Colian Holding S.A. Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Colian Holding S.A. faces moderate competitive rivalry in branded confectionery and snacks, backed by strong Polish distribution yet pressured by price-sensitive retailers. Supplier power is limited while buyers gain influence via private labels and promotions. New entrants and substitutes create moderate disruption to margins. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for detailed, force-by-force insights.

Suppliers Bargaining Power

Dependence on key commodities

Colian depends on cocoa, sugar, dairy, nuts and spices, making input costs and availability sensitive to global commodity cycles. Cocoa and nuts face weather, geopolitical and sustainability pressures that can sharply reduce supply and raise supplier leverage in tight markets. Such volatility increases procurement risk for Colian, which mitigates exposure via long-term contracts and hedging strategies.

Supplier concentration in cocoa

Upstream cocoa supply is concentrated in origin countries—Côte d'Ivoire and Ghana account for ~60–65% of global output (2024)—and among large traders/processors (top firms like Olam, Barry Callebaut, Cargill dominate trade). Certification and traceability requirements (certified cocoa ~30% of supply in 2024) limit quick supplier switching, boosting bargaining power of qualified suppliers. Diversifying origins and certified partners can materially reduce supply and price risk.

Packaging and logistics dependencies

Specialized packaging films, cartons and bottling materials for Colian depend on a handful of regional vendors, concentrating supplier power. Transport capacity and energy cost volatility directly lift delivered input prices, and tightened logistics allow suppliers to apply surcharges. Strategic multi-sourcing and higher inventory buffers are used to reduce exposure. This limits suppliers’ ability to extract sustained margins.

Quality and certification barriers

Food safety and BRC/IFS plus sustainability standards substantially narrow Colian’s eligible supplier pool, raising the bargaining power of certified suppliers; higher qualification and compliance costs strengthen approved suppliers’ leverage and create audit-driven switching frictions, while supplier development programs can gradually reduce dependence.

- Food safety certifications tighten supply base

- Qualification costs increase supplier leverage

- Audits create switching frictions

- Supplier development lowers dependence

Scale vs. local ingredient options

For spices, fruits and sugar Colian faces moderated supplier power because viable local and regional alternatives exist, while its purchasing scale enables stronger negotiation of price, lead times and payment terms. Specialty ingredients and integrated flavor systems remain concentrated and less substitutable, preserving pockets of supplier leverage. Strategic partnerships and co-development agreements balance innovation needs with cost control.

- Local/regional alternatives reduce supplier leverage

- Scale improves negotiation on price and terms

- Specialty ingredients = higher supplier power

- Partnerships align innovation with cost management

60-65% cocoa share; 30% certified — long-term contracts & hedging

Colian is exposed to cocoa, sugar, dairy and packaging concentration; Côte d'Ivoire and Ghana supply ~60–65% of cocoa (2024) and certified cocoa ≈30% (2024), increasing supplier leverage in tight markets. Company uses long-term contracts, hedging and multi-sourcing to limit procurement risk and switching frictions.

| Input | Concentration | 2024 stat | Mitigation |

|---|---|---|---|

| Cocoa | High | 60–65% origin share; 30% certified | Long-term contracts, hedging |

| Packaging | Medium-High | Few regional vendors | Multi-sourcing, stockpiles |

What is included in the product

Tailored Porter’s Five Forces analysis for Colian Holding S.A. uncovering key drivers of competition, customer influence, supplier power, and substitution risks within Poland’s confectionery and beverage sectors. Identifies barriers protecting incumbents, emerging threats from private labels and health-oriented substitutes, and strategic levers to defend pricing and profitability.

