Coca-Cola HBC PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Explore how political shifts, economic trends, social preferences, technological innovation, environmental pressures, and legal risks are shaping Coca-Cola HBC’s strategy and performance. Our concise PESTLE highlights key external drivers and risk hotspots—perfect for investors and strategists. Purchase the full, editable analysis to access actionable insights and immediate download.

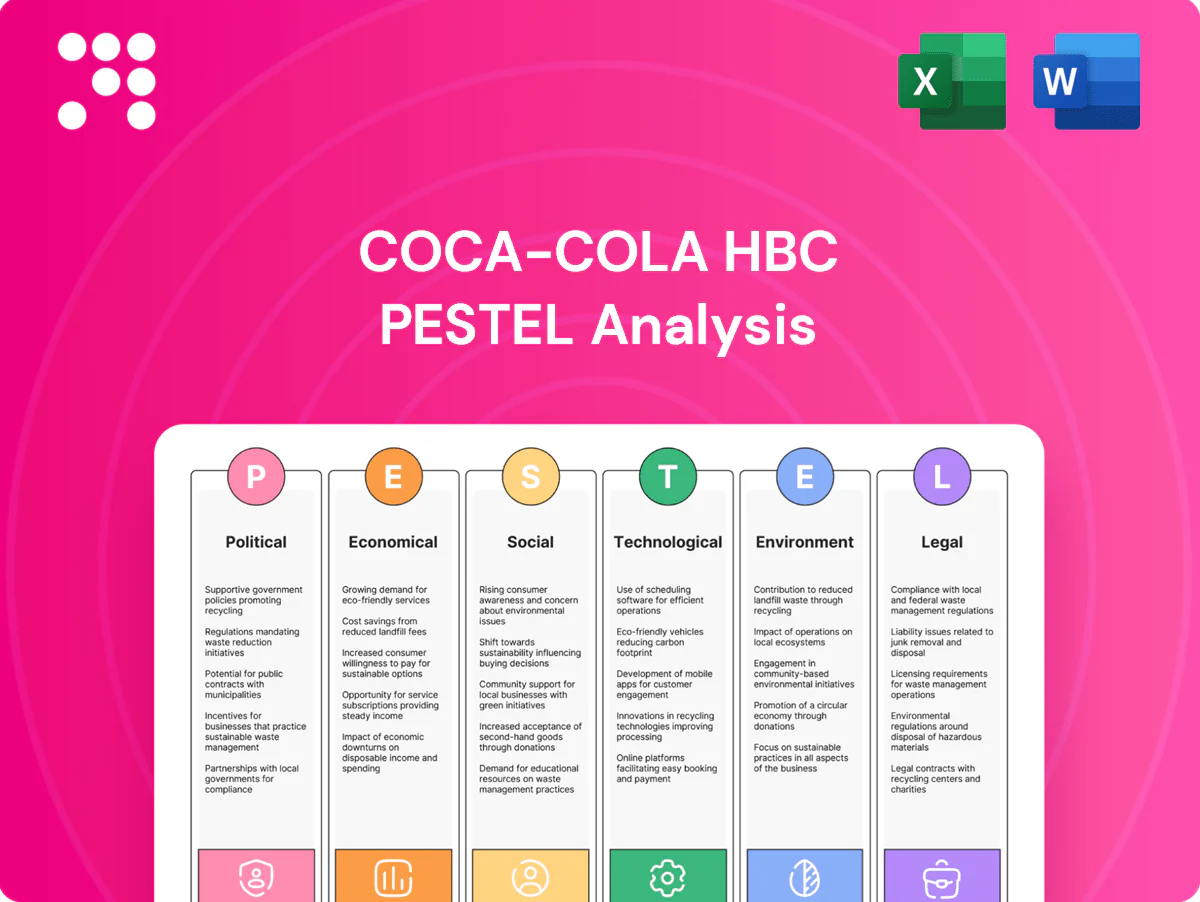

Political factors

Geopolitical stability across 29 markets

Operating across 29 markets in Europe, Africa and Asia exposes Coca‑Cola HBC to shifting political climates and regional conflicts that can rapidly disrupt supply chains, cross‑border logistics and raise security costs. Portfolio and route‑to‑market diversification across those 29 countries helps cushion shocks to volumes and margins. Continual country‑risk monitoring informs inventory positioning and capex allocation to reduce exposure.

Government policy shifts and industrial priorities

Shifts in subsidies, fuel pricing and industrial policy materially affect Coca‑Cola HBC’s production and distribution economics across its 28 operating countries, raising logistics and bottling costs. Local content and localization rules force sourcing realignments and can increase input costs for a group employing around 26,000 people. Active engagement with authorities helps secure operational continuity and speeds permits and investment approvals.

EU and regional regulations influence

EU directives including the Packaging and Packaging Waste Regulation (PPWR) across 27 member states and the Waste Framework targets such as 65% municipal recycling by 2035 set binding packaging, sustainability and trade standards for many of Coca‑Cola HBC’s markets.

Neighboring non‑EU countries (eg Norway, Switzerland) often harmonize these rules, tightening compliance and enabling procurement and packaging scale efficiencies when rules converge.

Where regulatory divergence persists, HBC must implement market‑specific pack formats, labeling and deposit systems, raising SKU complexity and incremental capex/OPEX.

Excise and health levies policy direction

Governments are expanding sugar and plastic levies—over 50 countries now apply sugar-sweetened beverage taxes—forcing changes to price architecture and channel mix; UK SDIL tiers (18p/24p per litre) show direct margin impacts. Coca-Cola HBC, operating in 28 countries, offsets pressure via reformulation, smaller pack sizes and industry advocacy backed by consumption and health evidence.

Trade, sanctions, and customs dynamics

Tariff changes and sanctions regimes (notably the 2022 exit from Russia) disrupt Coca‑Cola HBC ingredient and packaging flows, raising lead times and working capital when borders tighten; dual‑sourcing and local procurement reduce exposure, while robust compliance programs are essential to avoid costly disruptions and penalties.

- Trade barriers: higher lead times

- Working capital: increases under tighter customs

- Mitigation: dual‑sourcing, local buy

- Control: strict compliance programs

Multimarket beverage bottler: 29 markets, 50+ SSB taxes, political & packaging risk

Operating in 29 markets exposes Coca‑Cola HBC to political risks—conflicts, tariffs and regulation—that can disrupt supply chains and raise costs; the group employs ~26,000 people. EU PPWR and 50+ SSB taxes (UK SDIL 18p/24p) drive packaging/price changes. Mitigants: diversification, dual‑sourcing, reformulation and government engagement.

| Metric | Value |

|---|---|

| Markets | 29 |

| Employees | ~26,000 |

| SSB taxes | 50+ |

| UK SDIL | 18p/24p per L |

What is included in the product

Explores how macro-environmental factors uniquely affect Coca‑Cola HBC across Political, Economic, Social, Technological, Environmental and Legal dimensions, backed by data and current trends to support executives and investors with forward-looking insights and deck-ready formatting.

A concise, visually segmented PESTLE summary for Coca‑Cola HBC that can be dropped into presentations, edited for local markets, and shared across teams to streamline external risk discussions and strategic planning.

Economic factors

Macroeconomic cycles and consumer spending

Macroeconomic cycles materially affect Coca‑Cola HBC’s volumes and premium mix: swings in real disposable income drive category volumes and tilt consumers between mainstream and premium SKUs; the group operates in 28 countries and reported group revenue of €9.1bn in 2023. Downturns shift purchase patterns to value packs and affordability strategies, while recoveries favor premiumization and out‑of‑home channels. Agile pricing and promo levers are used to smooth volatility and protect margins.

Inflation and input cost volatility

Fluctuations in PET, sugar, aluminum and energy directly pressure Coca-Cola HBC gross margins by driving raw-material and production costs.

The company uses contracting, commodity hedging and targeted efficiency programmes to offset spikes and stabilise input cost exposure.

Active mix management and revenue growth management protect EBITDA while cost-to-serve optimisation preserves competitiveness across markets.

