Coastal Community Bank Porter's Five Forces Analysis

Don't Miss the Bigger Picture

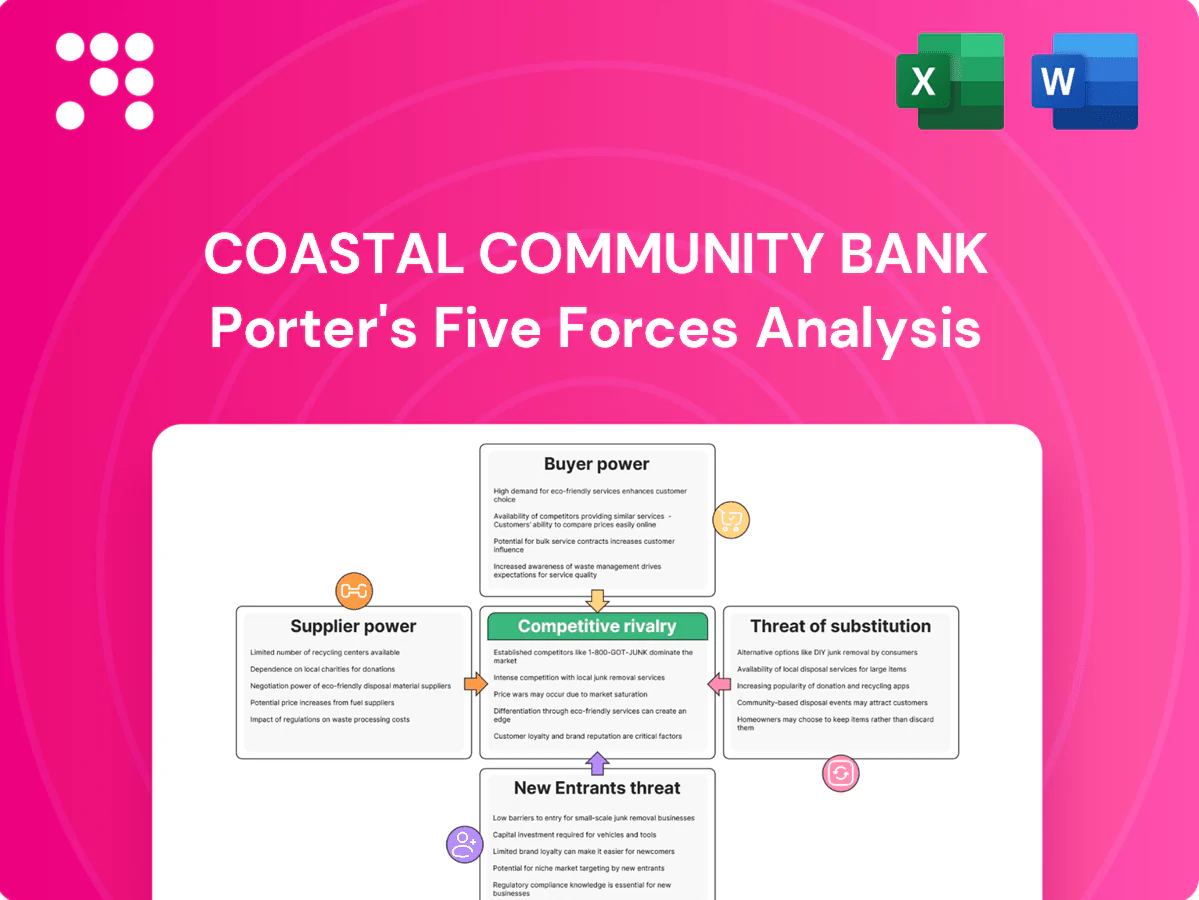

Coastal Community Bank’s Porter's Five Forces snapshot highlights competitive intensity, customer bargaining, and emerging substitute pressures shaping margins and growth prospects. It identifies key supplier relationships and regulatory risks that could alter strategy. This preview only scratches the surface — unlock the full Porter's Five Forces Analysis to explore market pressures and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated core tech vendors

Core processing, digital banking, and payment rails are concentrated: three national providers control roughly 80% of the US core market, creating dependency and limited negotiating leverage for Coastal Community Bank.

