CNA Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

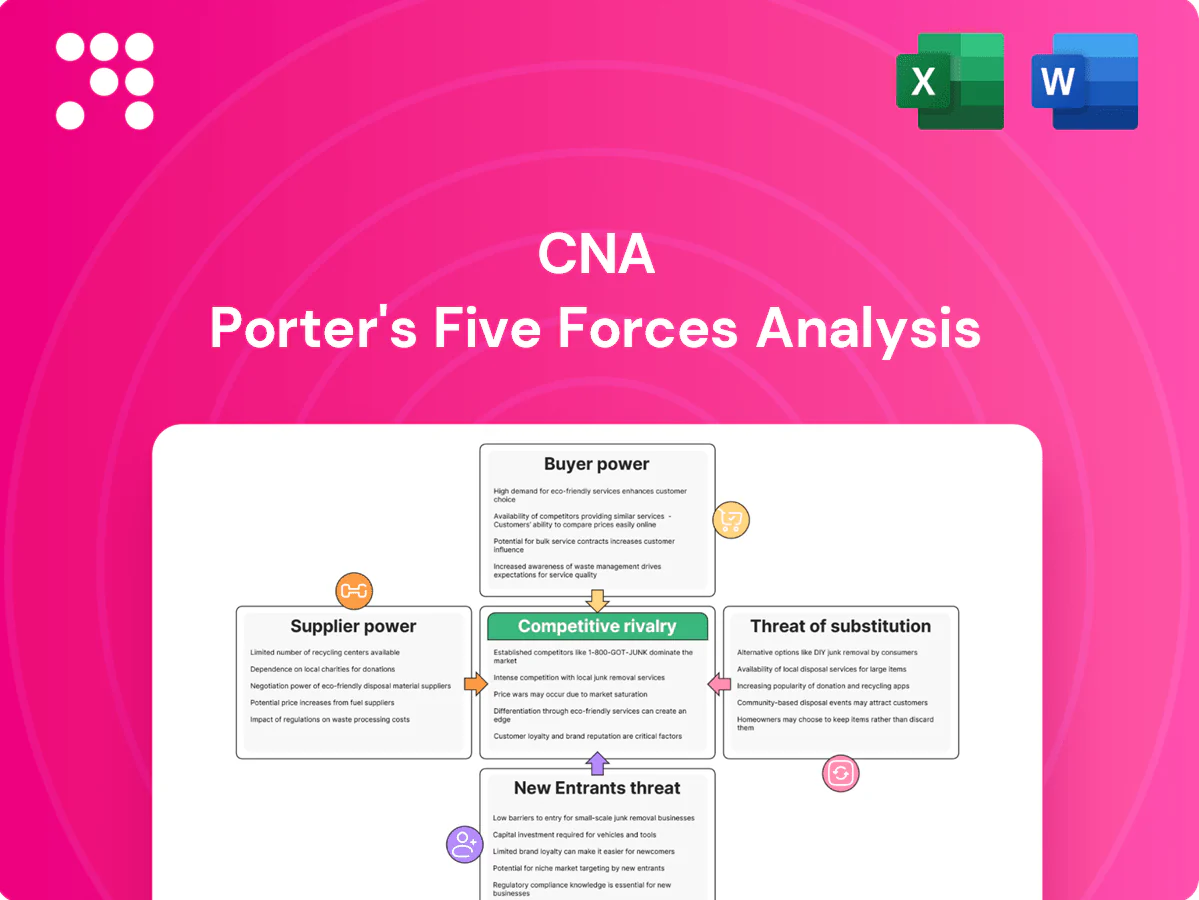

CNA’s Porter's Five Forces snapshot highlights supplier leverage, buyer power, competitive rivalry, threat of substitutes and new entrants and their strategic implications for insurers. This brief view surfaces key pressures shaping CNA’s profitability and market positioning. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals and actionable recommendations tailored to CNA.

Suppliers Bargaining Power

Reinsurers’ Pricing Leverage

Reinsurers supply vital risk capacity that stabilizes CNA’s earnings but can reprice sharply after catastrophe or inflation shocks, pushing up ceded rates and claims volatility.

Tight retrocession markets and higher catastrophe loads directly raise CNA’s cost of goods sold through increased reinsurance expense and reduced net retention flexibility.

Long-term panels and multi-year treaties moderate volatility, yet renewal timing remains a pressure point; diversification of cedents and growth in alternative capital—ILS AUM topped $100 billion in 2024—can temper reinsurer leverage.

