Coastal Community Bank PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political, economic, social, technological, legal, and environmental forces are reshaping Coastal Community Bank’s strategy and risk profile. This concise PESTLE snapshot highlights key external drivers and blind spots investors and strategists must know. Buy the full analysis for detailed, actionable insights and ready-to-use charts to inform decisions and mitigate risk.

Political factors

Federal banking stance

Shifts in FDIC, Federal Reserve, and Treasury priorities since the March 2023 banking stress—with roughly 4,400 FDIC‑insured banks remaining—have tightened capital, liquidity, and resolution expectations for community banks. Policy emphasis on stability can ease compliance through targeted guidance or raise standards after stress, altering exam intensity and risk appetite. Coastal must stay agile to policy cycles that affect growth plans, and active board engagement with regulators and policy horizons reduces surprise risk.

Washington state policy climate

Washington’s progressive policy mix—no state income tax but a B&O tax regime and a $16.28 minimum wage in 2024—shapes SMB margins and consumer protections; the Washington State Department of Financial Institutions (DFI) maintains active supervision that, together with city ordinances, raises compliance complexity for fees and product design; municipal housing and small‑business programs (e.g., Seattle/King County initiatives) expand lending pipelines while a strong statewide equity agenda shifts community reinvestment priorities.

SBA and public finance programs

Availability of SBA 7(a) (max $5 million), 504 (up to $5.5 million) and state-backed programs drives demand across Coastal’s SMB base; SBA guarantees (typically 75–85%) materially improve lender economics. Budget shifts or rule changes can alter guarantee terms and underwriting criteria, changing risk-weighted returns. Active alignment with public lenders expands pipeline and de-risks growth. Faster execution and SBA expertise are key competitive differentiators.

Infrastructure and housing agendas

- Infrastructure funding: $550 billion (Bipartisan Infrastructure Law)

- Regional demand: Washington ~7.8M population

- Risk drivers: zoning/permits → credit conversion

- Opportunity: supply-chain/public-project financing

Trade and immigration dynamics

Port trade policy shapes regional logistics, manufacturing and export SMBs and can alter inland freight volumes and cost structures; immigration rules — H-1B cap 85,000 and ~1.16M lawful permanent residents in 2023 — influence labor supply for hospitality, healthcare and tech-adjacent services. Policy-driven demand swings can affect deposit flows and credit quality; sector diversification reduces shock exposure.

- Trade policy: alters port throughput, freight costs

- Immigration: H-1B 85,000 impacts skilled labor

- Risk: demand volatility -> deposit/credit stress

- Mitigation: diversified sector lending

Post‑2023 tightening raises capital scrutiny; WA policy and $550B BIL reshape SMB lending

Post‑2023 regulatory tightening (≈4,400 FDIC banks) raises capital, liquidity and exam intensity for community banks; Washington policy (no state income tax, B&O tax, $16.28 min wage in 2024) and active DFI supervision increase compliance and shape SMB margins. SBA and infrastructure flows ($550B BIL; SBA 7(a) $5M, 504 $5.5M) expand lending pipelines but hinge on rule changes.

| Metric | Value |

|---|---|

| FDIC banks | ≈4,400 |

| WA population | ~7.8M |

| BIL | $550B |

| Min wage (2024) | $16.28 |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Coastal Community Bank, with data-backed trends and region-specific examples to identify risks, opportunities, and strategic actions for executives, investors, and advisors.

A concise, visually segmented PESTLE summary tailored to Coastal Community Bank that simplifies regulatory, economic, and technological risks for quick presentation and team alignment; editable notes enable regional or product-specific context during planning sessions.

Economic factors

Interest rate cycle

NIM at Coastal Community Bank is highly sensitive to Fed policy, deposit repricing, and asset-yield resets as the federal funds target sits at 5.25–5.50% (July 2025). Higher-for-longer rates elevate funding costs and compress margin unless loan yields reprice ahead of deposit betas. Mortgage prepayment and security-duration dynamics drive OCI volatility and capital implications. Active balance-sheet hedging and portfolio-mix management are therefore critical.

