Canadian National Railway Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

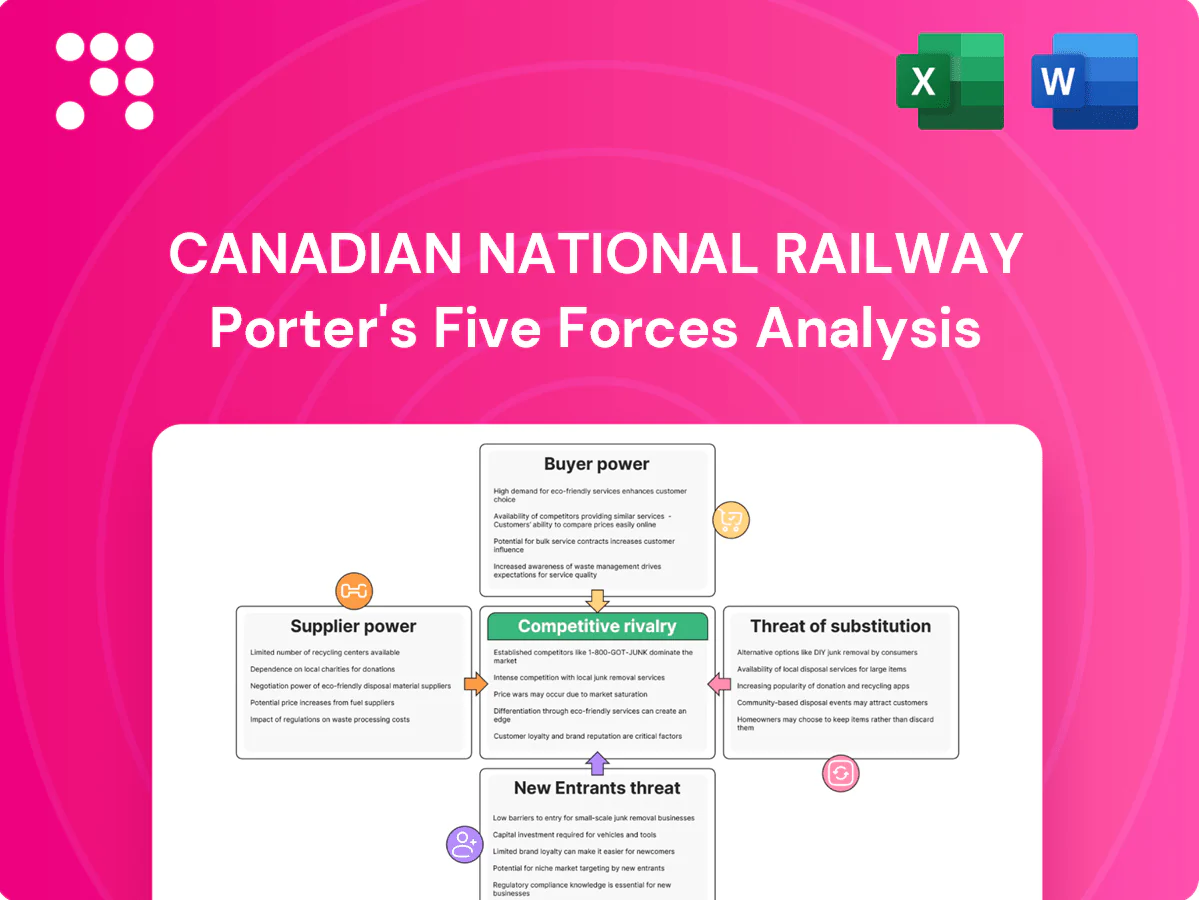

Canadian National Railway faces moderate supplier power, high buyer dependence from freight shippers, and intense rivalry driven by scale and pricing. Barriers to entry are strong, yet regulatory shifts and intermodal competition pose growing threats. This snapshot highlights strategic pressure points and operational strengths. Unlock the full Porter's Five Forces Analysis for CN to get detailed ratings, visuals, and actionable strategy insights.

