China National Nuclear Power Business Model Canvas

Business Model Canvas: Strategic Blueprint for a Leading Chinese Nuclear Power Operator

Unlock the full strategic blueprint behind China National Nuclear Power with our Business Model Canvas. This concise, actionable canvas maps value propositions, key partnerships, revenue streams and risks—ideal for investors, consultants and strategists. Download the complete Word/Excel package to benchmark, plan and capitalize on industry insights.

Partnerships

CNNC group subsidiaries and SOE ecosystem

Deep integration with parent CNNC aligns strategy, financing and technology roadmaps within China’s state-owned nuclear ecosystem, supporting national targets as China operated 55 reactors and had 23 under construction in 2024. Subsidiaries such as CNPE (EPC), CNI (installation) and CNNC Uranium provide full‑lifecycle services from supply to build and fuel. This SOE network lowers coordination risk and accelerates deployment timelines.

Grid operators and dispatch centers

Partnerships with State Grid and China Southern Power Grid secure offtake and dispatch priority across China's two major transmission operators, aligning with national policy to prioritize nuclear for baseload stability. Joint planning with these operators optimizes baseload scheduling and outage windows, reducing curtailment and enabling steady dispatch of CNNP units. Tight coupling ensures reliable integration of nuclear output from China's roughly 57 GW installed nuclear fleet (end-2024).

Regulators and safety authorities

Close collaboration with the NNSA and other agencies secures licensing, routine inspections and regulatory compliance for China National Nuclear Power, which operates about 55 reactors (~55 GW) with roughly 22 units under construction (IAEA/2024). Proactive engagement helps shape safety cases and drives continuous improvement in plant performance and emergency preparedness. This regulatory partnership builds public trust and supports operating license continuity, reducing shutdown risk and preserving revenue streams.

Fuel cycle and waste management partners

Long-term contracts with uranium miners, enrichers and fabricators secure feedstock for China National Nuclear Power as China’s nuclear fleet reached about 57 GW with roughly 21 reactors under construction at end-2024, lowering spot-price exposure. Partnerships for spent-fuel storage and back-end solutions shift lifecycle liabilities off balance sheets and reduce regulatory and disposal risk. Coordinated logistics across mining, enrichment and fuel fabrication cut downtime and mitigate cost volatility in fuel delivery.

- Long-term uranium, enrichment and fabrication contracts

- Back-end storage and disposal partnerships

- Integrated logistics to minimize downtime and price exposure

R&D institutes, universities, and international bodies

Integration, long-term fuel contracts and grid offtake de-risk 55 reactors

Deep CNNC integration, EPC/subsidiary linkages and long-term fuel contracts de-risk projects and finance, supporting China’s 55 reactors and 23 under construction in 2024. Grid partnerships (State Grid, China Southern) secure dispatch and offtake for ~57 GW fleet (end-2024). Regulatory and R&D ties (NNSA, CIAE, IAEA programs) speed licensing, safety upgrades and talent flow.

