Compal Electronics Porter's Five Forces Analysis

From Overview to Strategy Blueprint

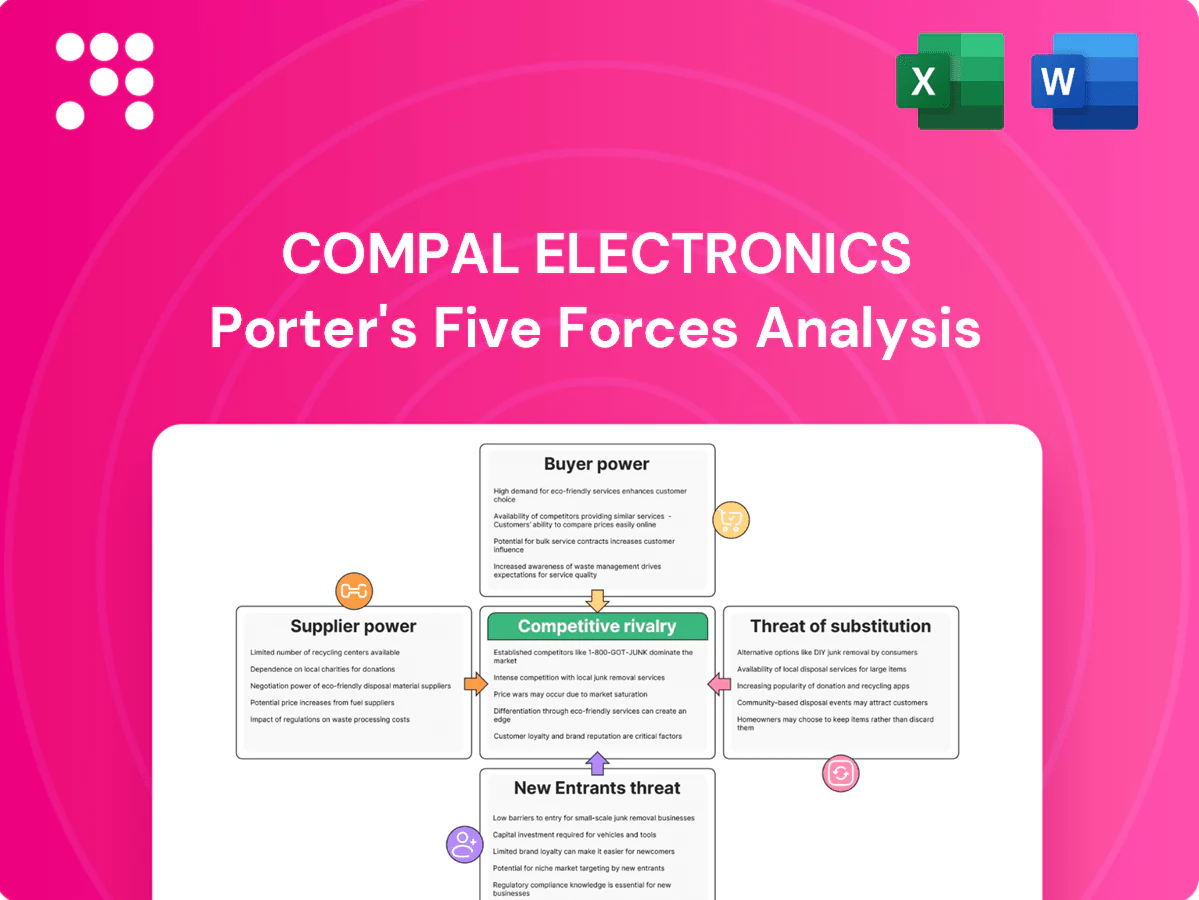

Compal Electronics faces intense buyer pressure, concentrated suppliers, moderate threat from new entrants, strong OEM rivalry, and rising substitute risks as devices evolve. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Compal Electronics’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Key component concentration

CPU/GPU suppliers such as Intel, AMD and NVIDIA, memory suppliers Samsung, SK Hynix and Micron, and panel makers BOE, Samsung Display and LG Display concentrate upstream bargaining power for Compal. Top three memory vendors held roughly 70% market share in 2024 and top three panel makers about 65%, limiting substitutes for leading-edge parts. Suppliers can dictate lead times and pricing, forcing Compal to multi-source while absorbing long qualification timelines. Volume commitments and vendor-managed inventory arrangements partially offset pricing pressure.

Semiconductor cycle swings

Semiconductor supply-demand cycles drive sharp price and allocation swings that suppliers leverage; the global semiconductor market was about $600 billion in 2024 (WSTS estimate). In tight cycles allocation favors highest-margin segments, squeezing ODMs' margins and availability. Compal’s scale improves allocation access but does not secure pricing autonomy. Greater design flexibility to alternative chipsets lowers exposure at the cost of higher engineering spend.

Panel and battery leverage

Display panels and lithium battery packs are high-value BOM items sourced from few tier-1 vendors such as Samsung Display, BOE, LG Display and battery suppliers CATL, LG Energy Solution, Panasonic; CATL held roughly 34% of the global EV battery pack market in 2024, underscoring supplier concentration. Suppliers with advanced nodes or safety certifications gain negotiating clout, long qualification and safety testing raise switching frictions for Compal, and framework agreements or co-development deals are used to trade volume for better terms.

Tooling and NRE lock-ins

Custom tooling, fixtures and NRE create sunk costs tied to specific suppliers, making mid-cycle supplier changes risky due to potential delays and quality variance; suppliers leverage these frictions to protect margins and stricter payment terms.

Compal mitigates exposure by using modular designs and standardized components to preserve supplier options and reduce lock-in.

- Custom NRE creates supplier-specific sunk costs

- Mid-cycle switches risk delays and quality issues

- Suppliers use lock-in to maintain margins and payment terms

- Compal uses modularity and standard components to retain flexibility

Geopolitics and logistics

Taiwan–China dynamics, tighter export controls on advanced semiconductors and episodic freight disruptions raise supplier leverage during shocks; Taiwan still supplies >90% of global 5nm+ capacity, concentrating strategic risk. Compliance demands on traceability and origin curb rapid re-sourcing, while Compal’s regional diversification and near-shoring reduce disruption risk at higher unit cost. Strategic buffers and dual logistics lanes blunt short-term leverage spikes.

- Supplier concentration: Taiwan >90% of 5nm+ capacity

- Compliance: traceability limits quick re-sourcing

- Mitigation: regional diversification raises cost

- Buffers: dual lanes reduce leverage spikes

Supply squeeze: Memory ~70%, Panels ~65%, 5nm+ Taiwan >90%

Compal faces strong supplier bargaining power: top-three memory vendors ~70% share and top-three panel makers ~65% in 2024, constraining substitutes and pricing. Semiconductor market ~$600B in 2024 with Taiwan holding >90% of 5nm+ capacity, increasing strategic leverage. Volume commitments, co-development and modular design partially mitigate but raise qualification and NRE lock-in costs.

| Supplier | 2024 metric | Concentration |

|---|---|---|

| Memory | Top3 ~70% | High |

| Panels | Top3 ~65% | High |

| Semiconductors | Market ~$600B; 5nm+ >90% Taiwan | Strategic |

| Batteries | CATL ~34% EV pack | High |

What is included in the product

Tailored Porter's Five Forces analysis for Compal Electronics uncovering competitive intensity, supplier and buyer power, threats from substitutes and new entrants, and emerging disruptive forces that influence pricing, margins, and strategic positioning.

A concise, one-sheet Porter's Five Forces view for Compal Electronics—instantly highlights supplier, buyer, rivalry, threat of entry and substitutes to ease strategic decisions. Clean spider chart and editable pressure levels make it slide-ready and simple to update as market dynamics change.

Customers Bargaining Power

Concentrated global OEMs

Large global OEMs place high-volume, multi-year orders that give them strong bargaining power; 2024 IDC data shows the top five PC OEMs held roughly 75% of global shipments, concentrating buyer leverage. They push aggressive pricing, tight SLAs and design-to-cost targets, squeezing supplier margins and forcing continuous cost optimization. Losing one anchor account can materially dent factory utilization and revenues, so Compal must defend share through superior service quality and faster speed-to-market.

Dual-sourcing norms

Most OEMs split programs across multiple ODMs to avoid single-supplier dependence, enabling direct price benchmarking and rapid vendor switches. This dual-sourcing norm forces Compal into continuous rebids and engineering bake-offs as customers leverage alternatives during design cycles. Long-term, sticky relationships with major clients reduce churn but do not eliminate buyer leverage.

Design ownership and specs

When buyers retain design specs and IP they can re-bid manufacturing with minimal friction, eroding margins and enabling supplier churn; in 2024 OEM cost-down targets averaged about 5% annually, keeping price pressure high. ODM-owned reference designs reduce this buyer power but remain uneven across segments. Compal’s JDM offerings, which grew in 2024, raise stickiness by embedding more engineering value, though lifecycle cost-down demands persist.

Quality and compliance leverage

Buyers enforce stringent yield, ESG and regulatory standards with explicit penalty regimes, shifting chargeback and noncompliance risk and cost to Compal across product ramps; failure can trigger chargebacks and lost future awards while exceeding KPIs secures preferred-vendor status and volume stability.

- Penalty regimes: transfer ramp risk to supplier

- Chargebacks: immediate financial impact

- KPIs: route to preferred-vendor + volume certainty

Cross-category bundling

OEMs in 2024 pushed cross-category bundling across notebooks, tablets and wearables to extract volume discounts, leveraging consolidated procurement to expand negotiating scope and lower ASPs for ODMs like Compal.

Compal responds by prioritizing capacity for higher-margin programs and offering differentiated engineering support to defend margins and lead times.

Diversification into automotive electronics and healthcare devices in 2024 reduces Compal’s exposure to any single category and strengthens bargaining resilience.

- OEM bundling: broader leverage across product lines

- Compal defense: capacity prioritization + engineering differentiation

- Diversification 2024: auto & healthcare lower single-category dependence

Top-5 OEMs hold ≈75% of PCs, forcing ≈5% annual cost-downs and stricter penalties

Large OEMs (top five ≈75% global PC shipments, IDC 2024) exert strong price and SLA pressure; OEMs targeted ~5% annual cost-downs in 2024, squeezing ODM margins. Dual-sourcing and retained IP enable rapid rebids, while Compal’s growing JDM and moves into automotive and healthcare in 2024 raise stickiness and resilience. Stringent penalty/chargeback regimes transfer ramp risk to suppliers.

| Metric | 2024 |

|---|---|

| Top‑5 OEM share (PC) | ≈75% |

| Avg OEM cost‑down | ≈5% p.a. |

| Buyer leverage | High |

| Compal response | JDM growth; auto & healthcare diversification |

What You See Is What You Get

Compal Electronics Porter's Five Forces Analysis

This preview shows the exact Compal Electronics Porter's Five Forces analysis you'll receive after purchase—no placeholders. The concise, professionally formatted report assesses industry rivalry, supplier and buyer power, and the threats of substitutes and new entrants. It highlights strategic implications and is ready to download and use immediately upon payment.

From Overview to Strategy Blueprint

Compal Electronics faces intense buyer pressure, concentrated suppliers, moderate threat from new entrants, strong OEM rivalry, and rising substitute risks as devices evolve. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Compal Electronics’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Key component concentration

CPU/GPU suppliers such as Intel, AMD and NVIDIA, memory suppliers Samsung, SK Hynix and Micron, and panel makers BOE, Samsung Display and LG Display concentrate upstream bargaining power for Compal. Top three memory vendors held roughly 70% market share in 2024 and top three panel makers about 65%, limiting substitutes for leading-edge parts. Suppliers can dictate lead times and pricing, forcing Compal to multi-source while absorbing long qualification timelines. Volume commitments and vendor-managed inventory arrangements partially offset pricing pressure.

Semiconductor cycle swings

Semiconductor supply-demand cycles drive sharp price and allocation swings that suppliers leverage; the global semiconductor market was about $600 billion in 2024 (WSTS estimate). In tight cycles allocation favors highest-margin segments, squeezing ODMs' margins and availability. Compal’s scale improves allocation access but does not secure pricing autonomy. Greater design flexibility to alternative chipsets lowers exposure at the cost of higher engineering spend.

Panel and battery leverage

Display panels and lithium battery packs are high-value BOM items sourced from few tier-1 vendors such as Samsung Display, BOE, LG Display and battery suppliers CATL, LG Energy Solution, Panasonic; CATL held roughly 34% of the global EV battery pack market in 2024, underscoring supplier concentration. Suppliers with advanced nodes or safety certifications gain negotiating clout, long qualification and safety testing raise switching frictions for Compal, and framework agreements or co-development deals are used to trade volume for better terms.

Tooling and NRE lock-ins

Custom tooling, fixtures and NRE create sunk costs tied to specific suppliers, making mid-cycle supplier changes risky due to potential delays and quality variance; suppliers leverage these frictions to protect margins and stricter payment terms.

Compal mitigates exposure by using modular designs and standardized components to preserve supplier options and reduce lock-in.

- Custom NRE creates supplier-specific sunk costs

- Mid-cycle switches risk delays and quality issues

- Suppliers use lock-in to maintain margins and payment terms

- Compal uses modularity and standard components to retain flexibility

Geopolitics and logistics

Taiwan–China dynamics, tighter export controls on advanced semiconductors and episodic freight disruptions raise supplier leverage during shocks; Taiwan still supplies >90% of global 5nm+ capacity, concentrating strategic risk. Compliance demands on traceability and origin curb rapid re-sourcing, while Compal’s regional diversification and near-shoring reduce disruption risk at higher unit cost. Strategic buffers and dual logistics lanes blunt short-term leverage spikes.

- Supplier concentration: Taiwan >90% of 5nm+ capacity

- Compliance: traceability limits quick re-sourcing

- Mitigation: regional diversification raises cost

- Buffers: dual lanes reduce leverage spikes

Supply squeeze: Memory ~70%, Panels ~65%, 5nm+ Taiwan >90%

Compal faces strong supplier bargaining power: top-three memory vendors ~70% share and top-three panel makers ~65% in 2024, constraining substitutes and pricing. Semiconductor market ~$600B in 2024 with Taiwan holding >90% of 5nm+ capacity, increasing strategic leverage. Volume commitments, co-development and modular design partially mitigate but raise qualification and NRE lock-in costs.

| Supplier | 2024 metric | Concentration |

|---|---|---|

| Memory | Top3 ~70% | High |

| Panels | Top3 ~65% | High |

| Semiconductors | Market ~$600B; 5nm+ >90% Taiwan | Strategic |

| Batteries | CATL ~34% EV pack | High |

What is included in the product

Tailored Porter's Five Forces analysis for Compal Electronics uncovering competitive intensity, supplier and buyer power, threats from substitutes and new entrants, and emerging disruptive forces that influence pricing, margins, and strategic positioning.

A concise, one-sheet Porter's Five Forces view for Compal Electronics—instantly highlights supplier, buyer, rivalry, threat of entry and substitutes to ease strategic decisions. Clean spider chart and editable pressure levels make it slide-ready and simple to update as market dynamics change.

Customers Bargaining Power

Concentrated global OEMs

Large global OEMs place high-volume, multi-year orders that give them strong bargaining power; 2024 IDC data shows the top five PC OEMs held roughly 75% of global shipments, concentrating buyer leverage. They push aggressive pricing, tight SLAs and design-to-cost targets, squeezing supplier margins and forcing continuous cost optimization. Losing one anchor account can materially dent factory utilization and revenues, so Compal must defend share through superior service quality and faster speed-to-market.

Dual-sourcing norms

Most OEMs split programs across multiple ODMs to avoid single-supplier dependence, enabling direct price benchmarking and rapid vendor switches. This dual-sourcing norm forces Compal into continuous rebids and engineering bake-offs as customers leverage alternatives during design cycles. Long-term, sticky relationships with major clients reduce churn but do not eliminate buyer leverage.

Design ownership and specs

When buyers retain design specs and IP they can re-bid manufacturing with minimal friction, eroding margins and enabling supplier churn; in 2024 OEM cost-down targets averaged about 5% annually, keeping price pressure high. ODM-owned reference designs reduce this buyer power but remain uneven across segments. Compal’s JDM offerings, which grew in 2024, raise stickiness by embedding more engineering value, though lifecycle cost-down demands persist.

Quality and compliance leverage

Buyers enforce stringent yield, ESG and regulatory standards with explicit penalty regimes, shifting chargeback and noncompliance risk and cost to Compal across product ramps; failure can trigger chargebacks and lost future awards while exceeding KPIs secures preferred-vendor status and volume stability.

- Penalty regimes: transfer ramp risk to supplier

- Chargebacks: immediate financial impact

- KPIs: route to preferred-vendor + volume certainty

Cross-category bundling

OEMs in 2024 pushed cross-category bundling across notebooks, tablets and wearables to extract volume discounts, leveraging consolidated procurement to expand negotiating scope and lower ASPs for ODMs like Compal.

Compal responds by prioritizing capacity for higher-margin programs and offering differentiated engineering support to defend margins and lead times.

Diversification into automotive electronics and healthcare devices in 2024 reduces Compal’s exposure to any single category and strengthens bargaining resilience.

- OEM bundling: broader leverage across product lines

- Compal defense: capacity prioritization + engineering differentiation

- Diversification 2024: auto & healthcare lower single-category dependence

Top-5 OEMs hold ≈75% of PCs, forcing ≈5% annual cost-downs and stricter penalties

Large OEMs (top five ≈75% global PC shipments, IDC 2024) exert strong price and SLA pressure; OEMs targeted ~5% annual cost-downs in 2024, squeezing ODM margins. Dual-sourcing and retained IP enable rapid rebids, while Compal’s growing JDM and moves into automotive and healthcare in 2024 raise stickiness and resilience. Stringent penalty/chargeback regimes transfer ramp risk to suppliers.

| Metric | 2024 |

|---|---|

| Top‑5 OEM share (PC) | ≈75% |

| Avg OEM cost‑down | ≈5% p.a. |

| Buyer leverage | High |

| Compal response | JDM growth; auto & healthcare diversification |

What You See Is What You Get

Compal Electronics Porter's Five Forces Analysis

This preview shows the exact Compal Electronics Porter's Five Forces analysis you'll receive after purchase—no placeholders. The concise, professionally formatted report assesses industry rivalry, supplier and buyer power, and the threats of substitutes and new entrants. It highlights strategic implications and is ready to download and use immediately upon payment.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Compal Electronics faces intense buyer pressure, concentrated suppliers, moderate threat from new entrants, strong OEM rivalry, and rising substitute risks as devices evolve. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Compal Electronics’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Key component concentration

CPU/GPU suppliers such as Intel, AMD and NVIDIA, memory suppliers Samsung, SK Hynix and Micron, and panel makers BOE, Samsung Display and LG Display concentrate upstream bargaining power for Compal. Top three memory vendors held roughly 70% market share in 2024 and top three panel makers about 65%, limiting substitutes for leading-edge parts. Suppliers can dictate lead times and pricing, forcing Compal to multi-source while absorbing long qualification timelines. Volume commitments and vendor-managed inventory arrangements partially offset pricing pressure.

Semiconductor cycle swings

Semiconductor supply-demand cycles drive sharp price and allocation swings that suppliers leverage; the global semiconductor market was about $600 billion in 2024 (WSTS estimate). In tight cycles allocation favors highest-margin segments, squeezing ODMs' margins and availability. Compal’s scale improves allocation access but does not secure pricing autonomy. Greater design flexibility to alternative chipsets lowers exposure at the cost of higher engineering spend.

Panel and battery leverage

Display panels and lithium battery packs are high-value BOM items sourced from few tier-1 vendors such as Samsung Display, BOE, LG Display and battery suppliers CATL, LG Energy Solution, Panasonic; CATL held roughly 34% of the global EV battery pack market in 2024, underscoring supplier concentration. Suppliers with advanced nodes or safety certifications gain negotiating clout, long qualification and safety testing raise switching frictions for Compal, and framework agreements or co-development deals are used to trade volume for better terms.

Tooling and NRE lock-ins

Custom tooling, fixtures and NRE create sunk costs tied to specific suppliers, making mid-cycle supplier changes risky due to potential delays and quality variance; suppliers leverage these frictions to protect margins and stricter payment terms.

Compal mitigates exposure by using modular designs and standardized components to preserve supplier options and reduce lock-in.

- Custom NRE creates supplier-specific sunk costs

- Mid-cycle switches risk delays and quality issues

- Suppliers use lock-in to maintain margins and payment terms

- Compal uses modularity and standard components to retain flexibility

Geopolitics and logistics

Taiwan–China dynamics, tighter export controls on advanced semiconductors and episodic freight disruptions raise supplier leverage during shocks; Taiwan still supplies >90% of global 5nm+ capacity, concentrating strategic risk. Compliance demands on traceability and origin curb rapid re-sourcing, while Compal’s regional diversification and near-shoring reduce disruption risk at higher unit cost. Strategic buffers and dual logistics lanes blunt short-term leverage spikes.

- Supplier concentration: Taiwan >90% of 5nm+ capacity

- Compliance: traceability limits quick re-sourcing

- Mitigation: regional diversification raises cost

- Buffers: dual lanes reduce leverage spikes

Supply squeeze: Memory ~70%, Panels ~65%, 5nm+ Taiwan >90%

Compal faces strong supplier bargaining power: top-three memory vendors ~70% share and top-three panel makers ~65% in 2024, constraining substitutes and pricing. Semiconductor market ~$600B in 2024 with Taiwan holding >90% of 5nm+ capacity, increasing strategic leverage. Volume commitments, co-development and modular design partially mitigate but raise qualification and NRE lock-in costs.

| Supplier | 2024 metric | Concentration |

|---|---|---|

| Memory | Top3 ~70% | High |

| Panels | Top3 ~65% | High |

| Semiconductors | Market ~$600B; 5nm+ >90% Taiwan | Strategic |

| Batteries | CATL ~34% EV pack | High |

What is included in the product

Tailored Porter's Five Forces analysis for Compal Electronics uncovering competitive intensity, supplier and buyer power, threats from substitutes and new entrants, and emerging disruptive forces that influence pricing, margins, and strategic positioning.

A concise, one-sheet Porter's Five Forces view for Compal Electronics—instantly highlights supplier, buyer, rivalry, threat of entry and substitutes to ease strategic decisions. Clean spider chart and editable pressure levels make it slide-ready and simple to update as market dynamics change.

Customers Bargaining Power

Concentrated global OEMs

Large global OEMs place high-volume, multi-year orders that give them strong bargaining power; 2024 IDC data shows the top five PC OEMs held roughly 75% of global shipments, concentrating buyer leverage. They push aggressive pricing, tight SLAs and design-to-cost targets, squeezing supplier margins and forcing continuous cost optimization. Losing one anchor account can materially dent factory utilization and revenues, so Compal must defend share through superior service quality and faster speed-to-market.

Dual-sourcing norms

Most OEMs split programs across multiple ODMs to avoid single-supplier dependence, enabling direct price benchmarking and rapid vendor switches. This dual-sourcing norm forces Compal into continuous rebids and engineering bake-offs as customers leverage alternatives during design cycles. Long-term, sticky relationships with major clients reduce churn but do not eliminate buyer leverage.

Design ownership and specs

When buyers retain design specs and IP they can re-bid manufacturing with minimal friction, eroding margins and enabling supplier churn; in 2024 OEM cost-down targets averaged about 5% annually, keeping price pressure high. ODM-owned reference designs reduce this buyer power but remain uneven across segments. Compal’s JDM offerings, which grew in 2024, raise stickiness by embedding more engineering value, though lifecycle cost-down demands persist.

Quality and compliance leverage

Buyers enforce stringent yield, ESG and regulatory standards with explicit penalty regimes, shifting chargeback and noncompliance risk and cost to Compal across product ramps; failure can trigger chargebacks and lost future awards while exceeding KPIs secures preferred-vendor status and volume stability.

- Penalty regimes: transfer ramp risk to supplier

- Chargebacks: immediate financial impact

- KPIs: route to preferred-vendor + volume certainty

Cross-category bundling

OEMs in 2024 pushed cross-category bundling across notebooks, tablets and wearables to extract volume discounts, leveraging consolidated procurement to expand negotiating scope and lower ASPs for ODMs like Compal.

Compal responds by prioritizing capacity for higher-margin programs and offering differentiated engineering support to defend margins and lead times.

Diversification into automotive electronics and healthcare devices in 2024 reduces Compal’s exposure to any single category and strengthens bargaining resilience.

- OEM bundling: broader leverage across product lines

- Compal defense: capacity prioritization + engineering differentiation

- Diversification 2024: auto & healthcare lower single-category dependence

Top-5 OEMs hold ≈75% of PCs, forcing ≈5% annual cost-downs and stricter penalties

Large OEMs (top five ≈75% global PC shipments, IDC 2024) exert strong price and SLA pressure; OEMs targeted ~5% annual cost-downs in 2024, squeezing ODM margins. Dual-sourcing and retained IP enable rapid rebids, while Compal’s growing JDM and moves into automotive and healthcare in 2024 raise stickiness and resilience. Stringent penalty/chargeback regimes transfer ramp risk to suppliers.

| Metric | 2024 |

|---|---|

| Top‑5 OEM share (PC) | ≈75% |

| Avg OEM cost‑down | ≈5% p.a. |

| Buyer leverage | High |

| Compal response | JDM growth; auto & healthcare diversification |

What You See Is What You Get

Compal Electronics Porter's Five Forces Analysis

This preview shows the exact Compal Electronics Porter's Five Forces analysis you'll receive after purchase—no placeholders. The concise, professionally formatted report assesses industry rivalry, supplier and buyer power, and the threats of substitutes and new entrants. It highlights strategic implications and is ready to download and use immediately upon payment.