Suppliers Bargaining Power

Concentrated locomotive and parts OEMs

As of 2024, locomotive OEMs are concentrated—notably Wabtec (including GE Transportation) and Progress Rail/EMD—limiting CN’s alternative sources and strengthening OEM pricing power. Specialized parts, proprietary software and compatibility constraints increase vendor lock-in. Long equipment lifecycles and stringent certification add high switching costs. CN mitigates through long-term contracts, fleet standardization and robust in-house maintenance capacity.

Fuel and energy cost volatility

Fuel is a major input for CN, typically 10-15% of operating expenses, with global crude (Brent averaged about $86/bbl in 2024) driving price swings and limiting suppliers' direct bargaining power while pressuring margins. Fuel surcharges offset spikes but often lag market moves. Energy transition pilots (renewable diesel, battery/hybrid trials) create new vendor links. Hedging plus PSR and trip-optimizer efficiency reduce net exposure.

Labor unions and skill scarcity

Rail operations rely on unionized, safety-critical labor, giving organized groups significant leverage over wages and work rules; CN reported about 22,400 employees in 2024, most covered by collective agreements. Tight labor markets and onerous training/licensing raise switching costs and slow recruitments. Work stoppages risk service disruption and customer churn, so CN invests in workforce relations, automation and training to rebalance bargaining power.

Railcar leasing and specialty equipment

For certain commodities and seasonality CN depends on leased railcars and specialty assets; lessors tightened terms as utilization climbed above 90% in 2024, boosting supplier power. Custom equipment such as modern tank cars meeting TC/DOT standards narrows supplier choice and raises replacement costs. CN mitigates cyclicality via fleet diversification and multi-year leases and capex to own more assets.

- Leased-dependency: high during peak grain/oil seasons

- Utilization: >90% in 2024 increases lessor leverage

- Mitigation: multi-year leases, diversified fleet, increased ownership capex

Digital systems and signaling vendors

PTC/ETCS-like onboard systems, dispatch software and telematics are supplied by a few specialized vendors (notably Wabtec, Siemens, Alstom), creating integration lock-in and limited substitutability.

Cybersecurity and safety certifications (SIL/EN standards) raise switching costs; vendor consolidation increases pricing and roadmap leverage, while CN mitigates risk via modular architectures, open APIs and negotiated SLAs and integration pilots.

- specialized vendors: 3 dominant suppliers

- barriers: safety/cyber certifications

- CN response: modular design, APIs, SLAs

OEM concentration raises leverage; fuel $86/bbl, labor pressure

Supplier power is moderate-high: locomotive OEMs concentrated (Wabtec, Progress Rail), PTC/telematics vendors ~3 dominant, raising lock-in and pricing leverage. Fuel (~10–15% of opex) and Brent ~$86/bbl (2024) drive costs but are hedged; leased-railcar utilization >90% in 2024 tightened lessor terms. Unionized labor (~22,400 employees) adds bargaining leverage and switching costs.

| Category | Metric | 2024 |

|---|---|---|

| OEM concentration | Top suppliers | 2–3 firms |

| Fuel | Share of opex / Brent | 10–15% / $86/bbl |

| Labor | Employees (unionized) | 22,400 |

| Railcars | Utilization | >90% |

What is included in the product

Comprehensive Porter's Five Forces review tailored to Canadian National Railway, detailing competitive rivalry, supplier and buyer power, entry barriers, substitutes and disruptive threats, with strategic implications for pricing, profitability and market positioning.

Concise Porter's Five Forces for Canadian National Railway—one-sheet clarity to spot competitive pressures, customize intensity by scenario, and drop directly into decks for fast, board-ready strategy decisions.

Customers Bargaining Power

Large, concentrated shippers

Bulk producers, ports and automotive OEMs are sizable CN accounts that leverage large volumes to negotiate rates and service levels, especially where alternate routings or carriers exist. Their multi-year contracts, commonly 3–7 years, balance revenue stability and pricing pressure. CN counters with national network reach, schedule reliability and integrated logistics solutions to retain these high-volume shippers.

Intermodal customers with modal options

Intermodal BCOs and IMCs can shift to long‑haul trucking—trucks move roughly 70% of US freight by value—so price/service gaps heighten buyer power; nearshoring and inventory strategies let shippers reconfigure lanes quickly. CN’s network of over 20,000 route miles and extensive port access plus inland terminals create customer stickiness, while service metrics and guaranteed capacity contracts blunt switching.

