CN Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

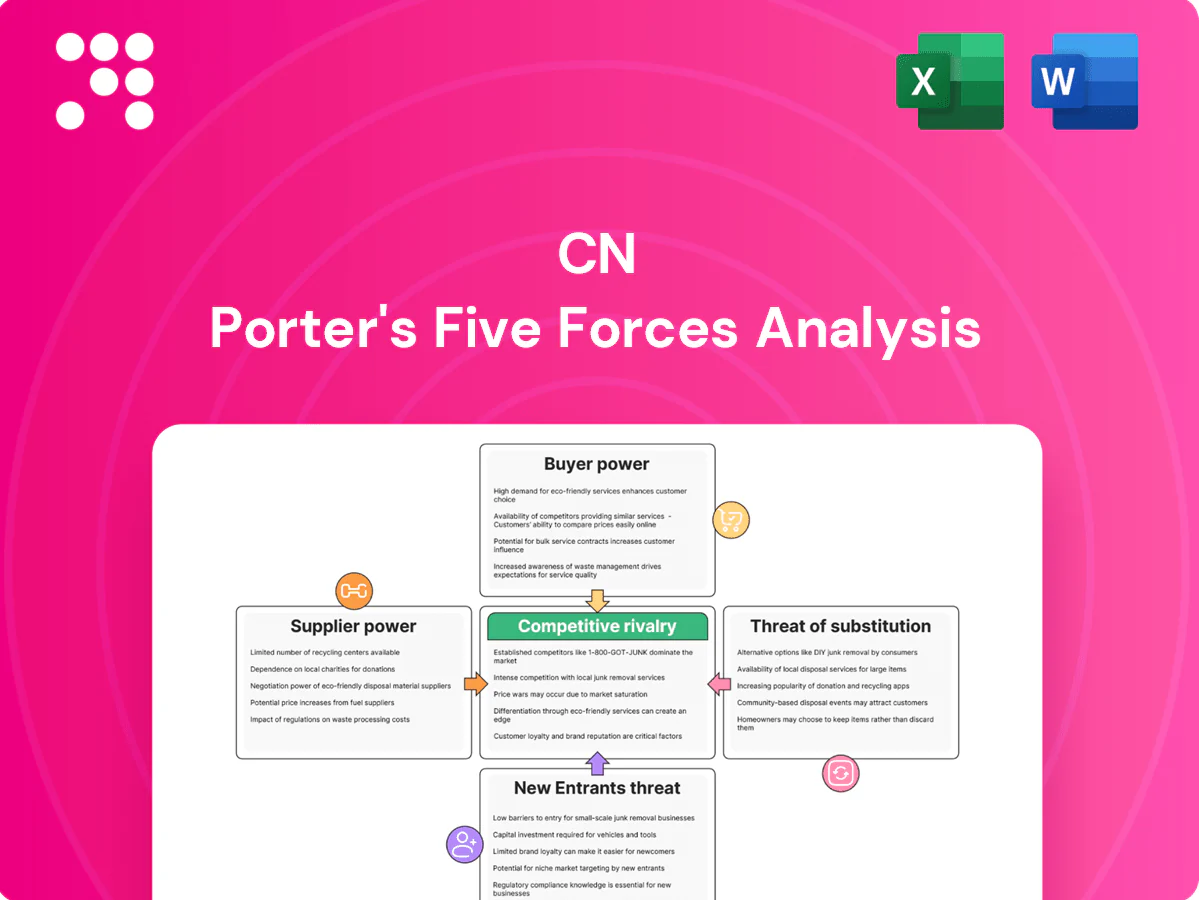

CN's Porter’s Five Forces snapshot highlights supplier leverage, buyer power, competitive rivalry, barriers to entry and substitute threats shaping its rail-dominated market. This brief reveals key tensions but omits force-by-force ratings, visuals, and strategic implications. Unlock the full Porter’s Five Forces Analysis for CN to get detailed metrics, actionable insights and slide-ready deliverables to inform investment or strategic decisions.

