Columbia Bank Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

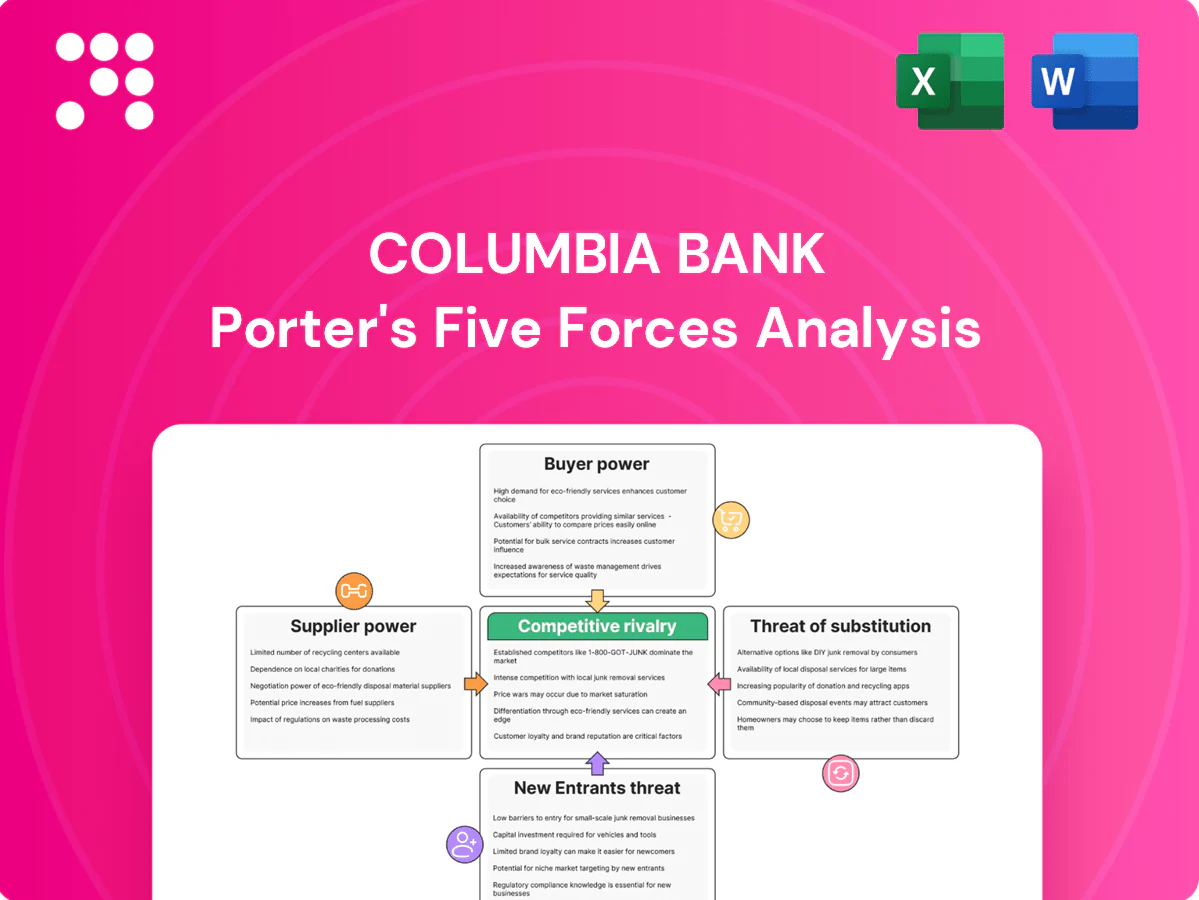

Columbia Bank’s Porter’s Five Forces snapshot highlights lender rivalry, evolving borrower bargaining power, regulatory constraints, fintech substitutes, and modest entrant threats. The analysis surfaces key pressures shaping margins and growth prospects. Unlock the full Porter’s Five Forces Analysis to explore these forces, ratings, visuals, and actionable strategy recommendations.

Suppliers Bargaining Power

Concentrated core IT vendors

Core processing, digital banking, and payments are dominated by a few suppliers (FIS, Fiserv, Jack Henry), raising switching costs and vendor leverage. Implementation cycles typically run 12–36 months with integration risks, giving suppliers pricing power. Vendor lock-in can compress service agility and margins; contracts commonly span 5–10 years, so Columbia must secure multi-year terms and strict performance SLAs.

