Colony Bank Boston Consulting Group Matrix

See the Bigger Picture

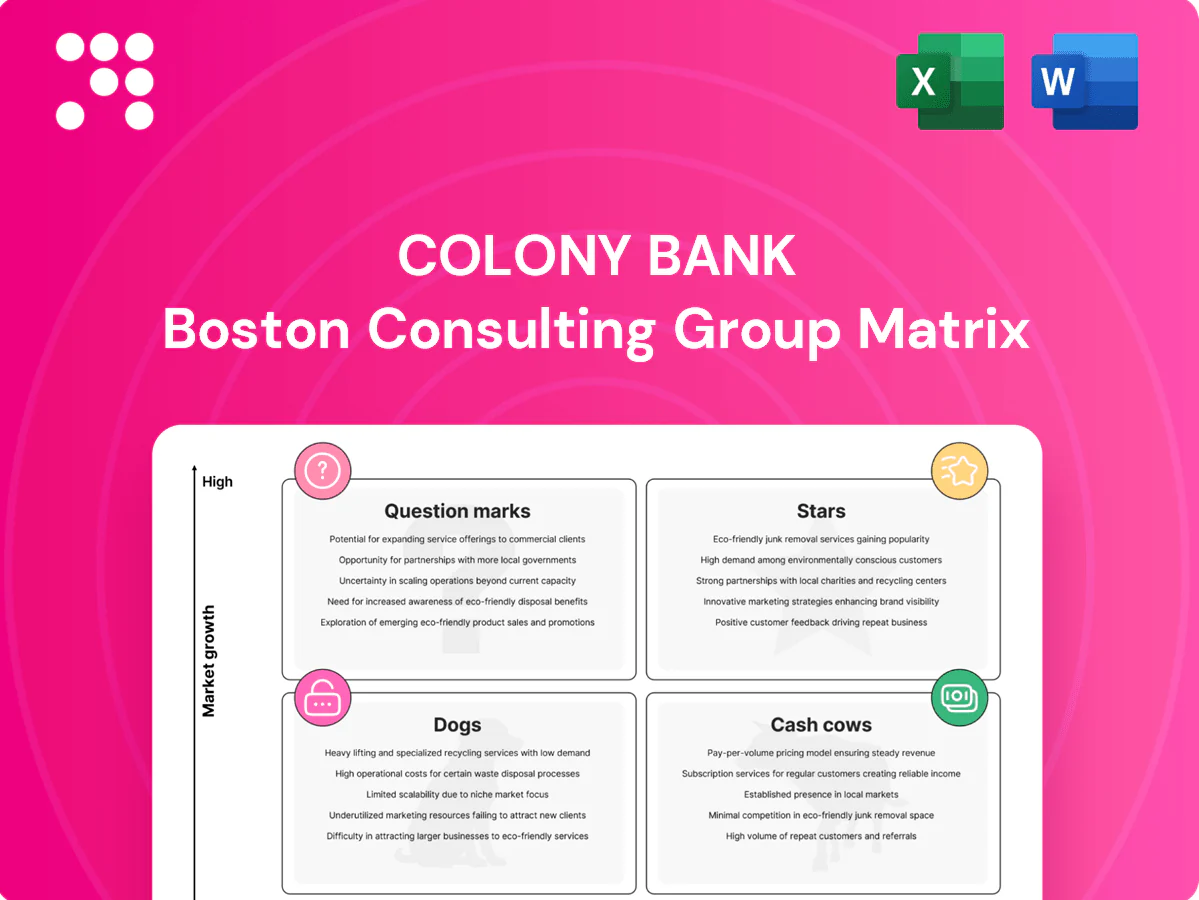

Curious where Colony Bank’s products land—Stars, Cash Cows, Dogs, or Question Marks? This snapshot hints at strengths and blindspots, but the full BCG Matrix gives quadrant-level placements, data-backed recommendations, and a clear playbook for where to invest or divest. Purchase the complete report for a Word + Excel pack that lets you present and act on strategy—fast, practical, and made for busy leaders.

Stars

SBA/USDA-backed small business lending

Government-guaranteed SBA (up to 85% guarantee) and USDA lending fits Georgia’s growing SMB market and Colony’s community ties give it a distribution edge. Demand and pipelines are strong, but underwriting and servicing tie up working capital and can slow median close times to roughly 30–45 days. Keep investing in brand, speed-to-close, and specialist bankers. Sustain share now and it will generate substantial cash flow later.

Commercial & treasury management for growth businesses

Middle-market clients demand payments, liquidity, and fraud tools urgently; 2024 adoption surged roughly 40% year-over-year as faster payments and API-led solutions become table stakes.

Colony can lead locally by combining responsive service and bundled pricing, capturing higher fee yield and reducing churn through tailored suites and relationship coverage.

Implementation is resource-intensive—invest in onboarding, APIs, and dedicated coverage teams now to realize retention gains and incremental fee revenue that offset setup costs.

Digital account opening and mobile banking

Digital account opening and mobile banking drive top-of-funnel acquisition for Colony Bank, meeting the 2024 trend of digital-first preferences where roughly two-thirds of US consumers favor online-first banking and digital account openings grew ~20% YoY. Strong usage growth and cross-sell convert those new customers into lower-cost deposit balances, improving share capture despite heavy tech spend. Continued UX iteration and instant verification cut dropout rates and shorten time-to-deposit, increasing lifetime value per acquired customer.

Owner-occupied CRE and professional practice lending

Owner-occupied CRE for physicians, dentists and accountants is a stable, expanding niche as practices borrow for space and equipment; Colony’s local underwriting and same-day decisioning can dominate referrals and lead capture in 2024. It requires tight credit discipline, active portfolio monitoring, and tailored terms to retain profitability and control concentration risk.

- Focus: professional practices

- Advantage: local underwriting & speed

- Requirement: strict credit & monitoring

- Strategy: tailored terms + referral ecosystem

Agribusiness banking in expanding counties

Agribusiness banking in expanding counties is a Star for Colony: Georgia agriculture drives a $75B state economic impact (UGA 2024) and is modernizing, increasing demand for working capital and equipment finance; Colony’s footprint can capture share but requires field expertise and seasonal cash management, so double down on specialists and data-driven risk tools.

- Focus: working capital & equipment

- Capability: seasonal cash mgmt + field teams

- Tooling: data-driven risk models

SBA/USDA, digital and ag demand surge in 2024 — speed, specialists and APIs win

Colony’s Stars—SBA/USDA lending, digital acquisition, agribusiness, owner-occupied CRE—show strong 2024 demand: SBA guarantees to 85%, median close 30–45 days, digital account openings +20% YoY and ~66% consumers online-first, Georgia ag $75B impact. Invest in speed, specialist coverage, APIs and seasonal cash tools to sustain share and future cash flow.

| Segment | 2024 KPI | Priority |

|---|---|---|

| SBA/USDA | 85% guarantee; 30–45d close | Specialists & faster underwriting |

| Digital | +20% accnt opens; 66% pref | UX, instant verification, APIs |

| Agribusiness | $75B state impact | Field teams & seasonal finance |

What is included in the product

Comprehensive BCG Matrix review of Colony Bank's units, identifying Stars, Cash Cows, Question Marks, Dogs and strategic moves.

One-page BCG matrix placing Colony Bank units into quadrants to simplify strategy and export cleanly for C-level decks

Cash Cows

Low-cost core deposits from long-time customers

Relationship checking and savings at Colony Bank are mature, sticky, and cheap to service, supplying the engine for margins and stability; industry data in 2024 showed core deposit costs under 1% versus wholesale funding north of 3%, supporting durable net interest margin. Promotion needs are light—focus on high-quality service. Optimize pricing and digital self-service to quietly boost yield and increase cross-sell conversion.

Established community CRE portfolios

Established community CRE portfolios are stabilized with ~93% occupancy and seasoned borrowers, delivering predictable cash flow and 2–3% annual NOI growth in 2024. Growth is modest, but average loan spreads remain near 250 bps and fee income is steady. Minimal marketing is required; focus on renewal discipline with ~85–90% renewal rates. Harvest fees and keep credit costs low through conservative underwriting.