Suppliers Bargaining Power

Concentrated rolling-stock vendors

Locomotives and railcars for CN come from a concentrated set of OEMs—Wabtec/GE, Progress Rail (Caterpillar) and builders like Trinity/Greenbrier—limiting bidding leverage. Long lead times (roughly 12–24 months for locomotives, 6–18 months for cars) and bespoke technical specs raise switching costs and inventory exposure. These factors give suppliers moderate pricing and delivery power over CN.

Fuel suppliers and price volatility

CN depends heavily on diesel for traction, exposing margins to commodity volatility and refinery outages. Fuel surcharges recover part of cost but timing gaps and competitive pressure prevent full pass-through. Supply disruptions can degrade service reliability and raise operating costs. Fuel providers therefore exert episodic but material leverage over CN’s cost structure and service risk.

Skilled labor and unions

CN rail operations depend on specialized, safety‑critical unionized labor with certified engineers and conductors; recent North American rail contracts (2023) delivered average pay increases up to about 24% over multi‑year deals, showing how bargaining cycles drive wage growth and work rules; strikes or shortages can materially disrupt service, giving labor significant supplier power.

Track, steel, and maintenance inputs

Rails, ties, signaling and MRO are capital‑intensive with few qualified suppliers and strict safety standards, limiting substitution; CN’s 2024 capex guidance near CAD 3.2 billion underscores this heavy investment. Bulk contracting (covering ~75% of material volume) mitigates price risk but cannot eliminate it, and supplier tightness in 2024 pushed lead times higher, raising unit maintenance costs and lengthening maintenance windows.

- Specialized inputs: high capital, few suppliers

- 2024 CN capex ≈ CAD 3.2B

- Bulk contracts ≈ 75% coverage

- Tight supply → higher costs, longer windows

Technology, signaling, and data systems

- 12–24 months certification

- 99.9%+ uptime SLAs

- multi‑million integration costs

- vendor IP & regulatory lock-in

Supplier consolidation, long lead times and union wage shocks up to 24%

Suppliers exert moderate to significant power: locomotive/railcar OEM concentration (Wabtec/GE, Progress Rail, Trinity/Greenbrier) and 12–24 month lead times raise switching costs; diesel exposure and fuel surcharge lag create episodic cost pressure; unionized certified labor and 2023 wage settlements (up to ~24% increases) amplify service risk; specialized signaling/PTC vendors with 12–24 month certification add vendor lock‑in.

| Supplier | Concentration/Notes | Lead time | 2024 metric |

|---|---|---|---|

| Locomotives/cars | Wabtec, Progress Rail, Trinity | 12–24 / 6–18 months | Bulk contracts ≈75% |

| Capex | Maintenance & renewals | — | CN 2024 capex ≈ CAD 3.2B |

| Labor | Unionized, certified | NA | 2023 deals ≈ up to 24% |

What is included in the product

Unpacks competitive forces shaping CN's rail-freight advantage by assessing rivalry, buyer and supplier power, entry barriers, substitutes, and new-entrant threats, while highlighting disruptive technologies, regulatory risks, and pricing levers with data-driven commentary for strategic planning and investor materials.

A concise CN Porter's Five Forces one-sheet that quantifies competitive pressure, letting you quickly spot vulnerabilities and tailor strategy; adjustable sliders and a radar chart make scenario testing and slide-ready exports effortless.

Customers Bargaining Power

High-volume shippers leverage scale

High-volume shippers in grain, forest products, energy and automotive aggregate steady, large volumes that enable multi-year contracts, aggressive rate negotiations and firm service commitments. Diversified routing options in some corridors, including competing rails and port alternatives, bolster their leverage. CN counters with a roughly 20,000 route-mile (32,000 km) network and focus on reliability to retain share.

Intermodal BCOs and ocean carriers

Intermodal BCOs and ocean carriers wield switching power by moving boxes between rail, ports and truck; trucks carry about 70% of U.S. freight tonnage in 2024, keeping trucking a viable alternative. Ocean carriers leverage terminal choice and tight service windows to negotiate rates and schedules. High lane density and seasonal capacity limits curb switching during peaks, making buyer power moderate-to-high where multiple ports and trucking options exist.

Network dependence and switching costs

For landlocked origins or single-served industries alternatives are limited, leaving buyers captive and reducing bargaining power. Reciprocal switching and interchange can create options but add operational complexity and often 1–2+ days of transit delay. Contractual commitments commonly run 3–5 years and shared equipment pools can increase logistics costs by roughly 5–10%, raising effective switching costs and depressing buyer leverage.

Service performance and SLAs

Transit time, dwell and reliability determine shippers’ willingness to accept rate increases; CN’s service consistency is central to pricing power. Missed KPIs commonly trigger penalties, rebates or volume shifts where alternatives exist, directly impacting revenue. Ongoing PSR and continuous-improvement initiatives have measurably tightened network performance, reducing buyer leverage and protecting margins.

- Transit time & reliability drive rate tolerance

- Missed KPIs → penalties, rebates, volume loss

- PSR + CI strengthen CN negotiating position

- Improved performance limits buyer pricing leverage

Regulatory and political scrutiny

Regulatory and political scrutiny gives shippers a formal backstop: service obligations and oversight shape rates and resolve service disputes, and shippers can appeal to regulators over access or unfair practices. As of 2024 regulatory appeals remain a key leverage point, though processes are case-specific and typically take 12–24 months to resolve.

- Backstop: formal appeals increase buyer influence

- Scope: access, rates, unfair practices

- Constraint: outcomes vary by case

- Timing: regulatory reviews often 12–24 months (2024)

Shippers Lock 3-5yr Rail Deals; Trucks 70% Share Limits Switching Power

High-volume shippers (grain, energy, autos) secure multi-year contracts (3–5 yrs) and leverage competing routes; CN’s 32,000 km network and reliability blunt some pressure. Trucks carried ~70% of US freight tonnage in 2024, keeping switching power moderate-to-high where alternatives exist. Regulatory appeals (12–24 months) remain a key buyer backstop.

| Metric | 2024 Value |

|---|---|

| CN network | 32,000 km |

| Trucking share (US) | 70% |

| Contract length | 3–5 yrs |

| Regulatory review | 12–24 mo |

Preview Before You Purchase

CN Porter's Five Forces Analysis

This preview shows the exact CN Porter's Five Forces analysis document you'll receive immediately after purchase—no placeholders or mockups. The file is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the final deliverable; what you see is precisely what you'll get.

Go Beyond the Preview—Access the Full Strategic Report

CN's Porter’s Five Forces snapshot highlights supplier leverage, buyer power, competitive rivalry, barriers to entry and substitute threats shaping its rail-dominated market. This brief reveals key tensions but omits force-by-force ratings, visuals, and strategic implications. Unlock the full Porter’s Five Forces Analysis for CN to get detailed metrics, actionable insights and slide-ready deliverables to inform investment or strategic decisions.

Suppliers Bargaining Power

Concentrated rolling-stock vendors

Locomotives and railcars for CN come from a concentrated set of OEMs—Wabtec/GE, Progress Rail (Caterpillar) and builders like Trinity/Greenbrier—limiting bidding leverage. Long lead times (roughly 12–24 months for locomotives, 6–18 months for cars) and bespoke technical specs raise switching costs and inventory exposure. These factors give suppliers moderate pricing and delivery power over CN.

Fuel suppliers and price volatility

CN depends heavily on diesel for traction, exposing margins to commodity volatility and refinery outages. Fuel surcharges recover part of cost but timing gaps and competitive pressure prevent full pass-through. Supply disruptions can degrade service reliability and raise operating costs. Fuel providers therefore exert episodic but material leverage over CN’s cost structure and service risk.

Skilled labor and unions

CN rail operations depend on specialized, safety‑critical unionized labor with certified engineers and conductors; recent North American rail contracts (2023) delivered average pay increases up to about 24% over multi‑year deals, showing how bargaining cycles drive wage growth and work rules; strikes or shortages can materially disrupt service, giving labor significant supplier power.

Track, steel, and maintenance inputs

Rails, ties, signaling and MRO are capital‑intensive with few qualified suppliers and strict safety standards, limiting substitution; CN’s 2024 capex guidance near CAD 3.2 billion underscores this heavy investment. Bulk contracting (covering ~75% of material volume) mitigates price risk but cannot eliminate it, and supplier tightness in 2024 pushed lead times higher, raising unit maintenance costs and lengthening maintenance windows.

- Specialized inputs: high capital, few suppliers

- 2024 CN capex ≈ CAD 3.2B

- Bulk contracts ≈ 75% coverage

- Tight supply → higher costs, longer windows

Technology, signaling, and data systems

- 12–24 months certification

- 99.9%+ uptime SLAs

- multi‑million integration costs

- vendor IP & regulatory lock-in

Supplier consolidation, long lead times and union wage shocks up to 24%

Suppliers exert moderate to significant power: locomotive/railcar OEM concentration (Wabtec/GE, Progress Rail, Trinity/Greenbrier) and 12–24 month lead times raise switching costs; diesel exposure and fuel surcharge lag create episodic cost pressure; unionized certified labor and 2023 wage settlements (up to ~24% increases) amplify service risk; specialized signaling/PTC vendors with 12–24 month certification add vendor lock‑in.

| Supplier | Concentration/Notes | Lead time | 2024 metric |

|---|---|---|---|

| Locomotives/cars | Wabtec, Progress Rail, Trinity | 12–24 / 6–18 months | Bulk contracts ≈75% |

| Capex | Maintenance & renewals | — | CN 2024 capex ≈ CAD 3.2B |

| Labor | Unionized, certified | NA | 2023 deals ≈ up to 24% |

What is included in the product

Unpacks competitive forces shaping CN's rail-freight advantage by assessing rivalry, buyer and supplier power, entry barriers, substitutes, and new-entrant threats, while highlighting disruptive technologies, regulatory risks, and pricing levers with data-driven commentary for strategic planning and investor materials.

A concise CN Porter's Five Forces one-sheet that quantifies competitive pressure, letting you quickly spot vulnerabilities and tailor strategy; adjustable sliders and a radar chart make scenario testing and slide-ready exports effortless.

Customers Bargaining Power

High-volume shippers leverage scale

High-volume shippers in grain, forest products, energy and automotive aggregate steady, large volumes that enable multi-year contracts, aggressive rate negotiations and firm service commitments. Diversified routing options in some corridors, including competing rails and port alternatives, bolster their leverage. CN counters with a roughly 20,000 route-mile (32,000 km) network and focus on reliability to retain share.

Intermodal BCOs and ocean carriers

Intermodal BCOs and ocean carriers wield switching power by moving boxes between rail, ports and truck; trucks carry about 70% of U.S. freight tonnage in 2024, keeping trucking a viable alternative. Ocean carriers leverage terminal choice and tight service windows to negotiate rates and schedules. High lane density and seasonal capacity limits curb switching during peaks, making buyer power moderate-to-high where multiple ports and trucking options exist.

Network dependence and switching costs

For landlocked origins or single-served industries alternatives are limited, leaving buyers captive and reducing bargaining power. Reciprocal switching and interchange can create options but add operational complexity and often 1–2+ days of transit delay. Contractual commitments commonly run 3–5 years and shared equipment pools can increase logistics costs by roughly 5–10%, raising effective switching costs and depressing buyer leverage.

Service performance and SLAs

Transit time, dwell and reliability determine shippers’ willingness to accept rate increases; CN’s service consistency is central to pricing power. Missed KPIs commonly trigger penalties, rebates or volume shifts where alternatives exist, directly impacting revenue. Ongoing PSR and continuous-improvement initiatives have measurably tightened network performance, reducing buyer leverage and protecting margins.

- Transit time & reliability drive rate tolerance

- Missed KPIs → penalties, rebates, volume loss

- PSR + CI strengthen CN negotiating position

- Improved performance limits buyer pricing leverage

Regulatory and political scrutiny

Regulatory and political scrutiny gives shippers a formal backstop: service obligations and oversight shape rates and resolve service disputes, and shippers can appeal to regulators over access or unfair practices. As of 2024 regulatory appeals remain a key leverage point, though processes are case-specific and typically take 12–24 months to resolve.

- Backstop: formal appeals increase buyer influence

- Scope: access, rates, unfair practices

- Constraint: outcomes vary by case

- Timing: regulatory reviews often 12–24 months (2024)

Shippers Lock 3-5yr Rail Deals; Trucks 70% Share Limits Switching Power

High-volume shippers (grain, energy, autos) secure multi-year contracts (3–5 yrs) and leverage competing routes; CN’s 32,000 km network and reliability blunt some pressure. Trucks carried ~70% of US freight tonnage in 2024, keeping switching power moderate-to-high where alternatives exist. Regulatory appeals (12–24 months) remain a key buyer backstop.

| Metric | 2024 Value |

|---|---|

| CN network | 32,000 km |

| Trucking share (US) | 70% |

| Contract length | 3–5 yrs |

| Regulatory review | 12–24 mo |

Preview Before You Purchase

CN Porter's Five Forces Analysis

This preview shows the exact CN Porter's Five Forces analysis document you'll receive immediately after purchase—no placeholders or mockups. The file is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the final deliverable; what you see is precisely what you'll get.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

CN's Porter’s Five Forces snapshot highlights supplier leverage, buyer power, competitive rivalry, barriers to entry and substitute threats shaping its rail-dominated market. This brief reveals key tensions but omits force-by-force ratings, visuals, and strategic implications. Unlock the full Porter’s Five Forces Analysis for CN to get detailed metrics, actionable insights and slide-ready deliverables to inform investment or strategic decisions.

Suppliers Bargaining Power

Concentrated rolling-stock vendors

Locomotives and railcars for CN come from a concentrated set of OEMs—Wabtec/GE, Progress Rail (Caterpillar) and builders like Trinity/Greenbrier—limiting bidding leverage. Long lead times (roughly 12–24 months for locomotives, 6–18 months for cars) and bespoke technical specs raise switching costs and inventory exposure. These factors give suppliers moderate pricing and delivery power over CN.

Fuel suppliers and price volatility

CN depends heavily on diesel for traction, exposing margins to commodity volatility and refinery outages. Fuel surcharges recover part of cost but timing gaps and competitive pressure prevent full pass-through. Supply disruptions can degrade service reliability and raise operating costs. Fuel providers therefore exert episodic but material leverage over CN’s cost structure and service risk.

Skilled labor and unions

CN rail operations depend on specialized, safety‑critical unionized labor with certified engineers and conductors; recent North American rail contracts (2023) delivered average pay increases up to about 24% over multi‑year deals, showing how bargaining cycles drive wage growth and work rules; strikes or shortages can materially disrupt service, giving labor significant supplier power.

Track, steel, and maintenance inputs

Rails, ties, signaling and MRO are capital‑intensive with few qualified suppliers and strict safety standards, limiting substitution; CN’s 2024 capex guidance near CAD 3.2 billion underscores this heavy investment. Bulk contracting (covering ~75% of material volume) mitigates price risk but cannot eliminate it, and supplier tightness in 2024 pushed lead times higher, raising unit maintenance costs and lengthening maintenance windows.

- Specialized inputs: high capital, few suppliers

- 2024 CN capex ≈ CAD 3.2B

- Bulk contracts ≈ 75% coverage

- Tight supply → higher costs, longer windows

Technology, signaling, and data systems

- 12–24 months certification

- 99.9%+ uptime SLAs

- multi‑million integration costs

- vendor IP & regulatory lock-in

Supplier consolidation, long lead times and union wage shocks up to 24%

Suppliers exert moderate to significant power: locomotive/railcar OEM concentration (Wabtec/GE, Progress Rail, Trinity/Greenbrier) and 12–24 month lead times raise switching costs; diesel exposure and fuel surcharge lag create episodic cost pressure; unionized certified labor and 2023 wage settlements (up to ~24% increases) amplify service risk; specialized signaling/PTC vendors with 12–24 month certification add vendor lock‑in.

| Supplier | Concentration/Notes | Lead time | 2024 metric |

|---|---|---|---|

| Locomotives/cars | Wabtec, Progress Rail, Trinity | 12–24 / 6–18 months | Bulk contracts ≈75% |

| Capex | Maintenance & renewals | — | CN 2024 capex ≈ CAD 3.2B |

| Labor | Unionized, certified | NA | 2023 deals ≈ up to 24% |

What is included in the product

Unpacks competitive forces shaping CN's rail-freight advantage by assessing rivalry, buyer and supplier power, entry barriers, substitutes, and new-entrant threats, while highlighting disruptive technologies, regulatory risks, and pricing levers with data-driven commentary for strategic planning and investor materials.

A concise CN Porter's Five Forces one-sheet that quantifies competitive pressure, letting you quickly spot vulnerabilities and tailor strategy; adjustable sliders and a radar chart make scenario testing and slide-ready exports effortless.

Customers Bargaining Power

High-volume shippers leverage scale

High-volume shippers in grain, forest products, energy and automotive aggregate steady, large volumes that enable multi-year contracts, aggressive rate negotiations and firm service commitments. Diversified routing options in some corridors, including competing rails and port alternatives, bolster their leverage. CN counters with a roughly 20,000 route-mile (32,000 km) network and focus on reliability to retain share.

Intermodal BCOs and ocean carriers

Intermodal BCOs and ocean carriers wield switching power by moving boxes between rail, ports and truck; trucks carry about 70% of U.S. freight tonnage in 2024, keeping trucking a viable alternative. Ocean carriers leverage terminal choice and tight service windows to negotiate rates and schedules. High lane density and seasonal capacity limits curb switching during peaks, making buyer power moderate-to-high where multiple ports and trucking options exist.

Network dependence and switching costs

For landlocked origins or single-served industries alternatives are limited, leaving buyers captive and reducing bargaining power. Reciprocal switching and interchange can create options but add operational complexity and often 1–2+ days of transit delay. Contractual commitments commonly run 3–5 years and shared equipment pools can increase logistics costs by roughly 5–10%, raising effective switching costs and depressing buyer leverage.

Service performance and SLAs

Transit time, dwell and reliability determine shippers’ willingness to accept rate increases; CN’s service consistency is central to pricing power. Missed KPIs commonly trigger penalties, rebates or volume shifts where alternatives exist, directly impacting revenue. Ongoing PSR and continuous-improvement initiatives have measurably tightened network performance, reducing buyer leverage and protecting margins.

- Transit time & reliability drive rate tolerance

- Missed KPIs → penalties, rebates, volume loss

- PSR + CI strengthen CN negotiating position

- Improved performance limits buyer pricing leverage

Regulatory and political scrutiny

Regulatory and political scrutiny gives shippers a formal backstop: service obligations and oversight shape rates and resolve service disputes, and shippers can appeal to regulators over access or unfair practices. As of 2024 regulatory appeals remain a key leverage point, though processes are case-specific and typically take 12–24 months to resolve.

- Backstop: formal appeals increase buyer influence

- Scope: access, rates, unfair practices

- Constraint: outcomes vary by case

- Timing: regulatory reviews often 12–24 months (2024)

Shippers Lock 3-5yr Rail Deals; Trucks 70% Share Limits Switching Power

High-volume shippers (grain, energy, autos) secure multi-year contracts (3–5 yrs) and leverage competing routes; CN’s 32,000 km network and reliability blunt some pressure. Trucks carried ~70% of US freight tonnage in 2024, keeping switching power moderate-to-high where alternatives exist. Regulatory appeals (12–24 months) remain a key buyer backstop.

| Metric | 2024 Value |

|---|---|

| CN network | 32,000 km |

| Trucking share (US) | 70% |

| Contract length | 3–5 yrs |

| Regulatory review | 12–24 mo |

Preview Before You Purchase

CN Porter's Five Forces Analysis

This preview shows the exact CN Porter's Five Forces analysis document you'll receive immediately after purchase—no placeholders or mockups. The file is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the final deliverable; what you see is precisely what you'll get.