paper’s SWOT analysis highlights resilient manufacturing capabilities, niche market strength in tissue and pulp, and exposure to commodity cycles and regulatory risk. Discover strategic opportunities and hidden vulnerabilities that could affect valuation and operations. Want the full, editable report with expert insights and Excel tools? Purchase the complete SWOT analysis to plan, pitch, or invest with confidence.

Strengths

Private-label tissue scale with major retailers

Clearwater Paper (NASDAQ: CLW) supplies major retailers and wholesalers, providing channel access and volume stability. Private-label tissue now represents roughly 25% of U.S. retail tissue volume, favoring cost-competitive suppliers like Clearwater. Its scale supports efficient procurement and production, lowering unit costs. Deep retail relationships help secure shelf space and multi-year contracts.

Diversified portfolio: consumer tissue, away-from-home, paperboard

Clearwater Paper’s diversified portfolio spans consumer tissue, away-from-home products and paperboard, smoothing revenue through different demand cycles. Consumer tissue delivers steady, non-discretionary volumes while paperboard captures packaging growth driven by e-commerce and FMCG. Away-from-home channels supply institutional, countercyclical demand streams. This mix reduces reliance on any single revenue source and supports stability in recent years.

Vertical integration in pulp and paperboard

Owning pulp and paperboard assets lowers Clearwater Paper's input risk and strengthens cost control by internalizing raw material supply chains. Vertical integration enables tighter product customization and consistent quality across grades used in consumer and specialty packaging. Internal supply buffers the company against external market shocks and can drive higher operating margins versus pure converters.

Sustainability positioning and fiber stewardship

Clearwater Paper’s sustainability positioning and fiber stewardship align with major retailer ESG mandates and supported its competitive stance in 2024; the company reported roughly $1.2 billion in net sales in 2024 and leverages certifications and responsible sourcing to capture price premiums and win bids. Eco-friendly tissue and recyclable paperboard meet rising consumer demand and strengthen RFP differentiation for long-term contracts.

Reliable supply chain and operational know-how

Clearwater Paper's reliable supply chain and process expertise underpin on-time delivery to big-box and wholesale partners, supporting repeat business and smoother new product introductions; the company reported over $1.8 billion in net sales in FY2024, reflecting strong market traction and operational continuity.

- On-time delivery to big-box/wholesale

- Converting and board production expertise

- Supply reliability builds trust

- Enables faster new product introductions

25% private-label, vertical integration & ESG drive stable margins and $1.83B sales

Clearwater Paper supplies major retailers with strong private-label exposure (≈25% U.S. retail tissue), driving stable volumes and channel access. Scale and vertical integration (own pulp/board) lower input risk and unit costs, supporting margins. Robust ESG certifications and recyclable offerings won RFPs and price premiums; FY2024 net sales ≈ $1.83B, with reliable on-time delivery to big-box partners.

| Metric | Value (2024) |

|---|---|

| Net sales | $1.83B |

| Private-label share | ≈25% |

| Vertical integration | Pulp, paperboard |

| ESG | Certifications driving premiums |

What is included in the product

Provides a concise SWOT overview of Clearwater Paper’s internal strengths and weaknesses and external opportunities and threats, highlighting competitive position, growth drivers, operational gaps, and market risks shaping its strategic outlook.

Delivers a concise SWOT matrix for Clearwater Paper to align strategy quickly; editable format enables rapid updates and seamless integration into reports and presentations for stakeholder decision-making.

Weaknesses

Exposure to commodity pulp and energy volatility

Exposure to commodity pulp and energy volatility can swing Clearwater Paper margins rapidly; pulp prices doubled in 2021–22 and remained elevated into 2024, compressing gross margins. Even with pulp and paperboard integration, market pricing feeds through to profitability. Hedging programs only partially offset short, sharp spikes. Volatility complicates pricing and inventory decisions and raises working-capital risk.

Limited brand equity versus national brands

Clearwater Paper's heavy reliance on private-label production means revenue is tied to retailer brands rather than its own, limiting consumer pull and reducing pricing power; private-label grocery penetration rose to about 17.5% in the US in 2024 (NielsenIQ), highlighting competitive pressure on branded premium pricing.

As a result, differentiation depends mainly on cost efficiency and service reliability instead of marketing-led brand equity, compressing margins when input costs rise.

Switching risk is elevated if large retail customers re-bid contracts or shift volumes to lower-cost suppliers, creating revenue volatility and contract renegotiation exposure.

Capital-intensive mills and maintenance needs

Paper and tissue assets demand ongoing capex—Clearwater Paper spent about $75 million in 2024 on maintenance and upgrades—yet planned downtime for rollovers can interrupt deliveries and service levels. High fixed costs in milling and converting raise operating leverage, making earnings highly volume-sensitive. Several plants date decades old and typically trail best-in-class efficiency and yield metrics.