Wholesale funding counterparties

Wholesale funding counterparties—brokered deposits, FHLB advances and capital markets investors—can reprice rapidly; FHLB advances totaled about $1.2 trillion in 2024, illustrating scale and repricing risk. In tighter liquidity cycles spreads widened and covenants strengthened, raising supplier power and costs. Dependence rises if core deposits lag growth. Diversifying funding and holding strong liquidity buffers reduces exposure.

Payment networks and processors

Card networks and merchant acquirers set interchange and network assessments with limited negotiation room; merchant fees in 2024 typically ranged between 1 and 3% of transaction value, pressuring noninterest income for regional banks. Columbia’s scale gives some offset versus smaller peers but remains well below mega-bank processing parity. Optimizing product mix, boosting card volumes, and deploying advanced fraud tools help manage net economics.

Talent and compliance expertise

- Labor scarcity: regional talent tight

- 2024: wage growth above pre‑pandemic levels

- Remote work: broader competition

- Retention: culture & career paths reduce turnover

Data, cloud, and cybersecurity vendors

Specialized data feeds, cloud platforms and security tools are mission-critical for Columbia Bank, with hyperscaler 2024 market shares roughly AWS 32%, Azure 23%, GCP 11%, and enterprise security breaches averaging multimillion-dollar impacts; certification, 99.99%+ uptime SLAs and regulatory compliance narrow switching options and raise vendor leverage. Pricing remains sticky and largely usage-based, while multi-vendor and rigorous vendor risk management reduce but do not eliminate supplier power.

Core processors boost switch costs; FHLB advances $1.2T raise repricing risk

Core processors (FIS/Fiserv/Jack Henry) raise switching costs and pricing power; contracts often 5–10 yrs. FHLB advances ~$1.2T in 2024 highlight funding repricing risk if deposits lag. Hyperscaler shares AWS 32%/Azure 23%/GCP 11% and wage growth above pre‑pandemic levels in 2024 tighten supplier leverage.

| Supplier | 2024 stat | Impact |

|---|---|---|

| Core processors | 3 vendors | High switch cost |

| FHLB/funding | $1.2T | Repricing risk |

| Hyperscalers | AWS32/AZ23/GCP11 | Vendor leverage |

What is included in the product

Comprehensive Porter's Five Forces assessment of Columbia Bank uncovering competitive pressures, customer and supplier influence, entry and substitute threats, and strategic levers to protect margins and market position.

A concise one-sheet Porter’s Five Forces for Columbia Bank—customize pressure levels, swap in your data, and export a clean spider chart ready for decks or executive decisions.

Customers Bargaining Power

Rate-sensitive depositors

Rate-sensitive depositors can shift quickly to online banks and MMFs—U.S. money market assets hit about $5.9 trillion at end-2023—pulling yields toward the fed funds effective rate (around 5.25–5.50% in 2024). Post-rate hikes deposit betas have risen, compressing community-bank NIMs and boosting promotional pricing battles that strengthen buyer power. Columbia can mitigate churn with relationship pricing and bundled services to lock balances.

Large commercial borrowers

Large commercial borrowers in the middle market (generally firms with $10M–$1B revenue) routinely bid credit to multiple banks, extracting better rates, structures, and fees. Covenant flexibility and rapid decisioning materially influence their bank choice, while cross-sell potential (treasury, FX, M&A) amplifies pricing leverage. Columbia must compete on industry expertise, tailored service, and speed to win these clients.

Low switching costs digitally

Digital account opening and payments portability lower friction to switch for Columbia Bank; 2024 data show roughly 70% of US consumers use mobile banking, accelerating onboarding and transfers. Negative service events can trigger rapid balance outflows—industry analyses in 2024 reported banks losing up to 15% of deposits after major outages. Customers expect seamless omnichannel experiences; superior UX and proactive service reduce buyer clout and stem churn.

Community relationships buffer power

Columbia Bank (NASDAQ: COLB) leverages local ties, advisory support and a dense branch presence to create relational switching costs that soften pure price competition for many households and SMBs. Community engagement and targeted outreach strengthen loyalty; niche lending and advisory solutions sustain this edge across Puget Sound customers.

- Local ties: deep community relationships

- Advisory support: personalized SME guidance

- Branch presence: convenience-driven retention

- Targeted outreach: niche product stickiness

Fee transparency expectations

- Compare-fees: 64% (2024)

- Overdraft pushback: rising

- Regulatory pressure: CFPB 2024

- Mitigation: simplified pricing, value-adds

Rate-sensitive depositors favor MMFs $5.9T; mobile banking 70% shapes loyalty

Customers wield strong price and service leverage: rate-sensitive depositors shift to MMFs (US MM assets $5.9T end-2023) as fed funds ~5.25–5.50% in 2024, 70% use mobile banking (2024), and outages can trigger up to 15% deposit loss; 64% compare fees before opening accounts (2024).

| Metric | Value |

|---|---|

| MM assets | $5.9T (end-2023) |

| Fed funds | 5.25–5.50% (2024) |

| Mobile use | 70% (2024) |

| Outage outflow | Up to 15% (2024) |

| Fee shoppers | 64% (2024) |

Preview the Actual Deliverable

Columbia Bank Porter's Five Forces Analysis

This preview shows the exact Columbia Bank Porter’s Five Forces analysis you’ll receive—no placeholders or mockups. The document is fully formatted, professionally written, and ready to download immediately after purchase. What you see here is the complete deliverable, suitable for use in presentations or decision-making.

Go Beyond the Preview—Access the Full Strategic Report

Columbia Bank’s Porter’s Five Forces snapshot highlights lender rivalry, evolving borrower bargaining power, regulatory constraints, fintech substitutes, and modest entrant threats. The analysis surfaces key pressures shaping margins and growth prospects. Unlock the full Porter’s Five Forces Analysis to explore these forces, ratings, visuals, and actionable strategy recommendations.

Suppliers Bargaining Power

Concentrated core IT vendors

Core processing, digital banking, and payments are dominated by a few suppliers (FIS, Fiserv, Jack Henry), raising switching costs and vendor leverage. Implementation cycles typically run 12–36 months with integration risks, giving suppliers pricing power. Vendor lock-in can compress service agility and margins; contracts commonly span 5–10 years, so Columbia must secure multi-year terms and strict performance SLAs.

Wholesale funding counterparties

Wholesale funding counterparties—brokered deposits, FHLB advances and capital markets investors—can reprice rapidly; FHLB advances totaled about $1.2 trillion in 2024, illustrating scale and repricing risk. In tighter liquidity cycles spreads widened and covenants strengthened, raising supplier power and costs. Dependence rises if core deposits lag growth. Diversifying funding and holding strong liquidity buffers reduces exposure.

Payment networks and processors

Card networks and merchant acquirers set interchange and network assessments with limited negotiation room; merchant fees in 2024 typically ranged between 1 and 3% of transaction value, pressuring noninterest income for regional banks. Columbia’s scale gives some offset versus smaller peers but remains well below mega-bank processing parity. Optimizing product mix, boosting card volumes, and deploying advanced fraud tools help manage net economics.

Talent and compliance expertise

- Labor scarcity: regional talent tight

- 2024: wage growth above pre‑pandemic levels

- Remote work: broader competition

- Retention: culture & career paths reduce turnover

Data, cloud, and cybersecurity vendors

Specialized data feeds, cloud platforms and security tools are mission-critical for Columbia Bank, with hyperscaler 2024 market shares roughly AWS 32%, Azure 23%, GCP 11%, and enterprise security breaches averaging multimillion-dollar impacts; certification, 99.99%+ uptime SLAs and regulatory compliance narrow switching options and raise vendor leverage. Pricing remains sticky and largely usage-based, while multi-vendor and rigorous vendor risk management reduce but do not eliminate supplier power.

Core processors boost switch costs; FHLB advances $1.2T raise repricing risk

Core processors (FIS/Fiserv/Jack Henry) raise switching costs and pricing power; contracts often 5–10 yrs. FHLB advances ~$1.2T in 2024 highlight funding repricing risk if deposits lag. Hyperscaler shares AWS 32%/Azure 23%/GCP 11% and wage growth above pre‑pandemic levels in 2024 tighten supplier leverage.

| Supplier | 2024 stat | Impact |

|---|---|---|

| Core processors | 3 vendors | High switch cost |

| FHLB/funding | $1.2T | Repricing risk |

| Hyperscalers | AWS32/AZ23/GCP11 | Vendor leverage |

What is included in the product

Comprehensive Porter's Five Forces assessment of Columbia Bank uncovering competitive pressures, customer and supplier influence, entry and substitute threats, and strategic levers to protect margins and market position.

A concise one-sheet Porter’s Five Forces for Columbia Bank—customize pressure levels, swap in your data, and export a clean spider chart ready for decks or executive decisions.

Customers Bargaining Power

Rate-sensitive depositors

Rate-sensitive depositors can shift quickly to online banks and MMFs—U.S. money market assets hit about $5.9 trillion at end-2023—pulling yields toward the fed funds effective rate (around 5.25–5.50% in 2024). Post-rate hikes deposit betas have risen, compressing community-bank NIMs and boosting promotional pricing battles that strengthen buyer power. Columbia can mitigate churn with relationship pricing and bundled services to lock balances.

Large commercial borrowers

Large commercial borrowers in the middle market (generally firms with $10M–$1B revenue) routinely bid credit to multiple banks, extracting better rates, structures, and fees. Covenant flexibility and rapid decisioning materially influence their bank choice, while cross-sell potential (treasury, FX, M&A) amplifies pricing leverage. Columbia must compete on industry expertise, tailored service, and speed to win these clients.

Low switching costs digitally

Digital account opening and payments portability lower friction to switch for Columbia Bank; 2024 data show roughly 70% of US consumers use mobile banking, accelerating onboarding and transfers. Negative service events can trigger rapid balance outflows—industry analyses in 2024 reported banks losing up to 15% of deposits after major outages. Customers expect seamless omnichannel experiences; superior UX and proactive service reduce buyer clout and stem churn.

Community relationships buffer power

Columbia Bank (NASDAQ: COLB) leverages local ties, advisory support and a dense branch presence to create relational switching costs that soften pure price competition for many households and SMBs. Community engagement and targeted outreach strengthen loyalty; niche lending and advisory solutions sustain this edge across Puget Sound customers.

- Local ties: deep community relationships

- Advisory support: personalized SME guidance

- Branch presence: convenience-driven retention

- Targeted outreach: niche product stickiness

Fee transparency expectations

- Compare-fees: 64% (2024)

- Overdraft pushback: rising

- Regulatory pressure: CFPB 2024

- Mitigation: simplified pricing, value-adds

Rate-sensitive depositors favor MMFs $5.9T; mobile banking 70% shapes loyalty

Customers wield strong price and service leverage: rate-sensitive depositors shift to MMFs (US MM assets $5.9T end-2023) as fed funds ~5.25–5.50% in 2024, 70% use mobile banking (2024), and outages can trigger up to 15% deposit loss; 64% compare fees before opening accounts (2024).

| Metric | Value |

|---|---|

| MM assets | $5.9T (end-2023) |

| Fed funds | 5.25–5.50% (2024) |

| Mobile use | 70% (2024) |

| Outage outflow | Up to 15% (2024) |

| Fee shoppers | 64% (2024) |

Preview the Actual Deliverable

Columbia Bank Porter's Five Forces Analysis

This preview shows the exact Columbia Bank Porter’s Five Forces analysis you’ll receive—no placeholders or mockups. The document is fully formatted, professionally written, and ready to download immediately after purchase. What you see here is the complete deliverable, suitable for use in presentations or decision-making.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Columbia Bank’s Porter’s Five Forces snapshot highlights lender rivalry, evolving borrower bargaining power, regulatory constraints, fintech substitutes, and modest entrant threats. The analysis surfaces key pressures shaping margins and growth prospects. Unlock the full Porter’s Five Forces Analysis to explore these forces, ratings, visuals, and actionable strategy recommendations.

Suppliers Bargaining Power

Concentrated core IT vendors

Core processing, digital banking, and payments are dominated by a few suppliers (FIS, Fiserv, Jack Henry), raising switching costs and vendor leverage. Implementation cycles typically run 12–36 months with integration risks, giving suppliers pricing power. Vendor lock-in can compress service agility and margins; contracts commonly span 5–10 years, so Columbia must secure multi-year terms and strict performance SLAs.

Wholesale funding counterparties

Wholesale funding counterparties—brokered deposits, FHLB advances and capital markets investors—can reprice rapidly; FHLB advances totaled about $1.2 trillion in 2024, illustrating scale and repricing risk. In tighter liquidity cycles spreads widened and covenants strengthened, raising supplier power and costs. Dependence rises if core deposits lag growth. Diversifying funding and holding strong liquidity buffers reduces exposure.

Payment networks and processors

Card networks and merchant acquirers set interchange and network assessments with limited negotiation room; merchant fees in 2024 typically ranged between 1 and 3% of transaction value, pressuring noninterest income for regional banks. Columbia’s scale gives some offset versus smaller peers but remains well below mega-bank processing parity. Optimizing product mix, boosting card volumes, and deploying advanced fraud tools help manage net economics.

Talent and compliance expertise

- Labor scarcity: regional talent tight

- 2024: wage growth above pre‑pandemic levels

- Remote work: broader competition

- Retention: culture & career paths reduce turnover

Data, cloud, and cybersecurity vendors

Specialized data feeds, cloud platforms and security tools are mission-critical for Columbia Bank, with hyperscaler 2024 market shares roughly AWS 32%, Azure 23%, GCP 11%, and enterprise security breaches averaging multimillion-dollar impacts; certification, 99.99%+ uptime SLAs and regulatory compliance narrow switching options and raise vendor leverage. Pricing remains sticky and largely usage-based, while multi-vendor and rigorous vendor risk management reduce but do not eliminate supplier power.

Core processors boost switch costs; FHLB advances $1.2T raise repricing risk

Core processors (FIS/Fiserv/Jack Henry) raise switching costs and pricing power; contracts often 5–10 yrs. FHLB advances ~$1.2T in 2024 highlight funding repricing risk if deposits lag. Hyperscaler shares AWS 32%/Azure 23%/GCP 11% and wage growth above pre‑pandemic levels in 2024 tighten supplier leverage.

| Supplier | 2024 stat | Impact |

|---|---|---|

| Core processors | 3 vendors | High switch cost |

| FHLB/funding | $1.2T | Repricing risk |

| Hyperscalers | AWS32/AZ23/GCP11 | Vendor leverage |

What is included in the product

Comprehensive Porter's Five Forces assessment of Columbia Bank uncovering competitive pressures, customer and supplier influence, entry and substitute threats, and strategic levers to protect margins and market position.

A concise one-sheet Porter’s Five Forces for Columbia Bank—customize pressure levels, swap in your data, and export a clean spider chart ready for decks or executive decisions.

Customers Bargaining Power

Rate-sensitive depositors

Rate-sensitive depositors can shift quickly to online banks and MMFs—U.S. money market assets hit about $5.9 trillion at end-2023—pulling yields toward the fed funds effective rate (around 5.25–5.50% in 2024). Post-rate hikes deposit betas have risen, compressing community-bank NIMs and boosting promotional pricing battles that strengthen buyer power. Columbia can mitigate churn with relationship pricing and bundled services to lock balances.

Large commercial borrowers

Large commercial borrowers in the middle market (generally firms with $10M–$1B revenue) routinely bid credit to multiple banks, extracting better rates, structures, and fees. Covenant flexibility and rapid decisioning materially influence their bank choice, while cross-sell potential (treasury, FX, M&A) amplifies pricing leverage. Columbia must compete on industry expertise, tailored service, and speed to win these clients.

Low switching costs digitally

Digital account opening and payments portability lower friction to switch for Columbia Bank; 2024 data show roughly 70% of US consumers use mobile banking, accelerating onboarding and transfers. Negative service events can trigger rapid balance outflows—industry analyses in 2024 reported banks losing up to 15% of deposits after major outages. Customers expect seamless omnichannel experiences; superior UX and proactive service reduce buyer clout and stem churn.

Community relationships buffer power

Columbia Bank (NASDAQ: COLB) leverages local ties, advisory support and a dense branch presence to create relational switching costs that soften pure price competition for many households and SMBs. Community engagement and targeted outreach strengthen loyalty; niche lending and advisory solutions sustain this edge across Puget Sound customers.

- Local ties: deep community relationships

- Advisory support: personalized SME guidance

- Branch presence: convenience-driven retention

- Targeted outreach: niche product stickiness

Fee transparency expectations

- Compare-fees: 64% (2024)

- Overdraft pushback: rising

- Regulatory pressure: CFPB 2024

- Mitigation: simplified pricing, value-adds

Rate-sensitive depositors favor MMFs $5.9T; mobile banking 70% shapes loyalty

Customers wield strong price and service leverage: rate-sensitive depositors shift to MMFs (US MM assets $5.9T end-2023) as fed funds ~5.25–5.50% in 2024, 70% use mobile banking (2024), and outages can trigger up to 15% deposit loss; 64% compare fees before opening accounts (2024).

| Metric | Value |

|---|---|

| MM assets | $5.9T (end-2023) |

| Fed funds | 5.25–5.50% (2024) |

| Mobile use | 70% (2024) |

| Outage outflow | Up to 15% (2024) |

| Fee shoppers | 64% (2024) |

Preview the Actual Deliverable

Columbia Bank Porter's Five Forces Analysis

This preview shows the exact Columbia Bank Porter’s Five Forces analysis you’ll receive—no placeholders or mockups. The document is fully formatted, professionally written, and ready to download immediately after purchase. What you see here is the complete deliverable, suitable for use in presentations or decision-making.