Broker and MGA Distribution Influence

Large brokers control deal flow and can demand higher commissions, bespoke services and tailored wordings, with the top 10 intermediaries estimated to handle roughly 65% of global commercial brokered premiums. MGAs with niche portfolios and proprietary distribution access negotiate favorable terms, contributing to MGA-written premiums rising into the low tens of billions annually by 2024. Concentration among top intermediaries increases pressure on pricing and servicing. Strengthening direct carrier relationships and offering value-added risk services can rebalance influence.

Data, Models, and Tech Vendors

Catastrophe models, telematics and cyber analytics vendors are specialized and not perfectly substitutable, with vendor switching often requiring integration projects lasting 6–18 months and implementation costs in the low-to-mid millions. Vendor lock-in and API/legacy integration raise switching barriers, so price hikes or model revisions can materially shift underwriting appetite and capital use. Building in-house analytics has reduced dependence for many firms by 2024, lowering long-term vendor spend.

Specialist Talent and Claims Ecosystem

Experienced underwriters, actuaries and complex-claims experts are scarce, with 61% of insurers citing talent shortages in 2024 (Willis Towers Watson 2024); base pay inflation averaged about 5.8% in the sector in 2024 (Mercer). External adjusters, repair networks and legal counsel materially affect loss costs and can extend cycle times by weeks, increasing claim expense. Investing in training and preferred networks reduces turnover and supplier leverage.

- Talent scarcity: 61% (Willis Towers Watson 2024)

- Wage inflation: ~5.8% avg pay rise (Mercer 2024)

- Outsourced providers: raise costs and cycle times

- Mitigation: training, preferred networks, retention packages

Capital Markets and Rating Agencies

Access to capital at competitive spreads hinges on ratings and market conditions; with the 10-year Treasury near 4.6% in 2024, rating-driven spread moves materially affect funding costs. Rating agencies effectively supply credibility and can raise capital costs via outlook downgrades or negative commentary. Tighter solvency or risk-charge increases limit growth and pricing flexibility, while conservative reserving and stable combined ratios preserve bargaining leverage.

- Ratings sensitivity: drive spread premium

- 10y Treasury ~4.6% (2024): baseline funding cost

- Solvency/risk charges: constrain capital deployment

- Conservative reserving: strengthens negotiating position

Reinsurers, brokers and talent drive moderate-to-high supplier power in insurance market

Reinsurers, brokers, analytics vendors and talent exert moderate-to-high supplier power over CNA: reinsurer repricing after catastrophes raises ceded costs, while top 10 brokers handle ~65% of commercial brokered premiums (2024), pushing commissions and bespoke demands. Talent scarcity (61% cite shortages in 2024) and 5.8% wage inflation raise operating costs; vendor lock-in (6–18 month integrations) limits switching. Strong ratings and access to capital (10y Treasury ~4.6% in 2024) affect funding spreads and negotiating leverage.

| Supplier | Key metric (2024) |

|---|---|

| Reinsurance/ILS | ILS AUM > $100B |

| Brokers | Top 10 ≈ 65% premiums |

| Talent | 61% shortage; +5.8% pay |

| Capital | 10y Treasury ~4.6% |

What is included in the product

Concise Porter's Five Forces analysis tailored for CNA, assessing competitive rivalry, buyer and supplier power, entry barriers, and substitute threats to reveal strategic risks, pricing pressure, and opportunities to defend market share and profitability.

One-sheet CNA Porter's Five Forces summary that maps competitive pressures and mitigation levers for fast board decisions—customizable pressure levels to reflect new data or regulatory shifts.

Customers Bargaining Power

Large Corporate Accounts’ Negotiating Clout

Fortune 1000 buyers run competitive tenders across the 1000 largest U.S. firms and use analytics to pit carriers against each other, forcing concessions on price and terms. Program scale drives bespoke coverage and multi-year rate caps, while loss-sensitive plans shift frequency and severity risk back to buyers yet demand low expense loads. CNA must differentiate through measurable risk engineering and superior claims outcomes to defend margin.

Broker-Led Market Transparency

Broker benchmarking exposes market pricing and terms, with over 60% of commercial renewals shopped in 2024, heightening buyer leverage; renewal marketing across multiple carriers forces competitive pricing on each account, while coverage enhancements and endorsements have become table stakes in soft markets; strong broker relationships still steer high-fit risks to CNA.

Mid-Market Price Sensitivity

Mid-sized buyers show high price sensitivity: a 2024 industry survey found ~38% actively shop at renewal and digital quoting platforms—used by roughly 65% of mid-market firms—lower switching friction, while strong claims satisfaction and service quality deliver measurable stickiness; bundled packaging and multi-year plans reduce churn materially, cutting renewal attrition by an estimated 10–20% in 2024 programs.

Specialty Buyers’ Limited Alternatives

Specialty buyers in marine, surety and cyber face limited credible carrier alternatives, so buyer bargaining is constrained despite demands for broader terms as exposures evolve.

CNA leverages underwriting expertise and vertical industry knowledge to retain pricing power, while demonstrable claims proficiency in rare events—highlighted in CNA public disclosures in 2024—reinforces its negotiating position.

- Limited alternatives: niche risk concentration

- Buyer pressure: broader terms from evolving exposures

- Mitigants: underwriting depth and sector expertise

- Strength: proven claims handling in low-frequency, high-severity events

Self-Insurance and Captives

Qualified buyers increasingly use captives or high deductibles to cut premiums; there were over 7,000 captives globally in 2024, making alternative risk transfer a credible outside option and raising buyer bargaining power. CNA can protect economics via fronting, reinsurance, or hybrid structures while advisory services on retention align incentives and preserve client relationships.

- Captive growth: >7,000 globally (2024)

- Buyer tools: high deductibles, ART

- CNA response: fronting, reinsurance, advisory

Buyers Hold Leverage as >60% of Commercial Renewals Were Shopped in 2024

Buyers wield strong leverage via tenders and broker benchmarking (over 60% commercial renewals shopped in 2024), forcing price and term concessions. Mid-market shopping (≈38%) and digital quoting (~65%) lower switching friction; >7,000 captives globally in 2024 raise alternative options. CNA defends margins through underwriting, risk engineering, claims outcomes, fronting and reinsurance.

| Metric | 2024 Value |

|---|---|

| Renewals shopped | >60% |

| Mid-market shopping | ≈38% |

| Digital quoting use | ≈65% |

| Captives | >7,000 |

Preview Before You Purchase

CNA Porter's Five Forces Analysis

This CNA Porter's Five Forces Analysis preview is the exact, fully formatted document you'll receive immediately after purchase—no placeholders or samples. It contains the complete industry assessment, competitive intensity evaluation, and actionable implications. Downloadable and ready for use upon payment.

Go Beyond the Preview—Access the Full Strategic Report

CNA’s Porter's Five Forces snapshot highlights supplier leverage, buyer power, competitive rivalry, threat of substitutes and new entrants and their strategic implications for insurers. This brief view surfaces key pressures shaping CNA’s profitability and market positioning. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals and actionable recommendations tailored to CNA.

Suppliers Bargaining Power

Reinsurers’ Pricing Leverage

Reinsurers supply vital risk capacity that stabilizes CNA’s earnings but can reprice sharply after catastrophe or inflation shocks, pushing up ceded rates and claims volatility.

Tight retrocession markets and higher catastrophe loads directly raise CNA’s cost of goods sold through increased reinsurance expense and reduced net retention flexibility.

Long-term panels and multi-year treaties moderate volatility, yet renewal timing remains a pressure point; diversification of cedents and growth in alternative capital—ILS AUM topped $100 billion in 2024—can temper reinsurer leverage.

Broker and MGA Distribution Influence

Large brokers control deal flow and can demand higher commissions, bespoke services and tailored wordings, with the top 10 intermediaries estimated to handle roughly 65% of global commercial brokered premiums. MGAs with niche portfolios and proprietary distribution access negotiate favorable terms, contributing to MGA-written premiums rising into the low tens of billions annually by 2024. Concentration among top intermediaries increases pressure on pricing and servicing. Strengthening direct carrier relationships and offering value-added risk services can rebalance influence.

Data, Models, and Tech Vendors

Catastrophe models, telematics and cyber analytics vendors are specialized and not perfectly substitutable, with vendor switching often requiring integration projects lasting 6–18 months and implementation costs in the low-to-mid millions. Vendor lock-in and API/legacy integration raise switching barriers, so price hikes or model revisions can materially shift underwriting appetite and capital use. Building in-house analytics has reduced dependence for many firms by 2024, lowering long-term vendor spend.

Specialist Talent and Claims Ecosystem

Experienced underwriters, actuaries and complex-claims experts are scarce, with 61% of insurers citing talent shortages in 2024 (Willis Towers Watson 2024); base pay inflation averaged about 5.8% in the sector in 2024 (Mercer). External adjusters, repair networks and legal counsel materially affect loss costs and can extend cycle times by weeks, increasing claim expense. Investing in training and preferred networks reduces turnover and supplier leverage.

- Talent scarcity: 61% (Willis Towers Watson 2024)

- Wage inflation: ~5.8% avg pay rise (Mercer 2024)

- Outsourced providers: raise costs and cycle times

- Mitigation: training, preferred networks, retention packages

Capital Markets and Rating Agencies

Access to capital at competitive spreads hinges on ratings and market conditions; with the 10-year Treasury near 4.6% in 2024, rating-driven spread moves materially affect funding costs. Rating agencies effectively supply credibility and can raise capital costs via outlook downgrades or negative commentary. Tighter solvency or risk-charge increases limit growth and pricing flexibility, while conservative reserving and stable combined ratios preserve bargaining leverage.

- Ratings sensitivity: drive spread premium

- 10y Treasury ~4.6% (2024): baseline funding cost

- Solvency/risk charges: constrain capital deployment

- Conservative reserving: strengthens negotiating position

Reinsurers, brokers and talent drive moderate-to-high supplier power in insurance market

Reinsurers, brokers, analytics vendors and talent exert moderate-to-high supplier power over CNA: reinsurer repricing after catastrophes raises ceded costs, while top 10 brokers handle ~65% of commercial brokered premiums (2024), pushing commissions and bespoke demands. Talent scarcity (61% cite shortages in 2024) and 5.8% wage inflation raise operating costs; vendor lock-in (6–18 month integrations) limits switching. Strong ratings and access to capital (10y Treasury ~4.6% in 2024) affect funding spreads and negotiating leverage.

| Supplier | Key metric (2024) |

|---|---|

| Reinsurance/ILS | ILS AUM > $100B |

| Brokers | Top 10 ≈ 65% premiums |

| Talent | 61% shortage; +5.8% pay |

| Capital | 10y Treasury ~4.6% |

What is included in the product

Concise Porter's Five Forces analysis tailored for CNA, assessing competitive rivalry, buyer and supplier power, entry barriers, and substitute threats to reveal strategic risks, pricing pressure, and opportunities to defend market share and profitability.

One-sheet CNA Porter's Five Forces summary that maps competitive pressures and mitigation levers for fast board decisions—customizable pressure levels to reflect new data or regulatory shifts.

Customers Bargaining Power

Large Corporate Accounts’ Negotiating Clout

Fortune 1000 buyers run competitive tenders across the 1000 largest U.S. firms and use analytics to pit carriers against each other, forcing concessions on price and terms. Program scale drives bespoke coverage and multi-year rate caps, while loss-sensitive plans shift frequency and severity risk back to buyers yet demand low expense loads. CNA must differentiate through measurable risk engineering and superior claims outcomes to defend margin.

Broker-Led Market Transparency

Broker benchmarking exposes market pricing and terms, with over 60% of commercial renewals shopped in 2024, heightening buyer leverage; renewal marketing across multiple carriers forces competitive pricing on each account, while coverage enhancements and endorsements have become table stakes in soft markets; strong broker relationships still steer high-fit risks to CNA.

Mid-Market Price Sensitivity

Mid-sized buyers show high price sensitivity: a 2024 industry survey found ~38% actively shop at renewal and digital quoting platforms—used by roughly 65% of mid-market firms—lower switching friction, while strong claims satisfaction and service quality deliver measurable stickiness; bundled packaging and multi-year plans reduce churn materially, cutting renewal attrition by an estimated 10–20% in 2024 programs.

Specialty Buyers’ Limited Alternatives

Specialty buyers in marine, surety and cyber face limited credible carrier alternatives, so buyer bargaining is constrained despite demands for broader terms as exposures evolve.

CNA leverages underwriting expertise and vertical industry knowledge to retain pricing power, while demonstrable claims proficiency in rare events—highlighted in CNA public disclosures in 2024—reinforces its negotiating position.

- Limited alternatives: niche risk concentration

- Buyer pressure: broader terms from evolving exposures

- Mitigants: underwriting depth and sector expertise

- Strength: proven claims handling in low-frequency, high-severity events

Self-Insurance and Captives

Qualified buyers increasingly use captives or high deductibles to cut premiums; there were over 7,000 captives globally in 2024, making alternative risk transfer a credible outside option and raising buyer bargaining power. CNA can protect economics via fronting, reinsurance, or hybrid structures while advisory services on retention align incentives and preserve client relationships.

- Captive growth: >7,000 globally (2024)

- Buyer tools: high deductibles, ART

- CNA response: fronting, reinsurance, advisory

Buyers Hold Leverage as >60% of Commercial Renewals Were Shopped in 2024

Buyers wield strong leverage via tenders and broker benchmarking (over 60% commercial renewals shopped in 2024), forcing price and term concessions. Mid-market shopping (≈38%) and digital quoting (~65%) lower switching friction; >7,000 captives globally in 2024 raise alternative options. CNA defends margins through underwriting, risk engineering, claims outcomes, fronting and reinsurance.

| Metric | 2024 Value |

|---|---|

| Renewals shopped | >60% |

| Mid-market shopping | ≈38% |

| Digital quoting use | ≈65% |

| Captives | >7,000 |

Preview Before You Purchase

CNA Porter's Five Forces Analysis

This CNA Porter's Five Forces Analysis preview is the exact, fully formatted document you'll receive immediately after purchase—no placeholders or samples. It contains the complete industry assessment, competitive intensity evaluation, and actionable implications. Downloadable and ready for use upon payment.

Description

Go Beyond the Preview—Access the Full Strategic Report

CNA’s Porter's Five Forces snapshot highlights supplier leverage, buyer power, competitive rivalry, threat of substitutes and new entrants and their strategic implications for insurers. This brief view surfaces key pressures shaping CNA’s profitability and market positioning. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals and actionable recommendations tailored to CNA.

Suppliers Bargaining Power

Reinsurers’ Pricing Leverage

Reinsurers supply vital risk capacity that stabilizes CNA’s earnings but can reprice sharply after catastrophe or inflation shocks, pushing up ceded rates and claims volatility.

Tight retrocession markets and higher catastrophe loads directly raise CNA’s cost of goods sold through increased reinsurance expense and reduced net retention flexibility.

Long-term panels and multi-year treaties moderate volatility, yet renewal timing remains a pressure point; diversification of cedents and growth in alternative capital—ILS AUM topped $100 billion in 2024—can temper reinsurer leverage.

Broker and MGA Distribution Influence

Large brokers control deal flow and can demand higher commissions, bespoke services and tailored wordings, with the top 10 intermediaries estimated to handle roughly 65% of global commercial brokered premiums. MGAs with niche portfolios and proprietary distribution access negotiate favorable terms, contributing to MGA-written premiums rising into the low tens of billions annually by 2024. Concentration among top intermediaries increases pressure on pricing and servicing. Strengthening direct carrier relationships and offering value-added risk services can rebalance influence.

Data, Models, and Tech Vendors

Catastrophe models, telematics and cyber analytics vendors are specialized and not perfectly substitutable, with vendor switching often requiring integration projects lasting 6–18 months and implementation costs in the low-to-mid millions. Vendor lock-in and API/legacy integration raise switching barriers, so price hikes or model revisions can materially shift underwriting appetite and capital use. Building in-house analytics has reduced dependence for many firms by 2024, lowering long-term vendor spend.

Specialist Talent and Claims Ecosystem

Experienced underwriters, actuaries and complex-claims experts are scarce, with 61% of insurers citing talent shortages in 2024 (Willis Towers Watson 2024); base pay inflation averaged about 5.8% in the sector in 2024 (Mercer). External adjusters, repair networks and legal counsel materially affect loss costs and can extend cycle times by weeks, increasing claim expense. Investing in training and preferred networks reduces turnover and supplier leverage.

- Talent scarcity: 61% (Willis Towers Watson 2024)

- Wage inflation: ~5.8% avg pay rise (Mercer 2024)

- Outsourced providers: raise costs and cycle times

- Mitigation: training, preferred networks, retention packages

Capital Markets and Rating Agencies

Access to capital at competitive spreads hinges on ratings and market conditions; with the 10-year Treasury near 4.6% in 2024, rating-driven spread moves materially affect funding costs. Rating agencies effectively supply credibility and can raise capital costs via outlook downgrades or negative commentary. Tighter solvency or risk-charge increases limit growth and pricing flexibility, while conservative reserving and stable combined ratios preserve bargaining leverage.

- Ratings sensitivity: drive spread premium

- 10y Treasury ~4.6% (2024): baseline funding cost

- Solvency/risk charges: constrain capital deployment

- Conservative reserving: strengthens negotiating position

Reinsurers, brokers and talent drive moderate-to-high supplier power in insurance market

Reinsurers, brokers, analytics vendors and talent exert moderate-to-high supplier power over CNA: reinsurer repricing after catastrophes raises ceded costs, while top 10 brokers handle ~65% of commercial brokered premiums (2024), pushing commissions and bespoke demands. Talent scarcity (61% cite shortages in 2024) and 5.8% wage inflation raise operating costs; vendor lock-in (6–18 month integrations) limits switching. Strong ratings and access to capital (10y Treasury ~4.6% in 2024) affect funding spreads and negotiating leverage.

| Supplier | Key metric (2024) |

|---|---|

| Reinsurance/ILS | ILS AUM > $100B |

| Brokers | Top 10 ≈ 65% premiums |

| Talent | 61% shortage; +5.8% pay |

| Capital | 10y Treasury ~4.6% |

What is included in the product

Concise Porter's Five Forces analysis tailored for CNA, assessing competitive rivalry, buyer and supplier power, entry barriers, and substitute threats to reveal strategic risks, pricing pressure, and opportunities to defend market share and profitability.

One-sheet CNA Porter's Five Forces summary that maps competitive pressures and mitigation levers for fast board decisions—customizable pressure levels to reflect new data or regulatory shifts.

Customers Bargaining Power

Large Corporate Accounts’ Negotiating Clout

Fortune 1000 buyers run competitive tenders across the 1000 largest U.S. firms and use analytics to pit carriers against each other, forcing concessions on price and terms. Program scale drives bespoke coverage and multi-year rate caps, while loss-sensitive plans shift frequency and severity risk back to buyers yet demand low expense loads. CNA must differentiate through measurable risk engineering and superior claims outcomes to defend margin.

Broker-Led Market Transparency

Broker benchmarking exposes market pricing and terms, with over 60% of commercial renewals shopped in 2024, heightening buyer leverage; renewal marketing across multiple carriers forces competitive pricing on each account, while coverage enhancements and endorsements have become table stakes in soft markets; strong broker relationships still steer high-fit risks to CNA.

Mid-Market Price Sensitivity

Mid-sized buyers show high price sensitivity: a 2024 industry survey found ~38% actively shop at renewal and digital quoting platforms—used by roughly 65% of mid-market firms—lower switching friction, while strong claims satisfaction and service quality deliver measurable stickiness; bundled packaging and multi-year plans reduce churn materially, cutting renewal attrition by an estimated 10–20% in 2024 programs.

Specialty Buyers’ Limited Alternatives

Specialty buyers in marine, surety and cyber face limited credible carrier alternatives, so buyer bargaining is constrained despite demands for broader terms as exposures evolve.

CNA leverages underwriting expertise and vertical industry knowledge to retain pricing power, while demonstrable claims proficiency in rare events—highlighted in CNA public disclosures in 2024—reinforces its negotiating position.

- Limited alternatives: niche risk concentration

- Buyer pressure: broader terms from evolving exposures

- Mitigants: underwriting depth and sector expertise

- Strength: proven claims handling in low-frequency, high-severity events

Self-Insurance and Captives

Qualified buyers increasingly use captives or high deductibles to cut premiums; there were over 7,000 captives globally in 2024, making alternative risk transfer a credible outside option and raising buyer bargaining power. CNA can protect economics via fronting, reinsurance, or hybrid structures while advisory services on retention align incentives and preserve client relationships.

- Captive growth: >7,000 globally (2024)

- Buyer tools: high deductibles, ART

- CNA response: fronting, reinsurance, advisory

Buyers Hold Leverage as >60% of Commercial Renewals Were Shopped in 2024

Buyers wield strong leverage via tenders and broker benchmarking (over 60% commercial renewals shopped in 2024), forcing price and term concessions. Mid-market shopping (≈38%) and digital quoting (~65%) lower switching friction; >7,000 captives globally in 2024 raise alternative options. CNA defends margins through underwriting, risk engineering, claims outcomes, fronting and reinsurance.

| Metric | 2024 Value |

|---|---|

| Renewals shopped | >60% |

| Mid-market shopping | ≈38% |

| Digital quoting use | ≈65% |

| Captives | >7,000 |

Preview Before You Purchase

CNA Porter's Five Forces Analysis

This CNA Porter's Five Forces Analysis preview is the exact, fully formatted document you'll receive immediately after purchase—no placeholders or samples. It contains the complete industry assessment, competitive intensity evaluation, and actionable implications. Downloadable and ready for use upon payment.