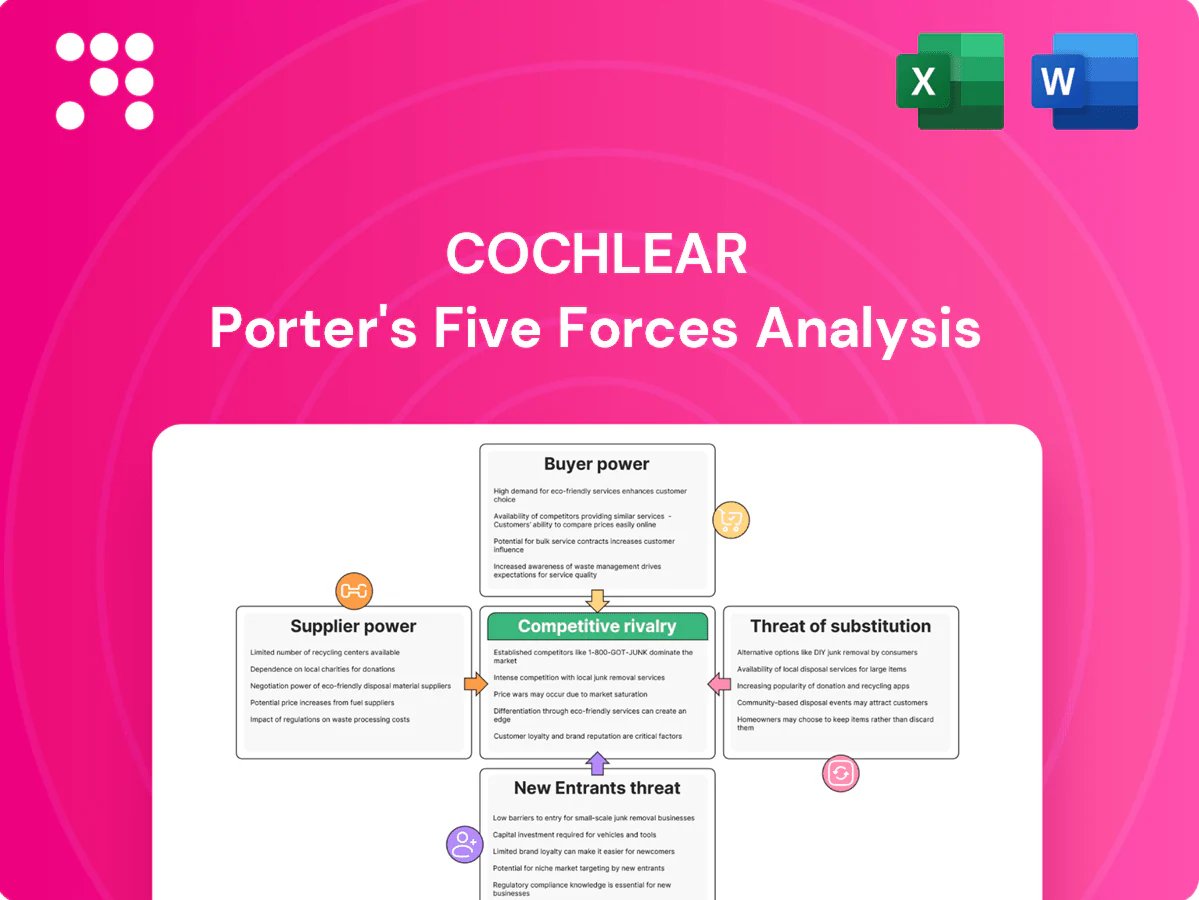

Cochlear Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Cochlear faces complex competitive dynamics—intense rivalry from established hearing-device makers, strong supplier relationships, and evolving substitute threats from emerging technologies. This brief snapshot highlights key pressures but only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights to inform strategy or investment decisions.