Regulated service obligations and remedies

CTA in Canada and the U.S. STB provide formal dispute-resolution powers and can order remedies such as reciprocal switching, while mandated carrier performance reporting increases transparency and gives shippers evidentiary leverage. These regulatory levers moderate CN’s pricing discretion and can constrain unilateral rate moves. In 2024 CN continued to submit regulator-required performance reports and engaged proactively with shippers to manage compliance and commercial disputes.

Commodity price cyclicality

- Commodity cyclicality raises renegotiation risk

- Dynamic pricing cushions margin impact

- Logistics/storage increase switching costs

Switching costs vary by commodity

Unit-train bulk flows (e.g., grain, coal) face materially higher switching costs than container freight, giving shippers less leverage; CN’s roughly 20,000-route-mile North American network and dedicated corridors for unit trains limit feasible alternatives. Where CN’s network overlaps with competitors, customers can play carriers off each other and use joint-line moves or interchanges to lower costs. CN leverages unique corridors and origin-destination density to retain pricing power.

- Unit-train switching costs: high

- Container switching: lower, more competition

- Network overlaps enable buyer leverage

- Joint-line/interchange provide alternatives

- CN unique corridors reduce buyer power

Bulk shippers' multi-year leverage (3–7 yrs) vs intermodal switching; trucking ~70%

Large bulk shippers and ports wield strong leverage via volume and 3–7 year contracts, constraining short-term rates. Intermodal shippers face lower switching costs given trucking's ~70% US freight-by-value share, boosting buyer power. Regulatory oversight (CTA/STB) and CN’s ~19,500 route miles (2024) plus logistics services counterbalance shipper leverage.

| Metric | 2024 |

|---|---|

| Route miles | 19,500 |

| Contract length | 3–7 yrs |

| Truck freight share (US) | ~70% |

Full Version Awaits

Canadian National Railway Porter's Five Forces Analysis

This Porter’s Five Forces analysis of Canadian National Railway examines competitive rivalry, supplier and buyer power, threat of new entrants, and substitutes, highlighting rail-specific barriers and regulatory influences. It assesses CN’s strategic positioning, margin drivers, and vulnerability to fuel and labor dynamics. The analysis includes actionable insights for investors and managers. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders.

A Must-Have Tool for Decision-Makers

Canadian National Railway faces moderate supplier power, high buyer dependence from freight shippers, and intense rivalry driven by scale and pricing. Barriers to entry are strong, yet regulatory shifts and intermodal competition pose growing threats. This snapshot highlights strategic pressure points and operational strengths. Unlock the full Porter's Five Forces Analysis for CN to get detailed ratings, visuals, and actionable strategy insights.

Suppliers Bargaining Power

Concentrated locomotive and parts OEMs

As of 2024, locomotive OEMs are concentrated—notably Wabtec (including GE Transportation) and Progress Rail/EMD—limiting CN’s alternative sources and strengthening OEM pricing power. Specialized parts, proprietary software and compatibility constraints increase vendor lock-in. Long equipment lifecycles and stringent certification add high switching costs. CN mitigates through long-term contracts, fleet standardization and robust in-house maintenance capacity.

Fuel and energy cost volatility

Fuel is a major input for CN, typically 10-15% of operating expenses, with global crude (Brent averaged about $86/bbl in 2024) driving price swings and limiting suppliers' direct bargaining power while pressuring margins. Fuel surcharges offset spikes but often lag market moves. Energy transition pilots (renewable diesel, battery/hybrid trials) create new vendor links. Hedging plus PSR and trip-optimizer efficiency reduce net exposure.

Labor unions and skill scarcity

Rail operations rely on unionized, safety-critical labor, giving organized groups significant leverage over wages and work rules; CN reported about 22,400 employees in 2024, most covered by collective agreements. Tight labor markets and onerous training/licensing raise switching costs and slow recruitments. Work stoppages risk service disruption and customer churn, so CN invests in workforce relations, automation and training to rebalance bargaining power.

