Clyde Bergemann GmbH Porter's Five Forces Analysis

From Overview to Strategy Blueprint

Clyde Bergemann GmbH faces moderate supplier power, differentiated technology reducing buyer bargaining, and industry rivalry driven by aftermarket services; threat of new entrants is low but substitutes in energy transition could rise. This snapshot highlights strategic pressure points and opportunity areas. The complete Porter's Five Forces Analysis unpacks each force with ratings, visuals, and actionable implications. Purchase the full report to inform investment or strategic moves.

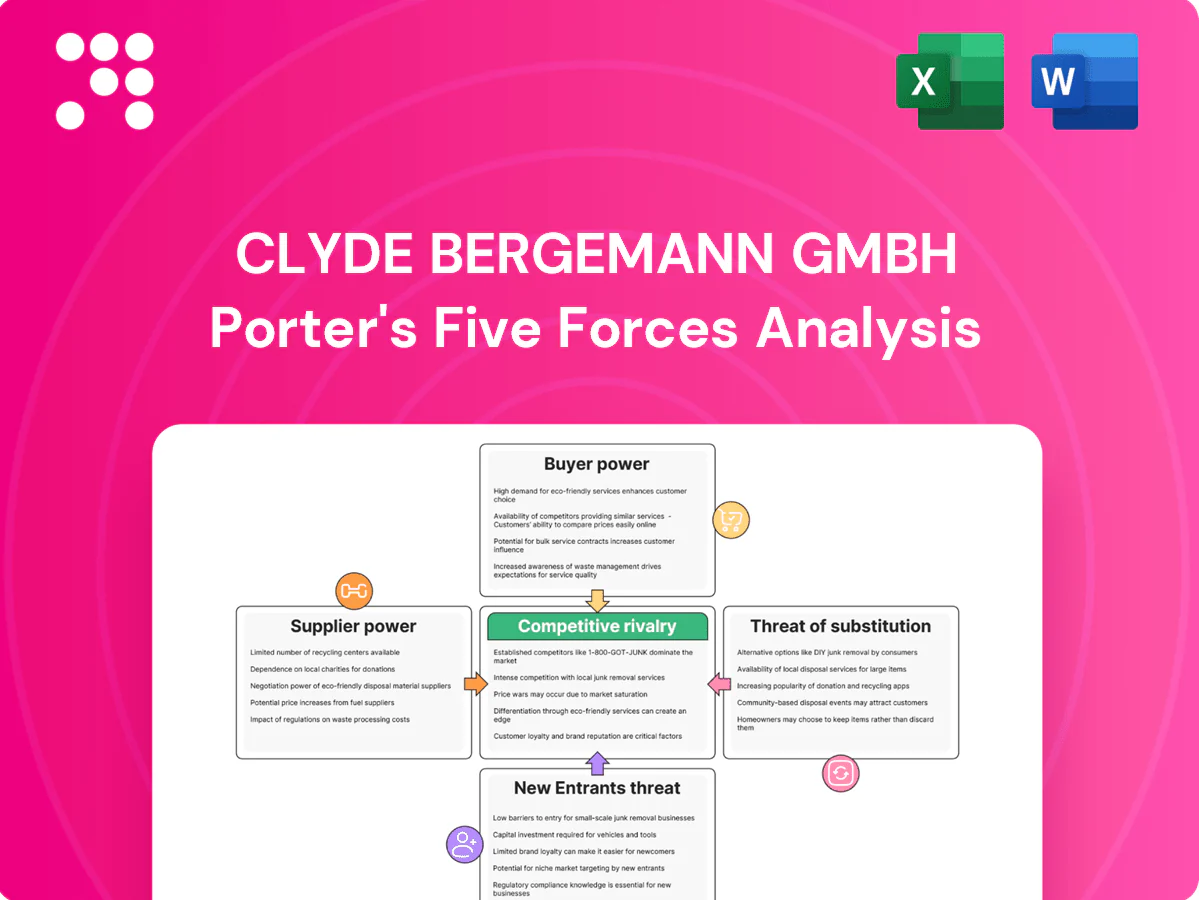

Suppliers Bargaining Power

Specialized alloy and component dependence

High-temperature alloys, precision actuators and control electronics for Clyde Bergemann are concentrated among few qualified suppliers, giving those vendors outsized leverage. In 2024 qualification and traceability cycles typically exceed 9 months, further narrowing alternatives and enabling price pass-through pressure. Resultant lead times often stretch 6–12 months, and dual-sourcing mitigations exist but are frequently constrained by stringent specifications and certification demands.