Cyclicality in paperboard and printing-related demand

Cyclicality in paperboard and printing-related demand exposes Clearwater Paper to economic swings: packaging paperboard volumes often track GDP and retail activity, while printing-grade papers face secular decline from digital substitution, pressuring volumes and prices. During downturns mix shifts toward lower-margin packaging or reduced printing runs can compress operating margins and EBITDA, and variable end-market recovery timing makes segment forecasting more difficult.

- Exposure: paperboard tied to cyclical packaging demand

- Secular risk: printing volumes decline with digital substitution

- Margin risk: adverse mix shifts compress margins in downturns

- Forecasting: greater volatility across segments complicates planning

Customer concentration and retailer bargaining power

Large national retailers exert strong bargaining power, pressuring price and terms and compressing margins; Clearwater Paper cites customer concentration risk in its 2024 Form 10-K. Losing a key account would materially reduce volumes and utilization, amplifying fixed-cost exposure. Frequent resets in private-label contracts limit pricing power and can cap margin expansion despite cost initiatives.

- Customer concentration: 2024 Form 10-K flagged material exposure

- Retailer bargaining: aggressive price/terms negotiations

- Key-account risk: disproportionate volume impact if lost

- Private-label pricing: frequent resets cap margins

Pulp surge, weak pricing and $75M capex squeeze margins; customer risk

Volatile pulp/energy costs (pulp ~100% rise in 2021–22; remained elevated into 2024) compress margins; heavy private-label exposure limits pricing power; 2024 capex ~75 million USD raises fixed-cost and downtime risk; 2024 Form 10-K flags material customer concentration, increasing switching and volume risk.

| Metric | 2024 |

|---|---|

| Pulp price change | ~+100% (2021–22, elevated into 2024) |

| Private-label exposure | US PL penetration ~17.5% |

| Capex | ~$75M |

| Customer risk | Material concentration (10‑K) |

Preview Before You Purchase

Clearwater Paper SWOT Analysis

This is a real excerpt from the complete Clearwater Paper SWOT Analysis you'll receive upon purchase. The preview below is taken directly from the full report, professional and structured. Buy now to unlock the entire, editable document for immediate download.

Description

Elevate Your Analysis with the Complete SWOT Report

Clearwater Paper’s SWOT analysis highlights resilient manufacturing capabilities, niche market strength in tissue and pulp, and exposure to commodity cycles and regulatory risk. Discover strategic opportunities and hidden vulnerabilities that could affect valuation and operations. Want the full, editable report with expert insights and Excel tools? Purchase the complete SWOT analysis to plan, pitch, or invest with confidence.

Strengths

Private-label tissue scale with major retailers

Clearwater Paper (NASDAQ: CLW) supplies major retailers and wholesalers, providing channel access and volume stability. Private-label tissue now represents roughly 25% of U.S. retail tissue volume, favoring cost-competitive suppliers like Clearwater. Its scale supports efficient procurement and production, lowering unit costs. Deep retail relationships help secure shelf space and multi-year contracts.

Diversified portfolio: consumer tissue, away-from-home, paperboard

Clearwater Paper’s diversified portfolio spans consumer tissue, away-from-home products and paperboard, smoothing revenue through different demand cycles. Consumer tissue delivers steady, non-discretionary volumes while paperboard captures packaging growth driven by e-commerce and FMCG. Away-from-home channels supply institutional, countercyclical demand streams. This mix reduces reliance on any single revenue source and supports stability in recent years.

Vertical integration in pulp and paperboard

Owning pulp and paperboard assets lowers Clearwater Paper's input risk and strengthens cost control by internalizing raw material supply chains. Vertical integration enables tighter product customization and consistent quality across grades used in consumer and specialty packaging. Internal supply buffers the company against external market shocks and can drive higher operating margins versus pure converters.

Sustainability positioning and fiber stewardship

Clearwater Paper’s sustainability positioning and fiber stewardship align with major retailer ESG mandates and supported its competitive stance in 2024; the company reported roughly $1.2 billion in net sales in 2024 and leverages certifications and responsible sourcing to capture price premiums and win bids. Eco-friendly tissue and recyclable paperboard meet rising consumer demand and strengthen RFP differentiation for long-term contracts.

Reliable supply chain and operational know-how

Clearwater Paper's reliable supply chain and process expertise underpin on-time delivery to big-box and wholesale partners, supporting repeat business and smoother new product introductions; the company reported over $1.8 billion in net sales in FY2024, reflecting strong market traction and operational continuity.