Switching cores is costly and risky—conversions often exceed $10M and take 12–24 months—driving vendor lock-in.

These vendors can influence pricing and the pace of innovation; multi-year contracts and long implementation cycles further reinforce supplier power.

Funding sources and depositors

Depositors supply the funds for Coastal Community Bank’s lending and can push for higher rates as the federal funds target ran 5.25–5.50% through 2024, making retail deposits more rate-sensitive. In the competitive Puget Sound market, certificate and brokered-like deposits have shown volatility, pressuring withdrawal-prone balances. Wholesale funding and FHLB lines provide alternatives but at market-driven costs, so funding suppliers exert moderate influence on bank margins.

Regulators as quasi-suppliers

Regulators act as quasi-suppliers by granting the license to operate and access to payment systems while imposing compliance, examination and capital rules that shape product design and growth. Capital rules require a CET1 minimum of 4.5% plus a 2.5% conservation buffer (effective 7.0%), and FDIC insurance limits remain $250,000, raising operating costs and limiting strategic flexibility. These expectations effectively increase supplier power.

Skilled labor and local talent

Experienced lenders, risk managers and technologists are scarce and highly mobile, raising supplier bargaining power for Coastal Community Bank; Washington state average annual wage was about 79,530 in 2023 (BLS), and Seattle metro wages rank among the highest nationally, intensifying regional competition. Recruiting specialty SMB bankers is costly and turnover risks push banks to use retention packages and culture as key countermeasures.

- Scarcity: experienced talent pool limited

- Regional wage pressure: Seattle area premium

- Recruiting cost: specialty bankers expensive

- Retention focus: pay, benefits, culture

Third-party fintech and service partners

Specialty fintech partners for treasury, fraud, AML and niche lending hold high supplier power for Coastal Community Bank because deep integration and compliance oversight make replacements costly; major integrations can represent up to 40% of delivered functionality and switching costs often exceed $1m per platform. Vendors may pass through rising fees or limit customization, though bargaining improves with multi-vendor optionality and scale.

- vendor-concentration: high

- integration-costs: >$1m per major swap

- outsourcing-share: ~40% functionality

- leverage-drivers: multi-vendor optionality, scale

Suppliers dominate: core vendors ~80%; switches >$10M, fintechs >$1M

Suppliers exert high bargaining power: three core vendors control ~80% of US cores, conversions cost >$10M and take 12–24 months, and fintech integrations often exceed $1M representing ~40% of functionality. Funding suppliers are moderately powerful with deposits rate-sensitive as fed funds ran 5.25–5.50% through 2024; regulators and talent shortages (WA avg wage $79,530 in 2023) further raise supplier influence.

| Supplier | Concentration | Switch Cost | Impact |

|---|---|---|---|

| Core vendors | ~80% | >$10M, 12–24m | High |

| Fintechs | Fragmented | >$1M | High |

| Depositors | Local | Market rates | Moderate |

What is included in the product

Tailored Porter's Five Forces analysis for Coastal Community Bank that uncovers competitive drivers, customer and supplier power, substitutes and entry barriers, identifies disruptive threats to market share, and provides strategic commentary suitable for reports, investor materials, or internal strategy decks.

Concise one-sheet Porter's Five Forces for Coastal Community Bank that clarifies competitive pressures and relieves analysis bottlenecks—customizable pressure levels and instant radar visualization make it boardroom-ready and easy to drop into decks.

Customers Bargaining Power

Rate-sensitive SMB and consumer deposits

Rate-sensitive SMB and consumer deposits amplify pricing pressure as customers can compare rates instantly and move funds digitally; online savings and money market yields ran about 4.5–5.0% in 2024, intensifying demands for yield. This dynamic compresses net interest margins during tightening cycles, with community bank median NIM near 3.3% in 2024 per FDIC data. Deeper relationships, fee income and service bundling help temper pure rate shopping.

Many local banking alternatives

The Puget Sound market in 2024 includes dozens of community banks, credit unions and national banks, giving customers many local alternatives. Easy branch access and robust mobile apps lower switching costs, so buyers can rapidly compare providers. Consumers routinely solicit multiple loan quotes to improve terms, strengthening leverage on fees and interest rates. This dynamic raises customer bargaining power in the region.