Custom fabrication and machining capacity

Large engineered-to-order vessels and lances require certified fabricators with niche capabilities, concentrating supply among fewer qualified shops and increasing supplier leverage.

Capacity tightness in heavy fabrication—with industry lead times often stretching beyond 16–20 weeks in 2024—shifts bargaining power to fabricators.

Project timeline pressures and penalties magnify this risk for Clyde Bergemann, while long-term framework agreements can lock in capacity and stabilize pricing and delivery terms.

Digital/PLC and sensor ecosystem lock-ins

Integration with specific PLCs, sensors and drives creates vendor lock-in for Clyde Bergemann, as the global PLC market was valued at about USD 12.4 billion in 2024, concentrating bargaining power among leading suppliers. Firmware and proprietary protocols limit switching and can raise lifecycle spares and upgrade costs by a material margin. Suppliers thus can influence total cost of ownership; open-architecture designs reduce but do not eliminate exposure.

Energy and logistics cost pass-through

Suppliers in metals and fabrication face significant energy and freight volatility; energy represented roughly 25-35% of metalmakers' variable costs in 2024 (World Steel Association), so indexation clauses commonly pass price swings through to Clyde Bergemann. Global supply-chain disruptions in 2023–24 tightened availability, raising lead times. Buffer inventories (3–6 months) and regional sourcing have emerged as primary hedges.

- energy exposure: ~25–35% of costs (2024)

- indexation shifts cost upstream

- lead-time pressure from 2023–24 disruptions

- hedges: 3–6 months inventory, regional sourcing

IP and proprietary sub-assemblies

Clyde Bergemann faces heightened supplier power where certain nozzles, valves and acoustic sub‑assemblies are protected by IP and supplied by niche vendors, with limited substitutes for critical performance parts. Qualification of alternates commonly takes 9–18 months, extending switching costs and operational risk. Over time design‑for‑substitutability can lower dependency and reduce single‑source exposure.

- High supplier power: proprietary parts, limited substitutes

- Switching cost: qualification 9–18 months

- Concentration risk: niche vendors control critical IP

- Mitigation: design for substitutability, alternate qualification

Concentrated suppliers, >9-month quals and 25–35% energy risk

Supplier power is high due to concentrated vendors for high‑temp alloys, actuators and niche fabricators. Qualification cycles exceed 9 months and lead times 6–12 months, raising switching costs. Energy volatility (25–35% of metalmakers' variable costs in 2024) and PLC market concentration (USD 12.4bn in 2024) enable price pass‑through. Long‑term frameworks and DfS reduce but do not eliminate risk.

| Metric | 2024 value | Impact |

|---|---|---|

| Qualification time | >9 months | High switching cost |

| Lead times | 6–12 months (components), 16–20+ weeks (fabrication) | Schedule risk |

| Energy share | 25–35% | Price pass‑through |

| PLC market | USD 12.4bn | Vendor concentration |

What is included in the product

Provides a tailored Porter’s Five Forces assessment for Clyde Bergemann GmbH, highlighting competitive intensity, supplier and buyer power, threat of substitutes and new entrants, and emerging disruptive risks; includes strategic implications to inform pricing, market positioning and defensive barriers.

A concise one-sheet Porter's Five Forces for Clyde Bergemann GmbH that highlights supplier/customer leverage, competitive rivalry, entrant threats and substitutes to speed strategic decisions and risk mitigation. Slide-ready, customizable pressure levels and clean layout make it easy to drop into board decks or operational planning.

Customers Bargaining Power

Concentrated, savvy industrial buyers

Concentrated, savvy industrial buyers—utilities, EPCs and large process plants—purchase in sizable, infrequent lots often exceeding €10m and run competitive tenders, giving them strong leverage. Professional procurement teams routinely extract 5–10% price concessions and push tougher terms. Buyers benchmark globally on TCO and warranties spanning 10–25 years. Volume discounts and reputation risk further heighten buyer power.