- On-time delivery to big-box/wholesale

- Converting and board production expertise

- Supply reliability builds trust

- Enables faster new product introductions

25% private-label, vertical integration & ESG drive stable margins and $1.83B sales

Clearwater Paper supplies major retailers with strong private-label exposure (≈25% U.S. retail tissue), driving stable volumes and channel access. Scale and vertical integration (own pulp/board) lower input risk and unit costs, supporting margins. Robust ESG certifications and recyclable offerings won RFPs and price premiums; FY2024 net sales ≈ $1.83B, with reliable on-time delivery to big-box partners.

| Metric | Value (2024) |

|---|---|

| Net sales | $1.83B |

| Private-label share | ≈25% |

| Vertical integration | Pulp, paperboard |

| ESG | Certifications driving premiums |

What is included in the product

Provides a concise SWOT overview of Clearwater Paper’s internal strengths and weaknesses and external opportunities and threats, highlighting competitive position, growth drivers, operational gaps, and market risks shaping its strategic outlook.

Delivers a concise SWOT matrix for Clearwater Paper to align strategy quickly; editable format enables rapid updates and seamless integration into reports and presentations for stakeholder decision-making.

Weaknesses

Exposure to commodity pulp and energy volatility

Exposure to commodity pulp and energy volatility can swing Clearwater Paper margins rapidly; pulp prices doubled in 2021–22 and remained elevated into 2024, compressing gross margins. Even with pulp and paperboard integration, market pricing feeds through to profitability. Hedging programs only partially offset short, sharp spikes. Volatility complicates pricing and inventory decisions and raises working-capital risk.

Limited brand equity versus national brands

Clearwater Paper's heavy reliance on private-label production means revenue is tied to retailer brands rather than its own, limiting consumer pull and reducing pricing power; private-label grocery penetration rose to about 17.5% in the US in 2024 (NielsenIQ), highlighting competitive pressure on branded premium pricing.

As a result, differentiation depends mainly on cost efficiency and service reliability instead of marketing-led brand equity, compressing margins when input costs rise.

Switching risk is elevated if large retail customers re-bid contracts or shift volumes to lower-cost suppliers, creating revenue volatility and contract renegotiation exposure.

Capital-intensive mills and maintenance needs

Paper and tissue assets demand ongoing capex—Clearwater Paper spent about $75 million in 2024 on maintenance and upgrades—yet planned downtime for rollovers can interrupt deliveries and service levels. High fixed costs in milling and converting raise operating leverage, making earnings highly volume-sensitive. Several plants date decades old and typically trail best-in-class efficiency and yield metrics.

Cyclicality in paperboard and printing-related demand

Cyclicality in paperboard and printing-related demand exposes Clearwater Paper to economic swings: packaging paperboard volumes often track GDP and retail activity, while printing-grade papers face secular decline from digital substitution, pressuring volumes and prices. During downturns mix shifts toward lower-margin packaging or reduced printing runs can compress operating margins and EBITDA, and variable end-market recovery timing makes segment forecasting more difficult.

- Exposure: paperboard tied to cyclical packaging demand

- Secular risk: printing volumes decline with digital substitution

- Margin risk: adverse mix shifts compress margins in downturns

- Forecasting: greater volatility across segments complicates planning

Customer concentration and retailer bargaining power

Large national retailers exert strong bargaining power, pressuring price and terms and compressing margins; Clearwater Paper cites customer concentration risk in its 2024 Form 10-K. Losing a key account would materially reduce volumes and utilization, amplifying fixed-cost exposure. Frequent resets in private-label contracts limit pricing power and can cap margin expansion despite cost initiatives.

- Customer concentration: 2024 Form 10-K flagged material exposure

- Retailer bargaining: aggressive price/terms negotiations

- Key-account risk: disproportionate volume impact if lost

- Private-label pricing: frequent resets cap margins

Pulp surge, weak pricing and $75M capex squeeze margins; customer risk

Volatile pulp/energy costs (pulp ~100% rise in 2021–22; remained elevated into 2024) compress margins; heavy private-label exposure limits pricing power; 2024 capex ~75 million USD raises fixed-cost and downtime risk; 2024 Form 10-K flags material customer concentration, increasing switching and volume risk.

| Metric | 2024 |

|---|---|

| Pulp price change | ~+100% (2021–22, elevated into 2024) |

| Private-label exposure | US PL penetration ~17.5% |

| Capex | ~$75M |

| Customer risk | Material concentration (10‑K) |

Preview Before You Purchase

Clearwater Paper SWOT Analysis

This is a real excerpt from the complete Clearwater Paper SWOT Analysis you'll receive upon purchase. The preview below is taken directly from the full report, professional and structured. Buy now to unlock the entire, editable document for immediate download.