China National Nuclear Power Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

China National Nuclear Power faces strong supplier influence, high regulatory barriers, and evolving substitute threats that shape its strategic outlook. Market rivalry is intense but cushioned by state backing and long-term power contracts. Buyer power remains moderate as utilities and grid operators dictate terms. This brief preview only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy insights.

Suppliers Bargaining Power

Narrow fuel vendor base

Qualified uranium and fabrication suppliers are few, concentrating bargaining power while CNNP relies mainly on domestic CNNC subsidiaries and limited international sources for enrichment and assemblies. China had about 55 operational reactors and 20+ under construction in 2024, anchoring steady fuel demand. Long-term contracts and state backing dampen price swings. Geopolitical risks and strict quality specs keep switching costs high.

State-integrated ecosystem

China National Nuclear Power benefits from a state-integrated ecosystem spanning mining, conversion, enrichment and fabrication, cutting external supplier leverage as China operated 55 reactors and had 22 under construction in 2024. Government coordination aligns pricing and availability with energy-security targets, while internal sourcing improves visibility and standardization across the fuel chain. Supplier bargaining power is therefore moderated by strong policy oversight and centralized planning.

Specialized heavy equipment

Large forgings, steam generators and reactor internals for CNNC projects come from a handful (3–5) of qualified OEMs; domestic champions Shanghai Electric and Dongfang Electric have reduced foreign reliance but face capacity constraints. Lead times for large forgings and SGs typically range 24–36 months, elevating schedule risk. Framework agreements signed in 2024 cap price escalation but do not resolve supply bottlenecks.

Technology licensing path

Legacy reliance on AP1000 (four Chinese units at Sanmen and Haiyang) has evolved toward domestically standardized HPR1000/CF3 platforms, cutting dependence on foreign IP while creating design lock-in that binds buyers to specific supplier ecosystems; rigorous qualification and safety documentation produce multi-year supplier-substitution timelines.

- AP1000 units in China: 4 (Sanmen, Haiyang)

- Shift to HPR1000/CF3 drives IP localization

- Design lock-in increases supplier switching costs

- Qualification/safety docs cause multi-year lead times

Fuel cycle and waste services

Back-end services for spent fuel handling and future reprocessing are highly specialized, giving suppliers elevated technical clout; China’s nuclear fleet exceeds 50 reactors as of 2024, sustaining steady spent-fuel volumes and long-term service demand. Limited international commercial reprocessing capacity and tight regulatory oversight in China constrain supplier turnover and raise switching costs, while long-dated contracts (decades) limit renegotiation flexibility. State planning and mandated frameworks, however, partially neutralize supplier pricing power by fixing standards, procurement channels and cost-recovery rules.

- Specialization: few qualified back-end providers

- Scale: China >50 reactors (2024) sustains demand

- Contracts: multi-decade commitments reduce repricing

- State control: planning and mandated frameworks curb pricing

Few suppliers, 55 reactors, 24-36mo lead times

Qualified uranium/enrichment/fabrication suppliers are few, so bargaining power is concentrated while CNNP leans on CNNC and limited imports; China had 55 operational reactors and 22 under construction in 2024, supporting steady fuel demand. Long-term (decades) contracts and state planning cap price volatility, but 24–36 month lead times for large forgings and design lock-in keep switching costs high.

| Metric | Value |

|---|---|

| Operational reactors (2024) | 55 |

| Under construction (2024) | 22 |

| Qualified OEMs for forgings | 3–5 |

| Forgings/SG lead time | 24–36 months |

| Contract duration | Decades |

What is included in the product

Tailored Porter's Five Forces analysis for China National Nuclear Power, uncovering competitive drivers, supplier and buyer influence, entry barriers, substitutes, and emerging threats to its market position.

Clear, one-sheet Porter's Five Forces for China National Nuclear Power—instantly visualized with a spider chart and customizable pressure levels to adapt to regulatory shifts, new entrants, or fuel-market changes for quick deck-ready decisions.

Customers Bargaining Power

Few grid buyers

State Grid and China Southern Grid account for over 80% of China's transmission and offtake, concentrating demand and raising coordination power among buyers. Centralized dispatch and NEA planning reduce transactional bargaining but impose strict technical and grid-compatibility requirements on nuclear units. Tariffs and volumes are policy-set by NDRC/NEA rather than purely negotiated; nuclear supplied about 5% of China's electricity in 2024, limiting price leverage.

Regulated nuclear tariffs

NDRC and provincial authorities set benchmark nuclear on-grid prices (national reference about 0.45 RMB/kWh in 2024), so buyers cannot freely negotiate market rates. Cost pass-through is constrained by multi-month regulatory reviews and approval processes, limiting rapid tariff adjustments. Stable, policy-driven tariffs lower buyer leverage for opportunistic discounts, with changes reflecting national energy and safety priorities rather than bilateral bargaining.

Baseload reliability premium

Nuclear provides firm, low-carbon baseload supporting grid stability as China expands renewables; reactors typically run at >90% capacity factors versus solar 10–25% and wind 20–40%, making substitution difficult. Limited alternatives for steady baseload narrow buyers' leverage over pricing and contract terms. Lower curtailment risk than intermittent sources reinforces a baseload reliability premium and reduces effective buyer power.

Long-term PPAs and planning

Long-lived nuclear assets (design lives 40–60 years) typically secure multi-decade PPAs (commonly 20–40 years), aligning with planning horizons and reducing renegotiation frequency; predictable baseload demand and grid integration needs shift buyer focus to reliability and China’s 2060 carbon neutrality targets rather than short-term price squeezing, which lowers customers’ bargaining intensity.

- Design life: 40–60 years

- PPA length: 20–40 years

- Policy anchor: China 2060 neutrality

Regional demand growth

- Regional hubs: concentrated industrial demand

- 55 GW: nuclear capacity end-2023

- Tight capacity lowers buyers’ leverage

- Oversupply pockets pressure margins

>80% buyers; tariffs ~0.45 RMB/kWh; nuclear ~5%

Buyers concentrated (State Grid + China Southern >80% of offtake) but tariffs/policy (NDRC/NEA) set pricing (~0.45 RMB/kWh national reference in 2024), limiting bilateral leverage. Nuclear ~5% of electricity in 2024 with ~55 GW capacity end-2023 and >90% capacity factors, reducing substitution and boosting seller bargaining. Long PPAs (20–40 years) and 40–60 year plant lives lower renegotiation frequency.

| Metric | Value | Note |

|---|---|---|

| Buyer concentration | >80% | State Grid + China Southern |

| On-grid price (2024) | ~0.45 RMB/kWh | NDRC/NEA reference |

| Nuclear share (2024) | ~5% | National electricity |

| Capacity (end-2023) | ~55 GW | Operational |

What You See Is What You Get

China National Nuclear Power Porter's Five Forces Analysis

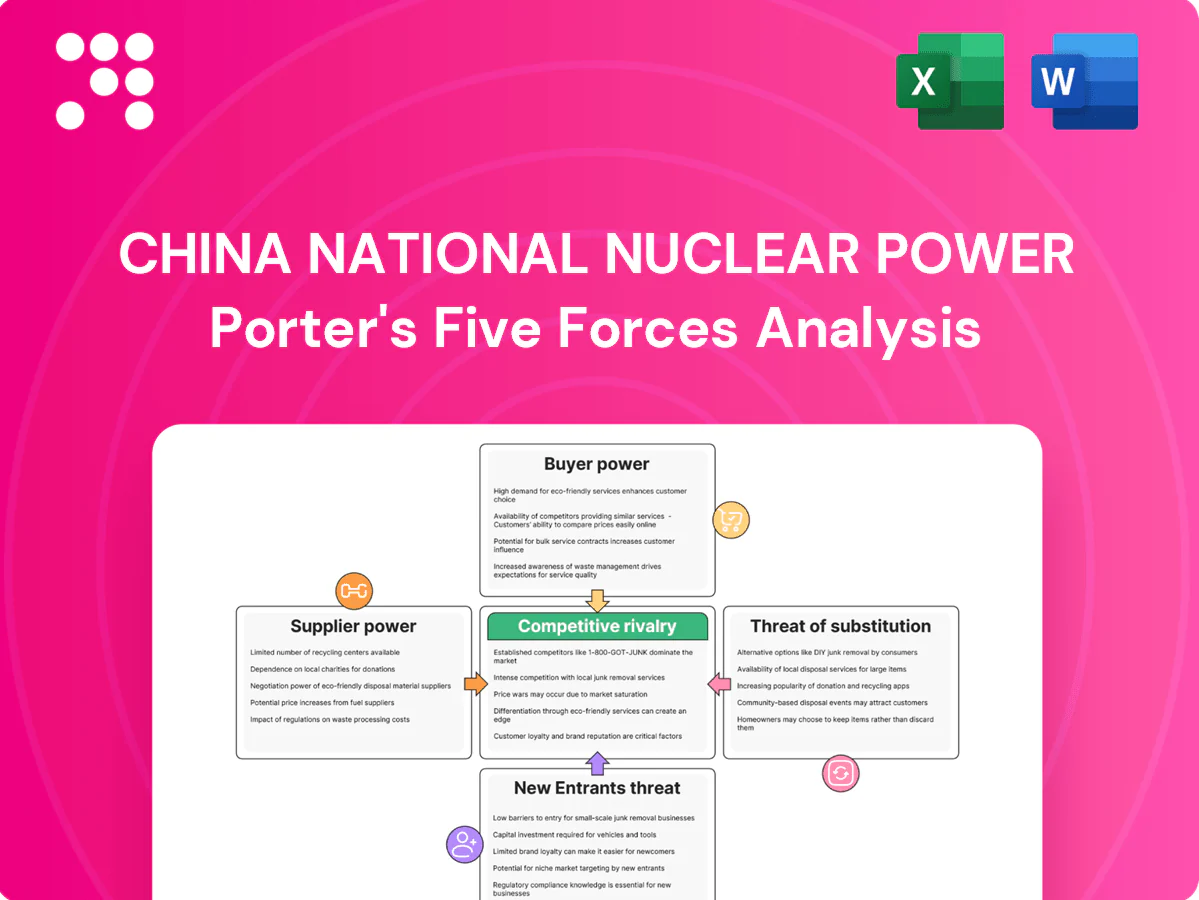

This Porter's Five Forces analysis of China National Nuclear Power assesses supplier and buyer bargaining power, the threat of new entrants and substitutes, and competitive rivalry to clarify industry dynamics and profit potential. It highlights supplier concentration in nuclear components, regulated market entry barriers, limited direct substitutes, and intense state-backed competition. Strategic implications and mitigation actions are provided. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders.

Go Beyond the Preview—Access the Full Strategic Report

China National Nuclear Power faces strong supplier influence, high regulatory barriers, and evolving substitute threats that shape its strategic outlook. Market rivalry is intense but cushioned by state backing and long-term power contracts. Buyer power remains moderate as utilities and grid operators dictate terms. This brief preview only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy insights.

Suppliers Bargaining Power

Narrow fuel vendor base

Qualified uranium and fabrication suppliers are few, concentrating bargaining power while CNNP relies mainly on domestic CNNC subsidiaries and limited international sources for enrichment and assemblies. China had about 55 operational reactors and 20+ under construction in 2024, anchoring steady fuel demand. Long-term contracts and state backing dampen price swings. Geopolitical risks and strict quality specs keep switching costs high.

State-integrated ecosystem

China National Nuclear Power benefits from a state-integrated ecosystem spanning mining, conversion, enrichment and fabrication, cutting external supplier leverage as China operated 55 reactors and had 22 under construction in 2024. Government coordination aligns pricing and availability with energy-security targets, while internal sourcing improves visibility and standardization across the fuel chain. Supplier bargaining power is therefore moderated by strong policy oversight and centralized planning.

Specialized heavy equipment

Large forgings, steam generators and reactor internals for CNNC projects come from a handful (3–5) of qualified OEMs; domestic champions Shanghai Electric and Dongfang Electric have reduced foreign reliance but face capacity constraints. Lead times for large forgings and SGs typically range 24–36 months, elevating schedule risk. Framework agreements signed in 2024 cap price escalation but do not resolve supply bottlenecks.

Technology licensing path

Legacy reliance on AP1000 (four Chinese units at Sanmen and Haiyang) has evolved toward domestically standardized HPR1000/CF3 platforms, cutting dependence on foreign IP while creating design lock-in that binds buyers to specific supplier ecosystems; rigorous qualification and safety documentation produce multi-year supplier-substitution timelines.