Digital experience expectations

Clients now expect seamless mobile, payments and treasury features, with 73% of consumers using mobile banking monthly in 2024, raising expectations versus Coastal’s app. Gaps versus large-bank UX increase buyer leverage to demand upgrades or price concessions. SMBs increasingly require API-enabled services and faster onboarding. Failure to meet UX standards risks elevated churn and lost deposits.

Information transparency

Online reviews, public rate tables and fintech aggregators make pricing and service quality highly visible; in 2024, 76% of U.S. banking customers compared rates online, compressing margin for opaque fees. Knowledgeable buyers increasingly demand fee waivers and bespoke pricing, forcing Coastal Community Bank to defend spreads. Transparency raises the premium for differentiated advice and faster execution.

- Visibility: online reviews + aggregators

- Pressure: fee waivers, custom structures

- Constraint: less room for opaque pricing

- Edge: advice quality and speed

Relationship-driven segments

Relationship-driven professional and SMB clients value Coastal Community Bank’s local decisioning and tailored service; a 2024 small business survey shows roughly 70% prioritize local lender relationships, which raises switching costs and reduces buyer power when deposits and lending are bundled with cash-management services. Bundles and deep ties cement loyalty, but competitive pricing or digital convenience can still unwind relationships if perceived value slips.

- Local decisioning: raises switching costs

- Bundled cash management: increases retention

- ~70% SMBs value relationship banking (2024)

- Competitive offers remain a churn risk

Rate shopping hits margins: online 4.5-5.0% vs NIM 3.3%

Customers wield strong bargaining power: online yields (4.5–5.0% in 2024) and instant rate comparison compress NIM (community bank median 3.3% in 2024) and raise fee pressure. High mobile use (73% monthly) and 76% rate comparison increase switching and demand for UX parity. SMBs still value local relationships (≈70% in 2024), which tempers but does not eliminate price sensitivity.

| Metric | 2024 Value |

|---|---|

| Online savings/money market yields | 4.5–5.0% |

| Community bank median NIM | 3.3% |

| Monthly mobile banking users | 73% |

| Customers comparing rates online | 76% |

| SMBs valuing local lender | ≈70% |

Preview Before You Purchase

Coastal Community Bank Porter's Five Forces Analysis

This preview is the full Coastal Community Bank Porter's Five Forces Analysis you’ll receive—no samples or placeholders—and it’s formatted for immediate use. The document delivered after purchase is identical to what you see here, professionally written and ready for download. Instant access is provided upon payment.

Don't Miss the Bigger Picture

Coastal Community Bank’s Porter's Five Forces snapshot highlights competitive intensity, customer bargaining, and emerging substitute pressures shaping margins and growth prospects. It identifies key supplier relationships and regulatory risks that could alter strategy. This preview only scratches the surface — unlock the full Porter's Five Forces Analysis to explore market pressures and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated core tech vendors

Core processing, digital banking, and payment rails are concentrated: three national providers control roughly 80% of the US core market, creating dependency and limited negotiating leverage for Coastal Community Bank.

Switching cores is costly and risky—conversions often exceed $10M and take 12–24 months—driving vendor lock-in.

These vendors can influence pricing and the pace of innovation; multi-year contracts and long implementation cycles further reinforce supplier power.

Funding sources and depositors

Depositors supply the funds for Coastal Community Bank’s lending and can push for higher rates as the federal funds target ran 5.25–5.50% through 2024, making retail deposits more rate-sensitive. In the competitive Puget Sound market, certificate and brokered-like deposits have shown volatility, pressuring withdrawal-prone balances. Wholesale funding and FHLB lines provide alternatives but at market-driven costs, so funding suppliers exert moderate influence on bank margins.

Regulators as quasi-suppliers

Regulators act as quasi-suppliers by granting the license to operate and access to payment systems while imposing compliance, examination and capital rules that shape product design and growth. Capital rules require a CET1 minimum of 4.5% plus a 2.5% conservation buffer (effective 7.0%), and FDIC insurance limits remain $250,000, raising operating costs and limiting strategic flexibility. These expectations effectively increase supplier power.