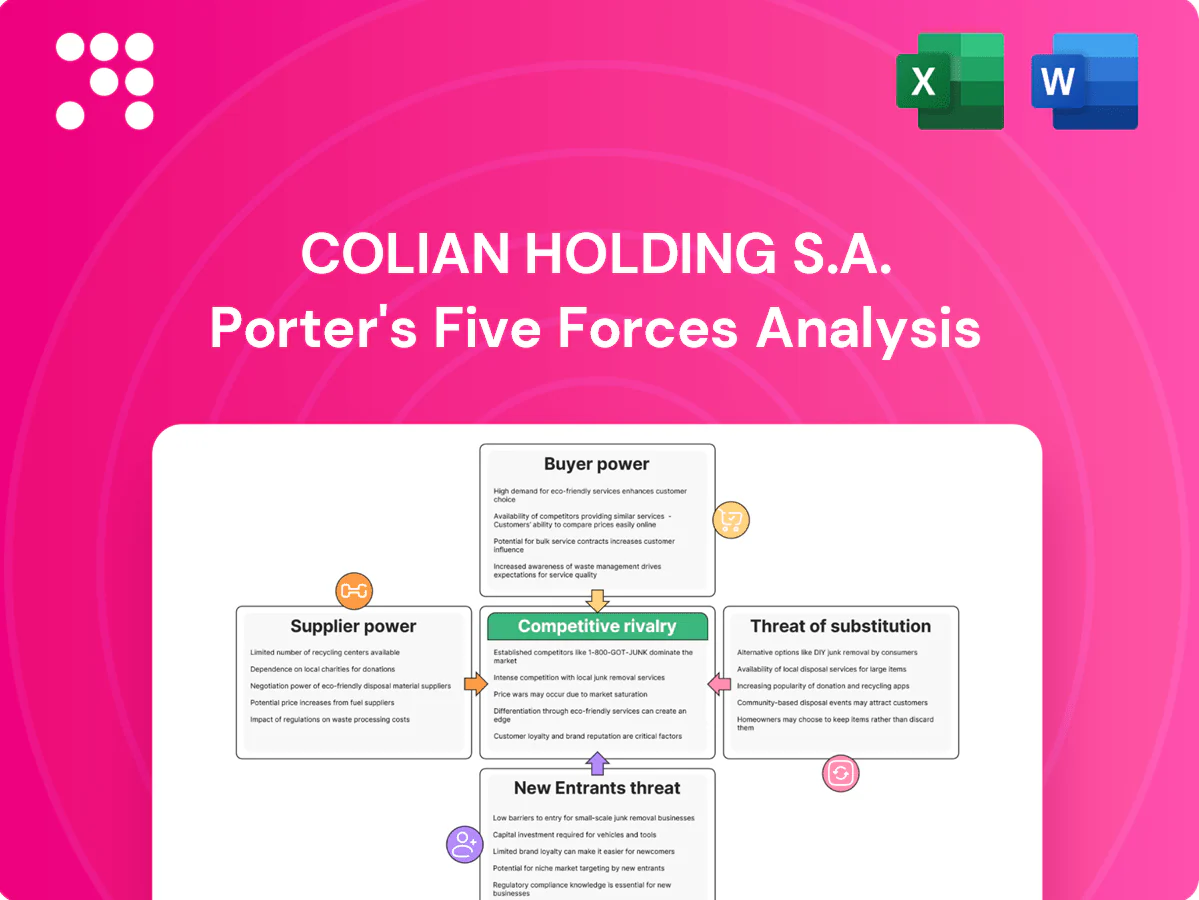

A concise one-sheet summary of Colian Holding's five forces—ideal for quick strategic decisions; toggle pressure levels with updated data, view a radar chart, and copy-ready layout for decks, dashboards or boardroom slides.

Customers Bargaining Power

Dominance of modern retail

Hypermarkets, discounters and large chains such as Biedronka (≈33% market share in Poland, Kantar 2023) and Lidl (≈10%) command shelf access and scale to demand lower prices, listing fees and promotional funding—trade spending in Polish FMCG is commonly near 15% of net sales. Consolidation (top 5 retailers ≈70%+ share) heightens their bargaining power, though Colian’s strong brands and differentiated SKUs partially offset pressure.

Private label competition

Retailers expand private labels in confectionery, snacks and culinary, with private-label penetration in Polish grocery around 28% in 2023, increasing category shelf share and price pressure. Comparable quality at lower prices strengthens buyer leverage and intensifies negotiations on margins and space, forcing retailers to seek larger promotional slots. Colian, with 2023 revenue near PLN 1.4bn, must defend with stronger branding, faster product innovation and value packs to protect margins.

Price-sensitive consumers

Confectionery and beverages show elastic demand with frequent promotions, which strengthens buyers’ ability to pressure Colian for discounts and EDLP models. Economic cycles and inflation increase price sensitivity, prompting retailers to demand lower prices or larger promotional allowances. Colian counters with bundling, optimized trade terms and portfolio mix management to protect margins and preserve shelf presence.