Puget Sound tech exposure

Puget Sound’s concentration of headquarters like Amazon and Microsoft drives SMB revenues and payrolls; tech swings have cascaded—Seattle office vacancy exceeded 20% in 2024, pressuring CRE occupancy and retail foot traffic. Hiring freezes or expansions quickly ripple through services and tax bases, so concentration risk demands ongoing sector monitoring and stress testing. Deep, multi-year banking relationships with tech-linked SMBs can stabilize balances across cycles.

Real estate market trends

Residential affordability strains—median US existing-home price ~$388k (mid-2024) and 30-year mortgage rates near 7%—compress purchase demand and lower collateral depth, while CRE repricing has pushed cap rates up to ~6–7% in many secondary markets. Office utilization dips (national vacancy ~18% in 2024) weigh on downtown asset values, whereas industrial vacancy remains tight (~4–5%), supporting rents. Rising construction costs and higher cap rates have tightened project feasibility; many lenders target conservative LTVs (~60–65%) and 60–70% pre-leasing thresholds to limit downside.

Deposit competition

Competition from money market funds (assets >5 trillion USD in 2024) and digital banks has pushed deposit betas higher and increased churn, with industry 12‑month betas moving toward 50–60% in 2023–24.

Coastal Community Bank's strong local relationships help retain core low‑cost deposits, while treasury services and bundled business cash management reduce rate sensitivity.

Disciplined pricing balances targeted growth against margin protection, limiting risky funding runs.

- deposit-threat: money market funds >5T (2024)

- deposit-beta: ~50–60% (12m, 2023–24)

- retention-driver: local relationships, treasury services

- strategy: pricing discipline to protect margin

SMB health and labor costs

Small business margins remain squeezed by wage inflation and input-cost volatility; BLS average hourly earnings rose about 4.1% year‑over‑year in 2024, pressuring labor margins. Consumer spending fuels service‑sector revenue and credit quality, with real PCE growth near 3.0% in 2024. Monitoring cash‑flow coverage and covenant headroom is essential, while advisory‑driven banking improves client resilience and lowers default risk.

- Wage growth: BLS avg hourly earnings +4.1% y/y (2024)

- Consumer demand: real PCE ~3.0% (2024)

- Watch cash‑flow coverage & covenant headroom

- Advisory banking boosts SME resilience

Post‑2023 tightening raises capital scrutiny; WA policy and $550B BIL reshape SMB lending

NIM remains highly sensitive to Fed funds 5.25–5.50% (Jul 2025), deposit repricing and asset-yield resets.

Puget Sound tech concentration (Amazon, Microsoft) amplifies SMB cashflow and CRE stress; Seattle office vacancy >20% (2024).

Housing affordability and 30y mortgage ≈7% (mid‑2024) suppress purchase demand; industrial tightness supports rents.

Competition from money market funds >5T (2024) raised deposit betas ~50–60% (2023–24).

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% |

| Money market AUM | >5T (2024) |

| Deposit beta | 50–60% |

| 30y mortgage | ~7% |

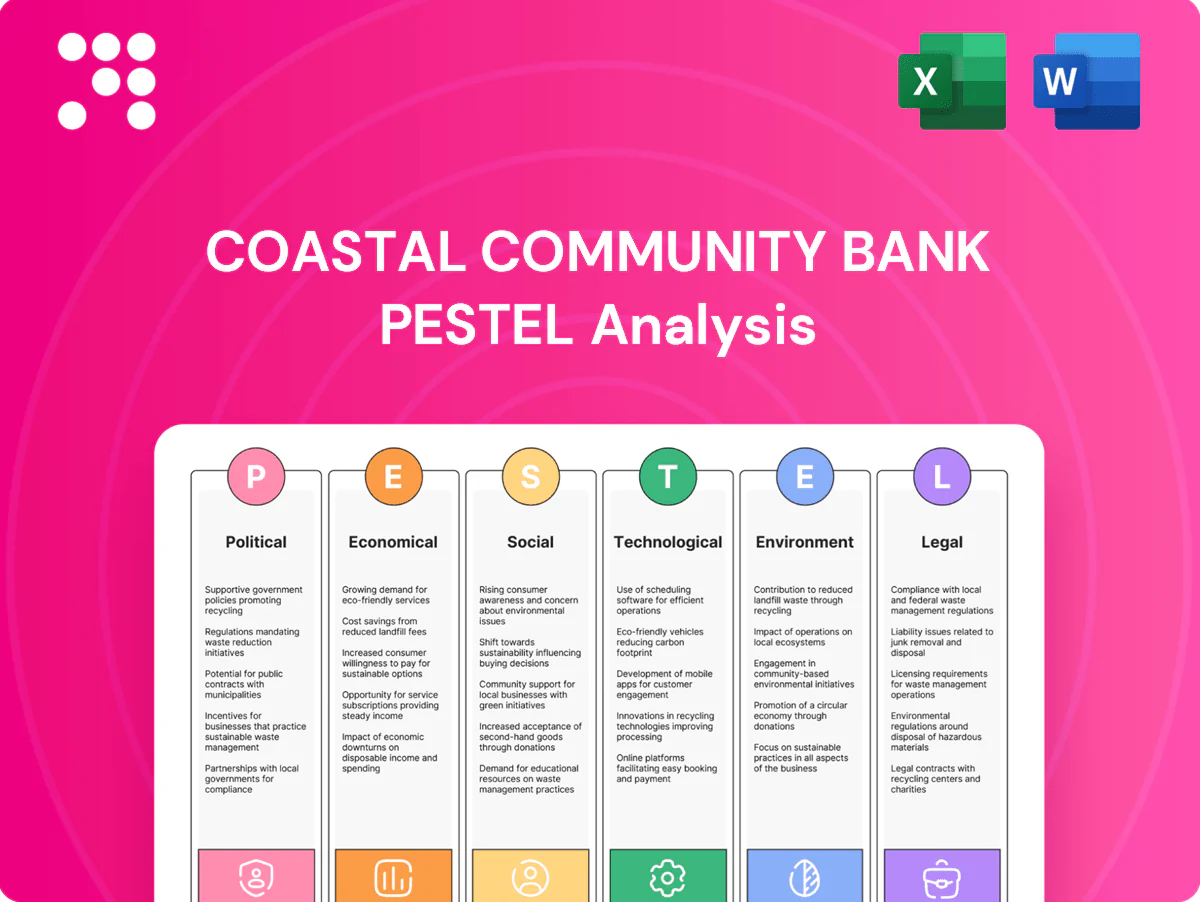

What You See Is What You Get

Coastal Community Bank PESTLE Analysis

The preview shown here is the exact Coastal Community Bank PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. This is a real screenshot of the product with no placeholders or teasers. The layout, content, and structure visible here are exactly what you’ll download instantly after payment.

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political, economic, social, technological, legal, and environmental forces are reshaping Coastal Community Bank’s strategy and risk profile. This concise PESTLE snapshot highlights key external drivers and blind spots investors and strategists must know. Buy the full analysis for detailed, actionable insights and ready-to-use charts to inform decisions and mitigate risk.

Political factors

Federal banking stance

Shifts in FDIC, Federal Reserve, and Treasury priorities since the March 2023 banking stress—with roughly 4,400 FDIC‑insured banks remaining—have tightened capital, liquidity, and resolution expectations for community banks. Policy emphasis on stability can ease compliance through targeted guidance or raise standards after stress, altering exam intensity and risk appetite. Coastal must stay agile to policy cycles that affect growth plans, and active board engagement with regulators and policy horizons reduces surprise risk.

Washington state policy climate

Washington’s progressive policy mix—no state income tax but a B&O tax regime and a $16.28 minimum wage in 2024—shapes SMB margins and consumer protections; the Washington State Department of Financial Institutions (DFI) maintains active supervision that, together with city ordinances, raises compliance complexity for fees and product design; municipal housing and small‑business programs (e.g., Seattle/King County initiatives) expand lending pipelines while a strong statewide equity agenda shifts community reinvestment priorities.

SBA and public finance programs

Availability of SBA 7(a) (max $5 million), 504 (up to $5.5 million) and state-backed programs drives demand across Coastal’s SMB base; SBA guarantees (typically 75–85%) materially improve lender economics. Budget shifts or rule changes can alter guarantee terms and underwriting criteria, changing risk-weighted returns. Active alignment with public lenders expands pipeline and de-risks growth. Faster execution and SBA expertise are key competitive differentiators.

Infrastructure and housing agendas

- Infrastructure funding: $550 billion (Bipartisan Infrastructure Law)

- Regional demand: Washington ~7.8M population

- Risk drivers: zoning/permits → credit conversion

- Opportunity: supply-chain/public-project financing

Trade and immigration dynamics

Port trade policy shapes regional logistics, manufacturing and export SMBs and can alter inland freight volumes and cost structures; immigration rules — H-1B cap 85,000 and ~1.16M lawful permanent residents in 2023 — influence labor supply for hospitality, healthcare and tech-adjacent services. Policy-driven demand swings can affect deposit flows and credit quality; sector diversification reduces shock exposure.

- Trade policy: alters port throughput, freight costs

- Immigration: H-1B 85,000 impacts skilled labor

- Risk: demand volatility -> deposit/credit stress

- Mitigation: diversified sector lending

Post‑2023 tightening raises capital scrutiny; WA policy and $550B BIL reshape SMB lending

Post‑2023 regulatory tightening (≈4,400 FDIC banks) raises capital, liquidity and exam intensity for community banks; Washington policy (no state income tax, B&O tax, $16.28 min wage in 2024) and active DFI supervision increase compliance and shape SMB margins. SBA and infrastructure flows ($550B BIL; SBA 7(a) $5M, 504 $5.5M) expand lending pipelines but hinge on rule changes.

| Metric | Value |

|---|---|

| FDIC banks | ≈4,400 |

| WA population | ~7.8M |

| BIL | $550B |

| Min wage (2024) | $16.28 |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Coastal Community Bank, with data-backed trends and region-specific examples to identify risks, opportunities, and strategic actions for executives, investors, and advisors.

A concise, visually segmented PESTLE summary tailored to Coastal Community Bank that simplifies regulatory, economic, and technological risks for quick presentation and team alignment; editable notes enable regional or product-specific context during planning sessions.

Economic factors

Interest rate cycle

NIM at Coastal Community Bank is highly sensitive to Fed policy, deposit repricing, and asset-yield resets as the federal funds target sits at 5.25–5.50% (July 2025). Higher-for-longer rates elevate funding costs and compress margin unless loan yields reprice ahead of deposit betas. Mortgage prepayment and security-duration dynamics drive OCI volatility and capital implications. Active balance-sheet hedging and portfolio-mix management are therefore critical.

Puget Sound tech exposure

Puget Sound’s concentration of headquarters like Amazon and Microsoft drives SMB revenues and payrolls; tech swings have cascaded—Seattle office vacancy exceeded 20% in 2024, pressuring CRE occupancy and retail foot traffic. Hiring freezes or expansions quickly ripple through services and tax bases, so concentration risk demands ongoing sector monitoring and stress testing. Deep, multi-year banking relationships with tech-linked SMBs can stabilize balances across cycles.

Real estate market trends

Residential affordability strains—median US existing-home price ~$388k (mid-2024) and 30-year mortgage rates near 7%—compress purchase demand and lower collateral depth, while CRE repricing has pushed cap rates up to ~6–7% in many secondary markets. Office utilization dips (national vacancy ~18% in 2024) weigh on downtown asset values, whereas industrial vacancy remains tight (~4–5%), supporting rents. Rising construction costs and higher cap rates have tightened project feasibility; many lenders target conservative LTVs (~60–65%) and 60–70% pre-leasing thresholds to limit downside.

Deposit competition

Competition from money market funds (assets >5 trillion USD in 2024) and digital banks has pushed deposit betas higher and increased churn, with industry 12‑month betas moving toward 50–60% in 2023–24.

Coastal Community Bank's strong local relationships help retain core low‑cost deposits, while treasury services and bundled business cash management reduce rate sensitivity.

Disciplined pricing balances targeted growth against margin protection, limiting risky funding runs.

- deposit-threat: money market funds >5T (2024)

- deposit-beta: ~50–60% (12m, 2023–24)

- retention-driver: local relationships, treasury services

- strategy: pricing discipline to protect margin

SMB health and labor costs

Small business margins remain squeezed by wage inflation and input-cost volatility; BLS average hourly earnings rose about 4.1% year‑over‑year in 2024, pressuring labor margins. Consumer spending fuels service‑sector revenue and credit quality, with real PCE growth near 3.0% in 2024. Monitoring cash‑flow coverage and covenant headroom is essential, while advisory‑driven banking improves client resilience and lowers default risk.

- Wage growth: BLS avg hourly earnings +4.1% y/y (2024)

- Consumer demand: real PCE ~3.0% (2024)

- Watch cash‑flow coverage & covenant headroom

- Advisory banking boosts SME resilience

Post‑2023 tightening raises capital scrutiny; WA policy and $550B BIL reshape SMB lending

NIM remains highly sensitive to Fed funds 5.25–5.50% (Jul 2025), deposit repricing and asset-yield resets.

Puget Sound tech concentration (Amazon, Microsoft) amplifies SMB cashflow and CRE stress; Seattle office vacancy >20% (2024).

Housing affordability and 30y mortgage ≈7% (mid‑2024) suppress purchase demand; industrial tightness supports rents.

Competition from money market funds >5T (2024) raised deposit betas ~50–60% (2023–24).

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% |

| Money market AUM | >5T (2024) |

| Deposit beta | 50–60% |

| 30y mortgage | ~7% |

What You See Is What You Get

Coastal Community Bank PESTLE Analysis

The preview shown here is the exact Coastal Community Bank PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. This is a real screenshot of the product with no placeholders or teasers. The layout, content, and structure visible here are exactly what you’ll download instantly after payment.

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political, economic, social, technological, legal, and environmental forces are reshaping Coastal Community Bank’s strategy and risk profile. This concise PESTLE snapshot highlights key external drivers and blind spots investors and strategists must know. Buy the full analysis for detailed, actionable insights and ready-to-use charts to inform decisions and mitigate risk.

Political factors

Federal banking stance

Shifts in FDIC, Federal Reserve, and Treasury priorities since the March 2023 banking stress—with roughly 4,400 FDIC‑insured banks remaining—have tightened capital, liquidity, and resolution expectations for community banks. Policy emphasis on stability can ease compliance through targeted guidance or raise standards after stress, altering exam intensity and risk appetite. Coastal must stay agile to policy cycles that affect growth plans, and active board engagement with regulators and policy horizons reduces surprise risk.

Washington state policy climate

Washington’s progressive policy mix—no state income tax but a B&O tax regime and a $16.28 minimum wage in 2024—shapes SMB margins and consumer protections; the Washington State Department of Financial Institutions (DFI) maintains active supervision that, together with city ordinances, raises compliance complexity for fees and product design; municipal housing and small‑business programs (e.g., Seattle/King County initiatives) expand lending pipelines while a strong statewide equity agenda shifts community reinvestment priorities.

SBA and public finance programs

Availability of SBA 7(a) (max $5 million), 504 (up to $5.5 million) and state-backed programs drives demand across Coastal’s SMB base; SBA guarantees (typically 75–85%) materially improve lender economics. Budget shifts or rule changes can alter guarantee terms and underwriting criteria, changing risk-weighted returns. Active alignment with public lenders expands pipeline and de-risks growth. Faster execution and SBA expertise are key competitive differentiators.

Infrastructure and housing agendas

- Infrastructure funding: $550 billion (Bipartisan Infrastructure Law)

- Regional demand: Washington ~7.8M population

- Risk drivers: zoning/permits → credit conversion

- Opportunity: supply-chain/public-project financing

Trade and immigration dynamics

Port trade policy shapes regional logistics, manufacturing and export SMBs and can alter inland freight volumes and cost structures; immigration rules — H-1B cap 85,000 and ~1.16M lawful permanent residents in 2023 — influence labor supply for hospitality, healthcare and tech-adjacent services. Policy-driven demand swings can affect deposit flows and credit quality; sector diversification reduces shock exposure.

- Trade policy: alters port throughput, freight costs

- Immigration: H-1B 85,000 impacts skilled labor

- Risk: demand volatility -> deposit/credit stress

- Mitigation: diversified sector lending

Post‑2023 tightening raises capital scrutiny; WA policy and $550B BIL reshape SMB lending

Post‑2023 regulatory tightening (≈4,400 FDIC banks) raises capital, liquidity and exam intensity for community banks; Washington policy (no state income tax, B&O tax, $16.28 min wage in 2024) and active DFI supervision increase compliance and shape SMB margins. SBA and infrastructure flows ($550B BIL; SBA 7(a) $5M, 504 $5.5M) expand lending pipelines but hinge on rule changes.

| Metric | Value |

|---|---|

| FDIC banks | ≈4,400 |

| WA population | ~7.8M |

| BIL | $550B |

| Min wage (2024) | $16.28 |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Coastal Community Bank, with data-backed trends and region-specific examples to identify risks, opportunities, and strategic actions for executives, investors, and advisors.

A concise, visually segmented PESTLE summary tailored to Coastal Community Bank that simplifies regulatory, economic, and technological risks for quick presentation and team alignment; editable notes enable regional or product-specific context during planning sessions.

Economic factors

Interest rate cycle

NIM at Coastal Community Bank is highly sensitive to Fed policy, deposit repricing, and asset-yield resets as the federal funds target sits at 5.25–5.50% (July 2025). Higher-for-longer rates elevate funding costs and compress margin unless loan yields reprice ahead of deposit betas. Mortgage prepayment and security-duration dynamics drive OCI volatility and capital implications. Active balance-sheet hedging and portfolio-mix management are therefore critical.

Puget Sound tech exposure

Puget Sound’s concentration of headquarters like Amazon and Microsoft drives SMB revenues and payrolls; tech swings have cascaded—Seattle office vacancy exceeded 20% in 2024, pressuring CRE occupancy and retail foot traffic. Hiring freezes or expansions quickly ripple through services and tax bases, so concentration risk demands ongoing sector monitoring and stress testing. Deep, multi-year banking relationships with tech-linked SMBs can stabilize balances across cycles.

Real estate market trends

Residential affordability strains—median US existing-home price ~$388k (mid-2024) and 30-year mortgage rates near 7%—compress purchase demand and lower collateral depth, while CRE repricing has pushed cap rates up to ~6–7% in many secondary markets. Office utilization dips (national vacancy ~18% in 2024) weigh on downtown asset values, whereas industrial vacancy remains tight (~4–5%), supporting rents. Rising construction costs and higher cap rates have tightened project feasibility; many lenders target conservative LTVs (~60–65%) and 60–70% pre-leasing thresholds to limit downside.

Deposit competition

Competition from money market funds (assets >5 trillion USD in 2024) and digital banks has pushed deposit betas higher and increased churn, with industry 12‑month betas moving toward 50–60% in 2023–24.

Coastal Community Bank's strong local relationships help retain core low‑cost deposits, while treasury services and bundled business cash management reduce rate sensitivity.

Disciplined pricing balances targeted growth against margin protection, limiting risky funding runs.

- deposit-threat: money market funds >5T (2024)

- deposit-beta: ~50–60% (12m, 2023–24)

- retention-driver: local relationships, treasury services

- strategy: pricing discipline to protect margin

SMB health and labor costs

Small business margins remain squeezed by wage inflation and input-cost volatility; BLS average hourly earnings rose about 4.1% year‑over‑year in 2024, pressuring labor margins. Consumer spending fuels service‑sector revenue and credit quality, with real PCE growth near 3.0% in 2024. Monitoring cash‑flow coverage and covenant headroom is essential, while advisory‑driven banking improves client resilience and lowers default risk.

- Wage growth: BLS avg hourly earnings +4.1% y/y (2024)

- Consumer demand: real PCE ~3.0% (2024)

- Watch cash‑flow coverage & covenant headroom

- Advisory banking boosts SME resilience

Post‑2023 tightening raises capital scrutiny; WA policy and $550B BIL reshape SMB lending

NIM remains highly sensitive to Fed funds 5.25–5.50% (Jul 2025), deposit repricing and asset-yield resets.

Puget Sound tech concentration (Amazon, Microsoft) amplifies SMB cashflow and CRE stress; Seattle office vacancy >20% (2024).

Housing affordability and 30y mortgage ≈7% (mid‑2024) suppress purchase demand; industrial tightness supports rents.

Competition from money market funds >5T (2024) raised deposit betas ~50–60% (2023–24).

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% |

| Money market AUM | >5T (2024) |

| Deposit beta | 50–60% |

| 30y mortgage | ~7% |

What You See Is What You Get

Coastal Community Bank PESTLE Analysis

The preview shown here is the exact Coastal Community Bank PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. This is a real screenshot of the product with no placeholders or teasers. The layout, content, and structure visible here are exactly what you’ll download instantly after payment.