Skilled labor and local talent

Experienced lenders, risk managers and technologists are scarce and highly mobile, raising supplier bargaining power for Coastal Community Bank; Washington state average annual wage was about 79,530 in 2023 (BLS), and Seattle metro wages rank among the highest nationally, intensifying regional competition. Recruiting specialty SMB bankers is costly and turnover risks push banks to use retention packages and culture as key countermeasures.

- Scarcity: experienced talent pool limited

- Regional wage pressure: Seattle area premium

- Recruiting cost: specialty bankers expensive

- Retention focus: pay, benefits, culture

Third-party fintech and service partners

Specialty fintech partners for treasury, fraud, AML and niche lending hold high supplier power for Coastal Community Bank because deep integration and compliance oversight make replacements costly; major integrations can represent up to 40% of delivered functionality and switching costs often exceed $1m per platform. Vendors may pass through rising fees or limit customization, though bargaining improves with multi-vendor optionality and scale.

- vendor-concentration: high

- integration-costs: >$1m per major swap

- outsourcing-share: ~40% functionality

- leverage-drivers: multi-vendor optionality, scale

Suppliers dominate: core vendors ~80%; switches >$10M, fintechs >$1M

Suppliers exert high bargaining power: three core vendors control ~80% of US cores, conversions cost >$10M and take 12–24 months, and fintech integrations often exceed $1M representing ~40% of functionality. Funding suppliers are moderately powerful with deposits rate-sensitive as fed funds ran 5.25–5.50% through 2024; regulators and talent shortages (WA avg wage $79,530 in 2023) further raise supplier influence.

| Supplier | Concentration | Switch Cost | Impact |

|---|---|---|---|

| Core vendors | ~80% | >$10M, 12–24m | High |

| Fintechs | Fragmented | >$1M | High |

| Depositors | Local | Market rates | Moderate |

What is included in the product

Tailored Porter's Five Forces analysis for Coastal Community Bank that uncovers competitive drivers, customer and supplier power, substitutes and entry barriers, identifies disruptive threats to market share, and provides strategic commentary suitable for reports, investor materials, or internal strategy decks.

Concise one-sheet Porter's Five Forces for Coastal Community Bank that clarifies competitive pressures and relieves analysis bottlenecks—customizable pressure levels and instant radar visualization make it boardroom-ready and easy to drop into decks.

Customers Bargaining Power

Rate-sensitive SMB and consumer deposits

Rate-sensitive SMB and consumer deposits amplify pricing pressure as customers can compare rates instantly and move funds digitally; online savings and money market yields ran about 4.5–5.0% in 2024, intensifying demands for yield. This dynamic compresses net interest margins during tightening cycles, with community bank median NIM near 3.3% in 2024 per FDIC data. Deeper relationships, fee income and service bundling help temper pure rate shopping.

Many local banking alternatives

The Puget Sound market in 2024 includes dozens of community banks, credit unions and national banks, giving customers many local alternatives. Easy branch access and robust mobile apps lower switching costs, so buyers can rapidly compare providers. Consumers routinely solicit multiple loan quotes to improve terms, strengthening leverage on fees and interest rates. This dynamic raises customer bargaining power in the region.

Digital experience expectations

Clients now expect seamless mobile, payments and treasury features, with 73% of consumers using mobile banking monthly in 2024, raising expectations versus Coastal’s app. Gaps versus large-bank UX increase buyer leverage to demand upgrades or price concessions. SMBs increasingly require API-enabled services and faster onboarding. Failure to meet UX standards risks elevated churn and lost deposits.

Information transparency

Online reviews, public rate tables and fintech aggregators make pricing and service quality highly visible; in 2024, 76% of U.S. banking customers compared rates online, compressing margin for opaque fees. Knowledgeable buyers increasingly demand fee waivers and bespoke pricing, forcing Coastal Community Bank to defend spreads. Transparency raises the premium for differentiated advice and faster execution.

- Visibility: online reviews + aggregators

- Pressure: fee waivers, custom structures

- Constraint: less room for opaque pricing

- Edge: advice quality and speed

Relationship-driven segments

Relationship-driven professional and SMB clients value Coastal Community Bank’s local decisioning and tailored service; a 2024 small business survey shows roughly 70% prioritize local lender relationships, which raises switching costs and reduces buyer power when deposits and lending are bundled with cash-management services. Bundles and deep ties cement loyalty, but competitive pricing or digital convenience can still unwind relationships if perceived value slips.

