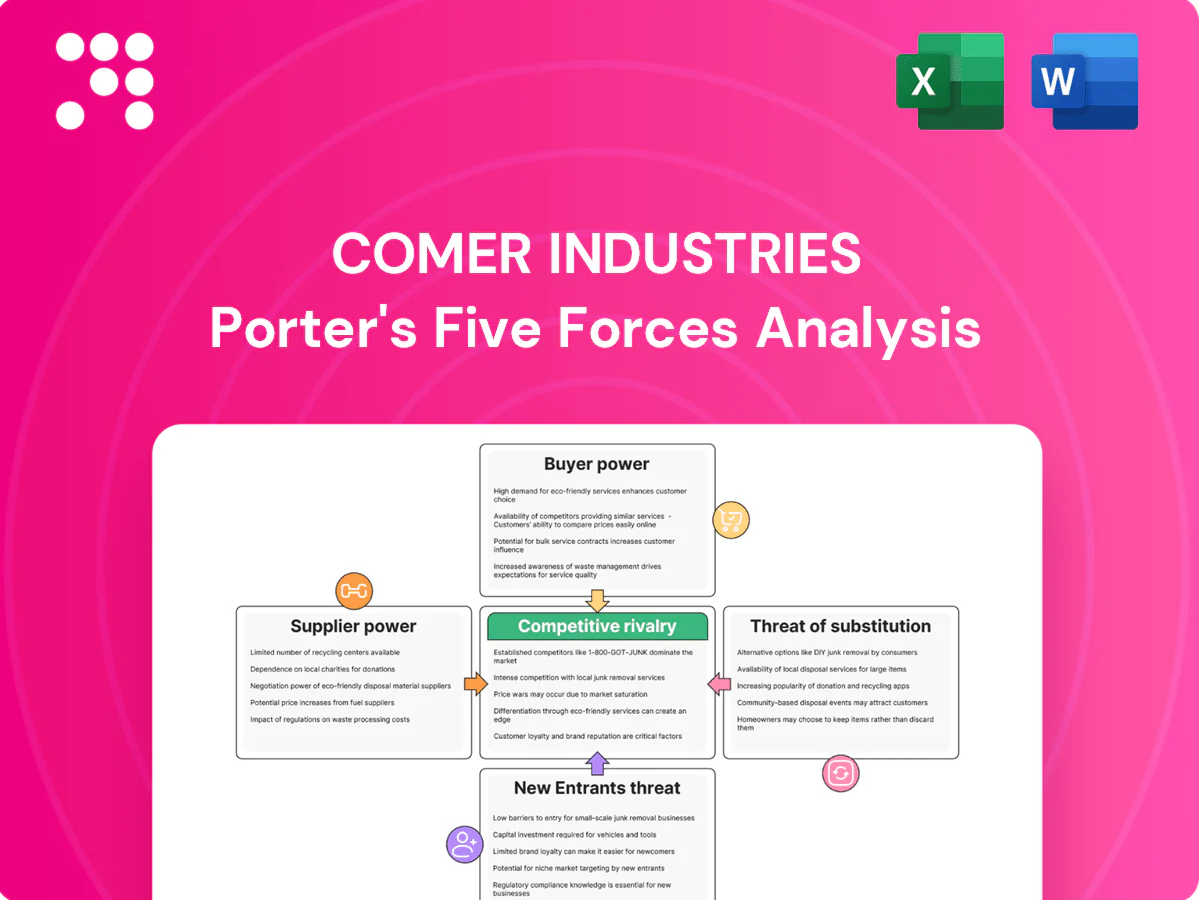

Comer Industries Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Comer Industries faces moderate supplier power and product differentiation in specialized driveline components, while buyer bargaining and substitute technologies pressure margins; competitive rivalry and entry barriers strongly shape strategy. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Comer Industries’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized alloy and precision components concentration

Comer depends on high-grade steels, bearings, seals and precision machined parts sourced from a concentrated supplier base, with single-source arrangements representing roughly 40–60% of specialty components in comparable industrial OEMs, increasing switching costs and lead-time risk. Supplier concentration routinely pushes lead times beyond 12 weeks for specialty bearings and alloys. Long-term contracts and dual-sourcing reduce but do not eliminate exposure. Any upstream capacity or quality constraint can cascade, disrupting delivery schedules and working capital.

Technological co-development with critical vendors

Mechatronic solutions require joint development of sensors, actuators and controllers, deepening supplier embedment and aligning roadmaps with Comer Industries’ product teams. Co-design improves system performance but increases dependence on vendors’ IP and strategic timelines, strengthening supplier leverage over price and allocations in 2024. Robust contracts and modular architectures help preserve flexibility and mitigate allocation risks.

Commodity price volatility passthrough

Steel, rare earths and energy cost swings in 2024 materially affect gearbox and motor BOMs, with suppliers frequently applying surcharges during spikes that compress margins. Comer can hedge raw-material exposure and use index-linked pricing with customers to pass through volatility. Ongoing value engineering and yield improvements lower raw-material intensity, reducing pass-through risk and margin pressure.

Global logistics and lead-time constraints

Long, complex supply chains for castings, forgings and electronics raise freight and delay risk; 2024 saw persistent port and inland congestion in key hubs (eg Los Angeles-Long Beach, Shanghai), amplifying supplier leverage. Suppliers with preferred logistics capacity capture outsized negotiating power during bottlenecks. Regionalization and inventory buffers lower disruption risk but tie up working capital, making rigorous supplier performance management a competitive differentiator.

- Higher freight/delay risk in long chains

- Preferred-logistics suppliers gain leverage

- Regionalization + buffers = lower risk, higher working capital

- Supplier performance management differentiates

Quality and certification requirements

High durability standards across agriculture, industrial and renewable applications narrow the qualified vendor pool, concentrating supplier power. Certification and audit overheads raise switching costs for buyers, while suppliers that meet stringent specs secure better pricing and contract terms. Rigorous incoming inspection plus PPAP/APQP processes preserve buyer confidence but also sustain supplier leverage through transparent performance data.

- Durability-led vendor concentration

- Certification/audit = higher switching costs

- Spec-compliant suppliers extract premium terms

- PPAP/APQP drive performance transparency

Supplier concentration and >12-week lead times squeeze margins, forcing inventory buffers

Comer faces concentrated supplier power: single-source specialty components account for roughly 40–60%, driving switching costs and >12 week lead times in 2024. Mechatronic co-design increases vendor IP dependence and 2024 allocation leverage. Raw-material and energy surcharges in 2024 compressed margins; regionalization and inventory buffers reduce disruption but raise working capital.

| Metric | 2024 |

|---|---|

| Single-source share | 40–60% |

| Specialty lead times | >12 weeks |

| Port congestion | Persistent (LA-LB, Shanghai) |

What is included in the product

Comer Industries Porter's Five Forces analysis uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats specific to Comer's industrial drivetrain and power transmission markets, with strategic implications for pricing and profitability.

A concise one-sheet Porter's Five Forces for Comer Industries pinpoints supplier, buyer and entrant pressures and highlights targeted strategic levers to reduce supplier power, deter new entrants, strengthen customer loyalty, and protect margins for faster decision-making.

Customers Bargaining Power

Concentrated OEM customer base

Large agricultural and industrial OEMs bring scale, professional procurement and pricing clout, routinely driving cost-downs of 5–15% through volume leverage. They can demand extended warranties and localization commitments, often tying suppliers into 3–7 year platform contracts. Losing a key OEM platform can materially cut volumes (commonly >20%), while multi-year wins stabilize revenue but raise dependency risk.

High switching costs from integration

Comer’s integrated transmissions and mechatronic systems are engineered into OEM drivetrains, and with vehicle development cycles typically 36–48 months (industry standard 2024), switching a drivetrain supplier commonly adds 12–24 months. The redesign, validation and field testing frequently push project costs beyond $10m, reducing short-term buyer power even for large OEMs. Lifecycle service contracts and recurring software updates further lock customers into Comer’s ecosystem, raising effective switching costs.

Price transparency and should-cost models

OEMs increasingly deploy should-cost analytics and competitive bidding to squeeze margins; the procurement analytics market reached about US$7.2B in 2024, reflecting accelerated adoption. Global supplier benchmarking sharpens negotiations, forcing Comer to defend value with documented efficiency, performance data and total cost of ownership analyses. Detailed cost breakdowns and VA/VE workshops can convert margin pressure into joint savings and contract wins.

Performance and uptime as decision drivers

End customers prioritize reliability, efficiency and torque density; proven field performance lowers price sensitivity as buyers focus on lifecycle cost. 99.9% uptime equates to ~8.76 hours downtime annually, making uptime critical. Serviceability and spare-parts availability directly cut lifetime downtime. Data-enabled maintenance shifts procurement from unit price to uptime value.

- Reliability-driven demand

- 99.9% uptime ≈ 8.76 hr/yr

- Spare parts reduce lifetime costs

- Predictive maintenance upsell on uptime

Customization and short lead-time demands

OEMs expect tailored ratios, housings and interfaces with rapid turnaround, increasing engineering load and complexity and giving buyers leverage on lead-time commitments.

Modular product platforms and configurable BOMs reduce custom engineering and protect margins, while collaborative planning aligns capacity with platform ramps.

- Tailored specs raise engineering effort and buyer leverage

- Modular platforms prevent margin leakage

- Configurable BOMs shorten delivery risk

- Collaborative planning matches capacity to ramp

OEM volume power cuts supplier margins 5-15%; long dev cycles and >US$10m locks

OEMs wield strong bargaining power via volume-driven cost-downs (5–15%) and multi-year platform contracts that can cut supplier volumes >20%. High switching costs — 36–48 month development cycles and >US$10m validation outlays — reduce short-term buyer mobility. Procurement analytics growth (US$7.2B in 2024) and benchmarking intensify price pressure; uptime (99.9% ≈ 8.76 hr/yr) shifts focus to lifecycle value.

| Metric | Value (2024) | Buyer Impact |

|---|---|---|

| OEM cost-downs | 5–15% | Margin pressure |

| Platform loss impact | >20% volume | Revenue risk |

| Dev cycle | 36–48 months | High switching cost |

| Validation cost | >US$10m | Locks suppliers |

| Procurement analytics | US$7.2B | Stronger negotiations |

| Uptime | 99.9% ≈ 8.76 hr/yr | Lifecycle value focus |

What You See Is What You Get

Comer Industries Porter's Five Forces Analysis

This Comer Industries Porter’s Five Forces analysis evaluates competitive rivalry, supplier and buyer power, threat of new entrants, and substitutes to inform strategic decisions. The preview is the exact document you'll receive immediately after purchase—fully formatted, complete, and ready to download for immediate use. It contains actionable insights and concise recommendations tailored to Comer Industries.

A Must-Have Tool for Decision-Makers

Comer Industries faces moderate supplier power and product differentiation in specialized driveline components, while buyer bargaining and substitute technologies pressure margins; competitive rivalry and entry barriers strongly shape strategy. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Comer Industries’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized alloy and precision components concentration

Comer depends on high-grade steels, bearings, seals and precision machined parts sourced from a concentrated supplier base, with single-source arrangements representing roughly 40–60% of specialty components in comparable industrial OEMs, increasing switching costs and lead-time risk. Supplier concentration routinely pushes lead times beyond 12 weeks for specialty bearings and alloys. Long-term contracts and dual-sourcing reduce but do not eliminate exposure. Any upstream capacity or quality constraint can cascade, disrupting delivery schedules and working capital.

Technological co-development with critical vendors

Mechatronic solutions require joint development of sensors, actuators and controllers, deepening supplier embedment and aligning roadmaps with Comer Industries’ product teams. Co-design improves system performance but increases dependence on vendors’ IP and strategic timelines, strengthening supplier leverage over price and allocations in 2024. Robust contracts and modular architectures help preserve flexibility and mitigate allocation risks.

Commodity price volatility passthrough

Steel, rare earths and energy cost swings in 2024 materially affect gearbox and motor BOMs, with suppliers frequently applying surcharges during spikes that compress margins. Comer can hedge raw-material exposure and use index-linked pricing with customers to pass through volatility. Ongoing value engineering and yield improvements lower raw-material intensity, reducing pass-through risk and margin pressure.

Global logistics and lead-time constraints

Long, complex supply chains for castings, forgings and electronics raise freight and delay risk; 2024 saw persistent port and inland congestion in key hubs (eg Los Angeles-Long Beach, Shanghai), amplifying supplier leverage. Suppliers with preferred logistics capacity capture outsized negotiating power during bottlenecks. Regionalization and inventory buffers lower disruption risk but tie up working capital, making rigorous supplier performance management a competitive differentiator.

- Higher freight/delay risk in long chains

- Preferred-logistics suppliers gain leverage

- Regionalization + buffers = lower risk, higher working capital

- Supplier performance management differentiates

Quality and certification requirements

High durability standards across agriculture, industrial and renewable applications narrow the qualified vendor pool, concentrating supplier power. Certification and audit overheads raise switching costs for buyers, while suppliers that meet stringent specs secure better pricing and contract terms. Rigorous incoming inspection plus PPAP/APQP processes preserve buyer confidence but also sustain supplier leverage through transparent performance data.

- Durability-led vendor concentration

- Certification/audit = higher switching costs

- Spec-compliant suppliers extract premium terms

- PPAP/APQP drive performance transparency

Supplier concentration and >12-week lead times squeeze margins, forcing inventory buffers

Comer faces concentrated supplier power: single-source specialty components account for roughly 40–60%, driving switching costs and >12 week lead times in 2024. Mechatronic co-design increases vendor IP dependence and 2024 allocation leverage. Raw-material and energy surcharges in 2024 compressed margins; regionalization and inventory buffers reduce disruption but raise working capital.

| Metric | 2024 |

|---|---|

| Single-source share | 40–60% |

| Specialty lead times | >12 weeks |

| Port congestion | Persistent (LA-LB, Shanghai) |

What is included in the product

Comer Industries Porter's Five Forces analysis uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats specific to Comer's industrial drivetrain and power transmission markets, with strategic implications for pricing and profitability.

A concise one-sheet Porter's Five Forces for Comer Industries pinpoints supplier, buyer and entrant pressures and highlights targeted strategic levers to reduce supplier power, deter new entrants, strengthen customer loyalty, and protect margins for faster decision-making.

Customers Bargaining Power

Concentrated OEM customer base

Large agricultural and industrial OEMs bring scale, professional procurement and pricing clout, routinely driving cost-downs of 5–15% through volume leverage. They can demand extended warranties and localization commitments, often tying suppliers into 3–7 year platform contracts. Losing a key OEM platform can materially cut volumes (commonly >20%), while multi-year wins stabilize revenue but raise dependency risk.

High switching costs from integration

Comer’s integrated transmissions and mechatronic systems are engineered into OEM drivetrains, and with vehicle development cycles typically 36–48 months (industry standard 2024), switching a drivetrain supplier commonly adds 12–24 months. The redesign, validation and field testing frequently push project costs beyond $10m, reducing short-term buyer power even for large OEMs. Lifecycle service contracts and recurring software updates further lock customers into Comer’s ecosystem, raising effective switching costs.

Price transparency and should-cost models

OEMs increasingly deploy should-cost analytics and competitive bidding to squeeze margins; the procurement analytics market reached about US$7.2B in 2024, reflecting accelerated adoption. Global supplier benchmarking sharpens negotiations, forcing Comer to defend value with documented efficiency, performance data and total cost of ownership analyses. Detailed cost breakdowns and VA/VE workshops can convert margin pressure into joint savings and contract wins.

Performance and uptime as decision drivers

End customers prioritize reliability, efficiency and torque density; proven field performance lowers price sensitivity as buyers focus on lifecycle cost. 99.9% uptime equates to ~8.76 hours downtime annually, making uptime critical. Serviceability and spare-parts availability directly cut lifetime downtime. Data-enabled maintenance shifts procurement from unit price to uptime value.

- Reliability-driven demand

- 99.9% uptime ≈ 8.76 hr/yr

- Spare parts reduce lifetime costs

- Predictive maintenance upsell on uptime

Customization and short lead-time demands

OEMs expect tailored ratios, housings and interfaces with rapid turnaround, increasing engineering load and complexity and giving buyers leverage on lead-time commitments.

Modular product platforms and configurable BOMs reduce custom engineering and protect margins, while collaborative planning aligns capacity with platform ramps.

- Tailored specs raise engineering effort and buyer leverage

- Modular platforms prevent margin leakage

- Configurable BOMs shorten delivery risk

- Collaborative planning matches capacity to ramp

OEM volume power cuts supplier margins 5-15%; long dev cycles and >US$10m locks

OEMs wield strong bargaining power via volume-driven cost-downs (5–15%) and multi-year platform contracts that can cut supplier volumes >20%. High switching costs — 36–48 month development cycles and >US$10m validation outlays — reduce short-term buyer mobility. Procurement analytics growth (US$7.2B in 2024) and benchmarking intensify price pressure; uptime (99.9% ≈ 8.76 hr/yr) shifts focus to lifecycle value.

| Metric | Value (2024) | Buyer Impact |

|---|---|---|

| OEM cost-downs | 5–15% | Margin pressure |

| Platform loss impact | >20% volume | Revenue risk |

| Dev cycle | 36–48 months | High switching cost |

| Validation cost | >US$10m | Locks suppliers |

| Procurement analytics | US$7.2B | Stronger negotiations |

| Uptime | 99.9% ≈ 8.76 hr/yr | Lifecycle value focus |

What You See Is What You Get

Comer Industries Porter's Five Forces Analysis

This Comer Industries Porter’s Five Forces analysis evaluates competitive rivalry, supplier and buyer power, threat of new entrants, and substitutes to inform strategic decisions. The preview is the exact document you'll receive immediately after purchase—fully formatted, complete, and ready to download for immediate use. It contains actionable insights and concise recommendations tailored to Comer Industries.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Comer Industries faces moderate supplier power and product differentiation in specialized driveline components, while buyer bargaining and substitute technologies pressure margins; competitive rivalry and entry barriers strongly shape strategy. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Comer Industries’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized alloy and precision components concentration

Comer depends on high-grade steels, bearings, seals and precision machined parts sourced from a concentrated supplier base, with single-source arrangements representing roughly 40–60% of specialty components in comparable industrial OEMs, increasing switching costs and lead-time risk. Supplier concentration routinely pushes lead times beyond 12 weeks for specialty bearings and alloys. Long-term contracts and dual-sourcing reduce but do not eliminate exposure. Any upstream capacity or quality constraint can cascade, disrupting delivery schedules and working capital.

Technological co-development with critical vendors

Mechatronic solutions require joint development of sensors, actuators and controllers, deepening supplier embedment and aligning roadmaps with Comer Industries’ product teams. Co-design improves system performance but increases dependence on vendors’ IP and strategic timelines, strengthening supplier leverage over price and allocations in 2024. Robust contracts and modular architectures help preserve flexibility and mitigate allocation risks.

Commodity price volatility passthrough

Steel, rare earths and energy cost swings in 2024 materially affect gearbox and motor BOMs, with suppliers frequently applying surcharges during spikes that compress margins. Comer can hedge raw-material exposure and use index-linked pricing with customers to pass through volatility. Ongoing value engineering and yield improvements lower raw-material intensity, reducing pass-through risk and margin pressure.

Global logistics and lead-time constraints

Long, complex supply chains for castings, forgings and electronics raise freight and delay risk; 2024 saw persistent port and inland congestion in key hubs (eg Los Angeles-Long Beach, Shanghai), amplifying supplier leverage. Suppliers with preferred logistics capacity capture outsized negotiating power during bottlenecks. Regionalization and inventory buffers lower disruption risk but tie up working capital, making rigorous supplier performance management a competitive differentiator.

- Higher freight/delay risk in long chains

- Preferred-logistics suppliers gain leverage

- Regionalization + buffers = lower risk, higher working capital

- Supplier performance management differentiates

Quality and certification requirements

High durability standards across agriculture, industrial and renewable applications narrow the qualified vendor pool, concentrating supplier power. Certification and audit overheads raise switching costs for buyers, while suppliers that meet stringent specs secure better pricing and contract terms. Rigorous incoming inspection plus PPAP/APQP processes preserve buyer confidence but also sustain supplier leverage through transparent performance data.

- Durability-led vendor concentration

- Certification/audit = higher switching costs

- Spec-compliant suppliers extract premium terms

- PPAP/APQP drive performance transparency

Supplier concentration and >12-week lead times squeeze margins, forcing inventory buffers

Comer faces concentrated supplier power: single-source specialty components account for roughly 40–60%, driving switching costs and >12 week lead times in 2024. Mechatronic co-design increases vendor IP dependence and 2024 allocation leverage. Raw-material and energy surcharges in 2024 compressed margins; regionalization and inventory buffers reduce disruption but raise working capital.

| Metric | 2024 |

|---|---|

| Single-source share | 40–60% |

| Specialty lead times | >12 weeks |

| Port congestion | Persistent (LA-LB, Shanghai) |

What is included in the product

Comer Industries Porter's Five Forces analysis uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats specific to Comer's industrial drivetrain and power transmission markets, with strategic implications for pricing and profitability.

A concise one-sheet Porter's Five Forces for Comer Industries pinpoints supplier, buyer and entrant pressures and highlights targeted strategic levers to reduce supplier power, deter new entrants, strengthen customer loyalty, and protect margins for faster decision-making.

Customers Bargaining Power

Concentrated OEM customer base

Large agricultural and industrial OEMs bring scale, professional procurement and pricing clout, routinely driving cost-downs of 5–15% through volume leverage. They can demand extended warranties and localization commitments, often tying suppliers into 3–7 year platform contracts. Losing a key OEM platform can materially cut volumes (commonly >20%), while multi-year wins stabilize revenue but raise dependency risk.

High switching costs from integration

Comer’s integrated transmissions and mechatronic systems are engineered into OEM drivetrains, and with vehicle development cycles typically 36–48 months (industry standard 2024), switching a drivetrain supplier commonly adds 12–24 months. The redesign, validation and field testing frequently push project costs beyond $10m, reducing short-term buyer power even for large OEMs. Lifecycle service contracts and recurring software updates further lock customers into Comer’s ecosystem, raising effective switching costs.

Price transparency and should-cost models

OEMs increasingly deploy should-cost analytics and competitive bidding to squeeze margins; the procurement analytics market reached about US$7.2B in 2024, reflecting accelerated adoption. Global supplier benchmarking sharpens negotiations, forcing Comer to defend value with documented efficiency, performance data and total cost of ownership analyses. Detailed cost breakdowns and VA/VE workshops can convert margin pressure into joint savings and contract wins.

Performance and uptime as decision drivers

End customers prioritize reliability, efficiency and torque density; proven field performance lowers price sensitivity as buyers focus on lifecycle cost. 99.9% uptime equates to ~8.76 hours downtime annually, making uptime critical. Serviceability and spare-parts availability directly cut lifetime downtime. Data-enabled maintenance shifts procurement from unit price to uptime value.

- Reliability-driven demand

- 99.9% uptime ≈ 8.76 hr/yr

- Spare parts reduce lifetime costs

- Predictive maintenance upsell on uptime

Customization and short lead-time demands

OEMs expect tailored ratios, housings and interfaces with rapid turnaround, increasing engineering load and complexity and giving buyers leverage on lead-time commitments.

Modular product platforms and configurable BOMs reduce custom engineering and protect margins, while collaborative planning aligns capacity with platform ramps.

- Tailored specs raise engineering effort and buyer leverage

- Modular platforms prevent margin leakage

- Configurable BOMs shorten delivery risk

- Collaborative planning matches capacity to ramp

OEM volume power cuts supplier margins 5-15%; long dev cycles and >US$10m locks

OEMs wield strong bargaining power via volume-driven cost-downs (5–15%) and multi-year platform contracts that can cut supplier volumes >20%. High switching costs — 36–48 month development cycles and >US$10m validation outlays — reduce short-term buyer mobility. Procurement analytics growth (US$7.2B in 2024) and benchmarking intensify price pressure; uptime (99.9% ≈ 8.76 hr/yr) shifts focus to lifecycle value.

| Metric | Value (2024) | Buyer Impact |

|---|---|---|

| OEM cost-downs | 5–15% | Margin pressure |

| Platform loss impact | >20% volume | Revenue risk |

| Dev cycle | 36–48 months | High switching cost |

| Validation cost | >US$10m | Locks suppliers |

| Procurement analytics | US$7.2B | Stronger negotiations |

| Uptime | 99.9% ≈ 8.76 hr/yr | Lifecycle value focus |

What You See Is What You Get

Comer Industries Porter's Five Forces Analysis

This Comer Industries Porter’s Five Forces analysis evaluates competitive rivalry, supplier and buyer power, threat of new entrants, and substitutes to inform strategic decisions. The preview is the exact document you'll receive immediately after purchase—fully formatted, complete, and ready to download for immediate use. It contains actionable insights and concise recommendations tailored to Comer Industries.