- AP1000 units in China: 4 (Sanmen, Haiyang)

- Shift to HPR1000/CF3 drives IP localization

- Design lock-in increases supplier switching costs

- Qualification/safety docs cause multi-year lead times

Fuel cycle and waste services

Back-end services for spent fuel handling and future reprocessing are highly specialized, giving suppliers elevated technical clout; China’s nuclear fleet exceeds 50 reactors as of 2024, sustaining steady spent-fuel volumes and long-term service demand. Limited international commercial reprocessing capacity and tight regulatory oversight in China constrain supplier turnover and raise switching costs, while long-dated contracts (decades) limit renegotiation flexibility. State planning and mandated frameworks, however, partially neutralize supplier pricing power by fixing standards, procurement channels and cost-recovery rules.

- Specialization: few qualified back-end providers

- Scale: China >50 reactors (2024) sustains demand

- Contracts: multi-decade commitments reduce repricing

- State control: planning and mandated frameworks curb pricing

Few suppliers, 55 reactors, 24-36mo lead times

Qualified uranium/enrichment/fabrication suppliers are few, so bargaining power is concentrated while CNNP leans on CNNC and limited imports; China had 55 operational reactors and 22 under construction in 2024, supporting steady fuel demand. Long-term (decades) contracts and state planning cap price volatility, but 24–36 month lead times for large forgings and design lock-in keep switching costs high.

| Metric | Value |

|---|---|

| Operational reactors (2024) | 55 |

| Under construction (2024) | 22 |

| Qualified OEMs for forgings | 3–5 |

| Forgings/SG lead time | 24–36 months |

| Contract duration | Decades |

What is included in the product

Tailored Porter's Five Forces analysis for China National Nuclear Power, uncovering competitive drivers, supplier and buyer influence, entry barriers, substitutes, and emerging threats to its market position.

Clear, one-sheet Porter's Five Forces for China National Nuclear Power—instantly visualized with a spider chart and customizable pressure levels to adapt to regulatory shifts, new entrants, or fuel-market changes for quick deck-ready decisions.

Customers Bargaining Power

Few grid buyers

State Grid and China Southern Grid account for over 80% of China's transmission and offtake, concentrating demand and raising coordination power among buyers. Centralized dispatch and NEA planning reduce transactional bargaining but impose strict technical and grid-compatibility requirements on nuclear units. Tariffs and volumes are policy-set by NDRC/NEA rather than purely negotiated; nuclear supplied about 5% of China's electricity in 2024, limiting price leverage.

Regulated nuclear tariffs

NDRC and provincial authorities set benchmark nuclear on-grid prices (national reference about 0.45 RMB/kWh in 2024), so buyers cannot freely negotiate market rates. Cost pass-through is constrained by multi-month regulatory reviews and approval processes, limiting rapid tariff adjustments. Stable, policy-driven tariffs lower buyer leverage for opportunistic discounts, with changes reflecting national energy and safety priorities rather than bilateral bargaining.

Baseload reliability premium

Nuclear provides firm, low-carbon baseload supporting grid stability as China expands renewables; reactors typically run at >90% capacity factors versus solar 10–25% and wind 20–40%, making substitution difficult. Limited alternatives for steady baseload narrow buyers' leverage over pricing and contract terms. Lower curtailment risk than intermittent sources reinforces a baseload reliability premium and reduces effective buyer power.

Long-term PPAs and planning

Long-lived nuclear assets (design lives 40–60 years) typically secure multi-decade PPAs (commonly 20–40 years), aligning with planning horizons and reducing renegotiation frequency; predictable baseload demand and grid integration needs shift buyer focus to reliability and China’s 2060 carbon neutrality targets rather than short-term price squeezing, which lowers customers’ bargaining intensity.

- Design life: 40–60 years

- PPA length: 20–40 years

- Policy anchor: China 2060 neutrality

Regional demand growth

- Regional hubs: concentrated industrial demand

- 55 GW: nuclear capacity end-2023

- Tight capacity lowers buyers’ leverage

- Oversupply pockets pressure margins

>80% buyers; tariffs ~0.45 RMB/kWh; nuclear ~5%

Buyers concentrated (State Grid + China Southern >80% of offtake) but tariffs/policy (NDRC/NEA) set pricing (~0.45 RMB/kWh national reference in 2024), limiting bilateral leverage. Nuclear ~5% of electricity in 2024 with ~55 GW capacity end-2023 and >90% capacity factors, reducing substitution and boosting seller bargaining. Long PPAs (20–40 years) and 40–60 year plant lives lower renegotiation frequency.

| Metric | Value | Note |

|---|---|---|

| Buyer concentration | >80% | State Grid + China Southern |

| On-grid price (2024) | ~0.45 RMB/kWh | NDRC/NEA reference |

| Nuclear share (2024) | ~5% | National electricity |

| Capacity (end-2023) | ~55 GW | Operational |

What You See Is What You Get

China National Nuclear Power Porter's Five Forces Analysis

This Porter's Five Forces analysis of China National Nuclear Power assesses supplier and buyer bargaining power, the threat of new entrants and substitutes, and competitive rivalry to clarify industry dynamics and profit potential. It highlights supplier concentration in nuclear components, regulated market entry barriers, limited direct substitutes, and intense state-backed competition. Strategic implications and mitigation actions are provided. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

China National Nuclear Power faces strong supplier influence, high regulatory barriers, and evolving substitute threats that shape its strategic outlook. Market rivalry is intense but cushioned by state backing and long-term power contracts. Buyer power remains moderate as utilities and grid operators dictate terms. This brief preview only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy insights.

Suppliers Bargaining Power

Narrow fuel vendor base

Qualified uranium and fabrication suppliers are few, concentrating bargaining power while CNNP relies mainly on domestic CNNC subsidiaries and limited international sources for enrichment and assemblies. China had about 55 operational reactors and 20+ under construction in 2024, anchoring steady fuel demand. Long-term contracts and state backing dampen price swings. Geopolitical risks and strict quality specs keep switching costs high.

State-integrated ecosystem

China National Nuclear Power benefits from a state-integrated ecosystem spanning mining, conversion, enrichment and fabrication, cutting external supplier leverage as China operated 55 reactors and had 22 under construction in 2024. Government coordination aligns pricing and availability with energy-security targets, while internal sourcing improves visibility and standardization across the fuel chain. Supplier bargaining power is therefore moderated by strong policy oversight and centralized planning.

Specialized heavy equipment

Large forgings, steam generators and reactor internals for CNNC projects come from a handful (3–5) of qualified OEMs; domestic champions Shanghai Electric and Dongfang Electric have reduced foreign reliance but face capacity constraints. Lead times for large forgings and SGs typically range 24–36 months, elevating schedule risk. Framework agreements signed in 2024 cap price escalation but do not resolve supply bottlenecks.

Technology licensing path

Legacy reliance on AP1000 (four Chinese units at Sanmen and Haiyang) has evolved toward domestically standardized HPR1000/CF3 platforms, cutting dependence on foreign IP while creating design lock-in that binds buyers to specific supplier ecosystems; rigorous qualification and safety documentation produce multi-year supplier-substitution timelines.

- AP1000 units in China: 4 (Sanmen, Haiyang)

- Shift to HPR1000/CF3 drives IP localization

- Design lock-in increases supplier switching costs

- Qualification/safety docs cause multi-year lead times

Fuel cycle and waste services

Back-end services for spent fuel handling and future reprocessing are highly specialized, giving suppliers elevated technical clout; China’s nuclear fleet exceeds 50 reactors as of 2024, sustaining steady spent-fuel volumes and long-term service demand. Limited international commercial reprocessing capacity and tight regulatory oversight in China constrain supplier turnover and raise switching costs, while long-dated contracts (decades) limit renegotiation flexibility. State planning and mandated frameworks, however, partially neutralize supplier pricing power by fixing standards, procurement channels and cost-recovery rules.

- Specialization: few qualified back-end providers

- Scale: China >50 reactors (2024) sustains demand

- Contracts: multi-decade commitments reduce repricing

- State control: planning and mandated frameworks curb pricing

Few suppliers, 55 reactors, 24-36mo lead times

Qualified uranium/enrichment/fabrication suppliers are few, so bargaining power is concentrated while CNNP leans on CNNC and limited imports; China had 55 operational reactors and 22 under construction in 2024, supporting steady fuel demand. Long-term (decades) contracts and state planning cap price volatility, but 24–36 month lead times for large forgings and design lock-in keep switching costs high.

| Metric | Value |

|---|---|

| Operational reactors (2024) | 55 |

| Under construction (2024) | 22 |

| Qualified OEMs for forgings | 3–5 |

| Forgings/SG lead time | 24–36 months |

| Contract duration | Decades |

What is included in the product

Tailored Porter's Five Forces analysis for China National Nuclear Power, uncovering competitive drivers, supplier and buyer influence, entry barriers, substitutes, and emerging threats to its market position.

Clear, one-sheet Porter's Five Forces for China National Nuclear Power—instantly visualized with a spider chart and customizable pressure levels to adapt to regulatory shifts, new entrants, or fuel-market changes for quick deck-ready decisions.

Customers Bargaining Power

Few grid buyers

State Grid and China Southern Grid account for over 80% of China's transmission and offtake, concentrating demand and raising coordination power among buyers. Centralized dispatch and NEA planning reduce transactional bargaining but impose strict technical and grid-compatibility requirements on nuclear units. Tariffs and volumes are policy-set by NDRC/NEA rather than purely negotiated; nuclear supplied about 5% of China's electricity in 2024, limiting price leverage.

Regulated nuclear tariffs

NDRC and provincial authorities set benchmark nuclear on-grid prices (national reference about 0.45 RMB/kWh in 2024), so buyers cannot freely negotiate market rates. Cost pass-through is constrained by multi-month regulatory reviews and approval processes, limiting rapid tariff adjustments. Stable, policy-driven tariffs lower buyer leverage for opportunistic discounts, with changes reflecting national energy and safety priorities rather than bilateral bargaining.

Baseload reliability premium

Nuclear provides firm, low-carbon baseload supporting grid stability as China expands renewables; reactors typically run at >90% capacity factors versus solar 10–25% and wind 20–40%, making substitution difficult. Limited alternatives for steady baseload narrow buyers' leverage over pricing and contract terms. Lower curtailment risk than intermittent sources reinforces a baseload reliability premium and reduces effective buyer power.

Long-term PPAs and planning

Long-lived nuclear assets (design lives 40–60 years) typically secure multi-decade PPAs (commonly 20–40 years), aligning with planning horizons and reducing renegotiation frequency; predictable baseload demand and grid integration needs shift buyer focus to reliability and China’s 2060 carbon neutrality targets rather than short-term price squeezing, which lowers customers’ bargaining intensity.

- Design life: 40–60 years

- PPA length: 20–40 years

- Policy anchor: China 2060 neutrality

Regional demand growth

- Regional hubs: concentrated industrial demand

- 55 GW: nuclear capacity end-2023

- Tight capacity lowers buyers’ leverage

- Oversupply pockets pressure margins

>80% buyers; tariffs ~0.45 RMB/kWh; nuclear ~5%

Buyers concentrated (State Grid + China Southern >80% of offtake) but tariffs/policy (NDRC/NEA) set pricing (~0.45 RMB/kWh national reference in 2024), limiting bilateral leverage. Nuclear ~5% of electricity in 2024 with ~55 GW capacity end-2023 and >90% capacity factors, reducing substitution and boosting seller bargaining. Long PPAs (20–40 years) and 40–60 year plant lives lower renegotiation frequency.

| Metric | Value | Note |

|---|---|---|

| Buyer concentration | >80% | State Grid + China Southern |

| On-grid price (2024) | ~0.45 RMB/kWh | NDRC/NEA reference |

| Nuclear share (2024) | ~5% | National electricity |

| Capacity (end-2023) | ~55 GW | Operational |

What You See Is What You Get

China National Nuclear Power Porter's Five Forces Analysis

This Porter's Five Forces analysis of China National Nuclear Power assesses supplier and buyer bargaining power, the threat of new entrants and substitutes, and competitive rivalry to clarify industry dynamics and profit potential. It highlights supplier concentration in nuclear components, regulated market entry barriers, limited direct substitutes, and intense state-backed competition. Strategic implications and mitigation actions are provided. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders.