CMS Info Systems Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

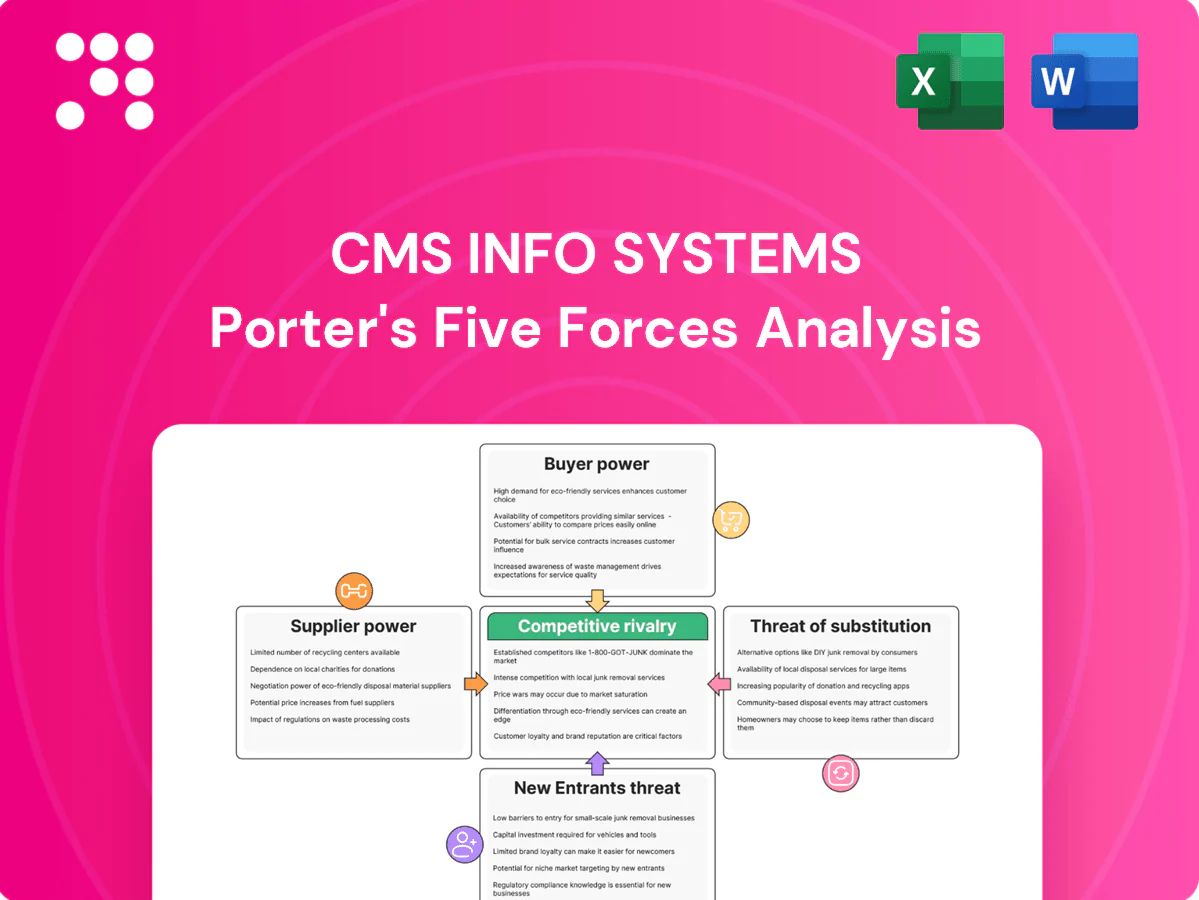

CMS Info Systems faces moderate supplier power, intense buyer negotiation in logistics contracts, and rising rivalry as digital warehousing attracts new entrants; substitutes and regulatory shifts add strategic complexity. This snapshot highlights key pressure points but only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy to inform investment or business decisions.

Suppliers Bargaining Power

ATM and equipment OEM dependence

Specialized OEMs for ATMs, cash recyclers, safes and sensors exert moderate supplier power because certification, PCI and local compliance requirements raise switching costs. Multi-year maintenance and spares contracts, typically spanning 3–5 years, can lock in pricing and service terms. CMS mitigates risk via multi-sourcing and scale-driven volume discounts. Any supply disruption can reduce ATM uptime and trigger SLA penalties and customer claim exposure.

Armored fleet, fuel, and vehicle suppliers

Vehicles, armor kits, and fuel are widely available, keeping supplier power low to moderate; industry reports in 2024 show compliance-grade armoring can add roughly 15–25% to vehicle costs, pressuring margins. Rising fuel costs (Brent averaging near 85–95 USD/bbl in early 2024) further squeeze margins, though scale purchasing and route optimization (fleet utilization gains of 5–10%) improve bargaining leverage. Long-term fleet vendors still retain influence on delivery timelines, with specialized armoring lead times often 4–8 weeks.

Cash processing tech and software vendors

Counting machines, note sorters, counterfeit detectors and analytics software come from specialized vendors, creating integration, certification and data-security frictions that raise switching costs for CMS Info Systems. CMS’s in-house technology and custom tooling reduce dependence on third-party suppliers and allow tighter operational control. Vendor bargaining power stays moderate, rising only where proprietary algorithms or mandatory certifications are decisive.

Security manpower agencies

Guarding and crew staffing are partly sourced from manpower agencies; tight labor markets and PSARA-driven training/vetting increase supplier leverage, though CMS’s brand and steady cash-management demand reduce reliance on agencies and improve direct recruitment. Unionization or regional shortages can still spike supplier power episodically.

- Partial outsourcing to agencies

- Compliance (training/vetting) raises costs

- CMS brand lowers agency dependence

- Union/region shortages cause episodic pressure

Currency chest and facility services

Access to RBI-regulated currency chests and compliant processing facilities is essential for cash logistics; facility vendors (vaults, surveillance, cash rooms) must meet strict RBI and security standards, which narrows alternatives. CMS’s national footprint and 2024 compliance track record strengthen its negotiating position, though regulatory constraints can indirectly raise supplier bargaining power by limiting supplier choice.

- RBI-regulated empanelment limits suppliers

- High compliance standards raise switching costs

- CMS national scale improves terms (2024)

Armoring adds +15–25%, CMS scale cuts fleet costs 5–10%

Specialized ATM OEMs, certified vendors and RBI-compliant facilities give suppliers moderate power due to certification, integration and 3–5 year maintenance contracts. Armoring adds ~15–25% to vehicle costs; Brent averaged ~85–95 USD/bbl in early 2024, pressuring fuel costs. CMS scale and multi-sourcing yield ~5–10% fleet savings and reduce disruption risk.

| Metric | Value (2024) |

|---|---|

| Maintenance contracts | 3–5 yrs |

| Armoring premium | +15–25% |

| Brent oil | 85–95 USD/bbl |

| Fleet savings | 5–10% |

What is included in the product

Tailored Porter's Five Forces analysis for CMS Info Systems uncovering competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and regulatory/disruption risks; includes strategic implications for pricing, margin protection, and growth defense.

A single-sheet Porter's Five Forces for CMS Info Systems that visualizes competitive pressures with an instant spider chart and lets you customize scenarios (regulation, new entrants, pricing shifts) for quick decision-making and deck-ready summaries.

Customers Bargaining Power

Concentrated banking clientele

Banks, NBFCs and payment firms run centralized tenders worth INR billions annually (2024), using scale and multi‑year contracts to exert strong price pressure. CMS mitigates this through a nationwide network and broad service mix—cash logistics, ATM services and reconciliation—that supports large incumbency advantages. Still, continued buyer consolidation among top banks/payment players sustains high bargaining power.

Price-sensitive RFPs and SLAs

In 2024 procurement for CMS Info Systems remained highly competitive with strict SLAs and penalties; buyers increasingly benchmarked vendors on uptime, cash losses and cost per route, amplifying negotiation leverage and driving rate compression. Performance differentiation (fewer cash losses, higher uptime) can command modest premiums, but measurable gaps are narrow and sustain only limited margin upside.

Switching costs and integration frictions

Operational switching disrupts routes, reconciliations and system integrations, often requiring phased transitions that typically span 6–18 months in 2024. Compliance re-onboarding and field retraining add measurable friction, moderating buyer power and raising implementation costs. Staggered cutovers allow partial continuity, preserving service but extending switching timelines. Net effect: medium switching cost that limits yet does not eliminate buyer leverage.

Service breadth and bundled value

CMS Info Systems bundles ATM cash, first/second-line maintenance, retail cash pick-up and analytics, reducing per-unit price transparency and deepening client lock-in; FY2024 consolidated revenue reported at INR 4,267 crore underscores scale that supports bundled offerings and cross-selling, which lowers buyer bargaining power for multi-service contracts while buyers accept efficiency gains at the cost of optionality.

- Bundling reduces transparency, raises switching costs

- Scale (FY2024 revenue INR 4,267 crore) enables cross-sell

- Buyers gain efficiency but lose optionality, weakening leverage

Regional reach and last-mile coverage

CMS Info Systems’ deep Tier-2/3/4 reach reduces alternative options for buyers in remote areas, shrinking choice and lowering buyer bargaining power outside metros; as of FY2024 CMS operated over 2,000 customer touchpoints across non-metro India, strengthening pricing leverage.

In metros, dense vendor presence restores buyer power, but CMS’s network density outside metros balances these dynamics in its favor.

- FY2024: 2,000+ non-metro touchpoints

- Low-density areas: fewer vendor alternatives → lower buyer power

- Metros: higher vendor count → increased buyer leverage

Metro leverage high; INR 4,267 crore, 2,000+ touchpoints, 6–18 months switching = medium bargaining power

In 2024 centralized bank/NBFC tenders (INR billions) and strict SLAs kept buyer leverage high in metros, but CMS’s FY2024 revenue of INR 4,267 crore and 2,000+ non‑metro touchpoints reduced alternatives and limited buyer power; switching takes 6–18 months, so net bargaining power = medium. Performance gaps allow small premiums but sustain rate compression overall.

| Metric | 2024 |

|---|---|

| CMS revenue | INR 4,267 crore |

| Non‑metro touchpoints | 2,000+ |

| Switching timeline | 6–18 months |

What You See Is What You Get

CMS Info Systems Porter's Five Forces Analysis

This preview displays the exact CMS Info Systems Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is fully formatted, professionally written, and ready for download and use the moment you complete your payment. What you see is what you get.

A Must-Have Tool for Decision-Makers

CMS Info Systems faces moderate supplier power, intense buyer negotiation in logistics contracts, and rising rivalry as digital warehousing attracts new entrants; substitutes and regulatory shifts add strategic complexity. This snapshot highlights key pressure points but only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy to inform investment or business decisions.

Suppliers Bargaining Power

ATM and equipment OEM dependence

Specialized OEMs for ATMs, cash recyclers, safes and sensors exert moderate supplier power because certification, PCI and local compliance requirements raise switching costs. Multi-year maintenance and spares contracts, typically spanning 3–5 years, can lock in pricing and service terms. CMS mitigates risk via multi-sourcing and scale-driven volume discounts. Any supply disruption can reduce ATM uptime and trigger SLA penalties and customer claim exposure.

Armored fleet, fuel, and vehicle suppliers

Vehicles, armor kits, and fuel are widely available, keeping supplier power low to moderate; industry reports in 2024 show compliance-grade armoring can add roughly 15–25% to vehicle costs, pressuring margins. Rising fuel costs (Brent averaging near 85–95 USD/bbl in early 2024) further squeeze margins, though scale purchasing and route optimization (fleet utilization gains of 5–10%) improve bargaining leverage. Long-term fleet vendors still retain influence on delivery timelines, with specialized armoring lead times often 4–8 weeks.

Cash processing tech and software vendors

Counting machines, note sorters, counterfeit detectors and analytics software come from specialized vendors, creating integration, certification and data-security frictions that raise switching costs for CMS Info Systems. CMS’s in-house technology and custom tooling reduce dependence on third-party suppliers and allow tighter operational control. Vendor bargaining power stays moderate, rising only where proprietary algorithms or mandatory certifications are decisive.

Security manpower agencies

Guarding and crew staffing are partly sourced from manpower agencies; tight labor markets and PSARA-driven training/vetting increase supplier leverage, though CMS’s brand and steady cash-management demand reduce reliance on agencies and improve direct recruitment. Unionization or regional shortages can still spike supplier power episodically.

- Partial outsourcing to agencies

- Compliance (training/vetting) raises costs

- CMS brand lowers agency dependence

- Union/region shortages cause episodic pressure

Currency chest and facility services

Access to RBI-regulated currency chests and compliant processing facilities is essential for cash logistics; facility vendors (vaults, surveillance, cash rooms) must meet strict RBI and security standards, which narrows alternatives. CMS’s national footprint and 2024 compliance track record strengthen its negotiating position, though regulatory constraints can indirectly raise supplier bargaining power by limiting supplier choice.

- RBI-regulated empanelment limits suppliers

- High compliance standards raise switching costs

- CMS national scale improves terms (2024)

Armoring adds +15–25%, CMS scale cuts fleet costs 5–10%

Specialized ATM OEMs, certified vendors and RBI-compliant facilities give suppliers moderate power due to certification, integration and 3–5 year maintenance contracts. Armoring adds ~15–25% to vehicle costs; Brent averaged ~85–95 USD/bbl in early 2024, pressuring fuel costs. CMS scale and multi-sourcing yield ~5–10% fleet savings and reduce disruption risk.

| Metric | Value (2024) |

|---|---|

| Maintenance contracts | 3–5 yrs |

| Armoring premium | +15–25% |

| Brent oil | 85–95 USD/bbl |

| Fleet savings | 5–10% |

What is included in the product

Tailored Porter's Five Forces analysis for CMS Info Systems uncovering competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and regulatory/disruption risks; includes strategic implications for pricing, margin protection, and growth defense.

A single-sheet Porter's Five Forces for CMS Info Systems that visualizes competitive pressures with an instant spider chart and lets you customize scenarios (regulation, new entrants, pricing shifts) for quick decision-making and deck-ready summaries.

Customers Bargaining Power

Concentrated banking clientele

Banks, NBFCs and payment firms run centralized tenders worth INR billions annually (2024), using scale and multi‑year contracts to exert strong price pressure. CMS mitigates this through a nationwide network and broad service mix—cash logistics, ATM services and reconciliation—that supports large incumbency advantages. Still, continued buyer consolidation among top banks/payment players sustains high bargaining power.

Price-sensitive RFPs and SLAs

In 2024 procurement for CMS Info Systems remained highly competitive with strict SLAs and penalties; buyers increasingly benchmarked vendors on uptime, cash losses and cost per route, amplifying negotiation leverage and driving rate compression. Performance differentiation (fewer cash losses, higher uptime) can command modest premiums, but measurable gaps are narrow and sustain only limited margin upside.

Switching costs and integration frictions

Operational switching disrupts routes, reconciliations and system integrations, often requiring phased transitions that typically span 6–18 months in 2024. Compliance re-onboarding and field retraining add measurable friction, moderating buyer power and raising implementation costs. Staggered cutovers allow partial continuity, preserving service but extending switching timelines. Net effect: medium switching cost that limits yet does not eliminate buyer leverage.

Service breadth and bundled value

CMS Info Systems bundles ATM cash, first/second-line maintenance, retail cash pick-up and analytics, reducing per-unit price transparency and deepening client lock-in; FY2024 consolidated revenue reported at INR 4,267 crore underscores scale that supports bundled offerings and cross-selling, which lowers buyer bargaining power for multi-service contracts while buyers accept efficiency gains at the cost of optionality.

- Bundling reduces transparency, raises switching costs

- Scale (FY2024 revenue INR 4,267 crore) enables cross-sell

- Buyers gain efficiency but lose optionality, weakening leverage

Regional reach and last-mile coverage

CMS Info Systems’ deep Tier-2/3/4 reach reduces alternative options for buyers in remote areas, shrinking choice and lowering buyer bargaining power outside metros; as of FY2024 CMS operated over 2,000 customer touchpoints across non-metro India, strengthening pricing leverage.

In metros, dense vendor presence restores buyer power, but CMS’s network density outside metros balances these dynamics in its favor.

- FY2024: 2,000+ non-metro touchpoints

- Low-density areas: fewer vendor alternatives → lower buyer power

- Metros: higher vendor count → increased buyer leverage

Metro leverage high; INR 4,267 crore, 2,000+ touchpoints, 6–18 months switching = medium bargaining power

In 2024 centralized bank/NBFC tenders (INR billions) and strict SLAs kept buyer leverage high in metros, but CMS’s FY2024 revenue of INR 4,267 crore and 2,000+ non‑metro touchpoints reduced alternatives and limited buyer power; switching takes 6–18 months, so net bargaining power = medium. Performance gaps allow small premiums but sustain rate compression overall.

| Metric | 2024 |

|---|---|

| CMS revenue | INR 4,267 crore |

| Non‑metro touchpoints | 2,000+ |

| Switching timeline | 6–18 months |

What You See Is What You Get

CMS Info Systems Porter's Five Forces Analysis

This preview displays the exact CMS Info Systems Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is fully formatted, professionally written, and ready for download and use the moment you complete your payment. What you see is what you get.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

CMS Info Systems faces moderate supplier power, intense buyer negotiation in logistics contracts, and rising rivalry as digital warehousing attracts new entrants; substitutes and regulatory shifts add strategic complexity. This snapshot highlights key pressure points but only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy to inform investment or business decisions.

Suppliers Bargaining Power

ATM and equipment OEM dependence

Specialized OEMs for ATMs, cash recyclers, safes and sensors exert moderate supplier power because certification, PCI and local compliance requirements raise switching costs. Multi-year maintenance and spares contracts, typically spanning 3–5 years, can lock in pricing and service terms. CMS mitigates risk via multi-sourcing and scale-driven volume discounts. Any supply disruption can reduce ATM uptime and trigger SLA penalties and customer claim exposure.

Armored fleet, fuel, and vehicle suppliers

Vehicles, armor kits, and fuel are widely available, keeping supplier power low to moderate; industry reports in 2024 show compliance-grade armoring can add roughly 15–25% to vehicle costs, pressuring margins. Rising fuel costs (Brent averaging near 85–95 USD/bbl in early 2024) further squeeze margins, though scale purchasing and route optimization (fleet utilization gains of 5–10%) improve bargaining leverage. Long-term fleet vendors still retain influence on delivery timelines, with specialized armoring lead times often 4–8 weeks.

Cash processing tech and software vendors

Counting machines, note sorters, counterfeit detectors and analytics software come from specialized vendors, creating integration, certification and data-security frictions that raise switching costs for CMS Info Systems. CMS’s in-house technology and custom tooling reduce dependence on third-party suppliers and allow tighter operational control. Vendor bargaining power stays moderate, rising only where proprietary algorithms or mandatory certifications are decisive.

Security manpower agencies

Guarding and crew staffing are partly sourced from manpower agencies; tight labor markets and PSARA-driven training/vetting increase supplier leverage, though CMS’s brand and steady cash-management demand reduce reliance on agencies and improve direct recruitment. Unionization or regional shortages can still spike supplier power episodically.

- Partial outsourcing to agencies

- Compliance (training/vetting) raises costs

- CMS brand lowers agency dependence

- Union/region shortages cause episodic pressure

Currency chest and facility services

Access to RBI-regulated currency chests and compliant processing facilities is essential for cash logistics; facility vendors (vaults, surveillance, cash rooms) must meet strict RBI and security standards, which narrows alternatives. CMS’s national footprint and 2024 compliance track record strengthen its negotiating position, though regulatory constraints can indirectly raise supplier bargaining power by limiting supplier choice.

- RBI-regulated empanelment limits suppliers

- High compliance standards raise switching costs

- CMS national scale improves terms (2024)

Armoring adds +15–25%, CMS scale cuts fleet costs 5–10%

Specialized ATM OEMs, certified vendors and RBI-compliant facilities give suppliers moderate power due to certification, integration and 3–5 year maintenance contracts. Armoring adds ~15–25% to vehicle costs; Brent averaged ~85–95 USD/bbl in early 2024, pressuring fuel costs. CMS scale and multi-sourcing yield ~5–10% fleet savings and reduce disruption risk.

| Metric | Value (2024) |

|---|---|

| Maintenance contracts | 3–5 yrs |

| Armoring premium | +15–25% |

| Brent oil | 85–95 USD/bbl |

| Fleet savings | 5–10% |

What is included in the product

Tailored Porter's Five Forces analysis for CMS Info Systems uncovering competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and regulatory/disruption risks; includes strategic implications for pricing, margin protection, and growth defense.

A single-sheet Porter's Five Forces for CMS Info Systems that visualizes competitive pressures with an instant spider chart and lets you customize scenarios (regulation, new entrants, pricing shifts) for quick decision-making and deck-ready summaries.

Customers Bargaining Power

Concentrated banking clientele

Banks, NBFCs and payment firms run centralized tenders worth INR billions annually (2024), using scale and multi‑year contracts to exert strong price pressure. CMS mitigates this through a nationwide network and broad service mix—cash logistics, ATM services and reconciliation—that supports large incumbency advantages. Still, continued buyer consolidation among top banks/payment players sustains high bargaining power.

Price-sensitive RFPs and SLAs

In 2024 procurement for CMS Info Systems remained highly competitive with strict SLAs and penalties; buyers increasingly benchmarked vendors on uptime, cash losses and cost per route, amplifying negotiation leverage and driving rate compression. Performance differentiation (fewer cash losses, higher uptime) can command modest premiums, but measurable gaps are narrow and sustain only limited margin upside.

Switching costs and integration frictions

Operational switching disrupts routes, reconciliations and system integrations, often requiring phased transitions that typically span 6–18 months in 2024. Compliance re-onboarding and field retraining add measurable friction, moderating buyer power and raising implementation costs. Staggered cutovers allow partial continuity, preserving service but extending switching timelines. Net effect: medium switching cost that limits yet does not eliminate buyer leverage.

Service breadth and bundled value

CMS Info Systems bundles ATM cash, first/second-line maintenance, retail cash pick-up and analytics, reducing per-unit price transparency and deepening client lock-in; FY2024 consolidated revenue reported at INR 4,267 crore underscores scale that supports bundled offerings and cross-selling, which lowers buyer bargaining power for multi-service contracts while buyers accept efficiency gains at the cost of optionality.

- Bundling reduces transparency, raises switching costs

- Scale (FY2024 revenue INR 4,267 crore) enables cross-sell

- Buyers gain efficiency but lose optionality, weakening leverage

Regional reach and last-mile coverage

CMS Info Systems’ deep Tier-2/3/4 reach reduces alternative options for buyers in remote areas, shrinking choice and lowering buyer bargaining power outside metros; as of FY2024 CMS operated over 2,000 customer touchpoints across non-metro India, strengthening pricing leverage.

In metros, dense vendor presence restores buyer power, but CMS’s network density outside metros balances these dynamics in its favor.

- FY2024: 2,000+ non-metro touchpoints

- Low-density areas: fewer vendor alternatives → lower buyer power

- Metros: higher vendor count → increased buyer leverage

Metro leverage high; INR 4,267 crore, 2,000+ touchpoints, 6–18 months switching = medium bargaining power

In 2024 centralized bank/NBFC tenders (INR billions) and strict SLAs kept buyer leverage high in metros, but CMS’s FY2024 revenue of INR 4,267 crore and 2,000+ non‑metro touchpoints reduced alternatives and limited buyer power; switching takes 6–18 months, so net bargaining power = medium. Performance gaps allow small premiums but sustain rate compression overall.

| Metric | 2024 |

|---|---|

| CMS revenue | INR 4,267 crore |

| Non‑metro touchpoints | 2,000+ |

| Switching timeline | 6–18 months |

What You See Is What You Get

CMS Info Systems Porter's Five Forces Analysis

This preview displays the exact CMS Info Systems Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is fully formatted, professionally written, and ready for download and use the moment you complete your payment. What you see is what you get.