- Local decisioning: raises switching costs

- Bundled cash management: increases retention

- ~70% SMBs value relationship banking (2024)

- Competitive offers remain a churn risk

Rate shopping hits margins: online 4.5-5.0% vs NIM 3.3%

Customers wield strong bargaining power: online yields (4.5–5.0% in 2024) and instant rate comparison compress NIM (community bank median 3.3% in 2024) and raise fee pressure. High mobile use (73% monthly) and 76% rate comparison increase switching and demand for UX parity. SMBs still value local relationships (≈70% in 2024), which tempers but does not eliminate price sensitivity.

| Metric | 2024 Value |

|---|---|

| Online savings/money market yields | 4.5–5.0% |

| Community bank median NIM | 3.3% |

| Monthly mobile banking users | 73% |

| Customers comparing rates online | 76% |

| SMBs valuing local lender | ≈70% |

Preview Before You Purchase

Coastal Community Bank Porter's Five Forces Analysis

This preview is the full Coastal Community Bank Porter's Five Forces Analysis you’ll receive—no samples or placeholders—and it’s formatted for immediate use. The document delivered after purchase is identical to what you see here, professionally written and ready for download. Instant access is provided upon payment.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Coastal Community Bank’s Porter's Five Forces snapshot highlights competitive intensity, customer bargaining, and emerging substitute pressures shaping margins and growth prospects. It identifies key supplier relationships and regulatory risks that could alter strategy. This preview only scratches the surface — unlock the full Porter's Five Forces Analysis to explore market pressures and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated core tech vendors

Core processing, digital banking, and payment rails are concentrated: three national providers control roughly 80% of the US core market, creating dependency and limited negotiating leverage for Coastal Community Bank.

Switching cores is costly and risky—conversions often exceed $10M and take 12–24 months—driving vendor lock-in.

These vendors can influence pricing and the pace of innovation; multi-year contracts and long implementation cycles further reinforce supplier power.

Funding sources and depositors

Depositors supply the funds for Coastal Community Bank’s lending and can push for higher rates as the federal funds target ran 5.25–5.50% through 2024, making retail deposits more rate-sensitive. In the competitive Puget Sound market, certificate and brokered-like deposits have shown volatility, pressuring withdrawal-prone balances. Wholesale funding and FHLB lines provide alternatives but at market-driven costs, so funding suppliers exert moderate influence on bank margins.

Regulators as quasi-suppliers

Regulators act as quasi-suppliers by granting the license to operate and access to payment systems while imposing compliance, examination and capital rules that shape product design and growth. Capital rules require a CET1 minimum of 4.5% plus a 2.5% conservation buffer (effective 7.0%), and FDIC insurance limits remain $250,000, raising operating costs and limiting strategic flexibility. These expectations effectively increase supplier power.

Skilled labor and local talent

Experienced lenders, risk managers and technologists are scarce and highly mobile, raising supplier bargaining power for Coastal Community Bank; Washington state average annual wage was about 79,530 in 2023 (BLS), and Seattle metro wages rank among the highest nationally, intensifying regional competition. Recruiting specialty SMB bankers is costly and turnover risks push banks to use retention packages and culture as key countermeasures.

- Scarcity: experienced talent pool limited

- Regional wage pressure: Seattle area premium

- Recruiting cost: specialty bankers expensive

- Retention focus: pay, benefits, culture

Third-party fintech and service partners

Specialty fintech partners for treasury, fraud, AML and niche lending hold high supplier power for Coastal Community Bank because deep integration and compliance oversight make replacements costly; major integrations can represent up to 40% of delivered functionality and switching costs often exceed $1m per platform. Vendors may pass through rising fees or limit customization, though bargaining improves with multi-vendor optionality and scale.