Railcar leasing and specialty equipment

For certain commodities and seasonality CN depends on leased railcars and specialty assets; lessors tightened terms as utilization climbed above 90% in 2024, boosting supplier power. Custom equipment such as modern tank cars meeting TC/DOT standards narrows supplier choice and raises replacement costs. CN mitigates cyclicality via fleet diversification and multi-year leases and capex to own more assets.

- Leased-dependency: high during peak grain/oil seasons

- Utilization: >90% in 2024 increases lessor leverage

- Mitigation: multi-year leases, diversified fleet, increased ownership capex

Digital systems and signaling vendors

PTC/ETCS-like onboard systems, dispatch software and telematics are supplied by a few specialized vendors (notably Wabtec, Siemens, Alstom), creating integration lock-in and limited substitutability.

Cybersecurity and safety certifications (SIL/EN standards) raise switching costs; vendor consolidation increases pricing and roadmap leverage, while CN mitigates risk via modular architectures, open APIs and negotiated SLAs and integration pilots.

- specialized vendors: 3 dominant suppliers

- barriers: safety/cyber certifications

- CN response: modular design, APIs, SLAs

OEM concentration raises leverage; fuel $86/bbl, labor pressure

Supplier power is moderate-high: locomotive OEMs concentrated (Wabtec, Progress Rail), PTC/telematics vendors ~3 dominant, raising lock-in and pricing leverage. Fuel (~10–15% of opex) and Brent ~$86/bbl (2024) drive costs but are hedged; leased-railcar utilization >90% in 2024 tightened lessor terms. Unionized labor (~22,400 employees) adds bargaining leverage and switching costs.

| Category | Metric | 2024 |

|---|---|---|

| OEM concentration | Top suppliers | 2–3 firms |

| Fuel | Share of opex / Brent | 10–15% / $86/bbl |

| Labor | Employees (unionized) | 22,400 |

| Railcars | Utilization | >90% |

What is included in the product

Comprehensive Porter's Five Forces review tailored to Canadian National Railway, detailing competitive rivalry, supplier and buyer power, entry barriers, substitutes and disruptive threats, with strategic implications for pricing, profitability and market positioning.

Concise Porter's Five Forces for Canadian National Railway—one-sheet clarity to spot competitive pressures, customize intensity by scenario, and drop directly into decks for fast, board-ready strategy decisions.

Customers Bargaining Power

Large, concentrated shippers

Bulk producers, ports and automotive OEMs are sizable CN accounts that leverage large volumes to negotiate rates and service levels, especially where alternate routings or carriers exist. Their multi-year contracts, commonly 3–7 years, balance revenue stability and pricing pressure. CN counters with national network reach, schedule reliability and integrated logistics solutions to retain these high-volume shippers.

Intermodal customers with modal options

Intermodal BCOs and IMCs can shift to long‑haul trucking—trucks move roughly 70% of US freight by value—so price/service gaps heighten buyer power; nearshoring and inventory strategies let shippers reconfigure lanes quickly. CN’s network of over 20,000 route miles and extensive port access plus inland terminals create customer stickiness, while service metrics and guaranteed capacity contracts blunt switching.

Regulated service obligations and remedies

CTA in Canada and the U.S. STB provide formal dispute-resolution powers and can order remedies such as reciprocal switching, while mandated carrier performance reporting increases transparency and gives shippers evidentiary leverage. These regulatory levers moderate CN’s pricing discretion and can constrain unilateral rate moves. In 2024 CN continued to submit regulator-required performance reports and engaged proactively with shippers to manage compliance and commercial disputes.

Commodity price cyclicality

- Commodity cyclicality raises renegotiation risk

- Dynamic pricing cushions margin impact

- Logistics/storage increase switching costs

Switching costs vary by commodity

Unit-train bulk flows (e.g., grain, coal) face materially higher switching costs than container freight, giving shippers less leverage; CN’s roughly 20,000-route-mile North American network and dedicated corridors for unit trains limit feasible alternatives. Where CN’s network overlaps with competitors, customers can play carriers off each other and use joint-line moves or interchanges to lower costs. CN leverages unique corridors and origin-destination density to retain pricing power.

