Componenta Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

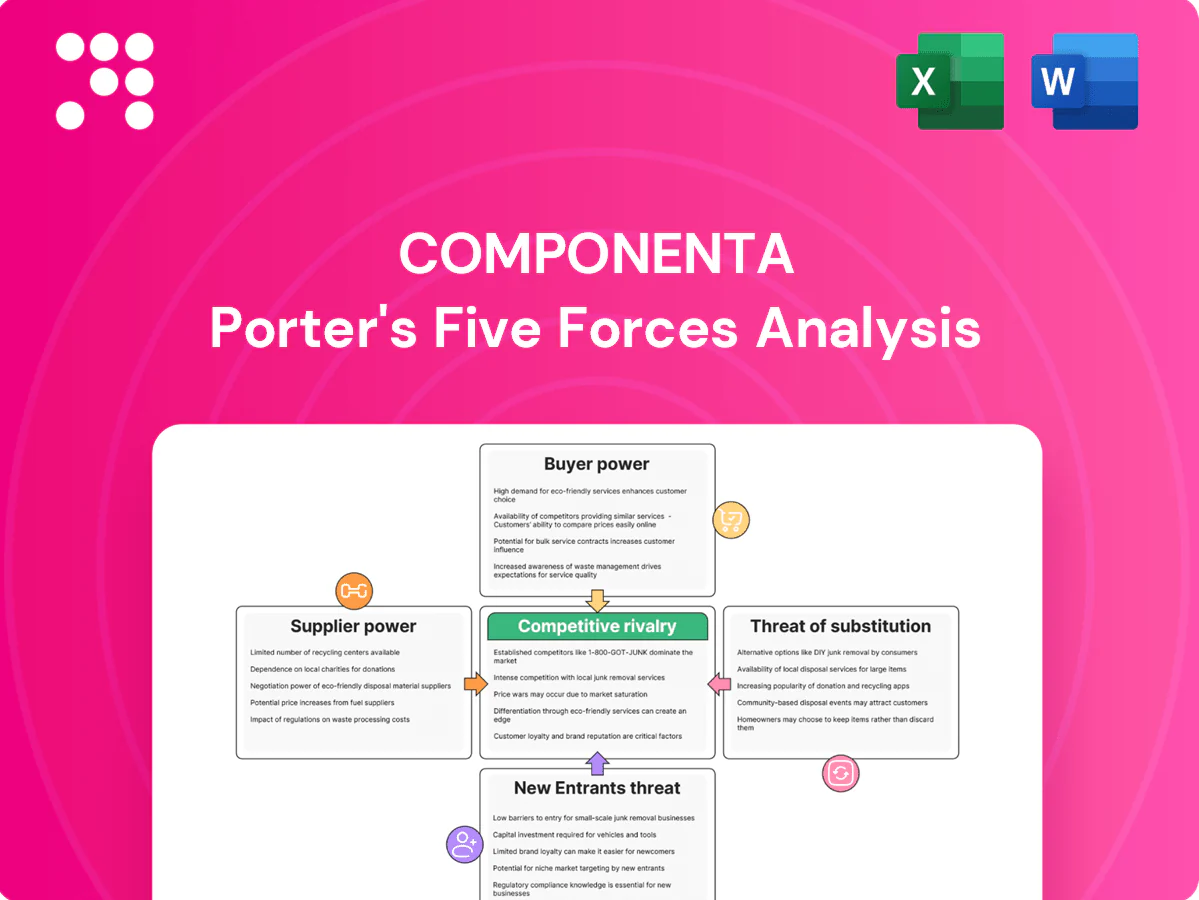

Componenta faces moderate supplier power, niche buyer pockets, and steady threat from substitutes amid cyclical metal demand. Competitive rivalry is intense but tempered by specialized casting capabilities and service contracts. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Componenta’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated raw material sources

Cast iron production depends on pig iron, steel scrap and alloying elements often sourced from a concentrated pool of regional metals traders, giving suppliers elevated pricing power and reducing Componenta’s negotiating room. Supplier consolidation raises the risk of cost pass-through and supply tightness; long-term contracts mitigate volatility but commonly include indexation that shifts price risk to buyers. Componenta can reduce leverage by diversifying suppliers geographically and locking in multi-sourced frameworks.

Energy intensity and utilities leverage

Melting and heat treatment make energy a major cost driver for foundries; EU average industrial electricity was about €0.12/kWh in 2024 and EUA carbon allowances averaged near €90/tCO2, giving power and gas providers structural influence. Price spikes or carbon-linked surcharges can compress margins quickly. Demand-side management and renewable PPAs reduce exposure and improve sustainability credentials. Location near stable grids and active hedging practices temper supplier power.

Specialized consumables and tooling

Specialized consumables—foundry sand, binders/resins, refractory linings and precision machining tools—are sourced from niche suppliers, giving suppliers elevated leverage in 2024 as qualified alternatives remain limited. Switching costs arise from process recalibration and quality consistency requirements, with testing and validation often taking several months. Dual-qualifying consumables lowers dependence but requires capital for trials and certification; collaborative supplier development secures performance and can yield preferential terms.

Logistics and proximity constraints

Bulky inputs and JIT schedules give regional suppliers outsized leverage over lead times and freight costs; 2024 industry surveys report proximity ranks as a top-3 supplier advantage for 72% of manufacturers. Port congestion and tight trucking capacity (peak delays up to multi-day) amplify that power, while nearshoring and inventory buffers stabilize flow. Digital tracking in 2024 cut dispute resolution times materially.

- Regional suppliers: proximity advantage

- Port/truck delays: amplify supplier power

- Nearshoring/inventory: flow stability

- Digital tracking: visibility, faster disputes

ESG and compliance requirements

Supplier adherence to ISO 14001/45001 and EU CSRD-driven disclosure (phased from 2024) directly affects Componenta’s certifications and customer audits; non-compliant suppliers tighten the qualified pool and raise supplier bargaining power. Collaborative ESG programs and transparency platforms plus sharing EN 15804/ISO 14025-compliant lifecycle data (EPDs) expand the qualified supplier base and support Componenta’s sustainable manufacturing claims.

- ISO 14001/45001: compliance baseline

- CSRD (phased from 2024): increased disclosure pressure

- EN 15804/ISO 14025: lifecycle data standardization (EPDs)

- Joint ESG programs: reduce supplier concentration risk

Supplier concentration and EU energy costs strengthen pricing power; use PPAs, dual-qualify

Cast iron inputs and specialized consumables are concentrated, giving suppliers strong pricing power; EU industrial electricity ~€0.12/kWh and EUA ~€90/tCO2 in 2024 amplify energy supplier influence. Proximity, port/truck delays (72% cite proximity as top‑3 advantage) and JIT logistics raise lead‑time leverage. Diversification, dual‑qualification, renewable PPAs and ESG collaboration reduce supplier bargaining power.

| Category | 2024 data | Impact |

|---|---|---|

| Energy | €0.12/kWh; EUA €90/tCO2 | High cost volatility |

| Proximity/logistics | 72% proximity importance | Lead‑time leverage |

| Consumables | Limited qualified suppliers | Switching costs |

| Standards/ESG | CSRD phased 2024 | Supplier pool constrained |

What is included in the product

Tailored Porter's Five Forces analysis for Componenta that uncovers key drivers of competition, buyer and supplier power, and market entry risks; evaluates pricing influence and profitability pressures. Identifies disruptive forces, substitutes and strategic barriers protecting incumbents, formatted for easy inclusion in reports or investor decks.

Componenta Porter's Five Forces delivers a concise one-sheet with an editable radar chart to visualize competitive pressures instantly—perfect for fast strategic decisions and boardroom slides. Customize force levels, swap in your data, and export clean visuals without complex tools to relieve analysis bottlenecks.

Customers Bargaining Power

Large OEMs with scale

Vehicle, machinery and equipment OEMs buy in high volumes and negotiate aggressively, often via structured tenders and multi-year frameworks of 3–5 years. Their scale forces price compression and payment-term pressure, commonly extending terms from 30 to 120 days. Componenta must differentiate through quality, engineering partnerships and service to preserve margins rather than competing on price alone.

Engineering lock-in vs dual sourcing

Custom castings create engineering lock-in: tooling (often $50k–$500k per tool) plus process know-how and PPAP/FAI cycles (commonly 4–12 weeks) raise switching costs for OEMs. Many OEMs nonetheless mandate dual sourcing for resilience, capping pricing power for any single supplier. Maintaining second-source status requires consistent quality and delivery metrics (PPM targets under 100 and OTIF >95%). Value engineering—cost reduction and part consolidation—deepens customer stickiness.

Cyclical demand and price sensitivity

End markets for Componenta are cyclical, making buyers markedly more price sensitive in downturns and intensifying requests for index-linked contracts and raw-material surcharges during negotiations.

Componenta defends margins through flexible capacity, transparent cost breakdowns and pass-through clauses, while VAVE proposals reposition talks toward total cost of ownership rather than unit price.

Service level and delivery expectations

On-time delivery, short lead times and low defect rates (industry benchmark: 95% OTIF, defect rate <1% in 2024) are primary buyer metrics used to rank suppliers; poor scores trigger penalties or re-sourcing via performance scorecards. Advanced planning, quality systems and integrated logistics/EDI reduce buyer leverage by closing service gaps.

- OTIF ≥95%

- Defect rate <1%

- Scorecards → penalties/re-sourcing

- EDI + integrated logistics improve responsiveness

ESG and traceability demands

OEMs increasingly require carbon footprint data, recycled content and compliance proofs; EU CSRD came into force in 2024 and EU carbon prices averaged near €90/tCO2 in 2024, raising procurement ESG scrutiny. Suppliers with verified sustainability metrics gain negotiating room, while lack of traceability lets buyers push discounts or switch; Componenta’s sustainability focus can convert compliance into a premium.

- OEM ESG demands: CSRD 2024, ~€90/tCO2

- Verified metrics = higher bargaining power

- Poor traceability → discounting/switch risk

- Componenta: opportunity to monetize compliance

OEM tenders squeeze margins: OTIF ≥95%, defects <1%, EU carbon ≈€90/tCO2

OEMs buy via structured tenders/multi-year (3–5y) contracts, pressuring price and extending payment terms to 30–120 days. Tooling ($50k–$500k) and PPAP (4–12w) raise switching costs but dual sourcing caps single-supplier power; buyers demand OTIF ≥95% and defect <1%. ESG rules (CSRD 2024) and EU carbon ≈€90/tCO2 in 2024 increase procurement scrutiny; verified sustainability metrics improve negotiating leverage.

| Metric | 2024 Benchmark | Impact |

|---|---|---|

| Payment terms | 30–120 days | Cash stress |

| Tooling cost | $50k–$500k | High switching cost |

| OTIF / Defect | ≥95% / <1% | Retention/penalties |

| EU carbon price | ≈€90/tCO2 | ESG pricing pressure |

Full Version Awaits

Componenta Porter's Five Forces Analysis

This preview shows the exact Componenta Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or sample excerpts. The file is the full, professionally formatted document ready for download and use the moment you buy. You’ll get instant access to this identical deliverable with no further setup required.

A Must-Have Tool for Decision-Makers

Componenta faces moderate supplier power, niche buyer pockets, and steady threat from substitutes amid cyclical metal demand. Competitive rivalry is intense but tempered by specialized casting capabilities and service contracts. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Componenta’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated raw material sources

Cast iron production depends on pig iron, steel scrap and alloying elements often sourced from a concentrated pool of regional metals traders, giving suppliers elevated pricing power and reducing Componenta’s negotiating room. Supplier consolidation raises the risk of cost pass-through and supply tightness; long-term contracts mitigate volatility but commonly include indexation that shifts price risk to buyers. Componenta can reduce leverage by diversifying suppliers geographically and locking in multi-sourced frameworks.

Energy intensity and utilities leverage

Melting and heat treatment make energy a major cost driver for foundries; EU average industrial electricity was about €0.12/kWh in 2024 and EUA carbon allowances averaged near €90/tCO2, giving power and gas providers structural influence. Price spikes or carbon-linked surcharges can compress margins quickly. Demand-side management and renewable PPAs reduce exposure and improve sustainability credentials. Location near stable grids and active hedging practices temper supplier power.

Specialized consumables and tooling

Specialized consumables—foundry sand, binders/resins, refractory linings and precision machining tools—are sourced from niche suppliers, giving suppliers elevated leverage in 2024 as qualified alternatives remain limited. Switching costs arise from process recalibration and quality consistency requirements, with testing and validation often taking several months. Dual-qualifying consumables lowers dependence but requires capital for trials and certification; collaborative supplier development secures performance and can yield preferential terms.

Logistics and proximity constraints

Bulky inputs and JIT schedules give regional suppliers outsized leverage over lead times and freight costs; 2024 industry surveys report proximity ranks as a top-3 supplier advantage for 72% of manufacturers. Port congestion and tight trucking capacity (peak delays up to multi-day) amplify that power, while nearshoring and inventory buffers stabilize flow. Digital tracking in 2024 cut dispute resolution times materially.

- Regional suppliers: proximity advantage

- Port/truck delays: amplify supplier power

- Nearshoring/inventory: flow stability

- Digital tracking: visibility, faster disputes

ESG and compliance requirements

Supplier adherence to ISO 14001/45001 and EU CSRD-driven disclosure (phased from 2024) directly affects Componenta’s certifications and customer audits; non-compliant suppliers tighten the qualified pool and raise supplier bargaining power. Collaborative ESG programs and transparency platforms plus sharing EN 15804/ISO 14025-compliant lifecycle data (EPDs) expand the qualified supplier base and support Componenta’s sustainable manufacturing claims.

- ISO 14001/45001: compliance baseline

- CSRD (phased from 2024): increased disclosure pressure

- EN 15804/ISO 14025: lifecycle data standardization (EPDs)

- Joint ESG programs: reduce supplier concentration risk

Supplier concentration and EU energy costs strengthen pricing power; use PPAs, dual-qualify

Cast iron inputs and specialized consumables are concentrated, giving suppliers strong pricing power; EU industrial electricity ~€0.12/kWh and EUA ~€90/tCO2 in 2024 amplify energy supplier influence. Proximity, port/truck delays (72% cite proximity as top‑3 advantage) and JIT logistics raise lead‑time leverage. Diversification, dual‑qualification, renewable PPAs and ESG collaboration reduce supplier bargaining power.

| Category | 2024 data | Impact |

|---|---|---|

| Energy | €0.12/kWh; EUA €90/tCO2 | High cost volatility |

| Proximity/logistics | 72% proximity importance | Lead‑time leverage |

| Consumables | Limited qualified suppliers | Switching costs |

| Standards/ESG | CSRD phased 2024 | Supplier pool constrained |

What is included in the product

Tailored Porter's Five Forces analysis for Componenta that uncovers key drivers of competition, buyer and supplier power, and market entry risks; evaluates pricing influence and profitability pressures. Identifies disruptive forces, substitutes and strategic barriers protecting incumbents, formatted for easy inclusion in reports or investor decks.

Componenta Porter's Five Forces delivers a concise one-sheet with an editable radar chart to visualize competitive pressures instantly—perfect for fast strategic decisions and boardroom slides. Customize force levels, swap in your data, and export clean visuals without complex tools to relieve analysis bottlenecks.

Customers Bargaining Power

Large OEMs with scale

Vehicle, machinery and equipment OEMs buy in high volumes and negotiate aggressively, often via structured tenders and multi-year frameworks of 3–5 years. Their scale forces price compression and payment-term pressure, commonly extending terms from 30 to 120 days. Componenta must differentiate through quality, engineering partnerships and service to preserve margins rather than competing on price alone.

Engineering lock-in vs dual sourcing

Custom castings create engineering lock-in: tooling (often $50k–$500k per tool) plus process know-how and PPAP/FAI cycles (commonly 4–12 weeks) raise switching costs for OEMs. Many OEMs nonetheless mandate dual sourcing for resilience, capping pricing power for any single supplier. Maintaining second-source status requires consistent quality and delivery metrics (PPM targets under 100 and OTIF >95%). Value engineering—cost reduction and part consolidation—deepens customer stickiness.

Cyclical demand and price sensitivity

End markets for Componenta are cyclical, making buyers markedly more price sensitive in downturns and intensifying requests for index-linked contracts and raw-material surcharges during negotiations.

Componenta defends margins through flexible capacity, transparent cost breakdowns and pass-through clauses, while VAVE proposals reposition talks toward total cost of ownership rather than unit price.

Service level and delivery expectations

On-time delivery, short lead times and low defect rates (industry benchmark: 95% OTIF, defect rate <1% in 2024) are primary buyer metrics used to rank suppliers; poor scores trigger penalties or re-sourcing via performance scorecards. Advanced planning, quality systems and integrated logistics/EDI reduce buyer leverage by closing service gaps.

- OTIF ≥95%

- Defect rate <1%

- Scorecards → penalties/re-sourcing

- EDI + integrated logistics improve responsiveness

ESG and traceability demands

OEMs increasingly require carbon footprint data, recycled content and compliance proofs; EU CSRD came into force in 2024 and EU carbon prices averaged near €90/tCO2 in 2024, raising procurement ESG scrutiny. Suppliers with verified sustainability metrics gain negotiating room, while lack of traceability lets buyers push discounts or switch; Componenta’s sustainability focus can convert compliance into a premium.

- OEM ESG demands: CSRD 2024, ~€90/tCO2

- Verified metrics = higher bargaining power

- Poor traceability → discounting/switch risk

- Componenta: opportunity to monetize compliance

OEM tenders squeeze margins: OTIF ≥95%, defects <1%, EU carbon ≈€90/tCO2

OEMs buy via structured tenders/multi-year (3–5y) contracts, pressuring price and extending payment terms to 30–120 days. Tooling ($50k–$500k) and PPAP (4–12w) raise switching costs but dual sourcing caps single-supplier power; buyers demand OTIF ≥95% and defect <1%. ESG rules (CSRD 2024) and EU carbon ≈€90/tCO2 in 2024 increase procurement scrutiny; verified sustainability metrics improve negotiating leverage.

| Metric | 2024 Benchmark | Impact |

|---|---|---|

| Payment terms | 30–120 days | Cash stress |

| Tooling cost | $50k–$500k | High switching cost |

| OTIF / Defect | ≥95% / <1% | Retention/penalties |

| EU carbon price | ≈€90/tCO2 | ESG pricing pressure |

Full Version Awaits

Componenta Porter's Five Forces Analysis

This preview shows the exact Componenta Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or sample excerpts. The file is the full, professionally formatted document ready for download and use the moment you buy. You’ll get instant access to this identical deliverable with no further setup required.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Componenta faces moderate supplier power, niche buyer pockets, and steady threat from substitutes amid cyclical metal demand. Competitive rivalry is intense but tempered by specialized casting capabilities and service contracts. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Componenta’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated raw material sources

Cast iron production depends on pig iron, steel scrap and alloying elements often sourced from a concentrated pool of regional metals traders, giving suppliers elevated pricing power and reducing Componenta’s negotiating room. Supplier consolidation raises the risk of cost pass-through and supply tightness; long-term contracts mitigate volatility but commonly include indexation that shifts price risk to buyers. Componenta can reduce leverage by diversifying suppliers geographically and locking in multi-sourced frameworks.

Energy intensity and utilities leverage

Melting and heat treatment make energy a major cost driver for foundries; EU average industrial electricity was about €0.12/kWh in 2024 and EUA carbon allowances averaged near €90/tCO2, giving power and gas providers structural influence. Price spikes or carbon-linked surcharges can compress margins quickly. Demand-side management and renewable PPAs reduce exposure and improve sustainability credentials. Location near stable grids and active hedging practices temper supplier power.

Specialized consumables and tooling

Specialized consumables—foundry sand, binders/resins, refractory linings and precision machining tools—are sourced from niche suppliers, giving suppliers elevated leverage in 2024 as qualified alternatives remain limited. Switching costs arise from process recalibration and quality consistency requirements, with testing and validation often taking several months. Dual-qualifying consumables lowers dependence but requires capital for trials and certification; collaborative supplier development secures performance and can yield preferential terms.

Logistics and proximity constraints

Bulky inputs and JIT schedules give regional suppliers outsized leverage over lead times and freight costs; 2024 industry surveys report proximity ranks as a top-3 supplier advantage for 72% of manufacturers. Port congestion and tight trucking capacity (peak delays up to multi-day) amplify that power, while nearshoring and inventory buffers stabilize flow. Digital tracking in 2024 cut dispute resolution times materially.