- vendor-concentration: high

- integration-costs: >$1m per major swap

- outsourcing-share: ~40% functionality

- leverage-drivers: multi-vendor optionality, scale

Suppliers dominate: core vendors ~80%; switches >$10M, fintechs >$1M

Suppliers exert high bargaining power: three core vendors control ~80% of US cores, conversions cost >$10M and take 12–24 months, and fintech integrations often exceed $1M representing ~40% of functionality. Funding suppliers are moderately powerful with deposits rate-sensitive as fed funds ran 5.25–5.50% through 2024; regulators and talent shortages (WA avg wage $79,530 in 2023) further raise supplier influence.

| Supplier | Concentration | Switch Cost | Impact |

|---|---|---|---|

| Core vendors | ~80% | >$10M, 12–24m | High |

| Fintechs | Fragmented | >$1M | High |

| Depositors | Local | Market rates | Moderate |

What is included in the product

Tailored Porter's Five Forces analysis for Coastal Community Bank that uncovers competitive drivers, customer and supplier power, substitutes and entry barriers, identifies disruptive threats to market share, and provides strategic commentary suitable for reports, investor materials, or internal strategy decks.

Concise one-sheet Porter's Five Forces for Coastal Community Bank that clarifies competitive pressures and relieves analysis bottlenecks—customizable pressure levels and instant radar visualization make it boardroom-ready and easy to drop into decks.

Customers Bargaining Power

Rate-sensitive SMB and consumer deposits

Rate-sensitive SMB and consumer deposits amplify pricing pressure as customers can compare rates instantly and move funds digitally; online savings and money market yields ran about 4.5–5.0% in 2024, intensifying demands for yield. This dynamic compresses net interest margins during tightening cycles, with community bank median NIM near 3.3% in 2024 per FDIC data. Deeper relationships, fee income and service bundling help temper pure rate shopping.

Many local banking alternatives

The Puget Sound market in 2024 includes dozens of community banks, credit unions and national banks, giving customers many local alternatives. Easy branch access and robust mobile apps lower switching costs, so buyers can rapidly compare providers. Consumers routinely solicit multiple loan quotes to improve terms, strengthening leverage on fees and interest rates. This dynamic raises customer bargaining power in the region.

Digital experience expectations

Clients now expect seamless mobile, payments and treasury features, with 73% of consumers using mobile banking monthly in 2024, raising expectations versus Coastal’s app. Gaps versus large-bank UX increase buyer leverage to demand upgrades or price concessions. SMBs increasingly require API-enabled services and faster onboarding. Failure to meet UX standards risks elevated churn and lost deposits.

Information transparency

Online reviews, public rate tables and fintech aggregators make pricing and service quality highly visible; in 2024, 76% of U.S. banking customers compared rates online, compressing margin for opaque fees. Knowledgeable buyers increasingly demand fee waivers and bespoke pricing, forcing Coastal Community Bank to defend spreads. Transparency raises the premium for differentiated advice and faster execution.

- Visibility: online reviews + aggregators

- Pressure: fee waivers, custom structures

- Constraint: less room for opaque pricing

- Edge: advice quality and speed

Relationship-driven segments

Relationship-driven professional and SMB clients value Coastal Community Bank’s local decisioning and tailored service; a 2024 small business survey shows roughly 70% prioritize local lender relationships, which raises switching costs and reduces buyer power when deposits and lending are bundled with cash-management services. Bundles and deep ties cement loyalty, but competitive pricing or digital convenience can still unwind relationships if perceived value slips.

- Local decisioning: raises switching costs

- Bundled cash management: increases retention

- ~70% SMBs value relationship banking (2024)

- Competitive offers remain a churn risk

Rate shopping hits margins: online 4.5-5.0% vs NIM 3.3%

Customers wield strong bargaining power: online yields (4.5–5.0% in 2024) and instant rate comparison compress NIM (community bank median 3.3% in 2024) and raise fee pressure. High mobile use (73% monthly) and 76% rate comparison increase switching and demand for UX parity. SMBs still value local relationships (≈70% in 2024), which tempers but does not eliminate price sensitivity.

| Metric | 2024 Value |

|---|---|

| Online savings/money market yields | 4.5–5.0% |

| Community bank median NIM | 3.3% |

| Monthly mobile banking users | 73% |

| Customers comparing rates online | 76% |

| SMBs valuing local lender | ≈70% |

Preview Before You Purchase

Coastal Community Bank Porter's Five Forces Analysis

This preview is the full Coastal Community Bank Porter's Five Forces Analysis you’ll receive—no samples or placeholders—and it’s formatted for immediate use. The document delivered after purchase is identical to what you see here, professionally written and ready for download. Instant access is provided upon payment.