CMS Info Systems PESTLE Analysis

Your Competitive Advantage Starts with This Report

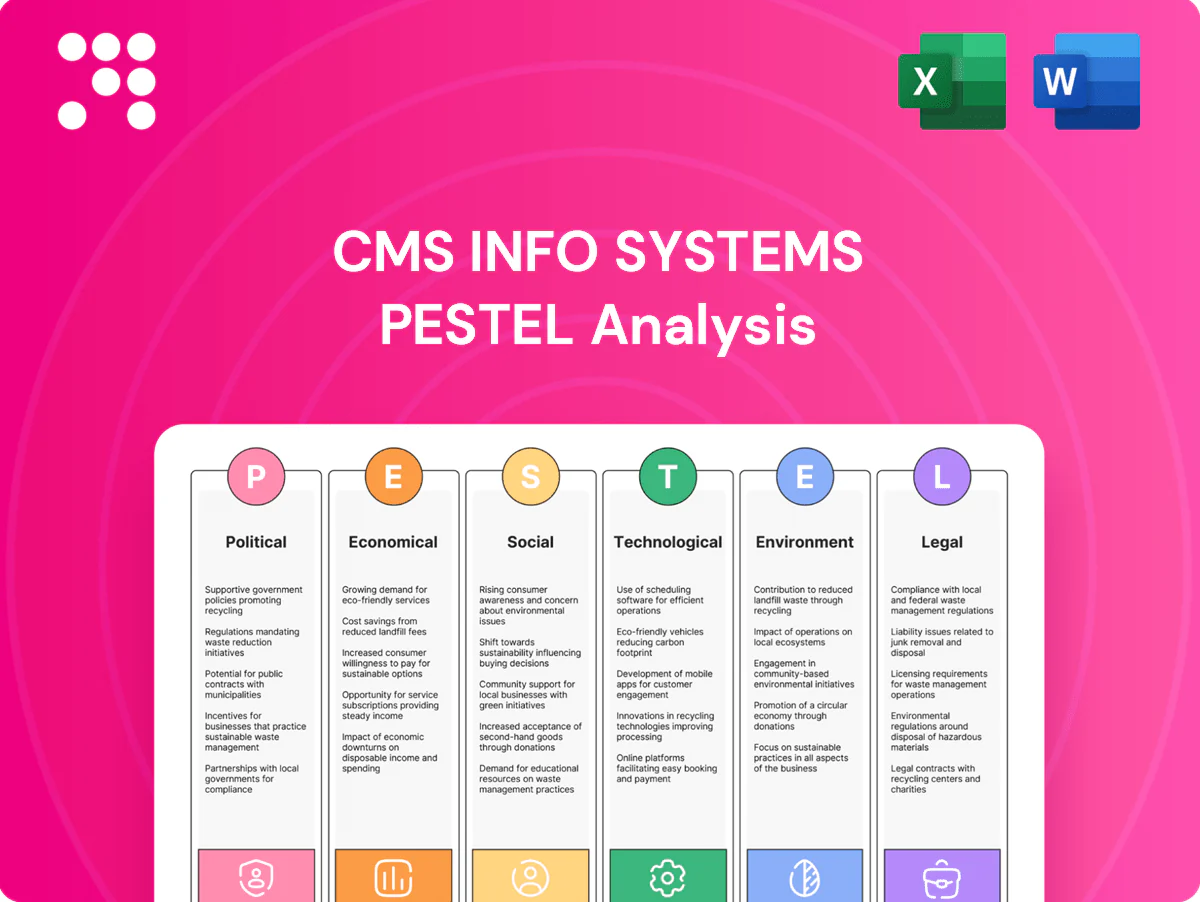

Gain a strategic edge with our PESTLE Analysis of CMS Info Systems—exploring political, economic, social, technological, legal and environmental forces shaping its future. Ready-made, actionable and editable; buy the full report now for instant, boardroom-ready insights.

Political factors

Government stance on cash vs. digital

CMS sits between cash logistics and digital rails, so policy nudges matter: currency in circulation remained around ₹36 lakh crore in 2024 while UPI volumes surged, crossing tens of billions annually, strengthening digital uptake but not displacing cash entirely.

Financial inclusion mandates keep cash demand in rural and semi‑urban India, supporting ATM networks that handle large cash loads despite UPI growth.

A policy tilt favoring digital-only settlements would risk compressing ATM volumes and CMS margins, so balanced support for cash continuity plus UPI sustains core revenues.

RBI oversight and public-sector banking priorities

RBI directives shape ATM uptime, cassette-swap and cash-handling protocols, imposing service-level norms that CMS must meet to serve banks' networks; RBI oversight has driven technical standards since 2017. Public-sector banks, controlling roughly 60% of branches, set budgets and ATM strategies that determine route density and volumes. A push for rural outreach increases dispersed routes and costs, while policy nudges for ATM rationalization could compress deployment footprints and shift cash logistics demand.

Law-and-order and internal security

Cash-in-transit operations depend on secure routes and predictable policing, especially with currency in circulation at roughly 36.3 lakh crore INR as of March 2024 (RBI). State-level policing effectiveness drives theft risk and can materially raise insurance premiums and claims exposure. Political stability in sensitive regions cuts operational disruptions and route rerouting costs. The 2024 general election increased scrutiny and permit requirements, tightening cash movement windows.

Public procurement and tender dynamics

Government-linked banks and agencies award large tenders that set pricing norms, often forcing bidders like CMS Info Systems to compete primarily on price rather than service differentiation, squeezing EBITDA margins.

Tender templates that prioritize lowest cost over lifecycle value increase risk of underpriced contracts; local content/MSME reservation clauses shift subcontracting patterns and supplier mix.

Policy-driven SLAs and compliance requirements raise capex and IT spend for secure cash logistics and vault upgrades, increasing fixed-cost intensity.

- Pricing pressure from government tenders

- Lowest-cost bias harms margins

- Local content/MSME rules affect subcontracting

- SLAs raise compliance and capex needs

Infrastructure and logistics policy

Transport and fuel policies materially affect CMS fleet economics, with fuel representing roughly 30–35% of cash operating cost and pump prices in 2024 averaging about 100 INR/litre for petrol in major metros. Highway expansion under Bharatmala Phase I targets ~34,800 km by 2025, improving route efficiency and SLA adherence, while urban traffic rules and congestion pricing influence delivery times. State tolls and city entry curfews can add 5–15% to transit time and per-trip costs; armored-vehicle safety mandates set by regulators raise capex and compliance spending.

- Fuel share ~30–35% of fleet Opex

- Bharatmala ~34,800 km by 2025

- City rules may add 5–15% delay

- Tolls add variable INR 50–500 per trip

- Safety mandates increase capex/compliance

Policy nudges keep cash+digital rails; currency 36.3 lakh crore, PSU ATM ~60%

Policy nudges sustain dual cash/digital rails: currency in circulation ~36.3 lakh crore (Mar 2024) while UPI volumes surged, preserving ATM demand. RBI SLAs, PSU bank ATM share ~60% and tender low-cost bias press margins and raise compliance capex. Fuel (30–35% fleet Opex) and Bharatmala (~34,800 km by 2025) affect route efficiency and costs.

| Factor | Metric | 2024/25 |

|---|---|---|

| Currency | In circulation | 36.3 lakh crore INR (Mar 2024) |

| Bank share | PSU branches | ~60% |

| Fuel | Fleet Opex | 30–35% |

What is included in the product

Explores how external macro-environmental factors uniquely affect CMS Info Systems across six dimensions: Political, Economic, Social, Technological, Environmental, and Legal. Backed by current data and forward-looking insights, the analysis helps executives, investors, and strategists identify region- and industry-specific threats, opportunities, and scenario-ready actions.

Visually segmented by PESTLE categories for rapid interpretation, the CMS Info Systems PESTLE summary offers a concise, shareable format that can be dropped into presentations or strategy sessions to streamline discussions on external risks and market positioning.

Economic factors

Cash in circulation and ATM throughput

India’s currency-in-circulation (~₹36 lakh crore as of 2024–25) sets CMS Info Systems’ replenishment frequency and cassette loads, with CMS servicing over 60,000 ATMs and retail outlets for cash pickup and processing. High retail cash use sustains steady demand; seasonal festivals and monthly salary cycles raise throughput by 20–30% at peak. Any sustained decline in cash would compress route density and lower revenue per stop.

GDP growth and retail footprint

Rising GDP — IMF pegged India growth near 7.2% for 2024–25 — and expansion of organized retail (organized share ~14%) and bank outlets increases CMS Info Systems serviceable locations, lifting ATM and cash logistics reach. Strong growth drives higher transaction volumes and demand for ancillary managed services, supporting fee income. Slower growth constrains new ATM deployments and pushes fee renegotiations. Regional disparities in retail density and per-ATM usage (India has ~210,000 ATMs) shape route profitability.

Inflation, fuel, and wage costs

Fuel price swings (Brent averaged about $83/bbl in 2024) directly lift CMS fleet OPEX and compress route margins, raising per-km costs and passthrough pressure.

Wage inflation for custodians, drivers and guards, against India’s CPI of 5.1% in FY2023-24, pushes fixed staff costs higher and pressures margins.

Index-linked contracts and productivity tech (telematics, route optimization) can offset some increases, but lag effects keep margins volatile.

Insurance premiums trend upward with claim frequency and inflation; Indian non-life premium growth remained elevated in 2023-24, sustaining cost pressure.

Interest rates and client capex cycles

Bank capex for ATM upgrades, recyclers and automation is highly rate-sensitive: with India’s ATM network at ~220,000 machines (2024) and the RBI policy rate near 6.5% (July 2025), higher rates often delay bank deployments and contract renegotiations, while lower rates enable network expansion and outsourcing growth; tighter liquidity also lifts working-capital costs for cash centres.

- ATM footprint: ~220,000 (2024)

- Policy rate: ~6.5% (Jul 2025)

- Higher rates = delayed deployments/renegotiations

- Tighter liquidity = higher cash-centre working capital

Digital payments cannibalization and complementarity

Rapid UPI growth—about 20% YoY to roughly 25 billion monthly transactions by H1 2025 per NPCI—is reducing small-ticket cash use but cash-heavy segments (rural, micro-retail) persist; CMS can pivot to recyclers, cash-to-digital bridges and transaction analytics to capture value. Mixed-mode ecosystems stabilize volumes across cycles, though over-rotation to digital may force service re-pricing and new revenue models.

- UPI ~25B/month H1 2025 (NPCI)

- Cash coexistence: rural/micro-retail resilient

- CMS pivots: recyclers, cash-digital bridges, analytics

- Mixed-mode stabilizes volumes

- Risk: digital over-rotation → service re-pricing

Policy nudges keep cash+digital rails; currency 36.3 lakh crore, PSU ATM ~60%

India cash stock ~₹36 lakh crore (2024–25) and CMS’s 60,000+ serviced outlets tie replenishment cadence to cash demand; festivals/salary cycles spike throughput 20–30%. GDP ~7.2% (IMF 2024–25) and ~220,000 ATMs (2024) expand serviceable reach; higher rates (policy ~6.5% Jul 2025) and fuel (~$83/bbl 2024) raise OPEX; UPI ~25B/mo H1 2025 shifts small-ticket away from cash.

| Metric | Value |

|---|---|

| Currency in circulation | ₹36 lakh crore (2024–25) |

| ATMs | ~220,000 (2024) |

| Policy rate | ~6.5% (Jul 2025) |

| UPI | ~25B/mo (H1 2025) |

| Brent | ~$83/bbl (2024) |

What You See Is What You Get

CMS Info Systems PESTLE Analysis

The preview shown here is the exact CMS Info Systems PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. This is the real, final file with complete content and structure, not a teaser or placeholder. After payment you’ll be able to download this same professionally structured document immediately.

Your Competitive Advantage Starts with This Report

Gain a strategic edge with our PESTLE Analysis of CMS Info Systems—exploring political, economic, social, technological, legal and environmental forces shaping its future. Ready-made, actionable and editable; buy the full report now for instant, boardroom-ready insights.

Political factors

Government stance on cash vs. digital

CMS sits between cash logistics and digital rails, so policy nudges matter: currency in circulation remained around ₹36 lakh crore in 2024 while UPI volumes surged, crossing tens of billions annually, strengthening digital uptake but not displacing cash entirely.

Financial inclusion mandates keep cash demand in rural and semi‑urban India, supporting ATM networks that handle large cash loads despite UPI growth.

A policy tilt favoring digital-only settlements would risk compressing ATM volumes and CMS margins, so balanced support for cash continuity plus UPI sustains core revenues.

RBI oversight and public-sector banking priorities

RBI directives shape ATM uptime, cassette-swap and cash-handling protocols, imposing service-level norms that CMS must meet to serve banks' networks; RBI oversight has driven technical standards since 2017. Public-sector banks, controlling roughly 60% of branches, set budgets and ATM strategies that determine route density and volumes. A push for rural outreach increases dispersed routes and costs, while policy nudges for ATM rationalization could compress deployment footprints and shift cash logistics demand.

Law-and-order and internal security

Cash-in-transit operations depend on secure routes and predictable policing, especially with currency in circulation at roughly 36.3 lakh crore INR as of March 2024 (RBI). State-level policing effectiveness drives theft risk and can materially raise insurance premiums and claims exposure. Political stability in sensitive regions cuts operational disruptions and route rerouting costs. The 2024 general election increased scrutiny and permit requirements, tightening cash movement windows.

Public procurement and tender dynamics

Government-linked banks and agencies award large tenders that set pricing norms, often forcing bidders like CMS Info Systems to compete primarily on price rather than service differentiation, squeezing EBITDA margins.

Tender templates that prioritize lowest cost over lifecycle value increase risk of underpriced contracts; local content/MSME reservation clauses shift subcontracting patterns and supplier mix.

Policy-driven SLAs and compliance requirements raise capex and IT spend for secure cash logistics and vault upgrades, increasing fixed-cost intensity.

- Pricing pressure from government tenders

- Lowest-cost bias harms margins

- Local content/MSME rules affect subcontracting

- SLAs raise compliance and capex needs

Infrastructure and logistics policy

Transport and fuel policies materially affect CMS fleet economics, with fuel representing roughly 30–35% of cash operating cost and pump prices in 2024 averaging about 100 INR/litre for petrol in major metros. Highway expansion under Bharatmala Phase I targets ~34,800 km by 2025, improving route efficiency and SLA adherence, while urban traffic rules and congestion pricing influence delivery times. State tolls and city entry curfews can add 5–15% to transit time and per-trip costs; armored-vehicle safety mandates set by regulators raise capex and compliance spending.

- Fuel share ~30–35% of fleet Opex

- Bharatmala ~34,800 km by 2025

- City rules may add 5–15% delay

- Tolls add variable INR 50–500 per trip

- Safety mandates increase capex/compliance

Policy nudges keep cash+digital rails; currency 36.3 lakh crore, PSU ATM ~60%

Policy nudges sustain dual cash/digital rails: currency in circulation ~36.3 lakh crore (Mar 2024) while UPI volumes surged, preserving ATM demand. RBI SLAs, PSU bank ATM share ~60% and tender low-cost bias press margins and raise compliance capex. Fuel (30–35% fleet Opex) and Bharatmala (~34,800 km by 2025) affect route efficiency and costs.

| Factor | Metric | 2024/25 |

|---|---|---|

| Currency | In circulation | 36.3 lakh crore INR (Mar 2024) |

| Bank share | PSU branches | ~60% |

| Fuel | Fleet Opex | 30–35% |

What is included in the product

Explores how external macro-environmental factors uniquely affect CMS Info Systems across six dimensions: Political, Economic, Social, Technological, Environmental, and Legal. Backed by current data and forward-looking insights, the analysis helps executives, investors, and strategists identify region- and industry-specific threats, opportunities, and scenario-ready actions.

Visually segmented by PESTLE categories for rapid interpretation, the CMS Info Systems PESTLE summary offers a concise, shareable format that can be dropped into presentations or strategy sessions to streamline discussions on external risks and market positioning.

Economic factors

Cash in circulation and ATM throughput

India’s currency-in-circulation (~₹36 lakh crore as of 2024–25) sets CMS Info Systems’ replenishment frequency and cassette loads, with CMS servicing over 60,000 ATMs and retail outlets for cash pickup and processing. High retail cash use sustains steady demand; seasonal festivals and monthly salary cycles raise throughput by 20–30% at peak. Any sustained decline in cash would compress route density and lower revenue per stop.

GDP growth and retail footprint

Rising GDP — IMF pegged India growth near 7.2% for 2024–25 — and expansion of organized retail (organized share ~14%) and bank outlets increases CMS Info Systems serviceable locations, lifting ATM and cash logistics reach. Strong growth drives higher transaction volumes and demand for ancillary managed services, supporting fee income. Slower growth constrains new ATM deployments and pushes fee renegotiations. Regional disparities in retail density and per-ATM usage (India has ~210,000 ATMs) shape route profitability.

Inflation, fuel, and wage costs

Fuel price swings (Brent averaged about $83/bbl in 2024) directly lift CMS fleet OPEX and compress route margins, raising per-km costs and passthrough pressure.

Wage inflation for custodians, drivers and guards, against India’s CPI of 5.1% in FY2023-24, pushes fixed staff costs higher and pressures margins.

Index-linked contracts and productivity tech (telematics, route optimization) can offset some increases, but lag effects keep margins volatile.

Insurance premiums trend upward with claim frequency and inflation; Indian non-life premium growth remained elevated in 2023-24, sustaining cost pressure.

Interest rates and client capex cycles

Bank capex for ATM upgrades, recyclers and automation is highly rate-sensitive: with India’s ATM network at ~220,000 machines (2024) and the RBI policy rate near 6.5% (July 2025), higher rates often delay bank deployments and contract renegotiations, while lower rates enable network expansion and outsourcing growth; tighter liquidity also lifts working-capital costs for cash centres.

- ATM footprint: ~220,000 (2024)

- Policy rate: ~6.5% (Jul 2025)

- Higher rates = delayed deployments/renegotiations

- Tighter liquidity = higher cash-centre working capital

Digital payments cannibalization and complementarity

Rapid UPI growth—about 20% YoY to roughly 25 billion monthly transactions by H1 2025 per NPCI—is reducing small-ticket cash use but cash-heavy segments (rural, micro-retail) persist; CMS can pivot to recyclers, cash-to-digital bridges and transaction analytics to capture value. Mixed-mode ecosystems stabilize volumes across cycles, though over-rotation to digital may force service re-pricing and new revenue models.

- UPI ~25B/month H1 2025 (NPCI)

- Cash coexistence: rural/micro-retail resilient

- CMS pivots: recyclers, cash-digital bridges, analytics

- Mixed-mode stabilizes volumes

- Risk: digital over-rotation → service re-pricing

Policy nudges keep cash+digital rails; currency 36.3 lakh crore, PSU ATM ~60%

India cash stock ~₹36 lakh crore (2024–25) and CMS’s 60,000+ serviced outlets tie replenishment cadence to cash demand; festivals/salary cycles spike throughput 20–30%. GDP ~7.2% (IMF 2024–25) and ~220,000 ATMs (2024) expand serviceable reach; higher rates (policy ~6.5% Jul 2025) and fuel (~$83/bbl 2024) raise OPEX; UPI ~25B/mo H1 2025 shifts small-ticket away from cash.

| Metric | Value |

|---|---|

| Currency in circulation | ₹36 lakh crore (2024–25) |

| ATMs | ~220,000 (2024) |

| Policy rate | ~6.5% (Jul 2025) |

| UPI | ~25B/mo (H1 2025) |

| Brent | ~$83/bbl (2024) |

What You See Is What You Get

CMS Info Systems PESTLE Analysis

The preview shown here is the exact CMS Info Systems PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. This is the real, final file with complete content and structure, not a teaser or placeholder. After payment you’ll be able to download this same professionally structured document immediately.

Description

Your Competitive Advantage Starts with This Report

Gain a strategic edge with our PESTLE Analysis of CMS Info Systems—exploring political, economic, social, technological, legal and environmental forces shaping its future. Ready-made, actionable and editable; buy the full report now for instant, boardroom-ready insights.

Political factors

Government stance on cash vs. digital

CMS sits between cash logistics and digital rails, so policy nudges matter: currency in circulation remained around ₹36 lakh crore in 2024 while UPI volumes surged, crossing tens of billions annually, strengthening digital uptake but not displacing cash entirely.

Financial inclusion mandates keep cash demand in rural and semi‑urban India, supporting ATM networks that handle large cash loads despite UPI growth.

A policy tilt favoring digital-only settlements would risk compressing ATM volumes and CMS margins, so balanced support for cash continuity plus UPI sustains core revenues.

RBI oversight and public-sector banking priorities

RBI directives shape ATM uptime, cassette-swap and cash-handling protocols, imposing service-level norms that CMS must meet to serve banks' networks; RBI oversight has driven technical standards since 2017. Public-sector banks, controlling roughly 60% of branches, set budgets and ATM strategies that determine route density and volumes. A push for rural outreach increases dispersed routes and costs, while policy nudges for ATM rationalization could compress deployment footprints and shift cash logistics demand.

Law-and-order and internal security

Cash-in-transit operations depend on secure routes and predictable policing, especially with currency in circulation at roughly 36.3 lakh crore INR as of March 2024 (RBI). State-level policing effectiveness drives theft risk and can materially raise insurance premiums and claims exposure. Political stability in sensitive regions cuts operational disruptions and route rerouting costs. The 2024 general election increased scrutiny and permit requirements, tightening cash movement windows.

Public procurement and tender dynamics

Government-linked banks and agencies award large tenders that set pricing norms, often forcing bidders like CMS Info Systems to compete primarily on price rather than service differentiation, squeezing EBITDA margins.

Tender templates that prioritize lowest cost over lifecycle value increase risk of underpriced contracts; local content/MSME reservation clauses shift subcontracting patterns and supplier mix.

Policy-driven SLAs and compliance requirements raise capex and IT spend for secure cash logistics and vault upgrades, increasing fixed-cost intensity.

- Pricing pressure from government tenders

- Lowest-cost bias harms margins

- Local content/MSME rules affect subcontracting

- SLAs raise compliance and capex needs

Infrastructure and logistics policy

Transport and fuel policies materially affect CMS fleet economics, with fuel representing roughly 30–35% of cash operating cost and pump prices in 2024 averaging about 100 INR/litre for petrol in major metros. Highway expansion under Bharatmala Phase I targets ~34,800 km by 2025, improving route efficiency and SLA adherence, while urban traffic rules and congestion pricing influence delivery times. State tolls and city entry curfews can add 5–15% to transit time and per-trip costs; armored-vehicle safety mandates set by regulators raise capex and compliance spending.

- Fuel share ~30–35% of fleet Opex

- Bharatmala ~34,800 km by 2025

- City rules may add 5–15% delay

- Tolls add variable INR 50–500 per trip

- Safety mandates increase capex/compliance

Policy nudges keep cash+digital rails; currency 36.3 lakh crore, PSU ATM ~60%

Policy nudges sustain dual cash/digital rails: currency in circulation ~36.3 lakh crore (Mar 2024) while UPI volumes surged, preserving ATM demand. RBI SLAs, PSU bank ATM share ~60% and tender low-cost bias press margins and raise compliance capex. Fuel (30–35% fleet Opex) and Bharatmala (~34,800 km by 2025) affect route efficiency and costs.

| Factor | Metric | 2024/25 |

|---|---|---|

| Currency | In circulation | 36.3 lakh crore INR (Mar 2024) |

| Bank share | PSU branches | ~60% |

| Fuel | Fleet Opex | 30–35% |

What is included in the product

Explores how external macro-environmental factors uniquely affect CMS Info Systems across six dimensions: Political, Economic, Social, Technological, Environmental, and Legal. Backed by current data and forward-looking insights, the analysis helps executives, investors, and strategists identify region- and industry-specific threats, opportunities, and scenario-ready actions.

Visually segmented by PESTLE categories for rapid interpretation, the CMS Info Systems PESTLE summary offers a concise, shareable format that can be dropped into presentations or strategy sessions to streamline discussions on external risks and market positioning.

Economic factors

Cash in circulation and ATM throughput

India’s currency-in-circulation (~₹36 lakh crore as of 2024–25) sets CMS Info Systems’ replenishment frequency and cassette loads, with CMS servicing over 60,000 ATMs and retail outlets for cash pickup and processing. High retail cash use sustains steady demand; seasonal festivals and monthly salary cycles raise throughput by 20–30% at peak. Any sustained decline in cash would compress route density and lower revenue per stop.

GDP growth and retail footprint

Rising GDP — IMF pegged India growth near 7.2% for 2024–25 — and expansion of organized retail (organized share ~14%) and bank outlets increases CMS Info Systems serviceable locations, lifting ATM and cash logistics reach. Strong growth drives higher transaction volumes and demand for ancillary managed services, supporting fee income. Slower growth constrains new ATM deployments and pushes fee renegotiations. Regional disparities in retail density and per-ATM usage (India has ~210,000 ATMs) shape route profitability.

Inflation, fuel, and wage costs

Fuel price swings (Brent averaged about $83/bbl in 2024) directly lift CMS fleet OPEX and compress route margins, raising per-km costs and passthrough pressure.

Wage inflation for custodians, drivers and guards, against India’s CPI of 5.1% in FY2023-24, pushes fixed staff costs higher and pressures margins.

Index-linked contracts and productivity tech (telematics, route optimization) can offset some increases, but lag effects keep margins volatile.

Insurance premiums trend upward with claim frequency and inflation; Indian non-life premium growth remained elevated in 2023-24, sustaining cost pressure.

Interest rates and client capex cycles

Bank capex for ATM upgrades, recyclers and automation is highly rate-sensitive: with India’s ATM network at ~220,000 machines (2024) and the RBI policy rate near 6.5% (July 2025), higher rates often delay bank deployments and contract renegotiations, while lower rates enable network expansion and outsourcing growth; tighter liquidity also lifts working-capital costs for cash centres.

- ATM footprint: ~220,000 (2024)

- Policy rate: ~6.5% (Jul 2025)

- Higher rates = delayed deployments/renegotiations

- Tighter liquidity = higher cash-centre working capital

Digital payments cannibalization and complementarity

Rapid UPI growth—about 20% YoY to roughly 25 billion monthly transactions by H1 2025 per NPCI—is reducing small-ticket cash use but cash-heavy segments (rural, micro-retail) persist; CMS can pivot to recyclers, cash-to-digital bridges and transaction analytics to capture value. Mixed-mode ecosystems stabilize volumes across cycles, though over-rotation to digital may force service re-pricing and new revenue models.

- UPI ~25B/month H1 2025 (NPCI)

- Cash coexistence: rural/micro-retail resilient

- CMS pivots: recyclers, cash-digital bridges, analytics

- Mixed-mode stabilizes volumes

- Risk: digital over-rotation → service re-pricing

Policy nudges keep cash+digital rails; currency 36.3 lakh crore, PSU ATM ~60%

India cash stock ~₹36 lakh crore (2024–25) and CMS’s 60,000+ serviced outlets tie replenishment cadence to cash demand; festivals/salary cycles spike throughput 20–30%. GDP ~7.2% (IMF 2024–25) and ~220,000 ATMs (2024) expand serviceable reach; higher rates (policy ~6.5% Jul 2025) and fuel (~$83/bbl 2024) raise OPEX; UPI ~25B/mo H1 2025 shifts small-ticket away from cash.

| Metric | Value |

|---|---|

| Currency in circulation | ₹36 lakh crore (2024–25) |

| ATMs | ~220,000 (2024) |

| Policy rate | ~6.5% (Jul 2025) |

| UPI | ~25B/mo (H1 2025) |

| Brent | ~$83/bbl (2024) |

What You See Is What You Get

CMS Info Systems PESTLE Analysis

The preview shown here is the exact CMS Info Systems PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. This is the real, final file with complete content and structure, not a teaser or placeholder. After payment you’ll be able to download this same professionally structured document immediately.