Export and distributor dynamics

Export and distributor dynamics: international distributors aggregate demand and pushed Colian to offer volume discounts; in 2024 Colian reported exports representing about 28% of sales, while Polish food exports reached €36bn in 2024, making distributors seek favorable terms. EUR/PLN volatility of ~6% in 2024 and varied local tariffs affected landed pricing; channel partners request exclusivity or marketing support; clear performance-based contracts (KPIs, rebates) balance power.

- EXPORT_SHARE_2024: ~28%

- POLAND_FOOD_EXPORTS_2024: €36bn

- EUR_PLN_VOL_2024: ~6%

- MITIGATION: KPI contracts, volume tiers, marketing co-funding

Data-driven category management

Data-driven category management gives retailers real-time POS visibility, enabling assortment rationalization and raising risk of delisting low-velocity SKUs that cannot prove incrementality; industry surveys in 2024 indicated CEE chains trimmed assortments by about 12% on average. This data advantage strengthens buyers’ negotiating stance, though joint business planning can align incentives and secure shelf space for Colian SKUs.

Retailer consolidation empowers buyers; high trade spend and private-label growth squeeze margins

Retailer consolidation (top 5 ≈70%+) and dominant chains (Biedronka ≈33%, Lidl ≈10%) drive strong buyer leverage; trade spend ~15% of net sales and private-label penetration ~28% increase margin pressure. Colian offsets via strong brands, SKU differentiation and export growth (~28% of sales). Data-driven delisting risk (assortments cut ~12%) and EUR/PLN volatility ~6% necessitate KPI contracts and co-funding.

| Metric | 2024 |

|---|---|

| Top-5 retailer share | ≈70%+ |

| Biedronka / Lidl | ≈33% / ≈10% |

| Trade spend | ~15% net sales |

| Private label | ~28% |

| Exports of Colian | ~28% sales |

| Poland food exports | €36bn |

| EUR/PLN vol | ~6% |

| Assortment cuts CEE | ~12% |

Same Document Delivered

Colian Holding S.A. Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The Colian Holding S.A. Porter's Five Forces analysis assesses high competitive rivalry in Polish FMCG, moderate supplier power, strong buyer influence, low threat of new entrants but meaningful threat from substitutes. Strategic implications highlight differentiation, cost control, and channel strength to sustain margins.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Colian Holding S.A. faces moderate competitive rivalry in branded confectionery and snacks, backed by strong Polish distribution yet pressured by price-sensitive retailers. Supplier power is limited while buyers gain influence via private labels and promotions. New entrants and substitutes create moderate disruption to margins. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for detailed, force-by-force insights.

Suppliers Bargaining Power

Dependence on key commodities

Colian depends on cocoa, sugar, dairy, nuts and spices, making input costs and availability sensitive to global commodity cycles. Cocoa and nuts face weather, geopolitical and sustainability pressures that can sharply reduce supply and raise supplier leverage in tight markets. Such volatility increases procurement risk for Colian, which mitigates exposure via long-term contracts and hedging strategies.

Supplier concentration in cocoa

Upstream cocoa supply is concentrated in origin countries—Côte d'Ivoire and Ghana account for ~60–65% of global output (2024)—and among large traders/processors (top firms like Olam, Barry Callebaut, Cargill dominate trade). Certification and traceability requirements (certified cocoa ~30% of supply in 2024) limit quick supplier switching, boosting bargaining power of qualified suppliers. Diversifying origins and certified partners can materially reduce supply and price risk.

Packaging and logistics dependencies

Specialized packaging films, cartons and bottling materials for Colian depend on a handful of regional vendors, concentrating supplier power. Transport capacity and energy cost volatility directly lift delivered input prices, and tightened logistics allow suppliers to apply surcharges. Strategic multi-sourcing and higher inventory buffers are used to reduce exposure. This limits suppliers’ ability to extract sustained margins.

Quality and certification barriers

Food safety and BRC/IFS plus sustainability standards substantially narrow Colian’s eligible supplier pool, raising the bargaining power of certified suppliers; higher qualification and compliance costs strengthen approved suppliers’ leverage and create audit-driven switching frictions, while supplier development programs can gradually reduce dependence.

- Food safety certifications tighten supply base

- Qualification costs increase supplier leverage

- Audits create switching frictions

- Supplier development lowers dependence

Scale vs. local ingredient options

For spices, fruits and sugar Colian faces moderated supplier power because viable local and regional alternatives exist, while its purchasing scale enables stronger negotiation of price, lead times and payment terms. Specialty ingredients and integrated flavor systems remain concentrated and less substitutable, preserving pockets of supplier leverage. Strategic partnerships and co-development agreements balance innovation needs with cost control.

- Local/regional alternatives reduce supplier leverage

- Scale improves negotiation on price and terms

- Specialty ingredients = higher supplier power

- Partnerships align innovation with cost management

60-65% cocoa share; 30% certified — long-term contracts & hedging

Colian is exposed to cocoa, sugar, dairy and packaging concentration; Côte d'Ivoire and Ghana supply ~60–65% of cocoa (2024) and certified cocoa ≈30% (2024), increasing supplier leverage in tight markets. Company uses long-term contracts, hedging and multi-sourcing to limit procurement risk and switching frictions.

| Input | Concentration | 2024 stat | Mitigation |

|---|---|---|---|

| Cocoa | High | 60–65% origin share; 30% certified | Long-term contracts, hedging |

| Packaging | Medium-High | Few regional vendors | Multi-sourcing, stockpiles |

What is included in the product

Tailored Porter’s Five Forces analysis for Colian Holding S.A. uncovering key drivers of competition, customer influence, supplier power, and substitution risks within Poland’s confectionery and beverage sectors. Identifies barriers protecting incumbents, emerging threats from private labels and health-oriented substitutes, and strategic levers to defend pricing and profitability.

A concise one-sheet summary of Colian Holding's five forces—ideal for quick strategic decisions; toggle pressure levels with updated data, view a radar chart, and copy-ready layout for decks, dashboards or boardroom slides.

Customers Bargaining Power

Dominance of modern retail

Hypermarkets, discounters and large chains such as Biedronka (≈33% market share in Poland, Kantar 2023) and Lidl (≈10%) command shelf access and scale to demand lower prices, listing fees and promotional funding—trade spending in Polish FMCG is commonly near 15% of net sales. Consolidation (top 5 retailers ≈70%+ share) heightens their bargaining power, though Colian’s strong brands and differentiated SKUs partially offset pressure.

Private label competition

Retailers expand private labels in confectionery, snacks and culinary, with private-label penetration in Polish grocery around 28% in 2023, increasing category shelf share and price pressure. Comparable quality at lower prices strengthens buyer leverage and intensifies negotiations on margins and space, forcing retailers to seek larger promotional slots. Colian, with 2023 revenue near PLN 1.4bn, must defend with stronger branding, faster product innovation and value packs to protect margins.

Price-sensitive consumers

Confectionery and beverages show elastic demand with frequent promotions, which strengthens buyers’ ability to pressure Colian for discounts and EDLP models. Economic cycles and inflation increase price sensitivity, prompting retailers to demand lower prices or larger promotional allowances. Colian counters with bundling, optimized trade terms and portfolio mix management to protect margins and preserve shelf presence.

Export and distributor dynamics

Export and distributor dynamics: international distributors aggregate demand and pushed Colian to offer volume discounts; in 2024 Colian reported exports representing about 28% of sales, while Polish food exports reached €36bn in 2024, making distributors seek favorable terms. EUR/PLN volatility of ~6% in 2024 and varied local tariffs affected landed pricing; channel partners request exclusivity or marketing support; clear performance-based contracts (KPIs, rebates) balance power.

- EXPORT_SHARE_2024: ~28%

- POLAND_FOOD_EXPORTS_2024: €36bn

- EUR_PLN_VOL_2024: ~6%

- MITIGATION: KPI contracts, volume tiers, marketing co-funding

Data-driven category management

Data-driven category management gives retailers real-time POS visibility, enabling assortment rationalization and raising risk of delisting low-velocity SKUs that cannot prove incrementality; industry surveys in 2024 indicated CEE chains trimmed assortments by about 12% on average. This data advantage strengthens buyers’ negotiating stance, though joint business planning can align incentives and secure shelf space for Colian SKUs.

Retailer consolidation empowers buyers; high trade spend and private-label growth squeeze margins

Retailer consolidation (top 5 ≈70%+) and dominant chains (Biedronka ≈33%, Lidl ≈10%) drive strong buyer leverage; trade spend ~15% of net sales and private-label penetration ~28% increase margin pressure. Colian offsets via strong brands, SKU differentiation and export growth (~28% of sales). Data-driven delisting risk (assortments cut ~12%) and EUR/PLN volatility ~6% necessitate KPI contracts and co-funding.

| Metric | 2024 |

|---|---|

| Top-5 retailer share | ≈70%+ |

| Biedronka / Lidl | ≈33% / ≈10% |

| Trade spend | ~15% net sales |

| Private label | ~28% |

| Exports of Colian | ~28% sales |

| Poland food exports | €36bn |

| EUR/PLN vol | ~6% |

| Assortment cuts CEE | ~12% |

Same Document Delivered

Colian Holding S.A. Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The Colian Holding S.A. Porter's Five Forces analysis assesses high competitive rivalry in Polish FMCG, moderate supplier power, strong buyer influence, low threat of new entrants but meaningful threat from substitutes. Strategic implications highlight differentiation, cost control, and channel strength to sustain margins.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Colian Holding S.A. faces moderate competitive rivalry in branded confectionery and snacks, backed by strong Polish distribution yet pressured by price-sensitive retailers. Supplier power is limited while buyers gain influence via private labels and promotions. New entrants and substitutes create moderate disruption to margins. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for detailed, force-by-force insights.

Suppliers Bargaining Power

Dependence on key commodities

Colian depends on cocoa, sugar, dairy, nuts and spices, making input costs and availability sensitive to global commodity cycles. Cocoa and nuts face weather, geopolitical and sustainability pressures that can sharply reduce supply and raise supplier leverage in tight markets. Such volatility increases procurement risk for Colian, which mitigates exposure via long-term contracts and hedging strategies.

Supplier concentration in cocoa

Upstream cocoa supply is concentrated in origin countries—Côte d'Ivoire and Ghana account for ~60–65% of global output (2024)—and among large traders/processors (top firms like Olam, Barry Callebaut, Cargill dominate trade). Certification and traceability requirements (certified cocoa ~30% of supply in 2024) limit quick supplier switching, boosting bargaining power of qualified suppliers. Diversifying origins and certified partners can materially reduce supply and price risk.

Packaging and logistics dependencies

Specialized packaging films, cartons and bottling materials for Colian depend on a handful of regional vendors, concentrating supplier power. Transport capacity and energy cost volatility directly lift delivered input prices, and tightened logistics allow suppliers to apply surcharges. Strategic multi-sourcing and higher inventory buffers are used to reduce exposure. This limits suppliers’ ability to extract sustained margins.

Quality and certification barriers

Food safety and BRC/IFS plus sustainability standards substantially narrow Colian’s eligible supplier pool, raising the bargaining power of certified suppliers; higher qualification and compliance costs strengthen approved suppliers’ leverage and create audit-driven switching frictions, while supplier development programs can gradually reduce dependence.

- Food safety certifications tighten supply base

- Qualification costs increase supplier leverage

- Audits create switching frictions

- Supplier development lowers dependence

Scale vs. local ingredient options

For spices, fruits and sugar Colian faces moderated supplier power because viable local and regional alternatives exist, while its purchasing scale enables stronger negotiation of price, lead times and payment terms. Specialty ingredients and integrated flavor systems remain concentrated and less substitutable, preserving pockets of supplier leverage. Strategic partnerships and co-development agreements balance innovation needs with cost control.

- Local/regional alternatives reduce supplier leverage

- Scale improves negotiation on price and terms

- Specialty ingredients = higher supplier power

- Partnerships align innovation with cost management

60-65% cocoa share; 30% certified — long-term contracts & hedging

Colian is exposed to cocoa, sugar, dairy and packaging concentration; Côte d'Ivoire and Ghana supply ~60–65% of cocoa (2024) and certified cocoa ≈30% (2024), increasing supplier leverage in tight markets. Company uses long-term contracts, hedging and multi-sourcing to limit procurement risk and switching frictions.

| Input | Concentration | 2024 stat | Mitigation |

|---|---|---|---|

| Cocoa | High | 60–65% origin share; 30% certified | Long-term contracts, hedging |

| Packaging | Medium-High | Few regional vendors | Multi-sourcing, stockpiles |

What is included in the product

Tailored Porter’s Five Forces analysis for Colian Holding S.A. uncovering key drivers of competition, customer influence, supplier power, and substitution risks within Poland’s confectionery and beverage sectors. Identifies barriers protecting incumbents, emerging threats from private labels and health-oriented substitutes, and strategic levers to defend pricing and profitability.

A concise one-sheet summary of Colian Holding's five forces—ideal for quick strategic decisions; toggle pressure levels with updated data, view a radar chart, and copy-ready layout for decks, dashboards or boardroom slides.

Customers Bargaining Power

Dominance of modern retail

Hypermarkets, discounters and large chains such as Biedronka (≈33% market share in Poland, Kantar 2023) and Lidl (≈10%) command shelf access and scale to demand lower prices, listing fees and promotional funding—trade spending in Polish FMCG is commonly near 15% of net sales. Consolidation (top 5 retailers ≈70%+ share) heightens their bargaining power, though Colian’s strong brands and differentiated SKUs partially offset pressure.

Private label competition

Retailers expand private labels in confectionery, snacks and culinary, with private-label penetration in Polish grocery around 28% in 2023, increasing category shelf share and price pressure. Comparable quality at lower prices strengthens buyer leverage and intensifies negotiations on margins and space, forcing retailers to seek larger promotional slots. Colian, with 2023 revenue near PLN 1.4bn, must defend with stronger branding, faster product innovation and value packs to protect margins.

Price-sensitive consumers

Confectionery and beverages show elastic demand with frequent promotions, which strengthens buyers’ ability to pressure Colian for discounts and EDLP models. Economic cycles and inflation increase price sensitivity, prompting retailers to demand lower prices or larger promotional allowances. Colian counters with bundling, optimized trade terms and portfolio mix management to protect margins and preserve shelf presence.

Export and distributor dynamics

Export and distributor dynamics: international distributors aggregate demand and pushed Colian to offer volume discounts; in 2024 Colian reported exports representing about 28% of sales, while Polish food exports reached €36bn in 2024, making distributors seek favorable terms. EUR/PLN volatility of ~6% in 2024 and varied local tariffs affected landed pricing; channel partners request exclusivity or marketing support; clear performance-based contracts (KPIs, rebates) balance power.

- EXPORT_SHARE_2024: ~28%

- POLAND_FOOD_EXPORTS_2024: €36bn

- EUR_PLN_VOL_2024: ~6%

- MITIGATION: KPI contracts, volume tiers, marketing co-funding

Data-driven category management

Data-driven category management gives retailers real-time POS visibility, enabling assortment rationalization and raising risk of delisting low-velocity SKUs that cannot prove incrementality; industry surveys in 2024 indicated CEE chains trimmed assortments by about 12% on average. This data advantage strengthens buyers’ negotiating stance, though joint business planning can align incentives and secure shelf space for Colian SKUs.

Retailer consolidation empowers buyers; high trade spend and private-label growth squeeze margins

Retailer consolidation (top 5 ≈70%+) and dominant chains (Biedronka ≈33%, Lidl ≈10%) drive strong buyer leverage; trade spend ~15% of net sales and private-label penetration ~28% increase margin pressure. Colian offsets via strong brands, SKU differentiation and export growth (~28% of sales). Data-driven delisting risk (assortments cut ~12%) and EUR/PLN volatility ~6% necessitate KPI contracts and co-funding.

| Metric | 2024 |

|---|---|

| Top-5 retailer share | ≈70%+ |

| Biedronka / Lidl | ≈33% / ≈10% |

| Trade spend | ~15% net sales |

| Private label | ~28% |

| Exports of Colian | ~28% sales |

| Poland food exports | €36bn |

| EUR/PLN vol | ~6% |

| Assortment cuts CEE | ~12% |

Same Document Delivered

Colian Holding S.A. Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The Colian Holding S.A. Porter's Five Forces analysis assesses high competitive rivalry in Polish FMCG, moderate supplier power, strong buyer influence, low threat of new entrants but meaningful threat from substitutes. Strategic implications highlight differentiation, cost control, and channel strength to sustain margins.