High switching costs but measurable outcomes

Installed-base integration, DCS tie-ins and performance guarantees create high switching frictions for Clyde Bergemann GmbH, but buyers can quantify cleaning efficiency (typically 0.5–1.5% heat-rate gains), emissions cuts and fuel savings, enabling hard negotiations; with EU carbon prices near €90–100/ton in 2024 these measurable gains translate to clear ROI. Performance-based contracts shift operational risk and proven ROI often offsets vendor price pressure.

Aftermarket leverage on spares and service

Aftermarket spares, nozzles and maintenance represent Clyde Bergemann’s key profit pools as buyers press multi-year service discounts and strict availability SLAs; since 2024 customers increasingly use framework agreements to bundle sites and extract concessions, while growing demand for predictive service offerings provides a defensible premium by shifting value from reactive spare sales to uptime guarantees.

Qualification and code compliance demands

Customers demand strict safety, environmental and QA certifications (eg ISO 9001, ISO 14001, TÜV) which create formal qualification gates that lengthen sales cycles and let buyers delay or split awards; failure to meet these codes risks outright disqualification and lost revenue. Strong audit readiness by suppliers narrows buyer options and shifts leverage toward certified vendors.

- Qualification gates increase procurement timelines

- Non-compliance = disqualification risk

- Audit readiness concentrates buyer choice

Project risk allocation and financing terms

Customers push liquidated damages, warranty extensions and performance bonds—commonly 5–10% of contract value in 2024—shifting risk and raising suppliers’ capital costs; payment milestones and 5–15% retention schedules tighten cash flow and can increase working capital needs by mid-single digits.

Industrial buyers secure 5-10% cuts as €90-100/ton carbon lifts ROI and bargaining power

Concentrated industrial buyers (utilities, EPCs) run global tenders and secure 5–10% price concessions, leveraging measurable efficiency gains; EU carbon ~€90–100/ton in 2024 increases ROI visibility and bargaining. High switching frictions from integration and warranties limit exits, but aftermarket/service discounting and strict SLAs keep buyer power elevated.

| Metric | 2024 Value |

|---|---|

| Buyer price concession | 5–10% |

| EU carbon | €90–100/ton |

| Liquidated damages | 5–10% contract |

| Retention | 5–15% |

Preview the Actual Deliverable

Clyde Bergemann GmbH Porter's Five Forces Analysis

This Porter's Five Forces analysis of Clyde Bergemann GmbH assesses competitive rivalry, supplier and buyer power, threats of new entrants and substitutes, and strategic implications for market positioning. This preview is the exact, fully formatted document you’ll receive immediately after purchase.

From Overview to Strategy Blueprint

Clyde Bergemann GmbH faces moderate supplier power, differentiated technology reducing buyer bargaining, and industry rivalry driven by aftermarket services; threat of new entrants is low but substitutes in energy transition could rise. This snapshot highlights strategic pressure points and opportunity areas. The complete Porter's Five Forces Analysis unpacks each force with ratings, visuals, and actionable implications. Purchase the full report to inform investment or strategic moves.

Suppliers Bargaining Power

Specialized alloy and component dependence

High-temperature alloys, precision actuators and control electronics for Clyde Bergemann are concentrated among few qualified suppliers, giving those vendors outsized leverage. In 2024 qualification and traceability cycles typically exceed 9 months, further narrowing alternatives and enabling price pass-through pressure. Resultant lead times often stretch 6–12 months, and dual-sourcing mitigations exist but are frequently constrained by stringent specifications and certification demands.

Custom fabrication and machining capacity

Large engineered-to-order vessels and lances require certified fabricators with niche capabilities, concentrating supply among fewer qualified shops and increasing supplier leverage.

Capacity tightness in heavy fabrication—with industry lead times often stretching beyond 16–20 weeks in 2024—shifts bargaining power to fabricators.

Project timeline pressures and penalties magnify this risk for Clyde Bergemann, while long-term framework agreements can lock in capacity and stabilize pricing and delivery terms.

Digital/PLC and sensor ecosystem lock-ins

Integration with specific PLCs, sensors and drives creates vendor lock-in for Clyde Bergemann, as the global PLC market was valued at about USD 12.4 billion in 2024, concentrating bargaining power among leading suppliers. Firmware and proprietary protocols limit switching and can raise lifecycle spares and upgrade costs by a material margin. Suppliers thus can influence total cost of ownership; open-architecture designs reduce but do not eliminate exposure.