- Unit-train switching costs: high

- Container switching: lower, more competition

- Network overlaps enable buyer leverage

- Joint-line/interchange provide alternatives

- CN unique corridors reduce buyer power

Bulk shippers' multi-year leverage (3–7 yrs) vs intermodal switching; trucking ~70%

Large bulk shippers and ports wield strong leverage via volume and 3–7 year contracts, constraining short-term rates. Intermodal shippers face lower switching costs given trucking's ~70% US freight-by-value share, boosting buyer power. Regulatory oversight (CTA/STB) and CN’s ~19,500 route miles (2024) plus logistics services counterbalance shipper leverage.

| Metric | 2024 |

|---|---|

| Route miles | 19,500 |

| Contract length | 3–7 yrs |

| Truck freight share (US) | ~70% |

Full Version Awaits

Canadian National Railway Porter's Five Forces Analysis

This Porter’s Five Forces analysis of Canadian National Railway examines competitive rivalry, supplier and buyer power, threat of new entrants, and substitutes, highlighting rail-specific barriers and regulatory influences. It assesses CN’s strategic positioning, margin drivers, and vulnerability to fuel and labor dynamics. The analysis includes actionable insights for investors and managers. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Canadian National Railway faces moderate supplier power, high buyer dependence from freight shippers, and intense rivalry driven by scale and pricing. Barriers to entry are strong, yet regulatory shifts and intermodal competition pose growing threats. This snapshot highlights strategic pressure points and operational strengths. Unlock the full Porter's Five Forces Analysis for CN to get detailed ratings, visuals, and actionable strategy insights.

Suppliers Bargaining Power

Concentrated locomotive and parts OEMs

As of 2024, locomotive OEMs are concentrated—notably Wabtec (including GE Transportation) and Progress Rail/EMD—limiting CN’s alternative sources and strengthening OEM pricing power. Specialized parts, proprietary software and compatibility constraints increase vendor lock-in. Long equipment lifecycles and stringent certification add high switching costs. CN mitigates through long-term contracts, fleet standardization and robust in-house maintenance capacity.

Fuel and energy cost volatility

Fuel is a major input for CN, typically 10-15% of operating expenses, with global crude (Brent averaged about $86/bbl in 2024) driving price swings and limiting suppliers' direct bargaining power while pressuring margins. Fuel surcharges offset spikes but often lag market moves. Energy transition pilots (renewable diesel, battery/hybrid trials) create new vendor links. Hedging plus PSR and trip-optimizer efficiency reduce net exposure.

Labor unions and skill scarcity

Rail operations rely on unionized, safety-critical labor, giving organized groups significant leverage over wages and work rules; CN reported about 22,400 employees in 2024, most covered by collective agreements. Tight labor markets and onerous training/licensing raise switching costs and slow recruitments. Work stoppages risk service disruption and customer churn, so CN invests in workforce relations, automation and training to rebalance bargaining power.

Railcar leasing and specialty equipment

For certain commodities and seasonality CN depends on leased railcars and specialty assets; lessors tightened terms as utilization climbed above 90% in 2024, boosting supplier power. Custom equipment such as modern tank cars meeting TC/DOT standards narrows supplier choice and raises replacement costs. CN mitigates cyclicality via fleet diversification and multi-year leases and capex to own more assets.

- Leased-dependency: high during peak grain/oil seasons

- Utilization: >90% in 2024 increases lessor leverage

- Mitigation: multi-year leases, diversified fleet, increased ownership capex

Digital systems and signaling vendors

PTC/ETCS-like onboard systems, dispatch software and telematics are supplied by a few specialized vendors (notably Wabtec, Siemens, Alstom), creating integration lock-in and limited substitutability.

Cybersecurity and safety certifications (SIL/EN standards) raise switching costs; vendor consolidation increases pricing and roadmap leverage, while CN mitigates risk via modular architectures, open APIs and negotiated SLAs and integration pilots.