| Partner | Role | 2024 metric |

|---|---|---|

| CNNC group | EPC, financing, fuel | 55 reactors / 23 UC |

| State Grid | Offtake, dispatch | ~57 GW fleet |

| Uranium suppliers | Fuel security | Long-term contracts |

| CIAE/IAEA | R&D, safety | Joint programs |

What is included in the product

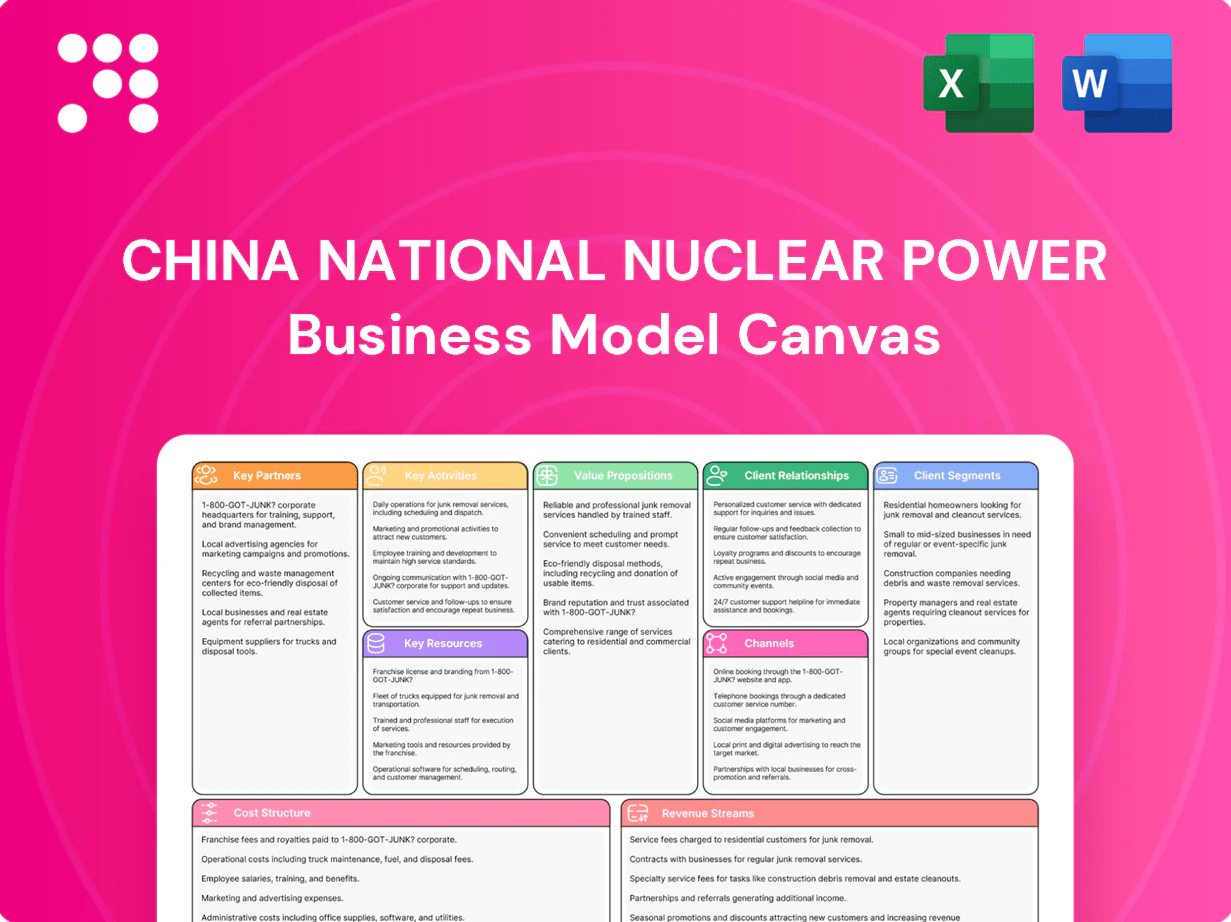

A comprehensive Business Model Canvas for China National Nuclear Power mapping all 9 blocks—customer segments, value propositions, channels, revenue streams, key partners, activities, resources, cost structure, and customer relationships—aligned with real-world nuclear operations and growth strategy. Ideal for investor presentations, it includes competitive advantage analysis and linked SWOT insights to support strategic decisions and funding discussions.

High-level, editable one-page snapshot of China National Nuclear Power’s business model that reduces analysis time and aligns stakeholders quickly for strategic decisions.

Activities

Investment and project development

Site selection, feasibility studies and permitting form the backbone of new-builds, with China operating about 55 reactors (~52 GW) and ~22 under construction (~25 GW) as of 2024, guiding regional grid, water and seismic assessments. Financial structuring commonly targets 60–70% debt in project finance to achieve bankability and allocate construction and market risks. Coordinated stakeholder management—central government, regulators, grid operators and local authorities—streamlines land, EPC contracts and off-take readiness for timely construction starts.

EPC management and commissioning

Oversee EPC with rigorous QA/QC aligned to China’s 2024 large-scale nuclear new-build program, enforcing vendor certification, weld inspection and materials traceability across GW-scale units. Schedule, cost and interface control manage multi‑billion‑dollar timelines and contractor interfaces to limit delays and claims. Commissioning executes hot functional tests, fuel loading and low‑power physics tests to validate performance and safety before grid synchronization.

Plant operations and maintenance

Operate reactors to high capacity factors with strict procedures; China had about 55 GW of nuclear capacity operational in 2024 and the national fleet averaged capacity factors above 80% under standardized safety protocols. Predictive and preventive maintenance using online monitoring and digital twins reduces forced outages and sustains reliability. Outage management schedules refueling and upgrades to minimize downtime and optimize LCOE.

Fuel cycle planning and logistics

Procure, fabricate, and deliver fuel assemblies on time for China’s fleet of 55 operational reactors (IAEA, June 2024), coordinating domestic manufacturers to meet outage windows and limit import dependence. Manage spent fuel handling and interim storage at site pools and centralized facilities, preparing for throughput growth from 23 reactors under construction. Optimize inventory with just-in-time deliveries plus buffer stocks sized to cover multi-month outages to balance cost and security.

- On-time delivery: align supply with outage schedules

- Spent fuel: site pools + centralized interim storage capacity planning

- Inventory: JIT + strategic buffers to minimize cost and enhance security

Safety, compliance, and continuous improvement

Conducts regular safety analyses, drills, and audits to meet CNNC and National Nuclear Safety Administration standards; China operated 55 commercial reactors by end-2024, underscoring scale and regulatory scrutiny.

Tracks KPIs and lessons learned (safety events per 10,000 reactor-hours, outage duration, maintenance cost per MW) to drive continuous improvement; transparent reporting preserves operating licenses and social license to operate.

- Safety audits: regulatory compliance

- KPI tracking: events per 10,000 reactor-hours

- Reporting: license and social license

China nuclear expansion: 55 reactors (~52 GW), 22 under build, 60–70% debt

Site selection, permitting and project finance (60–70% debt) drive new-build execution for China’s ~55 reactors (~52 GW) with ~22 under construction (~25 GW) in 2024.

EPC oversight, QA/QC, commissioning and schedule control limit delays on GW-scale units and manage multi‑billion‑dollar interfaces.

Operations focus on >80% fleet capacity factors, predictive maintenance, fuel supply coordination and spent-fuel interim storage planning.

| Metric | 2024 |

|---|---|

| Operational reactors | 55 (~52 GW) |

| Under construction | 22 (~25 GW) |

| Target debt | 60–70% |

| Avg capacity factor | >80% |

Full Version Awaits

Business Model Canvas

The document previewed here is the actual China National Nuclear Power Business Model Canvas, not a mockup or sample. When you purchase, you’ll receive this exact, fully formatted file with all sections included. It’s ready to download, edit, present, and apply—no surprises, just the real deliverable.

Business Model Canvas: Strategic Blueprint for a Leading Chinese Nuclear Power Operator

Unlock the full strategic blueprint behind China National Nuclear Power with our Business Model Canvas. This concise, actionable canvas maps value propositions, key partnerships, revenue streams and risks—ideal for investors, consultants and strategists. Download the complete Word/Excel package to benchmark, plan and capitalize on industry insights.

Partnerships

CNNC group subsidiaries and SOE ecosystem

Deep integration with parent CNNC aligns strategy, financing and technology roadmaps within China’s state-owned nuclear ecosystem, supporting national targets as China operated 55 reactors and had 23 under construction in 2024. Subsidiaries such as CNPE (EPC), CNI (installation) and CNNC Uranium provide full‑lifecycle services from supply to build and fuel. This SOE network lowers coordination risk and accelerates deployment timelines.

Grid operators and dispatch centers

Partnerships with State Grid and China Southern Power Grid secure offtake and dispatch priority across China's two major transmission operators, aligning with national policy to prioritize nuclear for baseload stability. Joint planning with these operators optimizes baseload scheduling and outage windows, reducing curtailment and enabling steady dispatch of CNNP units. Tight coupling ensures reliable integration of nuclear output from China's roughly 57 GW installed nuclear fleet (end-2024).

Regulators and safety authorities

Close collaboration with the NNSA and other agencies secures licensing, routine inspections and regulatory compliance for China National Nuclear Power, which operates about 55 reactors (~55 GW) with roughly 22 units under construction (IAEA/2024). Proactive engagement helps shape safety cases and drives continuous improvement in plant performance and emergency preparedness. This regulatory partnership builds public trust and supports operating license continuity, reducing shutdown risk and preserving revenue streams.

Fuel cycle and waste management partners

Long-term contracts with uranium miners, enrichers and fabricators secure feedstock for China National Nuclear Power as China’s nuclear fleet reached about 57 GW with roughly 21 reactors under construction at end-2024, lowering spot-price exposure. Partnerships for spent-fuel storage and back-end solutions shift lifecycle liabilities off balance sheets and reduce regulatory and disposal risk. Coordinated logistics across mining, enrichment and fuel fabrication cut downtime and mitigate cost volatility in fuel delivery.

- Long-term uranium, enrichment and fabrication contracts

- Back-end storage and disposal partnerships

- Integrated logistics to minimize downtime and price exposure

R&D institutes, universities, and international bodies

Integration, long-term fuel contracts and grid offtake de-risk 55 reactors

Deep CNNC integration, EPC/subsidiary linkages and long-term fuel contracts de-risk projects and finance, supporting China’s 55 reactors and 23 under construction in 2024. Grid partnerships (State Grid, China Southern) secure dispatch and offtake for ~57 GW fleet (end-2024). Regulatory and R&D ties (NNSA, CIAE, IAEA programs) speed licensing, safety upgrades and talent flow.

| Partner | Role | 2024 metric |

|---|---|---|

| CNNC group | EPC, financing, fuel | 55 reactors / 23 UC |

| State Grid | Offtake, dispatch | ~57 GW fleet |

| Uranium suppliers | Fuel security | Long-term contracts |

| CIAE/IAEA | R&D, safety | Joint programs |

What is included in the product

A comprehensive Business Model Canvas for China National Nuclear Power mapping all 9 blocks—customer segments, value propositions, channels, revenue streams, key partners, activities, resources, cost structure, and customer relationships—aligned with real-world nuclear operations and growth strategy. Ideal for investor presentations, it includes competitive advantage analysis and linked SWOT insights to support strategic decisions and funding discussions.

High-level, editable one-page snapshot of China National Nuclear Power’s business model that reduces analysis time and aligns stakeholders quickly for strategic decisions.

Activities

Investment and project development

Site selection, feasibility studies and permitting form the backbone of new-builds, with China operating about 55 reactors (~52 GW) and ~22 under construction (~25 GW) as of 2024, guiding regional grid, water and seismic assessments. Financial structuring commonly targets 60–70% debt in project finance to achieve bankability and allocate construction and market risks. Coordinated stakeholder management—central government, regulators, grid operators and local authorities—streamlines land, EPC contracts and off-take readiness for timely construction starts.

EPC management and commissioning

Oversee EPC with rigorous QA/QC aligned to China’s 2024 large-scale nuclear new-build program, enforcing vendor certification, weld inspection and materials traceability across GW-scale units. Schedule, cost and interface control manage multi‑billion‑dollar timelines and contractor interfaces to limit delays and claims. Commissioning executes hot functional tests, fuel loading and low‑power physics tests to validate performance and safety before grid synchronization.

Plant operations and maintenance

Operate reactors to high capacity factors with strict procedures; China had about 55 GW of nuclear capacity operational in 2024 and the national fleet averaged capacity factors above 80% under standardized safety protocols. Predictive and preventive maintenance using online monitoring and digital twins reduces forced outages and sustains reliability. Outage management schedules refueling and upgrades to minimize downtime and optimize LCOE.

Fuel cycle planning and logistics

Procure, fabricate, and deliver fuel assemblies on time for China’s fleet of 55 operational reactors (IAEA, June 2024), coordinating domestic manufacturers to meet outage windows and limit import dependence. Manage spent fuel handling and interim storage at site pools and centralized facilities, preparing for throughput growth from 23 reactors under construction. Optimize inventory with just-in-time deliveries plus buffer stocks sized to cover multi-month outages to balance cost and security.

- On-time delivery: align supply with outage schedules

- Spent fuel: site pools + centralized interim storage capacity planning

- Inventory: JIT + strategic buffers to minimize cost and enhance security

Safety, compliance, and continuous improvement

Conducts regular safety analyses, drills, and audits to meet CNNC and National Nuclear Safety Administration standards; China operated 55 commercial reactors by end-2024, underscoring scale and regulatory scrutiny.

Tracks KPIs and lessons learned (safety events per 10,000 reactor-hours, outage duration, maintenance cost per MW) to drive continuous improvement; transparent reporting preserves operating licenses and social license to operate.

- Safety audits: regulatory compliance

- KPI tracking: events per 10,000 reactor-hours

- Reporting: license and social license

China nuclear expansion: 55 reactors (~52 GW), 22 under build, 60–70% debt

Site selection, permitting and project finance (60–70% debt) drive new-build execution for China’s ~55 reactors (~52 GW) with ~22 under construction (~25 GW) in 2024.

EPC oversight, QA/QC, commissioning and schedule control limit delays on GW-scale units and manage multi‑billion‑dollar interfaces.

Operations focus on >80% fleet capacity factors, predictive maintenance, fuel supply coordination and spent-fuel interim storage planning.

| Metric | 2024 |

|---|---|

| Operational reactors | 55 (~52 GW) |

| Under construction | 22 (~25 GW) |

| Target debt | 60–70% |

| Avg capacity factor | >80% |

Full Version Awaits

Business Model Canvas

The document previewed here is the actual China National Nuclear Power Business Model Canvas, not a mockup or sample. When you purchase, you’ll receive this exact, fully formatted file with all sections included. It’s ready to download, edit, present, and apply—no surprises, just the real deliverable.

Description

Business Model Canvas: Strategic Blueprint for a Leading Chinese Nuclear Power Operator

Unlock the full strategic blueprint behind China National Nuclear Power with our Business Model Canvas. This concise, actionable canvas maps value propositions, key partnerships, revenue streams and risks—ideal for investors, consultants and strategists. Download the complete Word/Excel package to benchmark, plan and capitalize on industry insights.

Partnerships

CNNC group subsidiaries and SOE ecosystem

Deep integration with parent CNNC aligns strategy, financing and technology roadmaps within China’s state-owned nuclear ecosystem, supporting national targets as China operated 55 reactors and had 23 under construction in 2024. Subsidiaries such as CNPE (EPC), CNI (installation) and CNNC Uranium provide full‑lifecycle services from supply to build and fuel. This SOE network lowers coordination risk and accelerates deployment timelines.

Grid operators and dispatch centers

Partnerships with State Grid and China Southern Power Grid secure offtake and dispatch priority across China's two major transmission operators, aligning with national policy to prioritize nuclear for baseload stability. Joint planning with these operators optimizes baseload scheduling and outage windows, reducing curtailment and enabling steady dispatch of CNNP units. Tight coupling ensures reliable integration of nuclear output from China's roughly 57 GW installed nuclear fleet (end-2024).

Regulators and safety authorities

Close collaboration with the NNSA and other agencies secures licensing, routine inspections and regulatory compliance for China National Nuclear Power, which operates about 55 reactors (~55 GW) with roughly 22 units under construction (IAEA/2024). Proactive engagement helps shape safety cases and drives continuous improvement in plant performance and emergency preparedness. This regulatory partnership builds public trust and supports operating license continuity, reducing shutdown risk and preserving revenue streams.

Fuel cycle and waste management partners

Long-term contracts with uranium miners, enrichers and fabricators secure feedstock for China National Nuclear Power as China’s nuclear fleet reached about 57 GW with roughly 21 reactors under construction at end-2024, lowering spot-price exposure. Partnerships for spent-fuel storage and back-end solutions shift lifecycle liabilities off balance sheets and reduce regulatory and disposal risk. Coordinated logistics across mining, enrichment and fuel fabrication cut downtime and mitigate cost volatility in fuel delivery.

- Long-term uranium, enrichment and fabrication contracts

- Back-end storage and disposal partnerships

- Integrated logistics to minimize downtime and price exposure

R&D institutes, universities, and international bodies

Integration, long-term fuel contracts and grid offtake de-risk 55 reactors

Deep CNNC integration, EPC/subsidiary linkages and long-term fuel contracts de-risk projects and finance, supporting China’s 55 reactors and 23 under construction in 2024. Grid partnerships (State Grid, China Southern) secure dispatch and offtake for ~57 GW fleet (end-2024). Regulatory and R&D ties (NNSA, CIAE, IAEA programs) speed licensing, safety upgrades and talent flow.

| Partner | Role | 2024 metric |

|---|---|---|

| CNNC group | EPC, financing, fuel | 55 reactors / 23 UC |

| State Grid | Offtake, dispatch | ~57 GW fleet |

| Uranium suppliers | Fuel security | Long-term contracts |

| CIAE/IAEA | R&D, safety | Joint programs |

What is included in the product

A comprehensive Business Model Canvas for China National Nuclear Power mapping all 9 blocks—customer segments, value propositions, channels, revenue streams, key partners, activities, resources, cost structure, and customer relationships—aligned with real-world nuclear operations and growth strategy. Ideal for investor presentations, it includes competitive advantage analysis and linked SWOT insights to support strategic decisions and funding discussions.

High-level, editable one-page snapshot of China National Nuclear Power’s business model that reduces analysis time and aligns stakeholders quickly for strategic decisions.

Activities

Investment and project development

Site selection, feasibility studies and permitting form the backbone of new-builds, with China operating about 55 reactors (~52 GW) and ~22 under construction (~25 GW) as of 2024, guiding regional grid, water and seismic assessments. Financial structuring commonly targets 60–70% debt in project finance to achieve bankability and allocate construction and market risks. Coordinated stakeholder management—central government, regulators, grid operators and local authorities—streamlines land, EPC contracts and off-take readiness for timely construction starts.

EPC management and commissioning

Oversee EPC with rigorous QA/QC aligned to China’s 2024 large-scale nuclear new-build program, enforcing vendor certification, weld inspection and materials traceability across GW-scale units. Schedule, cost and interface control manage multi‑billion‑dollar timelines and contractor interfaces to limit delays and claims. Commissioning executes hot functional tests, fuel loading and low‑power physics tests to validate performance and safety before grid synchronization.

Plant operations and maintenance

Operate reactors to high capacity factors with strict procedures; China had about 55 GW of nuclear capacity operational in 2024 and the national fleet averaged capacity factors above 80% under standardized safety protocols. Predictive and preventive maintenance using online monitoring and digital twins reduces forced outages and sustains reliability. Outage management schedules refueling and upgrades to minimize downtime and optimize LCOE.

Fuel cycle planning and logistics

Procure, fabricate, and deliver fuel assemblies on time for China’s fleet of 55 operational reactors (IAEA, June 2024), coordinating domestic manufacturers to meet outage windows and limit import dependence. Manage spent fuel handling and interim storage at site pools and centralized facilities, preparing for throughput growth from 23 reactors under construction. Optimize inventory with just-in-time deliveries plus buffer stocks sized to cover multi-month outages to balance cost and security.

- On-time delivery: align supply with outage schedules

- Spent fuel: site pools + centralized interim storage capacity planning

- Inventory: JIT + strategic buffers to minimize cost and enhance security

Safety, compliance, and continuous improvement

Conducts regular safety analyses, drills, and audits to meet CNNC and National Nuclear Safety Administration standards; China operated 55 commercial reactors by end-2024, underscoring scale and regulatory scrutiny.

Tracks KPIs and lessons learned (safety events per 10,000 reactor-hours, outage duration, maintenance cost per MW) to drive continuous improvement; transparent reporting preserves operating licenses and social license to operate.

- Safety audits: regulatory compliance

- KPI tracking: events per 10,000 reactor-hours

- Reporting: license and social license

China nuclear expansion: 55 reactors (~52 GW), 22 under build, 60–70% debt

Site selection, permitting and project finance (60–70% debt) drive new-build execution for China’s ~55 reactors (~52 GW) with ~22 under construction (~25 GW) in 2024.

EPC oversight, QA/QC, commissioning and schedule control limit delays on GW-scale units and manage multi‑billion‑dollar interfaces.

Operations focus on >80% fleet capacity factors, predictive maintenance, fuel supply coordination and spent-fuel interim storage planning.

| Metric | 2024 |

|---|---|

| Operational reactors | 55 (~52 GW) |

| Under construction | 22 (~25 GW) |

| Target debt | 60–70% |

| Avg capacity factor | >80% |

Full Version Awaits

Business Model Canvas

The document previewed here is the actual China National Nuclear Power Business Model Canvas, not a mockup or sample. When you purchase, you’ll receive this exact, fully formatted file with all sections included. It’s ready to download, edit, present, and apply—no surprises, just the real deliverable.