Columbia Bank PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

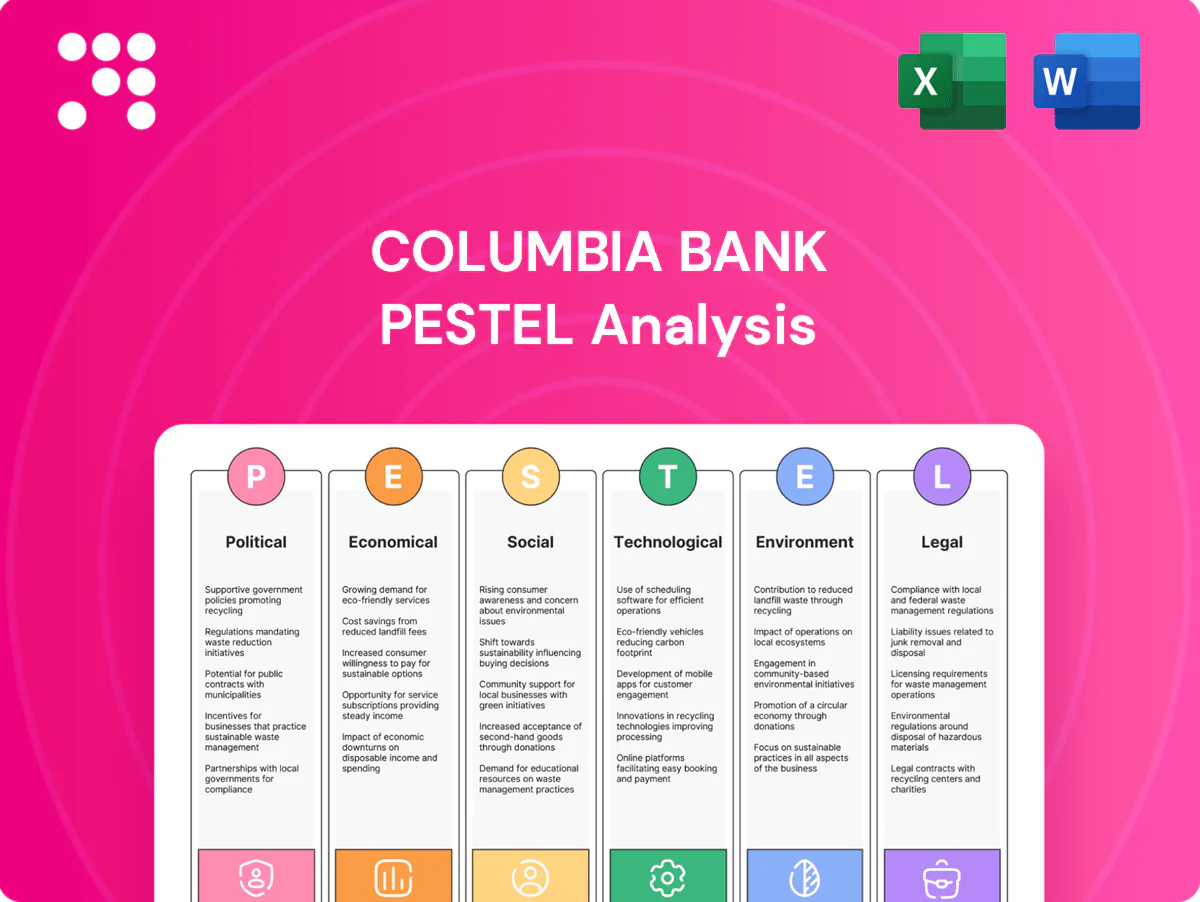

Gain a strategic edge with our PESTLE Analysis of Columbia Bank—three to five crucial external dimensions evaluated to show how politics, economy, society, technology, law, and environment shape its outlook. Use these insights to anticipate risks, spot growth levers, and refine your investment or competitive strategy. Purchase the full report for the complete, ready-to-use breakdown and downloadable templates.

Political factors

Banking regulation and supervision

Federal and state policy priorities—CET1 minimum 4.5% plus a 2.5% capital conservation buffer and a 4% leverage ratio—shape capital, liquidity and risk governance standards for regional banks. Changes in oversight intensity raise compliance costs and can limit strategic flexibility; Columbia Banking System (NASDAQ: COLB) with roughly $28 billion in assets in 2024 must anticipate supervisory themes to avoid remediation burdens. Proactive regulatory engagement supports stable operations and growth.

Community reinvestment priorities

Public policy under the Community Reinvestment Act requires banks to address local credit needs and is assessed by four possible ratings (Outstanding, Satisfactory, Needs to Improve, Unsatisfactory). CRA and interagency exam results directly influence branch strategy, product design, reputation and regulatory actions such as merger approvals. Strengthening community lending aligns with mission and reduces political scrutiny, while targeted programs address specific assessment-area needs.

Fiscal policy and public spending

Government stimulus and the Bipartisan Infrastructure Law (roughly $550bn new spending) plus rising state and local debt (> $4.5tn in 2024) shape deposits and loan demand; tax changes alter corporate investment and the US personal saving rate (~4.6% in 2024). Columbia Bank’s local footprint links results to municipal budget cycles, so scenario planning mitigates fiscal volatility.

Geopolitical and trade dynamics

Geopolitical tensions tighten financial conditions, spiking volatility (VIX averaged ~17 in 2024) and denting borrower confidence; supply-chain shifts slowed global trade to about 2.5% in 2024 (WTO), raising SME cash-flow pressure and credit demand. Columbia Bank faces indirect effects on deposit flows and credit performance; conservative liquidity buffers and hedging reduce spillover risks.

- VIX ~17 (2024)

- Global trade ~2.5% (WTO 2024)

- Higher SME credit demand, cash-flow stress

- Mitigation: liquidity buffers, hedging

Housing and small-business policy

Government-backed lending and housing incentives—with Columbia Banking System reporting roughly $21.4B in assets at year-end 2024—help sustain mortgage pipelines as public guarantees increase credit capacity and borrower affordability.

SMB programs and SBA partnerships expand C&I originations while policy shifts alter guarantee availability and underwriting appetite, requiring active portfolio calibration.

Aligning with federal and state housing programs and community partners amplifies reach and manages risk through shared guarantees and targeted credit products.

- gov-backed lending: boosts capacity via guarantees

- housing incentives: improve affordability, demand

- SMB programs: expand C&I pipelines

- partnerships: amplify community impact, mitigate risk

Regulatory capital, CRA oversight and fiscal stimulus drive regional bank strategy and loan flows

Federal/state regulatory capital (CET1 min 4.5% + 2.5% buffer; 4% leverage) and CRA oversight shape Columbia Banking System (≈$28B assets, 2024) strategy, compliance costs and branch/product choices. Fiscal stimulus and infrastructure spending (~$550B) plus 2024 VIX ~17 and US saving rate ~4.6% drive deposit and loan demand. Government-backed lending and SBA programs sustain mortgage and SMB pipelines, requiring active portfolio calibration.

| Metric | Value (2024) |

|---|---|

| Assets | $28B (approx) |

| CET1 min + buffer | 4.5% + 2.5% |

| Leverage ratio | 4% |

| VIX avg | ~17 |

| US saving rate | 4.6% |

| Infra spend | ~$550B |

What is included in the product

Explores how macro-environmental factors uniquely affect Columbia Bank across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed, region-specific trends and forward-looking insights to identify risks and opportunities; designed for executives, advisors, and investors to support strategy, scenario planning, and funding decisions.

A concise, visually segmented PESTLE summary of Columbia Bank that’s easy to edit and share—ready to drop into slides or strategy packs to support quick alignment on external risks, market positioning, and planning discussions.

Economic factors

Interest rate cycles and NIM

Fed policy drives asset yields, deposit betas and securities valuations: the federal funds target averaged 5.25–5.50% in 2023–24 and the 2‑year Treasury traded near 4.5–5.0%, compressing fair values on securities and inflating OCI volatility. Rapid rate shifts squeeze NIM as deposit betas climbed and funding costs reprice. Columbia Bank must balance repricing, hedging and funding mix; disciplined ALM sustains earnings across cycles.

Credit quality and default risk

Economic slowdowns drive higher delinquencies across CRE, C&I and consumer loans—Trepp reported CRE delinquency north of 6% in 2024—so sectoral stress can concentrate losses in hotel, retail and office portfolios. Columbia Bank requires robust underwriting, early‑warning monitoring and enhanced reserves to absorb shocks. Diversified loan mix and geographic spread moderate downturn impact and limit loss concentration.

Deposit competition and liquidity

Tight liquidity and policy rates near 5.25% in 2024–25 elevate competition for core deposits and raise wholesale funding costs, forcing banks to price more aggressively to retain balances.

High customer rate sensitivity challenges retention, but Columbia Bank's deep client relationships and expanded treasury solutions help preserve stickiness and fee income.

Stable core funding supports organic growth and cushions regulatory ratios, reducing reliance on volatile wholesale funding during rate stress.

Regional economic health

Regional economic health in Columbia Bank’s Pacific Northwest footprint—centered in Washington, Oregon and Idaho—shapes loan demand as local employment (US unemployment averaged 4.0% in 2024 per BLS) and real estate trends drive mortgage and CRE flows; SME dynamics (SMEs represent 99.9% of US firms) determine commercial lending and repayment risk. Industry mix creates cyclicality, so align lending to resilient sectors and deploy market intelligence to guide branch and product allocation.

- Local employment: 2024 U.S. avg unemployment 4.0%

- Real estate: monitor regional housing and CRE activity

- SMEs: 99.9% of U.S. firms—key loan drivers

- Strategy: target resilient sectors; use market intelligence for branches/products

Inflation and cost structure

Inflation compresses household budgets and borrower capacity while raising Columbia Bank’s operating expenses; US CPI averaged 3.4% in 2024 and the federal funds rate reached about 5.25–5.50%, elevating funding costs. Pricing discipline and efficiency gains are critical; Columbia Bank can leverage fee adjustments, mix shift toward higher-yield products, and automation to protect margins while cost control supports competitive positioning.

- US CPI 2024: 3.4%

- Fed funds peak ~5.25–5.50%

- Defend margins via fees, product mix, automation

Regulatory capital, CRA oversight and fiscal stimulus drive regional bank strategy and loan flows

Fed policy (FF 5.25–5.50% in 2024) and CPI 3.4% compressed securities values, raised funding costs and squeezed NIM; Trepp CRE delinquency >6% in 2024 heightens credit risk. Regional unemployment ~4.0% (2024) shapes loan demand; deposit competition forces pricing and ALM discipline.

| Metric | 2024 |

|---|---|

| Fed funds | 5.25–5.50% |

| CPI | 3.4% |

| CRE delinquency | >6% |

| Unemployment (US) | 4.0% |

Preview Before You Purchase

Columbia Bank PESTLE Analysis

The Columbia Bank PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This is the real, final file with no placeholders or teasers, delivered exactly as shown. After payment you’ll instantly be able to download and work with the same professionally structured document.

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a strategic edge with our PESTLE Analysis of Columbia Bank—three to five crucial external dimensions evaluated to show how politics, economy, society, technology, law, and environment shape its outlook. Use these insights to anticipate risks, spot growth levers, and refine your investment or competitive strategy. Purchase the full report for the complete, ready-to-use breakdown and downloadable templates.

Political factors

Banking regulation and supervision

Federal and state policy priorities—CET1 minimum 4.5% plus a 2.5% capital conservation buffer and a 4% leverage ratio—shape capital, liquidity and risk governance standards for regional banks. Changes in oversight intensity raise compliance costs and can limit strategic flexibility; Columbia Banking System (NASDAQ: COLB) with roughly $28 billion in assets in 2024 must anticipate supervisory themes to avoid remediation burdens. Proactive regulatory engagement supports stable operations and growth.

Community reinvestment priorities

Public policy under the Community Reinvestment Act requires banks to address local credit needs and is assessed by four possible ratings (Outstanding, Satisfactory, Needs to Improve, Unsatisfactory). CRA and interagency exam results directly influence branch strategy, product design, reputation and regulatory actions such as merger approvals. Strengthening community lending aligns with mission and reduces political scrutiny, while targeted programs address specific assessment-area needs.

Fiscal policy and public spending

Government stimulus and the Bipartisan Infrastructure Law (roughly $550bn new spending) plus rising state and local debt (> $4.5tn in 2024) shape deposits and loan demand; tax changes alter corporate investment and the US personal saving rate (~4.6% in 2024). Columbia Bank’s local footprint links results to municipal budget cycles, so scenario planning mitigates fiscal volatility.

Geopolitical and trade dynamics

Geopolitical tensions tighten financial conditions, spiking volatility (VIX averaged ~17 in 2024) and denting borrower confidence; supply-chain shifts slowed global trade to about 2.5% in 2024 (WTO), raising SME cash-flow pressure and credit demand. Columbia Bank faces indirect effects on deposit flows and credit performance; conservative liquidity buffers and hedging reduce spillover risks.

- VIX ~17 (2024)

- Global trade ~2.5% (WTO 2024)

- Higher SME credit demand, cash-flow stress

- Mitigation: liquidity buffers, hedging

Housing and small-business policy

Government-backed lending and housing incentives—with Columbia Banking System reporting roughly $21.4B in assets at year-end 2024—help sustain mortgage pipelines as public guarantees increase credit capacity and borrower affordability.

SMB programs and SBA partnerships expand C&I originations while policy shifts alter guarantee availability and underwriting appetite, requiring active portfolio calibration.

Aligning with federal and state housing programs and community partners amplifies reach and manages risk through shared guarantees and targeted credit products.

- gov-backed lending: boosts capacity via guarantees

- housing incentives: improve affordability, demand

- SMB programs: expand C&I pipelines

- partnerships: amplify community impact, mitigate risk

Regulatory capital, CRA oversight and fiscal stimulus drive regional bank strategy and loan flows

Federal/state regulatory capital (CET1 min 4.5% + 2.5% buffer; 4% leverage) and CRA oversight shape Columbia Banking System (≈$28B assets, 2024) strategy, compliance costs and branch/product choices. Fiscal stimulus and infrastructure spending (~$550B) plus 2024 VIX ~17 and US saving rate ~4.6% drive deposit and loan demand. Government-backed lending and SBA programs sustain mortgage and SMB pipelines, requiring active portfolio calibration.

| Metric | Value (2024) |

|---|---|

| Assets | $28B (approx) |

| CET1 min + buffer | 4.5% + 2.5% |

| Leverage ratio | 4% |

| VIX avg | ~17 |

| US saving rate | 4.6% |

| Infra spend | ~$550B |

What is included in the product

Explores how macro-environmental factors uniquely affect Columbia Bank across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed, region-specific trends and forward-looking insights to identify risks and opportunities; designed for executives, advisors, and investors to support strategy, scenario planning, and funding decisions.

A concise, visually segmented PESTLE summary of Columbia Bank that’s easy to edit and share—ready to drop into slides or strategy packs to support quick alignment on external risks, market positioning, and planning discussions.

Economic factors

Interest rate cycles and NIM

Fed policy drives asset yields, deposit betas and securities valuations: the federal funds target averaged 5.25–5.50% in 2023–24 and the 2‑year Treasury traded near 4.5–5.0%, compressing fair values on securities and inflating OCI volatility. Rapid rate shifts squeeze NIM as deposit betas climbed and funding costs reprice. Columbia Bank must balance repricing, hedging and funding mix; disciplined ALM sustains earnings across cycles.

Credit quality and default risk

Economic slowdowns drive higher delinquencies across CRE, C&I and consumer loans—Trepp reported CRE delinquency north of 6% in 2024—so sectoral stress can concentrate losses in hotel, retail and office portfolios. Columbia Bank requires robust underwriting, early‑warning monitoring and enhanced reserves to absorb shocks. Diversified loan mix and geographic spread moderate downturn impact and limit loss concentration.

Deposit competition and liquidity

Tight liquidity and policy rates near 5.25% in 2024–25 elevate competition for core deposits and raise wholesale funding costs, forcing banks to price more aggressively to retain balances.

High customer rate sensitivity challenges retention, but Columbia Bank's deep client relationships and expanded treasury solutions help preserve stickiness and fee income.

Stable core funding supports organic growth and cushions regulatory ratios, reducing reliance on volatile wholesale funding during rate stress.

Regional economic health

Regional economic health in Columbia Bank’s Pacific Northwest footprint—centered in Washington, Oregon and Idaho—shapes loan demand as local employment (US unemployment averaged 4.0% in 2024 per BLS) and real estate trends drive mortgage and CRE flows; SME dynamics (SMEs represent 99.9% of US firms) determine commercial lending and repayment risk. Industry mix creates cyclicality, so align lending to resilient sectors and deploy market intelligence to guide branch and product allocation.

- Local employment: 2024 U.S. avg unemployment 4.0%

- Real estate: monitor regional housing and CRE activity

- SMEs: 99.9% of U.S. firms—key loan drivers

- Strategy: target resilient sectors; use market intelligence for branches/products

Inflation and cost structure

Inflation compresses household budgets and borrower capacity while raising Columbia Bank’s operating expenses; US CPI averaged 3.4% in 2024 and the federal funds rate reached about 5.25–5.50%, elevating funding costs. Pricing discipline and efficiency gains are critical; Columbia Bank can leverage fee adjustments, mix shift toward higher-yield products, and automation to protect margins while cost control supports competitive positioning.

- US CPI 2024: 3.4%

- Fed funds peak ~5.25–5.50%

- Defend margins via fees, product mix, automation

Regulatory capital, CRA oversight and fiscal stimulus drive regional bank strategy and loan flows

Fed policy (FF 5.25–5.50% in 2024) and CPI 3.4% compressed securities values, raised funding costs and squeezed NIM; Trepp CRE delinquency >6% in 2024 heightens credit risk. Regional unemployment ~4.0% (2024) shapes loan demand; deposit competition forces pricing and ALM discipline.

| Metric | 2024 |

|---|---|

| Fed funds | 5.25–5.50% |

| CPI | 3.4% |

| CRE delinquency | >6% |

| Unemployment (US) | 4.0% |

Preview Before You Purchase

Columbia Bank PESTLE Analysis

The Columbia Bank PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This is the real, final file with no placeholders or teasers, delivered exactly as shown. After payment you’ll instantly be able to download and work with the same professionally structured document.

Original: $10.00

-65%$10.00

$3.50Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a strategic edge with our PESTLE Analysis of Columbia Bank—three to five crucial external dimensions evaluated to show how politics, economy, society, technology, law, and environment shape its outlook. Use these insights to anticipate risks, spot growth levers, and refine your investment or competitive strategy. Purchase the full report for the complete, ready-to-use breakdown and downloadable templates.

Political factors

Banking regulation and supervision

Federal and state policy priorities—CET1 minimum 4.5% plus a 2.5% capital conservation buffer and a 4% leverage ratio—shape capital, liquidity and risk governance standards for regional banks. Changes in oversight intensity raise compliance costs and can limit strategic flexibility; Columbia Banking System (NASDAQ: COLB) with roughly $28 billion in assets in 2024 must anticipate supervisory themes to avoid remediation burdens. Proactive regulatory engagement supports stable operations and growth.

Community reinvestment priorities

Public policy under the Community Reinvestment Act requires banks to address local credit needs and is assessed by four possible ratings (Outstanding, Satisfactory, Needs to Improve, Unsatisfactory). CRA and interagency exam results directly influence branch strategy, product design, reputation and regulatory actions such as merger approvals. Strengthening community lending aligns with mission and reduces political scrutiny, while targeted programs address specific assessment-area needs.

Fiscal policy and public spending

Government stimulus and the Bipartisan Infrastructure Law (roughly $550bn new spending) plus rising state and local debt (> $4.5tn in 2024) shape deposits and loan demand; tax changes alter corporate investment and the US personal saving rate (~4.6% in 2024). Columbia Bank’s local footprint links results to municipal budget cycles, so scenario planning mitigates fiscal volatility.

Geopolitical and trade dynamics

Geopolitical tensions tighten financial conditions, spiking volatility (VIX averaged ~17 in 2024) and denting borrower confidence; supply-chain shifts slowed global trade to about 2.5% in 2024 (WTO), raising SME cash-flow pressure and credit demand. Columbia Bank faces indirect effects on deposit flows and credit performance; conservative liquidity buffers and hedging reduce spillover risks.

- VIX ~17 (2024)

- Global trade ~2.5% (WTO 2024)

- Higher SME credit demand, cash-flow stress

- Mitigation: liquidity buffers, hedging

Housing and small-business policy

Government-backed lending and housing incentives—with Columbia Banking System reporting roughly $21.4B in assets at year-end 2024—help sustain mortgage pipelines as public guarantees increase credit capacity and borrower affordability.

SMB programs and SBA partnerships expand C&I originations while policy shifts alter guarantee availability and underwriting appetite, requiring active portfolio calibration.

Aligning with federal and state housing programs and community partners amplifies reach and manages risk through shared guarantees and targeted credit products.

- gov-backed lending: boosts capacity via guarantees

- housing incentives: improve affordability, demand

- SMB programs: expand C&I pipelines

- partnerships: amplify community impact, mitigate risk

Regulatory capital, CRA oversight and fiscal stimulus drive regional bank strategy and loan flows

Federal/state regulatory capital (CET1 min 4.5% + 2.5% buffer; 4% leverage) and CRA oversight shape Columbia Banking System (≈$28B assets, 2024) strategy, compliance costs and branch/product choices. Fiscal stimulus and infrastructure spending (~$550B) plus 2024 VIX ~17 and US saving rate ~4.6% drive deposit and loan demand. Government-backed lending and SBA programs sustain mortgage and SMB pipelines, requiring active portfolio calibration.

| Metric | Value (2024) |

|---|---|

| Assets | $28B (approx) |

| CET1 min + buffer | 4.5% + 2.5% |

| Leverage ratio | 4% |

| VIX avg | ~17 |

| US saving rate | 4.6% |

| Infra spend | ~$550B |

What is included in the product

Explores how macro-environmental factors uniquely affect Columbia Bank across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed, region-specific trends and forward-looking insights to identify risks and opportunities; designed for executives, advisors, and investors to support strategy, scenario planning, and funding decisions.

A concise, visually segmented PESTLE summary of Columbia Bank that’s easy to edit and share—ready to drop into slides or strategy packs to support quick alignment on external risks, market positioning, and planning discussions.

Economic factors

Interest rate cycles and NIM

Fed policy drives asset yields, deposit betas and securities valuations: the federal funds target averaged 5.25–5.50% in 2023–24 and the 2‑year Treasury traded near 4.5–5.0%, compressing fair values on securities and inflating OCI volatility. Rapid rate shifts squeeze NIM as deposit betas climbed and funding costs reprice. Columbia Bank must balance repricing, hedging and funding mix; disciplined ALM sustains earnings across cycles.

Credit quality and default risk

Economic slowdowns drive higher delinquencies across CRE, C&I and consumer loans—Trepp reported CRE delinquency north of 6% in 2024—so sectoral stress can concentrate losses in hotel, retail and office portfolios. Columbia Bank requires robust underwriting, early‑warning monitoring and enhanced reserves to absorb shocks. Diversified loan mix and geographic spread moderate downturn impact and limit loss concentration.

Deposit competition and liquidity

Tight liquidity and policy rates near 5.25% in 2024–25 elevate competition for core deposits and raise wholesale funding costs, forcing banks to price more aggressively to retain balances.

High customer rate sensitivity challenges retention, but Columbia Bank's deep client relationships and expanded treasury solutions help preserve stickiness and fee income.

Stable core funding supports organic growth and cushions regulatory ratios, reducing reliance on volatile wholesale funding during rate stress.

Regional economic health

Regional economic health in Columbia Bank’s Pacific Northwest footprint—centered in Washington, Oregon and Idaho—shapes loan demand as local employment (US unemployment averaged 4.0% in 2024 per BLS) and real estate trends drive mortgage and CRE flows; SME dynamics (SMEs represent 99.9% of US firms) determine commercial lending and repayment risk. Industry mix creates cyclicality, so align lending to resilient sectors and deploy market intelligence to guide branch and product allocation.

- Local employment: 2024 U.S. avg unemployment 4.0%

- Real estate: monitor regional housing and CRE activity

- SMEs: 99.9% of U.S. firms—key loan drivers

- Strategy: target resilient sectors; use market intelligence for branches/products

Inflation and cost structure

Inflation compresses household budgets and borrower capacity while raising Columbia Bank’s operating expenses; US CPI averaged 3.4% in 2024 and the federal funds rate reached about 5.25–5.50%, elevating funding costs. Pricing discipline and efficiency gains are critical; Columbia Bank can leverage fee adjustments, mix shift toward higher-yield products, and automation to protect margins while cost control supports competitive positioning.

- US CPI 2024: 3.4%

- Fed funds peak ~5.25–5.50%

- Defend margins via fees, product mix, automation

Regulatory capital, CRA oversight and fiscal stimulus drive regional bank strategy and loan flows

Fed policy (FF 5.25–5.50% in 2024) and CPI 3.4% compressed securities values, raised funding costs and squeezed NIM; Trepp CRE delinquency >6% in 2024 heightens credit risk. Regional unemployment ~4.0% (2024) shapes loan demand; deposit competition forces pricing and ALM discipline.

| Metric | 2024 |

|---|---|

| Fed funds | 5.25–5.50% |

| CPI | 3.4% |

| CRE delinquency | >6% |

| Unemployment (US) | 4.0% |

Preview Before You Purchase

Columbia Bank PESTLE Analysis

The Columbia Bank PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This is the real, final file with no placeholders or teasers, delivered exactly as shown. After payment you’ll instantly be able to download and work with the same professionally structured document.