FX movements across multi-currency footprint

Coca-Cola HBC operates across 28 countries and around 600 million consumers, generating revenues and costs in dozens of currencies and creating meaningful translation and transaction risk. Local currency devaluations — notably in parts of Africa and Eastern Europe in 2023–24 — raise the local cost of imported inputs and capital goods. The group relies on natural hedges from local sourcing and selective financial hedging to dampen earnings volatility, and its pricing cadence is regularly adjusted to reflect currency moves.

Channel recovery and tourism flows

On-the-go and HoReCa channels have rebounded with mobility and tourism returning to near pre-pandemic levels by 2024 (UNWTO), lifting Coca-Cola HBC on-trade volumes during peak seasons and events.

Seasonality and major events amplify demand spikes; strategic chiller and cold-drink equipment placement in high-traffic venues maximizes capture.

Route-to-market has shifted dynamically to match footfall and shopper missions, prioritizing impulse locations and flexible distribution for urban tourists.

- tourism: near pre-2019 levels by 2024 (UNWTO)

- focus: on-the-go & HoReCa recovery

- tactics: chillers in high-footfall venues

- route: flexible, footfall-driven

Employment and wage trends

- Operating footprint: 28 countries

- EU wage growth 2024: ~5%

- Focus: automation + training

- Strategy: local supplier partnerships

Multimarket beverage bottler: 29 markets, 50+ SSB taxes, political & packaging risk

Macroeconomic cycles drive volumes and premium mix; group revenue €9.1bn in 2023, operating in 28 countries and ~600m consumers.

PET, sugar, aluminium and energy swings pressure gross margins; contracting, hedging and efficiency offset shocks.

Currency volatility and wage inflation (EU ~5% 2024) raise local costs; tourism and HoReCa recovered to near pre-2019 levels by 2024.

| Metric | Value | Impact |

|---|---|---|

| Revenue 2023 | €9.1bn | Scale |

| Countries | 28 | Currency risk |

| Consumers | ~600m | Demand base |

| EU wage growth 2024 | ~5% | Opex pressure |

Preview Before You Purchase

Coca-Cola HBC PESTLE Analysis

This preview of the Coca‑Cola HBC PESTLE Analysis is the exact, fully formatted document you’ll receive after purchase. No placeholders or teasers—the content, layout and structure shown are the finished file ready to download. Use it immediately for strategy, risk assessment and market insight.

Make Smarter Strategic Decisions with a Complete PESTEL View

Explore how political shifts, economic trends, social preferences, technological innovation, environmental pressures, and legal risks are shaping Coca-Cola HBC’s strategy and performance. Our concise PESTLE highlights key external drivers and risk hotspots—perfect for investors and strategists. Purchase the full, editable analysis to access actionable insights and immediate download.

Political factors

Geopolitical stability across 29 markets

Operating across 29 markets in Europe, Africa and Asia exposes Coca‑Cola HBC to shifting political climates and regional conflicts that can rapidly disrupt supply chains, cross‑border logistics and raise security costs. Portfolio and route‑to‑market diversification across those 29 countries helps cushion shocks to volumes and margins. Continual country‑risk monitoring informs inventory positioning and capex allocation to reduce exposure.

Government policy shifts and industrial priorities

Shifts in subsidies, fuel pricing and industrial policy materially affect Coca‑Cola HBC’s production and distribution economics across its 28 operating countries, raising logistics and bottling costs. Local content and localization rules force sourcing realignments and can increase input costs for a group employing around 26,000 people. Active engagement with authorities helps secure operational continuity and speeds permits and investment approvals.

EU and regional regulations influence

EU directives including the Packaging and Packaging Waste Regulation (PPWR) across 27 member states and the Waste Framework targets such as 65% municipal recycling by 2035 set binding packaging, sustainability and trade standards for many of Coca‑Cola HBC’s markets.

Neighboring non‑EU countries (eg Norway, Switzerland) often harmonize these rules, tightening compliance and enabling procurement and packaging scale efficiencies when rules converge.

Where regulatory divergence persists, HBC must implement market‑specific pack formats, labeling and deposit systems, raising SKU complexity and incremental capex/OPEX.

Excise and health levies policy direction

Governments are expanding sugar and plastic levies—over 50 countries now apply sugar-sweetened beverage taxes—forcing changes to price architecture and channel mix; UK SDIL tiers (18p/24p per litre) show direct margin impacts. Coca-Cola HBC, operating in 28 countries, offsets pressure via reformulation, smaller pack sizes and industry advocacy backed by consumption and health evidence.

Trade, sanctions, and customs dynamics

Tariff changes and sanctions regimes (notably the 2022 exit from Russia) disrupt Coca‑Cola HBC ingredient and packaging flows, raising lead times and working capital when borders tighten; dual‑sourcing and local procurement reduce exposure, while robust compliance programs are essential to avoid costly disruptions and penalties.

- Trade barriers: higher lead times

- Working capital: increases under tighter customs

- Mitigation: dual‑sourcing, local buy

- Control: strict compliance programs

Multimarket beverage bottler: 29 markets, 50+ SSB taxes, political & packaging risk

Operating in 29 markets exposes Coca‑Cola HBC to political risks—conflicts, tariffs and regulation—that can disrupt supply chains and raise costs; the group employs ~26,000 people. EU PPWR and 50+ SSB taxes (UK SDIL 18p/24p) drive packaging/price changes. Mitigants: diversification, dual‑sourcing, reformulation and government engagement.

| Metric | Value |

|---|---|

| Markets | 29 |

| Employees | ~26,000 |

| SSB taxes | 50+ |

| UK SDIL | 18p/24p per L |

What is included in the product

Explores how macro-environmental factors uniquely affect Coca‑Cola HBC across Political, Economic, Social, Technological, Environmental and Legal dimensions, backed by data and current trends to support executives and investors with forward-looking insights and deck-ready formatting.

A concise, visually segmented PESTLE summary for Coca‑Cola HBC that can be dropped into presentations, edited for local markets, and shared across teams to streamline external risk discussions and strategic planning.

Economic factors

Macroeconomic cycles and consumer spending

Macroeconomic cycles materially affect Coca‑Cola HBC’s volumes and premium mix: swings in real disposable income drive category volumes and tilt consumers between mainstream and premium SKUs; the group operates in 28 countries and reported group revenue of €9.1bn in 2023. Downturns shift purchase patterns to value packs and affordability strategies, while recoveries favor premiumization and out‑of‑home channels. Agile pricing and promo levers are used to smooth volatility and protect margins.

Inflation and input cost volatility

Fluctuations in PET, sugar, aluminum and energy directly pressure Coca-Cola HBC gross margins by driving raw-material and production costs.

The company uses contracting, commodity hedging and targeted efficiency programmes to offset spikes and stabilise input cost exposure.

Active mix management and revenue growth management protect EBITDA while cost-to-serve optimisation preserves competitiveness across markets.

FX movements across multi-currency footprint

Coca-Cola HBC operates across 28 countries and around 600 million consumers, generating revenues and costs in dozens of currencies and creating meaningful translation and transaction risk. Local currency devaluations — notably in parts of Africa and Eastern Europe in 2023–24 — raise the local cost of imported inputs and capital goods. The group relies on natural hedges from local sourcing and selective financial hedging to dampen earnings volatility, and its pricing cadence is regularly adjusted to reflect currency moves.

Channel recovery and tourism flows

On-the-go and HoReCa channels have rebounded with mobility and tourism returning to near pre-pandemic levels by 2024 (UNWTO), lifting Coca-Cola HBC on-trade volumes during peak seasons and events.

Seasonality and major events amplify demand spikes; strategic chiller and cold-drink equipment placement in high-traffic venues maximizes capture.

Route-to-market has shifted dynamically to match footfall and shopper missions, prioritizing impulse locations and flexible distribution for urban tourists.

- tourism: near pre-2019 levels by 2024 (UNWTO)

- focus: on-the-go & HoReCa recovery

- tactics: chillers in high-footfall venues

- route: flexible, footfall-driven

Employment and wage trends

- Operating footprint: 28 countries

- EU wage growth 2024: ~5%

- Focus: automation + training

- Strategy: local supplier partnerships

Multimarket beverage bottler: 29 markets, 50+ SSB taxes, political & packaging risk

Macroeconomic cycles drive volumes and premium mix; group revenue €9.1bn in 2023, operating in 28 countries and ~600m consumers.

PET, sugar, aluminium and energy swings pressure gross margins; contracting, hedging and efficiency offset shocks.

Currency volatility and wage inflation (EU ~5% 2024) raise local costs; tourism and HoReCa recovered to near pre-2019 levels by 2024.

| Metric | Value | Impact |

|---|---|---|

| Revenue 2023 | €9.1bn | Scale |

| Countries | 28 | Currency risk |

| Consumers | ~600m | Demand base |

| EU wage growth 2024 | ~5% | Opex pressure |

Preview Before You Purchase

Coca-Cola HBC PESTLE Analysis

This preview of the Coca‑Cola HBC PESTLE Analysis is the exact, fully formatted document you’ll receive after purchase. No placeholders or teasers—the content, layout and structure shown are the finished file ready to download. Use it immediately for strategy, risk assessment and market insight.

Original: $10.00

-65%$10.00

$3.50Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Explore how political shifts, economic trends, social preferences, technological innovation, environmental pressures, and legal risks are shaping Coca-Cola HBC’s strategy and performance. Our concise PESTLE highlights key external drivers and risk hotspots—perfect for investors and strategists. Purchase the full, editable analysis to access actionable insights and immediate download.

Political factors

Geopolitical stability across 29 markets

Operating across 29 markets in Europe, Africa and Asia exposes Coca‑Cola HBC to shifting political climates and regional conflicts that can rapidly disrupt supply chains, cross‑border logistics and raise security costs. Portfolio and route‑to‑market diversification across those 29 countries helps cushion shocks to volumes and margins. Continual country‑risk monitoring informs inventory positioning and capex allocation to reduce exposure.

Government policy shifts and industrial priorities

Shifts in subsidies, fuel pricing and industrial policy materially affect Coca‑Cola HBC’s production and distribution economics across its 28 operating countries, raising logistics and bottling costs. Local content and localization rules force sourcing realignments and can increase input costs for a group employing around 26,000 people. Active engagement with authorities helps secure operational continuity and speeds permits and investment approvals.

EU and regional regulations influence

EU directives including the Packaging and Packaging Waste Regulation (PPWR) across 27 member states and the Waste Framework targets such as 65% municipal recycling by 2035 set binding packaging, sustainability and trade standards for many of Coca‑Cola HBC’s markets.

Neighboring non‑EU countries (eg Norway, Switzerland) often harmonize these rules, tightening compliance and enabling procurement and packaging scale efficiencies when rules converge.

Where regulatory divergence persists, HBC must implement market‑specific pack formats, labeling and deposit systems, raising SKU complexity and incremental capex/OPEX.

Excise and health levies policy direction

Governments are expanding sugar and plastic levies—over 50 countries now apply sugar-sweetened beverage taxes—forcing changes to price architecture and channel mix; UK SDIL tiers (18p/24p per litre) show direct margin impacts. Coca-Cola HBC, operating in 28 countries, offsets pressure via reformulation, smaller pack sizes and industry advocacy backed by consumption and health evidence.

Trade, sanctions, and customs dynamics

Tariff changes and sanctions regimes (notably the 2022 exit from Russia) disrupt Coca‑Cola HBC ingredient and packaging flows, raising lead times and working capital when borders tighten; dual‑sourcing and local procurement reduce exposure, while robust compliance programs are essential to avoid costly disruptions and penalties.

- Trade barriers: higher lead times

- Working capital: increases under tighter customs

- Mitigation: dual‑sourcing, local buy

- Control: strict compliance programs

Multimarket beverage bottler: 29 markets, 50+ SSB taxes, political & packaging risk

Operating in 29 markets exposes Coca‑Cola HBC to political risks—conflicts, tariffs and regulation—that can disrupt supply chains and raise costs; the group employs ~26,000 people. EU PPWR and 50+ SSB taxes (UK SDIL 18p/24p) drive packaging/price changes. Mitigants: diversification, dual‑sourcing, reformulation and government engagement.

| Metric | Value |

|---|---|

| Markets | 29 |

| Employees | ~26,000 |

| SSB taxes | 50+ |

| UK SDIL | 18p/24p per L |

What is included in the product

Explores how macro-environmental factors uniquely affect Coca‑Cola HBC across Political, Economic, Social, Technological, Environmental and Legal dimensions, backed by data and current trends to support executives and investors with forward-looking insights and deck-ready formatting.

A concise, visually segmented PESTLE summary for Coca‑Cola HBC that can be dropped into presentations, edited for local markets, and shared across teams to streamline external risk discussions and strategic planning.

Economic factors

Macroeconomic cycles and consumer spending

Macroeconomic cycles materially affect Coca‑Cola HBC’s volumes and premium mix: swings in real disposable income drive category volumes and tilt consumers between mainstream and premium SKUs; the group operates in 28 countries and reported group revenue of €9.1bn in 2023. Downturns shift purchase patterns to value packs and affordability strategies, while recoveries favor premiumization and out‑of‑home channels. Agile pricing and promo levers are used to smooth volatility and protect margins.

Inflation and input cost volatility

Fluctuations in PET, sugar, aluminum and energy directly pressure Coca-Cola HBC gross margins by driving raw-material and production costs.

The company uses contracting, commodity hedging and targeted efficiency programmes to offset spikes and stabilise input cost exposure.

Active mix management and revenue growth management protect EBITDA while cost-to-serve optimisation preserves competitiveness across markets.

FX movements across multi-currency footprint

Coca-Cola HBC operates across 28 countries and around 600 million consumers, generating revenues and costs in dozens of currencies and creating meaningful translation and transaction risk. Local currency devaluations — notably in parts of Africa and Eastern Europe in 2023–24 — raise the local cost of imported inputs and capital goods. The group relies on natural hedges from local sourcing and selective financial hedging to dampen earnings volatility, and its pricing cadence is regularly adjusted to reflect currency moves.

Channel recovery and tourism flows

On-the-go and HoReCa channels have rebounded with mobility and tourism returning to near pre-pandemic levels by 2024 (UNWTO), lifting Coca-Cola HBC on-trade volumes during peak seasons and events.

Seasonality and major events amplify demand spikes; strategic chiller and cold-drink equipment placement in high-traffic venues maximizes capture.

Route-to-market has shifted dynamically to match footfall and shopper missions, prioritizing impulse locations and flexible distribution for urban tourists.

- tourism: near pre-2019 levels by 2024 (UNWTO)

- focus: on-the-go & HoReCa recovery

- tactics: chillers in high-footfall venues

- route: flexible, footfall-driven

Employment and wage trends

- Operating footprint: 28 countries

- EU wage growth 2024: ~5%

- Focus: automation + training

- Strategy: local supplier partnerships

Multimarket beverage bottler: 29 markets, 50+ SSB taxes, political & packaging risk

Macroeconomic cycles drive volumes and premium mix; group revenue €9.1bn in 2023, operating in 28 countries and ~600m consumers.

PET, sugar, aluminium and energy swings pressure gross margins; contracting, hedging and efficiency offset shocks.

Currency volatility and wage inflation (EU ~5% 2024) raise local costs; tourism and HoReCa recovered to near pre-2019 levels by 2024.

| Metric | Value | Impact |

|---|---|---|

| Revenue 2023 | €9.1bn | Scale |

| Countries | 28 | Currency risk |

| Consumers | ~600m | Demand base |

| EU wage growth 2024 | ~5% | Opex pressure |

Preview Before You Purchase

Coca-Cola HBC PESTLE Analysis

This preview of the Coca‑Cola HBC PESTLE Analysis is the exact, fully formatted document you’ll receive after purchase. No placeholders or teasers—the content, layout and structure shown are the finished file ready to download. Use it immediately for strategy, risk assessment and market insight.