Basic treasury services (ACH, wires, RDC at scale)

Basic treasury services (ACH, wires, RDC at scale) are entrenched with existing business clients, driving low churn and steady recurring revenue; the ACH network processes tens of billions of transactions annually (Nacha). Operational unit costs decline as volumes scale on existing rails, so small fee adjustments flow largely to the bottom line. Focus on reliability and uptime; avoid over-engineering features that raise fixed costs and risk service disruption.

Service charges and interchange from legacy accounts

Service charges and interchange from legacy accounts are everyday fees and card-swipe revenue: boring but dependable, driven by existing customer volumes rather than market expansion. Light-touch, compliance-aware optimization (pricing hygiene, dispute handling) yields steady margin uplift while minimizing complaints. Focus on operational efficiency and retention to preserve cash cow returns.

- Everyday fees: stable recurring income

- Card swipe: predictable interchange

- Volumes track base, not market

- Optimize lightly, prioritize compliance

- Reduce complaints, maximize efficiency

Time deposits/CDs from loyal savers

Time deposits/CDs from loyal savers are a steady, non-flashy funding source for Colony Bank when priced inside a normalized rate band, preserving margins while avoiding broad repricing; branch-led sales are simple, repeatable, and cost-efficient.

- Branch-led acquisition

- Stable margins in normal rate bands

- Use targeted specials, avoid blanket repricing

Core 1%, wholesale 3%, CRE 93% — steady margins

Core deposits <1% vs wholesale >3% (2024), CRE 93% occ., NOI +2–3% (2024), avg loan spread ~250bps, renewals 85–90%, ACH tens of billions txns — low promo, high retention, steady margins.

| Metric | 2024 |

|---|---|

| Core deposit cost | <1% |

| Wholesale funding | >3% |

| CRE occupancy | 93% |

| NOI growth | 2–3% |

| Loan spread | ~250bps |

| Renewal rate | 85–90% |

| ACH volume | tens of billions |

Preview = Final Product

Colony Bank BCG Matrix

The file you're previewing is the exact Colony Bank BCG Matrix you'll receive after purchase. No watermarks, no placeholders—just the fully formatted, ready-to-use report. It’s editable, printable, and designed by strategy pros for immediate presentation. Buy once and download instantly—no surprises, no extra steps.

See the Bigger Picture

Curious where Colony Bank’s products land—Stars, Cash Cows, Dogs, or Question Marks? This snapshot hints at strengths and blindspots, but the full BCG Matrix gives quadrant-level placements, data-backed recommendations, and a clear playbook for where to invest or divest. Purchase the complete report for a Word + Excel pack that lets you present and act on strategy—fast, practical, and made for busy leaders.

Stars

SBA/USDA-backed small business lending

Government-guaranteed SBA (up to 85% guarantee) and USDA lending fits Georgia’s growing SMB market and Colony’s community ties give it a distribution edge. Demand and pipelines are strong, but underwriting and servicing tie up working capital and can slow median close times to roughly 30–45 days. Keep investing in brand, speed-to-close, and specialist bankers. Sustain share now and it will generate substantial cash flow later.

Commercial & treasury management for growth businesses

Middle-market clients demand payments, liquidity, and fraud tools urgently; 2024 adoption surged roughly 40% year-over-year as faster payments and API-led solutions become table stakes.

Colony can lead locally by combining responsive service and bundled pricing, capturing higher fee yield and reducing churn through tailored suites and relationship coverage.

Implementation is resource-intensive—invest in onboarding, APIs, and dedicated coverage teams now to realize retention gains and incremental fee revenue that offset setup costs.

Digital account opening and mobile banking

Digital account opening and mobile banking drive top-of-funnel acquisition for Colony Bank, meeting the 2024 trend of digital-first preferences where roughly two-thirds of US consumers favor online-first banking and digital account openings grew ~20% YoY. Strong usage growth and cross-sell convert those new customers into lower-cost deposit balances, improving share capture despite heavy tech spend. Continued UX iteration and instant verification cut dropout rates and shorten time-to-deposit, increasing lifetime value per acquired customer.

Owner-occupied CRE and professional practice lending

Owner-occupied CRE for physicians, dentists and accountants is a stable, expanding niche as practices borrow for space and equipment; Colony’s local underwriting and same-day decisioning can dominate referrals and lead capture in 2024. It requires tight credit discipline, active portfolio monitoring, and tailored terms to retain profitability and control concentration risk.

- Focus: professional practices

- Advantage: local underwriting & speed

- Requirement: strict credit & monitoring

- Strategy: tailored terms + referral ecosystem

Agribusiness banking in expanding counties

Agribusiness banking in expanding counties is a Star for Colony: Georgia agriculture drives a $75B state economic impact (UGA 2024) and is modernizing, increasing demand for working capital and equipment finance; Colony’s footprint can capture share but requires field expertise and seasonal cash management, so double down on specialists and data-driven risk tools.

- Focus: working capital & equipment

- Capability: seasonal cash mgmt + field teams

- Tooling: data-driven risk models

SBA/USDA, digital and ag demand surge in 2024 — speed, specialists and APIs win

Colony’s Stars—SBA/USDA lending, digital acquisition, agribusiness, owner-occupied CRE—show strong 2024 demand: SBA guarantees to 85%, median close 30–45 days, digital account openings +20% YoY and ~66% consumers online-first, Georgia ag $75B impact. Invest in speed, specialist coverage, APIs and seasonal cash tools to sustain share and future cash flow.

| Segment | 2024 KPI | Priority |

|---|---|---|

| SBA/USDA | 85% guarantee; 30–45d close | Specialists & faster underwriting |

| Digital | +20% accnt opens; 66% pref | UX, instant verification, APIs |

| Agribusiness | $75B state impact | Field teams & seasonal finance |

What is included in the product

Comprehensive BCG Matrix review of Colony Bank's units, identifying Stars, Cash Cows, Question Marks, Dogs and strategic moves.

One-page BCG matrix placing Colony Bank units into quadrants to simplify strategy and export cleanly for C-level decks

Cash Cows

Low-cost core deposits from long-time customers

Relationship checking and savings at Colony Bank are mature, sticky, and cheap to service, supplying the engine for margins and stability; industry data in 2024 showed core deposit costs under 1% versus wholesale funding north of 3%, supporting durable net interest margin. Promotion needs are light—focus on high-quality service. Optimize pricing and digital self-service to quietly boost yield and increase cross-sell conversion.

Established community CRE portfolios

Established community CRE portfolios are stabilized with ~93% occupancy and seasoned borrowers, delivering predictable cash flow and 2–3% annual NOI growth in 2024. Growth is modest, but average loan spreads remain near 250 bps and fee income is steady. Minimal marketing is required; focus on renewal discipline with ~85–90% renewal rates. Harvest fees and keep credit costs low through conservative underwriting.

Basic treasury services (ACH, wires, RDC at scale)

Basic treasury services (ACH, wires, RDC at scale) are entrenched with existing business clients, driving low churn and steady recurring revenue; the ACH network processes tens of billions of transactions annually (Nacha). Operational unit costs decline as volumes scale on existing rails, so small fee adjustments flow largely to the bottom line. Focus on reliability and uptime; avoid over-engineering features that raise fixed costs and risk service disruption.

Service charges and interchange from legacy accounts

Service charges and interchange from legacy accounts are everyday fees and card-swipe revenue: boring but dependable, driven by existing customer volumes rather than market expansion. Light-touch, compliance-aware optimization (pricing hygiene, dispute handling) yields steady margin uplift while minimizing complaints. Focus on operational efficiency and retention to preserve cash cow returns.

- Everyday fees: stable recurring income

- Card swipe: predictable interchange

- Volumes track base, not market

- Optimize lightly, prioritize compliance

- Reduce complaints, maximize efficiency

Time deposits/CDs from loyal savers

Time deposits/CDs from loyal savers are a steady, non-flashy funding source for Colony Bank when priced inside a normalized rate band, preserving margins while avoiding broad repricing; branch-led sales are simple, repeatable, and cost-efficient.

- Branch-led acquisition

- Stable margins in normal rate bands

- Use targeted specials, avoid blanket repricing

Core 1%, wholesale 3%, CRE 93% — steady margins

Core deposits <1% vs wholesale >3% (2024), CRE 93% occ., NOI +2–3% (2024), avg loan spread ~250bps, renewals 85–90%, ACH tens of billions txns — low promo, high retention, steady margins.

| Metric | 2024 |

|---|---|

| Core deposit cost | <1% |

| Wholesale funding | >3% |

| CRE occupancy | 93% |

| NOI growth | 2–3% |

| Loan spread | ~250bps |

| Renewal rate | 85–90% |

| ACH volume | tens of billions |

Preview = Final Product

Colony Bank BCG Matrix

The file you're previewing is the exact Colony Bank BCG Matrix you'll receive after purchase. No watermarks, no placeholders—just the fully formatted, ready-to-use report. It’s editable, printable, and designed by strategy pros for immediate presentation. Buy once and download instantly—no surprises, no extra steps.

Original: $10.00

-65%$10.00

$3.50Description

See the Bigger Picture

Curious where Colony Bank’s products land—Stars, Cash Cows, Dogs, or Question Marks? This snapshot hints at strengths and blindspots, but the full BCG Matrix gives quadrant-level placements, data-backed recommendations, and a clear playbook for where to invest or divest. Purchase the complete report for a Word + Excel pack that lets you present and act on strategy—fast, practical, and made for busy leaders.

Stars

SBA/USDA-backed small business lending

Government-guaranteed SBA (up to 85% guarantee) and USDA lending fits Georgia’s growing SMB market and Colony’s community ties give it a distribution edge. Demand and pipelines are strong, but underwriting and servicing tie up working capital and can slow median close times to roughly 30–45 days. Keep investing in brand, speed-to-close, and specialist bankers. Sustain share now and it will generate substantial cash flow later.

Commercial & treasury management for growth businesses

Middle-market clients demand payments, liquidity, and fraud tools urgently; 2024 adoption surged roughly 40% year-over-year as faster payments and API-led solutions become table stakes.

Colony can lead locally by combining responsive service and bundled pricing, capturing higher fee yield and reducing churn through tailored suites and relationship coverage.

Implementation is resource-intensive—invest in onboarding, APIs, and dedicated coverage teams now to realize retention gains and incremental fee revenue that offset setup costs.

Digital account opening and mobile banking

Digital account opening and mobile banking drive top-of-funnel acquisition for Colony Bank, meeting the 2024 trend of digital-first preferences where roughly two-thirds of US consumers favor online-first banking and digital account openings grew ~20% YoY. Strong usage growth and cross-sell convert those new customers into lower-cost deposit balances, improving share capture despite heavy tech spend. Continued UX iteration and instant verification cut dropout rates and shorten time-to-deposit, increasing lifetime value per acquired customer.

Owner-occupied CRE and professional practice lending

Owner-occupied CRE for physicians, dentists and accountants is a stable, expanding niche as practices borrow for space and equipment; Colony’s local underwriting and same-day decisioning can dominate referrals and lead capture in 2024. It requires tight credit discipline, active portfolio monitoring, and tailored terms to retain profitability and control concentration risk.

- Focus: professional practices

- Advantage: local underwriting & speed

- Requirement: strict credit & monitoring

- Strategy: tailored terms + referral ecosystem

Agribusiness banking in expanding counties

Agribusiness banking in expanding counties is a Star for Colony: Georgia agriculture drives a $75B state economic impact (UGA 2024) and is modernizing, increasing demand for working capital and equipment finance; Colony’s footprint can capture share but requires field expertise and seasonal cash management, so double down on specialists and data-driven risk tools.

- Focus: working capital & equipment

- Capability: seasonal cash mgmt + field teams

- Tooling: data-driven risk models

SBA/USDA, digital and ag demand surge in 2024 — speed, specialists and APIs win

Colony’s Stars—SBA/USDA lending, digital acquisition, agribusiness, owner-occupied CRE—show strong 2024 demand: SBA guarantees to 85%, median close 30–45 days, digital account openings +20% YoY and ~66% consumers online-first, Georgia ag $75B impact. Invest in speed, specialist coverage, APIs and seasonal cash tools to sustain share and future cash flow.

| Segment | 2024 KPI | Priority |

|---|---|---|

| SBA/USDA | 85% guarantee; 30–45d close | Specialists & faster underwriting |

| Digital | +20% accnt opens; 66% pref | UX, instant verification, APIs |

| Agribusiness | $75B state impact | Field teams & seasonal finance |

What is included in the product

Comprehensive BCG Matrix review of Colony Bank's units, identifying Stars, Cash Cows, Question Marks, Dogs and strategic moves.

One-page BCG matrix placing Colony Bank units into quadrants to simplify strategy and export cleanly for C-level decks

Cash Cows

Low-cost core deposits from long-time customers

Relationship checking and savings at Colony Bank are mature, sticky, and cheap to service, supplying the engine for margins and stability; industry data in 2024 showed core deposit costs under 1% versus wholesale funding north of 3%, supporting durable net interest margin. Promotion needs are light—focus on high-quality service. Optimize pricing and digital self-service to quietly boost yield and increase cross-sell conversion.

Established community CRE portfolios

Established community CRE portfolios are stabilized with ~93% occupancy and seasoned borrowers, delivering predictable cash flow and 2–3% annual NOI growth in 2024. Growth is modest, but average loan spreads remain near 250 bps and fee income is steady. Minimal marketing is required; focus on renewal discipline with ~85–90% renewal rates. Harvest fees and keep credit costs low through conservative underwriting.

Basic treasury services (ACH, wires, RDC at scale)

Basic treasury services (ACH, wires, RDC at scale) are entrenched with existing business clients, driving low churn and steady recurring revenue; the ACH network processes tens of billions of transactions annually (Nacha). Operational unit costs decline as volumes scale on existing rails, so small fee adjustments flow largely to the bottom line. Focus on reliability and uptime; avoid over-engineering features that raise fixed costs and risk service disruption.

Service charges and interchange from legacy accounts

Service charges and interchange from legacy accounts are everyday fees and card-swipe revenue: boring but dependable, driven by existing customer volumes rather than market expansion. Light-touch, compliance-aware optimization (pricing hygiene, dispute handling) yields steady margin uplift while minimizing complaints. Focus on operational efficiency and retention to preserve cash cow returns.

- Everyday fees: stable recurring income

- Card swipe: predictable interchange

- Volumes track base, not market

- Optimize lightly, prioritize compliance

- Reduce complaints, maximize efficiency

Time deposits/CDs from loyal savers

Time deposits/CDs from loyal savers are a steady, non-flashy funding source for Colony Bank when priced inside a normalized rate band, preserving margins while avoiding broad repricing; branch-led sales are simple, repeatable, and cost-efficient.

- Branch-led acquisition

- Stable margins in normal rate bands

- Use targeted specials, avoid blanket repricing

Core 1%, wholesale 3%, CRE 93% — steady margins

Core deposits <1% vs wholesale >3% (2024), CRE 93% occ., NOI +2–3% (2024), avg loan spread ~250bps, renewals 85–90%, ACH tens of billions txns — low promo, high retention, steady margins.

| Metric | 2024 |

|---|---|

| Core deposit cost | <1% |

| Wholesale funding | >3% |

| CRE occupancy | 93% |

| NOI growth | 2–3% |

| Loan spread | ~250bps |

| Renewal rate | 85–90% |

| ACH volume | tens of billions |

Preview = Final Product

Colony Bank BCG Matrix

The file you're previewing is the exact Colony Bank BCG Matrix you'll receive after purchase. No watermarks, no placeholders—just the fully formatted, ready-to-use report. It’s editable, printable, and designed by strategy pros for immediate presentation. Buy once and download instantly—no surprises, no extra steps.