Suppliers Bargaining Power

Concentrated critical component base

Implant-grade metals, microelectronics and biocompatible polymers for Cochlear come from a very small pool of qualified suppliers, increasing supplier leverage. Limited alternatives and costly qualification/audit processes heighten switching friction, as noted in Cochlear’s FY2024 disclosures. Any supplier disruption can directly delay production schedules and order fulfilment. This concentrated base raises negotiation risk and supply-chain vulnerability.

Regulatory and quality constraints

ISO/GMP and medical device regulations lock Cochlear into exact specs and controlled processes, raising switching costs; FDA PMA median review was 282 days in recent FDA data and EU MDR notified body backlogs have pushed certifications toward 9–12 months. Revalidating a supplier entails batch testing, stability studies and regulatory filings that commonly span many months to over a year, elevating supplier bargaining power. That compliance burden constrains Cochlear’s ability to dual-source rapidly, limiting procurement flexibility and price leverage.

Customized components and tooling

Custom ASICs, coils and hermetic packages for cochlear implants require bespoke designs and tooling, with non-recurring engineering often exceeding $500,000 and lead times commonly 6–12 months in 2024, discouraging frequent supplier changes. Suppliers embedded in early designs can negotiate firmer commercial terms. Engineering-driven redesigns to qualify alternate sources introduce material technical risk and added cost.

Mitigating via scale and contracts

Cochlear’s volume commitments and long-term agreements—supporting its ~AUD1.9bn FY2024 revenue base—secure supplier priority and better pricing, while multi‑year forecasts give suppliers capacity visibility that lowers risk premiums. Dual‑sourcing where feasible and strategic inventory buffers further temper supplier leverage and reduce disruption risk.

- Volume commitments: priority pricing

- Forecasts: lower supplier risk premiums

- Dual‑sourcing: caps dependence

- Inventory buffers: reduce disruption exposure

Logistics and geo-risk exposure

Global supply chains expose Cochlear to geopolitical, freight and raw‑material volatility; FY2024 revenue ~AUD 1.8bn increases sensitivity to cost pass‑through and allocation pressure. Specialized sterilization and cleanroom packaging lengthen lead times and validation complexity, so disruptions often force expedited freight or premium sourcing. Suppliers can pass through inflationary input costs, squeezing margins.

- FY2024 revenue ~AUD 1.8bn — magnifies supply risk

- Specialized packaging/sterilization increases lead-time and cost

- Disruptions → expedited freight or allocation; supplier cost pass-through

Small supplier pool, long regulatory requalification and high NRE raise switching costs

Small pool of qualified suppliers (custom ASICs, implant metals, polymers) raises supplier leverage; Cochlear FY2024 revenue ~AUD 1.9bn amplifies impact. Regulatory requalification (FDA PMA median 282 days; EU MDR delays 9–12 months) elevates switching costs. NRE >AUD500k and 6–12 month lead times discourage changes. Volume contracts and dual‑sourcing partially mitigate risk.

| Metric | 2024 |

|---|---|

| Revenue | AUD 1.9bn |

| FDA PMA median | 282 days |

| NRE | >AUD 500k |

What is included in the product

Tailored Porter's Five Forces analysis for Cochlear that uncovers competitive drivers, buyer and supplier power, threat of substitutes and new entrants, and identifies disruptive forces and strategic defenses to protect market share.

A concise one-sheet Porter's Five Forces for Cochlear that visualizes strategic pressure with a radar chart, lets you adjust force levels for regulation/tech shifts, and drops straight into decks or Excel without macros—ideal for rapid boardroom decisions and cross-team use.

Customers Bargaining Power

Institutional procurement leverage

Hospitals, clinics and governments commonly procure implants via competitive tenders, consolidating demand and exerting significant price pressure on suppliers; public procurement represents roughly 12% of GDP (OECD). Aggregated volumes and bid-based selection force Cochlear to defend margins while value analysis committees increasingly scrutinize clinical outcomes and total cost of care. Discounts, bundled service agreements and extended warranties are routinely negotiated to secure contracts.

High switching costs post-implant

Once implanted patients are effectively locked into Cochlear’s ecosystem for years; the company reported an installed base of over 600,000 recipients globally in 2023–24, underpinning durable after‑market demand. Processors, proprietary software and accessories create recurring tie‑ins that reduce buyer power in the aftermarket. Upgrades still need budget approval in health systems and insurers, but vendor lock‑in sustains long‑term revenue streams.

Reimbursement shapes price sensitivity

Payer coverage and coding frameworks directly shape affordability and demand elasticity for cochlear implants; Medicare (about 63 million beneficiaries) and other public payers determine large market access. In markets with strong reimbursement price pressure eases, while weak or inconsistent coverage intensifies price sensitivity. HTA outcomes (eg NICE, CADTH) and rising real-world evidence drive funding decisions; delays or denials can stall patient conversions.

Clinical performance and support

- Installed base: over 600,000 recipients (2024)

- Global presence: 100+ countries

- Premium justified by outcomes and training

- Field service lowers switching risk

International mix and inequality

Buyer power varies by region: emerging markets are more price-sensitive and tender-driven while premium segments prioritize brand and clinical outcomes; Cochlear reported FY2024 revenue A$1.38bn, reflecting strength in premium markets. Currency swings in 2023–24 led to contract renegotiations and margin pressure in FX-exposed regions.

- Regional variance: high in tenders

- Emerging markets: price-sensitive

- Premium: brand-driven

- FY2024 revenue: A$1.38bn

- FX volatility: renegotiation risk

600,000+ installed base buffers margins despite tender price pressure

Hospitals/governments via tenders exert strong price pressure. Installed base and proprietary ecosystem (600,000+ recipients; 100+ countries) reduce aftermarket power. Reimbursement and FX volatility shape access and margins (FY2024 revenue A$1.38bn; Medicare ~63M).

| Metric | 2024 |

|---|---|

| Installed base | 600,000+ |

| Global reach | 100+ countries |

| FY revenue | A$1.38bn |

Full Version Awaits

Cochlear Porter's Five Forces Analysis

This preview shows the exact Cochlear Porter's Five Forces analysis you'll receive after purchase—no placeholders or mockups. The document is fully formatted, professionally written and ready for immediate download. What you see is the final deliverable.

Don't Miss the Bigger Picture

Cochlear faces complex competitive dynamics—intense rivalry from established hearing-device makers, strong supplier relationships, and evolving substitute threats from emerging technologies. This brief snapshot highlights key pressures but only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights to inform strategy or investment decisions.

Suppliers Bargaining Power

Concentrated critical component base

Implant-grade metals, microelectronics and biocompatible polymers for Cochlear come from a very small pool of qualified suppliers, increasing supplier leverage. Limited alternatives and costly qualification/audit processes heighten switching friction, as noted in Cochlear’s FY2024 disclosures. Any supplier disruption can directly delay production schedules and order fulfilment. This concentrated base raises negotiation risk and supply-chain vulnerability.

Regulatory and quality constraints

ISO/GMP and medical device regulations lock Cochlear into exact specs and controlled processes, raising switching costs; FDA PMA median review was 282 days in recent FDA data and EU MDR notified body backlogs have pushed certifications toward 9–12 months. Revalidating a supplier entails batch testing, stability studies and regulatory filings that commonly span many months to over a year, elevating supplier bargaining power. That compliance burden constrains Cochlear’s ability to dual-source rapidly, limiting procurement flexibility and price leverage.

Customized components and tooling

Custom ASICs, coils and hermetic packages for cochlear implants require bespoke designs and tooling, with non-recurring engineering often exceeding $500,000 and lead times commonly 6–12 months in 2024, discouraging frequent supplier changes. Suppliers embedded in early designs can negotiate firmer commercial terms. Engineering-driven redesigns to qualify alternate sources introduce material technical risk and added cost.

Mitigating via scale and contracts

Cochlear’s volume commitments and long-term agreements—supporting its ~AUD1.9bn FY2024 revenue base—secure supplier priority and better pricing, while multi‑year forecasts give suppliers capacity visibility that lowers risk premiums. Dual‑sourcing where feasible and strategic inventory buffers further temper supplier leverage and reduce disruption risk.

- Volume commitments: priority pricing

- Forecasts: lower supplier risk premiums

- Dual‑sourcing: caps dependence

- Inventory buffers: reduce disruption exposure

Logistics and geo-risk exposure

Global supply chains expose Cochlear to geopolitical, freight and raw‑material volatility; FY2024 revenue ~AUD 1.8bn increases sensitivity to cost pass‑through and allocation pressure. Specialized sterilization and cleanroom packaging lengthen lead times and validation complexity, so disruptions often force expedited freight or premium sourcing. Suppliers can pass through inflationary input costs, squeezing margins.

- FY2024 revenue ~AUD 1.8bn — magnifies supply risk

- Specialized packaging/sterilization increases lead-time and cost

- Disruptions → expedited freight or allocation; supplier cost pass-through

Small supplier pool, long regulatory requalification and high NRE raise switching costs

Small pool of qualified suppliers (custom ASICs, implant metals, polymers) raises supplier leverage; Cochlear FY2024 revenue ~AUD 1.9bn amplifies impact. Regulatory requalification (FDA PMA median 282 days; EU MDR delays 9–12 months) elevates switching costs. NRE >AUD500k and 6–12 month lead times discourage changes. Volume contracts and dual‑sourcing partially mitigate risk.

| Metric | 2024 |

|---|---|

| Revenue | AUD 1.9bn |

| FDA PMA median | 282 days |

| NRE | >AUD 500k |

What is included in the product

Tailored Porter's Five Forces analysis for Cochlear that uncovers competitive drivers, buyer and supplier power, threat of substitutes and new entrants, and identifies disruptive forces and strategic defenses to protect market share.

A concise one-sheet Porter's Five Forces for Cochlear that visualizes strategic pressure with a radar chart, lets you adjust force levels for regulation/tech shifts, and drops straight into decks or Excel without macros—ideal for rapid boardroom decisions and cross-team use.

Customers Bargaining Power

Institutional procurement leverage

Hospitals, clinics and governments commonly procure implants via competitive tenders, consolidating demand and exerting significant price pressure on suppliers; public procurement represents roughly 12% of GDP (OECD). Aggregated volumes and bid-based selection force Cochlear to defend margins while value analysis committees increasingly scrutinize clinical outcomes and total cost of care. Discounts, bundled service agreements and extended warranties are routinely negotiated to secure contracts.

High switching costs post-implant

Once implanted patients are effectively locked into Cochlear’s ecosystem for years; the company reported an installed base of over 600,000 recipients globally in 2023–24, underpinning durable after‑market demand. Processors, proprietary software and accessories create recurring tie‑ins that reduce buyer power in the aftermarket. Upgrades still need budget approval in health systems and insurers, but vendor lock‑in sustains long‑term revenue streams.

Reimbursement shapes price sensitivity

Payer coverage and coding frameworks directly shape affordability and demand elasticity for cochlear implants; Medicare (about 63 million beneficiaries) and other public payers determine large market access. In markets with strong reimbursement price pressure eases, while weak or inconsistent coverage intensifies price sensitivity. HTA outcomes (eg NICE, CADTH) and rising real-world evidence drive funding decisions; delays or denials can stall patient conversions.

Clinical performance and support

- Installed base: over 600,000 recipients (2024)

- Global presence: 100+ countries

- Premium justified by outcomes and training

- Field service lowers switching risk

International mix and inequality

Buyer power varies by region: emerging markets are more price-sensitive and tender-driven while premium segments prioritize brand and clinical outcomes; Cochlear reported FY2024 revenue A$1.38bn, reflecting strength in premium markets. Currency swings in 2023–24 led to contract renegotiations and margin pressure in FX-exposed regions.

- Regional variance: high in tenders

- Emerging markets: price-sensitive

- Premium: brand-driven

- FY2024 revenue: A$1.38bn

- FX volatility: renegotiation risk

600,000+ installed base buffers margins despite tender price pressure

Hospitals/governments via tenders exert strong price pressure. Installed base and proprietary ecosystem (600,000+ recipients; 100+ countries) reduce aftermarket power. Reimbursement and FX volatility shape access and margins (FY2024 revenue A$1.38bn; Medicare ~63M).

| Metric | 2024 |

|---|---|

| Installed base | 600,000+ |

| Global reach | 100+ countries |

| FY revenue | A$1.38bn |

Full Version Awaits

Cochlear Porter's Five Forces Analysis

This preview shows the exact Cochlear Porter's Five Forces analysis you'll receive after purchase—no placeholders or mockups. The document is fully formatted, professionally written and ready for immediate download. What you see is the final deliverable.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Cochlear faces complex competitive dynamics—intense rivalry from established hearing-device makers, strong supplier relationships, and evolving substitute threats from emerging technologies. This brief snapshot highlights key pressures but only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights to inform strategy or investment decisions.

Suppliers Bargaining Power

Concentrated critical component base

Implant-grade metals, microelectronics and biocompatible polymers for Cochlear come from a very small pool of qualified suppliers, increasing supplier leverage. Limited alternatives and costly qualification/audit processes heighten switching friction, as noted in Cochlear’s FY2024 disclosures. Any supplier disruption can directly delay production schedules and order fulfilment. This concentrated base raises negotiation risk and supply-chain vulnerability.

Regulatory and quality constraints

ISO/GMP and medical device regulations lock Cochlear into exact specs and controlled processes, raising switching costs; FDA PMA median review was 282 days in recent FDA data and EU MDR notified body backlogs have pushed certifications toward 9–12 months. Revalidating a supplier entails batch testing, stability studies and regulatory filings that commonly span many months to over a year, elevating supplier bargaining power. That compliance burden constrains Cochlear’s ability to dual-source rapidly, limiting procurement flexibility and price leverage.

Customized components and tooling

Custom ASICs, coils and hermetic packages for cochlear implants require bespoke designs and tooling, with non-recurring engineering often exceeding $500,000 and lead times commonly 6–12 months in 2024, discouraging frequent supplier changes. Suppliers embedded in early designs can negotiate firmer commercial terms. Engineering-driven redesigns to qualify alternate sources introduce material technical risk and added cost.

Mitigating via scale and contracts

Cochlear’s volume commitments and long-term agreements—supporting its ~AUD1.9bn FY2024 revenue base—secure supplier priority and better pricing, while multi‑year forecasts give suppliers capacity visibility that lowers risk premiums. Dual‑sourcing where feasible and strategic inventory buffers further temper supplier leverage and reduce disruption risk.

- Volume commitments: priority pricing

- Forecasts: lower supplier risk premiums

- Dual‑sourcing: caps dependence

- Inventory buffers: reduce disruption exposure

Logistics and geo-risk exposure

Global supply chains expose Cochlear to geopolitical, freight and raw‑material volatility; FY2024 revenue ~AUD 1.8bn increases sensitivity to cost pass‑through and allocation pressure. Specialized sterilization and cleanroom packaging lengthen lead times and validation complexity, so disruptions often force expedited freight or premium sourcing. Suppliers can pass through inflationary input costs, squeezing margins.

- FY2024 revenue ~AUD 1.8bn — magnifies supply risk

- Specialized packaging/sterilization increases lead-time and cost

- Disruptions → expedited freight or allocation; supplier cost pass-through

Small supplier pool, long regulatory requalification and high NRE raise switching costs

Small pool of qualified suppliers (custom ASICs, implant metals, polymers) raises supplier leverage; Cochlear FY2024 revenue ~AUD 1.9bn amplifies impact. Regulatory requalification (FDA PMA median 282 days; EU MDR delays 9–12 months) elevates switching costs. NRE >AUD500k and 6–12 month lead times discourage changes. Volume contracts and dual‑sourcing partially mitigate risk.

| Metric | 2024 |

|---|---|

| Revenue | AUD 1.9bn |

| FDA PMA median | 282 days |

| NRE | >AUD 500k |

What is included in the product

Tailored Porter's Five Forces analysis for Cochlear that uncovers competitive drivers, buyer and supplier power, threat of substitutes and new entrants, and identifies disruptive forces and strategic defenses to protect market share.

A concise one-sheet Porter's Five Forces for Cochlear that visualizes strategic pressure with a radar chart, lets you adjust force levels for regulation/tech shifts, and drops straight into decks or Excel without macros—ideal for rapid boardroom decisions and cross-team use.

Customers Bargaining Power

Institutional procurement leverage

Hospitals, clinics and governments commonly procure implants via competitive tenders, consolidating demand and exerting significant price pressure on suppliers; public procurement represents roughly 12% of GDP (OECD). Aggregated volumes and bid-based selection force Cochlear to defend margins while value analysis committees increasingly scrutinize clinical outcomes and total cost of care. Discounts, bundled service agreements and extended warranties are routinely negotiated to secure contracts.

High switching costs post-implant

Once implanted patients are effectively locked into Cochlear’s ecosystem for years; the company reported an installed base of over 600,000 recipients globally in 2023–24, underpinning durable after‑market demand. Processors, proprietary software and accessories create recurring tie‑ins that reduce buyer power in the aftermarket. Upgrades still need budget approval in health systems and insurers, but vendor lock‑in sustains long‑term revenue streams.

Reimbursement shapes price sensitivity

Payer coverage and coding frameworks directly shape affordability and demand elasticity for cochlear implants; Medicare (about 63 million beneficiaries) and other public payers determine large market access. In markets with strong reimbursement price pressure eases, while weak or inconsistent coverage intensifies price sensitivity. HTA outcomes (eg NICE, CADTH) and rising real-world evidence drive funding decisions; delays or denials can stall patient conversions.

Clinical performance and support

- Installed base: over 600,000 recipients (2024)

- Global presence: 100+ countries

- Premium justified by outcomes and training

- Field service lowers switching risk

International mix and inequality

Buyer power varies by region: emerging markets are more price-sensitive and tender-driven while premium segments prioritize brand and clinical outcomes; Cochlear reported FY2024 revenue A$1.38bn, reflecting strength in premium markets. Currency swings in 2023–24 led to contract renegotiations and margin pressure in FX-exposed regions.

- Regional variance: high in tenders

- Emerging markets: price-sensitive

- Premium: brand-driven

- FY2024 revenue: A$1.38bn

- FX volatility: renegotiation risk

600,000+ installed base buffers margins despite tender price pressure

Hospitals/governments via tenders exert strong price pressure. Installed base and proprietary ecosystem (600,000+ recipients; 100+ countries) reduce aftermarket power. Reimbursement and FX volatility shape access and margins (FY2024 revenue A$1.38bn; Medicare ~63M).

| Metric | 2024 |

|---|---|

| Installed base | 600,000+ |

| Global reach | 100+ countries |

| FY revenue | A$1.38bn |

Full Version Awaits

Cochlear Porter's Five Forces Analysis

This preview shows the exact Cochlear Porter's Five Forces analysis you'll receive after purchase—no placeholders or mockups. The document is fully formatted, professionally written and ready for immediate download. What you see is the final deliverable.