- specialized vendors: 3 dominant suppliers

- barriers: safety/cyber certifications

- CN response: modular design, APIs, SLAs

OEM concentration raises leverage; fuel $86/bbl, labor pressure

Supplier power is moderate-high: locomotive OEMs concentrated (Wabtec, Progress Rail), PTC/telematics vendors ~3 dominant, raising lock-in and pricing leverage. Fuel (~10–15% of opex) and Brent ~$86/bbl (2024) drive costs but are hedged; leased-railcar utilization >90% in 2024 tightened lessor terms. Unionized labor (~22,400 employees) adds bargaining leverage and switching costs.

| Category | Metric | 2024 |

|---|---|---|

| OEM concentration | Top suppliers | 2–3 firms |

| Fuel | Share of opex / Brent | 10–15% / $86/bbl |

| Labor | Employees (unionized) | 22,400 |

| Railcars | Utilization | >90% |

What is included in the product

Comprehensive Porter's Five Forces review tailored to Canadian National Railway, detailing competitive rivalry, supplier and buyer power, entry barriers, substitutes and disruptive threats, with strategic implications for pricing, profitability and market positioning.

Concise Porter's Five Forces for Canadian National Railway—one-sheet clarity to spot competitive pressures, customize intensity by scenario, and drop directly into decks for fast, board-ready strategy decisions.

Customers Bargaining Power

Large, concentrated shippers

Bulk producers, ports and automotive OEMs are sizable CN accounts that leverage large volumes to negotiate rates and service levels, especially where alternate routings or carriers exist. Their multi-year contracts, commonly 3–7 years, balance revenue stability and pricing pressure. CN counters with national network reach, schedule reliability and integrated logistics solutions to retain these high-volume shippers.

Intermodal customers with modal options

Intermodal BCOs and IMCs can shift to long‑haul trucking—trucks move roughly 70% of US freight by value—so price/service gaps heighten buyer power; nearshoring and inventory strategies let shippers reconfigure lanes quickly. CN’s network of over 20,000 route miles and extensive port access plus inland terminals create customer stickiness, while service metrics and guaranteed capacity contracts blunt switching.

Regulated service obligations and remedies

CTA in Canada and the U.S. STB provide formal dispute-resolution powers and can order remedies such as reciprocal switching, while mandated carrier performance reporting increases transparency and gives shippers evidentiary leverage. These regulatory levers moderate CN’s pricing discretion and can constrain unilateral rate moves. In 2024 CN continued to submit regulator-required performance reports and engaged proactively with shippers to manage compliance and commercial disputes.

Commodity price cyclicality

- Commodity cyclicality raises renegotiation risk

- Dynamic pricing cushions margin impact

- Logistics/storage increase switching costs

Switching costs vary by commodity

Unit-train bulk flows (e.g., grain, coal) face materially higher switching costs than container freight, giving shippers less leverage; CN’s roughly 20,000-route-mile North American network and dedicated corridors for unit trains limit feasible alternatives. Where CN’s network overlaps with competitors, customers can play carriers off each other and use joint-line moves or interchanges to lower costs. CN leverages unique corridors and origin-destination density to retain pricing power.

- Unit-train switching costs: high

- Container switching: lower, more competition

- Network overlaps enable buyer leverage

- Joint-line/interchange provide alternatives

- CN unique corridors reduce buyer power

Bulk shippers' multi-year leverage (3–7 yrs) vs intermodal switching; trucking ~70%

Large bulk shippers and ports wield strong leverage via volume and 3–7 year contracts, constraining short-term rates. Intermodal shippers face lower switching costs given trucking's ~70% US freight-by-value share, boosting buyer power. Regulatory oversight (CTA/STB) and CN’s ~19,500 route miles (2024) plus logistics services counterbalance shipper leverage.

| Metric | 2024 |

|---|---|

| Route miles | 19,500 |

| Contract length | 3–7 yrs |

| Truck freight share (US) | ~70% |

Full Version Awaits

Canadian National Railway Porter's Five Forces Analysis

This Porter’s Five Forces analysis of Canadian National Railway examines competitive rivalry, supplier and buyer power, threat of new entrants, and substitutes, highlighting rail-specific barriers and regulatory influences. It assesses CN’s strategic positioning, margin drivers, and vulnerability to fuel and labor dynamics. The analysis includes actionable insights for investors and managers. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders.