Colony Bank PESTLE Analysis

Your Shortcut to Market Insight Starts Here

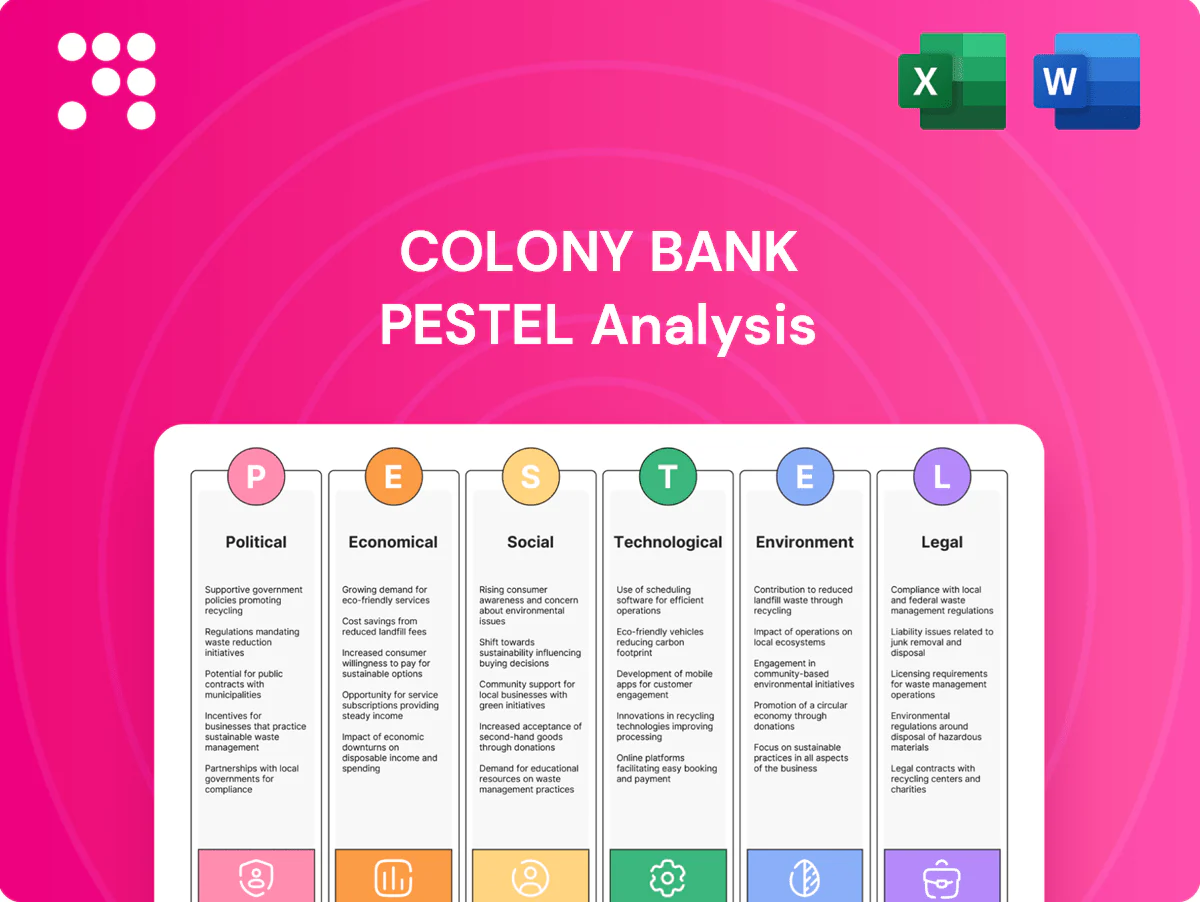

Gain strategic clarity with our PESTLE Analysis of Colony Bank—three to five expert-level insights into political, economic, social, technological, legal, and environmental forces shaping its future. Ideal for investors and strategists, this report is fully researched and actionable. Purchase the full analysis to download the complete, editable briefing and make confident decisions.

Political factors

State-level banking policy in Georgia

Georgia’s pro-business legislative stance, in a state of about 10.9 million residents (2024), lowers regulatory friction for Colony Bank, reducing branching and small-business lending barriers and affecting operating costs and expansion flexibility. Changes in state leadership can redirect grant funding or regulatory focus, so tracking bills on fintech partnerships and consumer protection is essential.

Federal banking oversight dynamics

Changes at the Federal Reserve, FDIC, OCC and CFPB have tightened examinations and capital expectations since the 2023–24 regional bank stress, with the federal funds rate holding at about 5.25–5.50% through 2024–mid‑2025. Leadership shifts have refocused scrutiny on consumer complaints, overdraft fees and fair lending. A firmer supervisory posture raises compliance costs and staffing needs, while regulatory stability enables multi‑year product rollout planning.

Community development priorities

Political emphasis on rural development and small-business support can unlock public-private lending programs that benefit banks serving underserved areas; the U.S. had about 33.2 million small businesses in 2022, underscoring market scale. Local officials may offer tax or grant incentives for branch presence in underserved counties, boosting deposit growth. Alignment with municipal projects can deepen relationships and deposits, but policy shifts could reallocate funding away from target communities.

Infrastructure and public investment

The Bipartisan Infrastructure Law commits roughly 550 billion dollars in new federal investment, boosting local construction activity and loan demand; bank involvement in public projects deepens treasury and cash-management revenues. Project delays or appropriations cuts shrink pipeline visibility, while active coordination with contractors and municipalities helps capture deposit flows and fee income.

- Fiscal tag: $550B new federal infrastructure

- Opportunity: increased loan & treasury fees

- Risk: delays cut pipeline visibility

- Strategy: partner with contractors/municipalities to win deposits

Disaster response funding

Political commitment to disaster relief in the Southeast shapes Colony Bank’s loan forbearance scope and recovery timelines, affecting charge-off timing and provisioning. Federal disaster declarations unlock SBA low-interest loans and FEMA assistance, bolstering borrower resilience and collateral recovery. Swift local response stabilizes deposits and credit quality, while gaps in funding prolong nonperforming loans in affected counties.

- Loan forbearance scope

- SBA/FEMA aid access

- Deposit stability

- Prolonged NPLs in funding gaps

Georgia pro-business lifts bank lending; $550B, rates ~5.25–5.50%

Georgia’s pro-business policy (pop. 10.9M in 2024) eases expansion for Colony Bank; federal supervision tightened after 2023–24 regional stress, with the fed funds rate ~5.25–5.50% through mid‑2025 raising compliance costs. Federal infrastructure ($550B) and 33.2M US small businesses create loan and treasury opportunities; disaster relief policy shapes forbearance and NPL timelines.

| Indicator | Value |

|---|---|

| Georgia population (2024) | 10.9M |

| Fed funds rate (2024–mid‑2025) | 5.25–5.50% |

| US small businesses (2022) | 33.2M |

| Bipartisan Infrastructure | $550B |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact Colony Bank, with data-backed trends, region-specific examples and forward-looking insights to help executives, consultants and investors identify risks, opportunities and strategic responses.

A compact, visually segmented PESTLE summary for Colony Bank that simplifies external risk assessment, can be dropped into presentations or annotated for local branches, and is easily shared across teams to speed planning and alignment.

Economic factors

Interest rate cycle sensitivity

Colony Bank's net interest margin is highly sensitive to Federal Reserve policy and the yield curve; US bank NIM averaged about 3.0% in 2024 while the fed funds rate was roughly 5.25–5.50% in 2024. Rising rates can widen margins but elevate credit risk and push deposit betas higher, stressing funding cost. Falling rates compress margins yet boost refinancing activity and fee income. Balance sheet positioning and interest-rate hedging are therefore critical.

Georgia’s regional growth trends

Georgia's population (10.71 million per 2020 Census) and metro growth—metro Atlanta had about 6.09 million residents in 2020—drive deposits and loan demand concentrated in urban corridors; rural counties (Georgia has 159 counties) often see slower growth and higher credit risk. Targeted outreach and branch/relationship expansion can rebalance portfolio geography. Local industry mix—fintech, logistics, film, manufacturing—creates concentration risk in metro centers.

Small-business and agricultural health

Community banks like Colony depend heavily on SMB and agricultural cycles for C&I and CRE lending, providing roughly half of small-business loans nationally and concentrating credit risk in local farm and main-street cash flows in 2024. Commodity price swings, elevated labor costs and ongoing supply‑chain frictions continue to squeeze borrower liquidity and repayment capacity. Diversifying across sectors and expanding advisory and treasury services (payments, cash management) deepens relationships and spreads portfolio risk.

Labor market and wage pressures

Tight labor markets raise operating expenses for branches and technology teams; U.S. unemployment was 3.7% in Dec 2024 and average hourly earnings rose about 4.1% YoY (BLS, Dec 2024). Higher wages can improve consumer deposit inflows as household incomes increase. Productivity tools can offset cost inflation, and staffing flexibility supports service levels across dispersed locations.

- Tight labor: unemployment 3.7% (Dec 2024, BLS)

- Wage growth: +4.1% YoY (Dec 2024, BLS)

- Productivity tech offsets costs

- Flexible staffing sustains service

Credit quality and CRE exposure

Office valuations (US office vacancy ~17% in 2024, CBRE) and retail trends (national retail vacancy ~5% in 2024, CBRE) directly affect Colony Bank collateral values and provisioning needs; stressed property types drive higher loss emergence and have contributed to elevated CRE-related noncurrent rates (about 1.3% at FDIC-insured institutions in 2024).

Prudent underwriting, tighter surveillance and conservative LTVs reduce realized losses, while subdued CMBS/secondary market activity in 2024 compressed liquidity options for CRE lenders.

- Office vacancy ~17% (CBRE, 2024)

- Retail vacancy ~5% (CBRE, 2024)

- CRE noncurrent ~1.3% (FDIC-insured, 2024)

Georgia pro-business lifts bank lending; $550B, rates ~5.25–5.50%

Colony Bank margins remain highly rate‑sensitive: US bank NIM ~3.0% (2024) vs fed funds ~5.25–5.50% (2024), so rate moves affect funding costs and credit risk. Georgia demographics (pop 10.71M; metro Atlanta ~6.09M in 2020) drive deposit/loan concentration. Tight labor (unemp 3.7%, wages +4.1% YoY, Dec 2024) and CRE stress (office vacancy ~17%, CRE noncurrent ~1.3%, 2024) shape costs and provisioning.

| Metric | Value |

|---|---|

| US bank NIM (2024) | ~3.0% |

| Fed funds (2024) | 5.25–5.50% |

| GA pop / ATL (2020) | 10.71M / 6.09M |

| Unemp / wage (Dec 2024) | 3.7% / +4.1% |

| Office vac / CRE noncurrent (2024) | ~17% / ~1.3% |

Full Version Awaits

Colony Bank PESTLE Analysis

The preview of the Colony Bank PESTLE Analysis is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. What you see here reflects the final layout, content, and structure with no placeholders or surprises. After checkout you’ll instantly download this same finished file.

Your Shortcut to Market Insight Starts Here

Gain strategic clarity with our PESTLE Analysis of Colony Bank—three to five expert-level insights into political, economic, social, technological, legal, and environmental forces shaping its future. Ideal for investors and strategists, this report is fully researched and actionable. Purchase the full analysis to download the complete, editable briefing and make confident decisions.

Political factors

State-level banking policy in Georgia

Georgia’s pro-business legislative stance, in a state of about 10.9 million residents (2024), lowers regulatory friction for Colony Bank, reducing branching and small-business lending barriers and affecting operating costs and expansion flexibility. Changes in state leadership can redirect grant funding or regulatory focus, so tracking bills on fintech partnerships and consumer protection is essential.

Federal banking oversight dynamics

Changes at the Federal Reserve, FDIC, OCC and CFPB have tightened examinations and capital expectations since the 2023–24 regional bank stress, with the federal funds rate holding at about 5.25–5.50% through 2024–mid‑2025. Leadership shifts have refocused scrutiny on consumer complaints, overdraft fees and fair lending. A firmer supervisory posture raises compliance costs and staffing needs, while regulatory stability enables multi‑year product rollout planning.

Community development priorities

Political emphasis on rural development and small-business support can unlock public-private lending programs that benefit banks serving underserved areas; the U.S. had about 33.2 million small businesses in 2022, underscoring market scale. Local officials may offer tax or grant incentives for branch presence in underserved counties, boosting deposit growth. Alignment with municipal projects can deepen relationships and deposits, but policy shifts could reallocate funding away from target communities.

Infrastructure and public investment

The Bipartisan Infrastructure Law commits roughly 550 billion dollars in new federal investment, boosting local construction activity and loan demand; bank involvement in public projects deepens treasury and cash-management revenues. Project delays or appropriations cuts shrink pipeline visibility, while active coordination with contractors and municipalities helps capture deposit flows and fee income.

- Fiscal tag: $550B new federal infrastructure

- Opportunity: increased loan & treasury fees

- Risk: delays cut pipeline visibility

- Strategy: partner with contractors/municipalities to win deposits

Disaster response funding

Political commitment to disaster relief in the Southeast shapes Colony Bank’s loan forbearance scope and recovery timelines, affecting charge-off timing and provisioning. Federal disaster declarations unlock SBA low-interest loans and FEMA assistance, bolstering borrower resilience and collateral recovery. Swift local response stabilizes deposits and credit quality, while gaps in funding prolong nonperforming loans in affected counties.

- Loan forbearance scope

- SBA/FEMA aid access

- Deposit stability

- Prolonged NPLs in funding gaps

Georgia pro-business lifts bank lending; $550B, rates ~5.25–5.50%

Georgia’s pro-business policy (pop. 10.9M in 2024) eases expansion for Colony Bank; federal supervision tightened after 2023–24 regional stress, with the fed funds rate ~5.25–5.50% through mid‑2025 raising compliance costs. Federal infrastructure ($550B) and 33.2M US small businesses create loan and treasury opportunities; disaster relief policy shapes forbearance and NPL timelines.

| Indicator | Value |

|---|---|

| Georgia population (2024) | 10.9M |

| Fed funds rate (2024–mid‑2025) | 5.25–5.50% |

| US small businesses (2022) | 33.2M |

| Bipartisan Infrastructure | $550B |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact Colony Bank, with data-backed trends, region-specific examples and forward-looking insights to help executives, consultants and investors identify risks, opportunities and strategic responses.

A compact, visually segmented PESTLE summary for Colony Bank that simplifies external risk assessment, can be dropped into presentations or annotated for local branches, and is easily shared across teams to speed planning and alignment.

Economic factors

Interest rate cycle sensitivity

Colony Bank's net interest margin is highly sensitive to Federal Reserve policy and the yield curve; US bank NIM averaged about 3.0% in 2024 while the fed funds rate was roughly 5.25–5.50% in 2024. Rising rates can widen margins but elevate credit risk and push deposit betas higher, stressing funding cost. Falling rates compress margins yet boost refinancing activity and fee income. Balance sheet positioning and interest-rate hedging are therefore critical.

Georgia’s regional growth trends

Georgia's population (10.71 million per 2020 Census) and metro growth—metro Atlanta had about 6.09 million residents in 2020—drive deposits and loan demand concentrated in urban corridors; rural counties (Georgia has 159 counties) often see slower growth and higher credit risk. Targeted outreach and branch/relationship expansion can rebalance portfolio geography. Local industry mix—fintech, logistics, film, manufacturing—creates concentration risk in metro centers.

Small-business and agricultural health

Community banks like Colony depend heavily on SMB and agricultural cycles for C&I and CRE lending, providing roughly half of small-business loans nationally and concentrating credit risk in local farm and main-street cash flows in 2024. Commodity price swings, elevated labor costs and ongoing supply‑chain frictions continue to squeeze borrower liquidity and repayment capacity. Diversifying across sectors and expanding advisory and treasury services (payments, cash management) deepens relationships and spreads portfolio risk.

Labor market and wage pressures

Tight labor markets raise operating expenses for branches and technology teams; U.S. unemployment was 3.7% in Dec 2024 and average hourly earnings rose about 4.1% YoY (BLS, Dec 2024). Higher wages can improve consumer deposit inflows as household incomes increase. Productivity tools can offset cost inflation, and staffing flexibility supports service levels across dispersed locations.

- Tight labor: unemployment 3.7% (Dec 2024, BLS)

- Wage growth: +4.1% YoY (Dec 2024, BLS)

- Productivity tech offsets costs

- Flexible staffing sustains service

Credit quality and CRE exposure

Office valuations (US office vacancy ~17% in 2024, CBRE) and retail trends (national retail vacancy ~5% in 2024, CBRE) directly affect Colony Bank collateral values and provisioning needs; stressed property types drive higher loss emergence and have contributed to elevated CRE-related noncurrent rates (about 1.3% at FDIC-insured institutions in 2024).

Prudent underwriting, tighter surveillance and conservative LTVs reduce realized losses, while subdued CMBS/secondary market activity in 2024 compressed liquidity options for CRE lenders.

- Office vacancy ~17% (CBRE, 2024)

- Retail vacancy ~5% (CBRE, 2024)

- CRE noncurrent ~1.3% (FDIC-insured, 2024)

Georgia pro-business lifts bank lending; $550B, rates ~5.25–5.50%

Colony Bank margins remain highly rate‑sensitive: US bank NIM ~3.0% (2024) vs fed funds ~5.25–5.50% (2024), so rate moves affect funding costs and credit risk. Georgia demographics (pop 10.71M; metro Atlanta ~6.09M in 2020) drive deposit/loan concentration. Tight labor (unemp 3.7%, wages +4.1% YoY, Dec 2024) and CRE stress (office vacancy ~17%, CRE noncurrent ~1.3%, 2024) shape costs and provisioning.

| Metric | Value |

|---|---|

| US bank NIM (2024) | ~3.0% |

| Fed funds (2024) | 5.25–5.50% |

| GA pop / ATL (2020) | 10.71M / 6.09M |

| Unemp / wage (Dec 2024) | 3.7% / +4.1% |

| Office vac / CRE noncurrent (2024) | ~17% / ~1.3% |

Full Version Awaits

Colony Bank PESTLE Analysis

The preview of the Colony Bank PESTLE Analysis is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. What you see here reflects the final layout, content, and structure with no placeholders or surprises. After checkout you’ll instantly download this same finished file.

Description

Your Shortcut to Market Insight Starts Here

Gain strategic clarity with our PESTLE Analysis of Colony Bank—three to five expert-level insights into political, economic, social, technological, legal, and environmental forces shaping its future. Ideal for investors and strategists, this report is fully researched and actionable. Purchase the full analysis to download the complete, editable briefing and make confident decisions.

Political factors

State-level banking policy in Georgia

Georgia’s pro-business legislative stance, in a state of about 10.9 million residents (2024), lowers regulatory friction for Colony Bank, reducing branching and small-business lending barriers and affecting operating costs and expansion flexibility. Changes in state leadership can redirect grant funding or regulatory focus, so tracking bills on fintech partnerships and consumer protection is essential.

Federal banking oversight dynamics

Changes at the Federal Reserve, FDIC, OCC and CFPB have tightened examinations and capital expectations since the 2023–24 regional bank stress, with the federal funds rate holding at about 5.25–5.50% through 2024–mid‑2025. Leadership shifts have refocused scrutiny on consumer complaints, overdraft fees and fair lending. A firmer supervisory posture raises compliance costs and staffing needs, while regulatory stability enables multi‑year product rollout planning.

Community development priorities

Political emphasis on rural development and small-business support can unlock public-private lending programs that benefit banks serving underserved areas; the U.S. had about 33.2 million small businesses in 2022, underscoring market scale. Local officials may offer tax or grant incentives for branch presence in underserved counties, boosting deposit growth. Alignment with municipal projects can deepen relationships and deposits, but policy shifts could reallocate funding away from target communities.

Infrastructure and public investment

The Bipartisan Infrastructure Law commits roughly 550 billion dollars in new federal investment, boosting local construction activity and loan demand; bank involvement in public projects deepens treasury and cash-management revenues. Project delays or appropriations cuts shrink pipeline visibility, while active coordination with contractors and municipalities helps capture deposit flows and fee income.

- Fiscal tag: $550B new federal infrastructure

- Opportunity: increased loan & treasury fees

- Risk: delays cut pipeline visibility

- Strategy: partner with contractors/municipalities to win deposits

Disaster response funding

Political commitment to disaster relief in the Southeast shapes Colony Bank’s loan forbearance scope and recovery timelines, affecting charge-off timing and provisioning. Federal disaster declarations unlock SBA low-interest loans and FEMA assistance, bolstering borrower resilience and collateral recovery. Swift local response stabilizes deposits and credit quality, while gaps in funding prolong nonperforming loans in affected counties.

- Loan forbearance scope

- SBA/FEMA aid access

- Deposit stability

- Prolonged NPLs in funding gaps

Georgia pro-business lifts bank lending; $550B, rates ~5.25–5.50%

Georgia’s pro-business policy (pop. 10.9M in 2024) eases expansion for Colony Bank; federal supervision tightened after 2023–24 regional stress, with the fed funds rate ~5.25–5.50% through mid‑2025 raising compliance costs. Federal infrastructure ($550B) and 33.2M US small businesses create loan and treasury opportunities; disaster relief policy shapes forbearance and NPL timelines.

| Indicator | Value |

|---|---|

| Georgia population (2024) | 10.9M |

| Fed funds rate (2024–mid‑2025) | 5.25–5.50% |

| US small businesses (2022) | 33.2M |

| Bipartisan Infrastructure | $550B |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact Colony Bank, with data-backed trends, region-specific examples and forward-looking insights to help executives, consultants and investors identify risks, opportunities and strategic responses.

A compact, visually segmented PESTLE summary for Colony Bank that simplifies external risk assessment, can be dropped into presentations or annotated for local branches, and is easily shared across teams to speed planning and alignment.

Economic factors

Interest rate cycle sensitivity

Colony Bank's net interest margin is highly sensitive to Federal Reserve policy and the yield curve; US bank NIM averaged about 3.0% in 2024 while the fed funds rate was roughly 5.25–5.50% in 2024. Rising rates can widen margins but elevate credit risk and push deposit betas higher, stressing funding cost. Falling rates compress margins yet boost refinancing activity and fee income. Balance sheet positioning and interest-rate hedging are therefore critical.

Georgia’s regional growth trends

Georgia's population (10.71 million per 2020 Census) and metro growth—metro Atlanta had about 6.09 million residents in 2020—drive deposits and loan demand concentrated in urban corridors; rural counties (Georgia has 159 counties) often see slower growth and higher credit risk. Targeted outreach and branch/relationship expansion can rebalance portfolio geography. Local industry mix—fintech, logistics, film, manufacturing—creates concentration risk in metro centers.

Small-business and agricultural health

Community banks like Colony depend heavily on SMB and agricultural cycles for C&I and CRE lending, providing roughly half of small-business loans nationally and concentrating credit risk in local farm and main-street cash flows in 2024. Commodity price swings, elevated labor costs and ongoing supply‑chain frictions continue to squeeze borrower liquidity and repayment capacity. Diversifying across sectors and expanding advisory and treasury services (payments, cash management) deepens relationships and spreads portfolio risk.

Labor market and wage pressures

Tight labor markets raise operating expenses for branches and technology teams; U.S. unemployment was 3.7% in Dec 2024 and average hourly earnings rose about 4.1% YoY (BLS, Dec 2024). Higher wages can improve consumer deposit inflows as household incomes increase. Productivity tools can offset cost inflation, and staffing flexibility supports service levels across dispersed locations.

- Tight labor: unemployment 3.7% (Dec 2024, BLS)

- Wage growth: +4.1% YoY (Dec 2024, BLS)

- Productivity tech offsets costs

- Flexible staffing sustains service

Credit quality and CRE exposure

Office valuations (US office vacancy ~17% in 2024, CBRE) and retail trends (national retail vacancy ~5% in 2024, CBRE) directly affect Colony Bank collateral values and provisioning needs; stressed property types drive higher loss emergence and have contributed to elevated CRE-related noncurrent rates (about 1.3% at FDIC-insured institutions in 2024).

Prudent underwriting, tighter surveillance and conservative LTVs reduce realized losses, while subdued CMBS/secondary market activity in 2024 compressed liquidity options for CRE lenders.

- Office vacancy ~17% (CBRE, 2024)

- Retail vacancy ~5% (CBRE, 2024)

- CRE noncurrent ~1.3% (FDIC-insured, 2024)

Georgia pro-business lifts bank lending; $550B, rates ~5.25–5.50%

Colony Bank margins remain highly rate‑sensitive: US bank NIM ~3.0% (2024) vs fed funds ~5.25–5.50% (2024), so rate moves affect funding costs and credit risk. Georgia demographics (pop 10.71M; metro Atlanta ~6.09M in 2020) drive deposit/loan concentration. Tight labor (unemp 3.7%, wages +4.1% YoY, Dec 2024) and CRE stress (office vacancy ~17%, CRE noncurrent ~1.3%, 2024) shape costs and provisioning.

| Metric | Value |

|---|---|

| US bank NIM (2024) | ~3.0% |

| Fed funds (2024) | 5.25–5.50% |

| GA pop / ATL (2020) | 10.71M / 6.09M |

| Unemp / wage (Dec 2024) | 3.7% / +4.1% |

| Office vac / CRE noncurrent (2024) | ~17% / ~1.3% |

Full Version Awaits

Colony Bank PESTLE Analysis

The preview of the Colony Bank PESTLE Analysis is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. What you see here reflects the final layout, content, and structure with no placeholders or surprises. After checkout you’ll instantly download this same finished file.