Energy and logistics cost pass-through

Suppliers in metals and fabrication face significant energy and freight volatility; energy represented roughly 25-35% of metalmakers' variable costs in 2024 (World Steel Association), so indexation clauses commonly pass price swings through to Clyde Bergemann. Global supply-chain disruptions in 2023–24 tightened availability, raising lead times. Buffer inventories (3–6 months) and regional sourcing have emerged as primary hedges.

- energy exposure: ~25–35% of costs (2024)

- indexation shifts cost upstream

- lead-time pressure from 2023–24 disruptions

- hedges: 3–6 months inventory, regional sourcing

IP and proprietary sub-assemblies

Clyde Bergemann faces heightened supplier power where certain nozzles, valves and acoustic sub‑assemblies are protected by IP and supplied by niche vendors, with limited substitutes for critical performance parts. Qualification of alternates commonly takes 9–18 months, extending switching costs and operational risk. Over time design‑for‑substitutability can lower dependency and reduce single‑source exposure.

- High supplier power: proprietary parts, limited substitutes

- Switching cost: qualification 9–18 months

- Concentration risk: niche vendors control critical IP

- Mitigation: design for substitutability, alternate qualification

Concentrated suppliers, >9-month quals and 25–35% energy risk

Supplier power is high due to concentrated vendors for high‑temp alloys, actuators and niche fabricators. Qualification cycles exceed 9 months and lead times 6–12 months, raising switching costs. Energy volatility (25–35% of metalmakers' variable costs in 2024) and PLC market concentration (USD 12.4bn in 2024) enable price pass‑through. Long‑term frameworks and DfS reduce but do not eliminate risk.

| Metric | 2024 value | Impact |

|---|---|---|

| Qualification time | >9 months | High switching cost |

| Lead times | 6–12 months (components), 16–20+ weeks (fabrication) | Schedule risk |

| Energy share | 25–35% | Price pass‑through |

| PLC market | USD 12.4bn | Vendor concentration |

What is included in the product

Provides a tailored Porter’s Five Forces assessment for Clyde Bergemann GmbH, highlighting competitive intensity, supplier and buyer power, threat of substitutes and new entrants, and emerging disruptive risks; includes strategic implications to inform pricing, market positioning and defensive barriers.

A concise one-sheet Porter's Five Forces for Clyde Bergemann GmbH that highlights supplier/customer leverage, competitive rivalry, entrant threats and substitutes to speed strategic decisions and risk mitigation. Slide-ready, customizable pressure levels and clean layout make it easy to drop into board decks or operational planning.

Customers Bargaining Power

Concentrated, savvy industrial buyers

Concentrated, savvy industrial buyers—utilities, EPCs and large process plants—purchase in sizable, infrequent lots often exceeding €10m and run competitive tenders, giving them strong leverage. Professional procurement teams routinely extract 5–10% price concessions and push tougher terms. Buyers benchmark globally on TCO and warranties spanning 10–25 years. Volume discounts and reputation risk further heighten buyer power.

High switching costs but measurable outcomes

Installed-base integration, DCS tie-ins and performance guarantees create high switching frictions for Clyde Bergemann GmbH, but buyers can quantify cleaning efficiency (typically 0.5–1.5% heat-rate gains), emissions cuts and fuel savings, enabling hard negotiations; with EU carbon prices near €90–100/ton in 2024 these measurable gains translate to clear ROI. Performance-based contracts shift operational risk and proven ROI often offsets vendor price pressure.

Aftermarket leverage on spares and service

Aftermarket spares, nozzles and maintenance represent Clyde Bergemann’s key profit pools as buyers press multi-year service discounts and strict availability SLAs; since 2024 customers increasingly use framework agreements to bundle sites and extract concessions, while growing demand for predictive service offerings provides a defensible premium by shifting value from reactive spare sales to uptime guarantees.

Qualification and code compliance demands

Customers demand strict safety, environmental and QA certifications (eg ISO 9001, ISO 14001, TÜV) which create formal qualification gates that lengthen sales cycles and let buyers delay or split awards; failure to meet these codes risks outright disqualification and lost revenue. Strong audit readiness by suppliers narrows buyer options and shifts leverage toward certified vendors.

- Qualification gates increase procurement timelines

- Non-compliance = disqualification risk

- Audit readiness concentrates buyer choice

Project risk allocation and financing terms

Customers push liquidated damages, warranty extensions and performance bonds—commonly 5–10% of contract value in 2024—shifting risk and raising suppliers’ capital costs; payment milestones and 5–15% retention schedules tighten cash flow and can increase working capital needs by mid-single digits.

Industrial buyers secure 5-10% cuts as €90-100/ton carbon lifts ROI and bargaining power

Concentrated industrial buyers (utilities, EPCs) run global tenders and secure 5–10% price concessions, leveraging measurable efficiency gains; EU carbon ~€90–100/ton in 2024 increases ROI visibility and bargaining. High switching frictions from integration and warranties limit exits, but aftermarket/service discounting and strict SLAs keep buyer power elevated.

| Metric | 2024 Value |

|---|---|

| Buyer price concession | 5–10% |

| EU carbon | €90–100/ton |

| Liquidated damages | 5–10% contract |

| Retention | 5–15% |

Preview the Actual Deliverable

Clyde Bergemann GmbH Porter's Five Forces Analysis

This Porter's Five Forces analysis of Clyde Bergemann GmbH assesses competitive rivalry, supplier and buyer power, threats of new entrants and substitutes, and strategic implications for market positioning. This preview is the exact, fully formatted document you’ll receive immediately after purchase.

Description

From Overview to Strategy Blueprint

Clyde Bergemann GmbH faces moderate supplier power, differentiated technology reducing buyer bargaining, and industry rivalry driven by aftermarket services; threat of new entrants is low but substitutes in energy transition could rise. This snapshot highlights strategic pressure points and opportunity areas. The complete Porter's Five Forces Analysis unpacks each force with ratings, visuals, and actionable implications. Purchase the full report to inform investment or strategic moves.

Suppliers Bargaining Power

Specialized alloy and component dependence

High-temperature alloys, precision actuators and control electronics for Clyde Bergemann are concentrated among few qualified suppliers, giving those vendors outsized leverage. In 2024 qualification and traceability cycles typically exceed 9 months, further narrowing alternatives and enabling price pass-through pressure. Resultant lead times often stretch 6–12 months, and dual-sourcing mitigations exist but are frequently constrained by stringent specifications and certification demands.

Custom fabrication and machining capacity

Large engineered-to-order vessels and lances require certified fabricators with niche capabilities, concentrating supply among fewer qualified shops and increasing supplier leverage.

Capacity tightness in heavy fabrication—with industry lead times often stretching beyond 16–20 weeks in 2024—shifts bargaining power to fabricators.

Project timeline pressures and penalties magnify this risk for Clyde Bergemann, while long-term framework agreements can lock in capacity and stabilize pricing and delivery terms.

Digital/PLC and sensor ecosystem lock-ins

Integration with specific PLCs, sensors and drives creates vendor lock-in for Clyde Bergemann, as the global PLC market was valued at about USD 12.4 billion in 2024, concentrating bargaining power among leading suppliers. Firmware and proprietary protocols limit switching and can raise lifecycle spares and upgrade costs by a material margin. Suppliers thus can influence total cost of ownership; open-architecture designs reduce but do not eliminate exposure.

Energy and logistics cost pass-through

Suppliers in metals and fabrication face significant energy and freight volatility; energy represented roughly 25-35% of metalmakers' variable costs in 2024 (World Steel Association), so indexation clauses commonly pass price swings through to Clyde Bergemann. Global supply-chain disruptions in 2023–24 tightened availability, raising lead times. Buffer inventories (3–6 months) and regional sourcing have emerged as primary hedges.

- energy exposure: ~25–35% of costs (2024)

- indexation shifts cost upstream

- lead-time pressure from 2023–24 disruptions

- hedges: 3–6 months inventory, regional sourcing

IP and proprietary sub-assemblies

Clyde Bergemann faces heightened supplier power where certain nozzles, valves and acoustic sub‑assemblies are protected by IP and supplied by niche vendors, with limited substitutes for critical performance parts. Qualification of alternates commonly takes 9–18 months, extending switching costs and operational risk. Over time design‑for‑substitutability can lower dependency and reduce single‑source exposure.

- High supplier power: proprietary parts, limited substitutes

- Switching cost: qualification 9–18 months

- Concentration risk: niche vendors control critical IP

- Mitigation: design for substitutability, alternate qualification

Concentrated suppliers, >9-month quals and 25–35% energy risk

Supplier power is high due to concentrated vendors for high‑temp alloys, actuators and niche fabricators. Qualification cycles exceed 9 months and lead times 6–12 months, raising switching costs. Energy volatility (25–35% of metalmakers' variable costs in 2024) and PLC market concentration (USD 12.4bn in 2024) enable price pass‑through. Long‑term frameworks and DfS reduce but do not eliminate risk.

| Metric | 2024 value | Impact |

|---|---|---|

| Qualification time | >9 months | High switching cost |

| Lead times | 6–12 months (components), 16–20+ weeks (fabrication) | Schedule risk |

| Energy share | 25–35% | Price pass‑through |

| PLC market | USD 12.4bn | Vendor concentration |

What is included in the product

Provides a tailored Porter’s Five Forces assessment for Clyde Bergemann GmbH, highlighting competitive intensity, supplier and buyer power, threat of substitutes and new entrants, and emerging disruptive risks; includes strategic implications to inform pricing, market positioning and defensive barriers.

A concise one-sheet Porter's Five Forces for Clyde Bergemann GmbH that highlights supplier/customer leverage, competitive rivalry, entrant threats and substitutes to speed strategic decisions and risk mitigation. Slide-ready, customizable pressure levels and clean layout make it easy to drop into board decks or operational planning.

Customers Bargaining Power

Concentrated, savvy industrial buyers

Concentrated, savvy industrial buyers—utilities, EPCs and large process plants—purchase in sizable, infrequent lots often exceeding €10m and run competitive tenders, giving them strong leverage. Professional procurement teams routinely extract 5–10% price concessions and push tougher terms. Buyers benchmark globally on TCO and warranties spanning 10–25 years. Volume discounts and reputation risk further heighten buyer power.

High switching costs but measurable outcomes

Installed-base integration, DCS tie-ins and performance guarantees create high switching frictions for Clyde Bergemann GmbH, but buyers can quantify cleaning efficiency (typically 0.5–1.5% heat-rate gains), emissions cuts and fuel savings, enabling hard negotiations; with EU carbon prices near €90–100/ton in 2024 these measurable gains translate to clear ROI. Performance-based contracts shift operational risk and proven ROI often offsets vendor price pressure.

Aftermarket leverage on spares and service

Aftermarket spares, nozzles and maintenance represent Clyde Bergemann’s key profit pools as buyers press multi-year service discounts and strict availability SLAs; since 2024 customers increasingly use framework agreements to bundle sites and extract concessions, while growing demand for predictive service offerings provides a defensible premium by shifting value from reactive spare sales to uptime guarantees.

Qualification and code compliance demands

Customers demand strict safety, environmental and QA certifications (eg ISO 9001, ISO 14001, TÜV) which create formal qualification gates that lengthen sales cycles and let buyers delay or split awards; failure to meet these codes risks outright disqualification and lost revenue. Strong audit readiness by suppliers narrows buyer options and shifts leverage toward certified vendors.

- Qualification gates increase procurement timelines

- Non-compliance = disqualification risk

- Audit readiness concentrates buyer choice

Project risk allocation and financing terms

Customers push liquidated damages, warranty extensions and performance bonds—commonly 5–10% of contract value in 2024—shifting risk and raising suppliers’ capital costs; payment milestones and 5–15% retention schedules tighten cash flow and can increase working capital needs by mid-single digits.

Industrial buyers secure 5-10% cuts as €90-100/ton carbon lifts ROI and bargaining power

Concentrated industrial buyers (utilities, EPCs) run global tenders and secure 5–10% price concessions, leveraging measurable efficiency gains; EU carbon ~€90–100/ton in 2024 increases ROI visibility and bargaining. High switching frictions from integration and warranties limit exits, but aftermarket/service discounting and strict SLAs keep buyer power elevated.

| Metric | 2024 Value |

|---|---|

| Buyer price concession | 5–10% |

| EU carbon | €90–100/ton |

| Liquidated damages | 5–10% contract |

| Retention | 5–15% |

Preview the Actual Deliverable

Clyde Bergemann GmbH Porter's Five Forces Analysis

This Porter's Five Forces analysis of Clyde Bergemann GmbH assesses competitive rivalry, supplier and buyer power, threats of new entrants and substitutes, and strategic implications for market positioning. This preview is the exact, fully formatted document you’ll receive immediately after purchase.