- Regional suppliers: proximity advantage

- Port/truck delays: amplify supplier power

- Nearshoring/inventory: flow stability

- Digital tracking: visibility, faster disputes

ESG and compliance requirements

Supplier adherence to ISO 14001/45001 and EU CSRD-driven disclosure (phased from 2024) directly affects Componenta’s certifications and customer audits; non-compliant suppliers tighten the qualified pool and raise supplier bargaining power. Collaborative ESG programs and transparency platforms plus sharing EN 15804/ISO 14025-compliant lifecycle data (EPDs) expand the qualified supplier base and support Componenta’s sustainable manufacturing claims.

- ISO 14001/45001: compliance baseline

- CSRD (phased from 2024): increased disclosure pressure

- EN 15804/ISO 14025: lifecycle data standardization (EPDs)

- Joint ESG programs: reduce supplier concentration risk

Supplier concentration and EU energy costs strengthen pricing power; use PPAs, dual-qualify

Cast iron inputs and specialized consumables are concentrated, giving suppliers strong pricing power; EU industrial electricity ~€0.12/kWh and EUA ~€90/tCO2 in 2024 amplify energy supplier influence. Proximity, port/truck delays (72% cite proximity as top‑3 advantage) and JIT logistics raise lead‑time leverage. Diversification, dual‑qualification, renewable PPAs and ESG collaboration reduce supplier bargaining power.

| Category | 2024 data | Impact |

|---|---|---|

| Energy | €0.12/kWh; EUA €90/tCO2 | High cost volatility |

| Proximity/logistics | 72% proximity importance | Lead‑time leverage |

| Consumables | Limited qualified suppliers | Switching costs |

| Standards/ESG | CSRD phased 2024 | Supplier pool constrained |

What is included in the product

Tailored Porter's Five Forces analysis for Componenta that uncovers key drivers of competition, buyer and supplier power, and market entry risks; evaluates pricing influence and profitability pressures. Identifies disruptive forces, substitutes and strategic barriers protecting incumbents, formatted for easy inclusion in reports or investor decks.

Componenta Porter's Five Forces delivers a concise one-sheet with an editable radar chart to visualize competitive pressures instantly—perfect for fast strategic decisions and boardroom slides. Customize force levels, swap in your data, and export clean visuals without complex tools to relieve analysis bottlenecks.

Customers Bargaining Power

Large OEMs with scale

Vehicle, machinery and equipment OEMs buy in high volumes and negotiate aggressively, often via structured tenders and multi-year frameworks of 3–5 years. Their scale forces price compression and payment-term pressure, commonly extending terms from 30 to 120 days. Componenta must differentiate through quality, engineering partnerships and service to preserve margins rather than competing on price alone.

Engineering lock-in vs dual sourcing

Custom castings create engineering lock-in: tooling (often $50k–$500k per tool) plus process know-how and PPAP/FAI cycles (commonly 4–12 weeks) raise switching costs for OEMs. Many OEMs nonetheless mandate dual sourcing for resilience, capping pricing power for any single supplier. Maintaining second-source status requires consistent quality and delivery metrics (PPM targets under 100 and OTIF >95%). Value engineering—cost reduction and part consolidation—deepens customer stickiness.

Cyclical demand and price sensitivity

End markets for Componenta are cyclical, making buyers markedly more price sensitive in downturns and intensifying requests for index-linked contracts and raw-material surcharges during negotiations.

Componenta defends margins through flexible capacity, transparent cost breakdowns and pass-through clauses, while VAVE proposals reposition talks toward total cost of ownership rather than unit price.

Service level and delivery expectations

On-time delivery, short lead times and low defect rates (industry benchmark: 95% OTIF, defect rate <1% in 2024) are primary buyer metrics used to rank suppliers; poor scores trigger penalties or re-sourcing via performance scorecards. Advanced planning, quality systems and integrated logistics/EDI reduce buyer leverage by closing service gaps.

- OTIF ≥95%

- Defect rate <1%

- Scorecards → penalties/re-sourcing

- EDI + integrated logistics improve responsiveness

ESG and traceability demands

OEMs increasingly require carbon footprint data, recycled content and compliance proofs; EU CSRD came into force in 2024 and EU carbon prices averaged near €90/tCO2 in 2024, raising procurement ESG scrutiny. Suppliers with verified sustainability metrics gain negotiating room, while lack of traceability lets buyers push discounts or switch; Componenta’s sustainability focus can convert compliance into a premium.

- OEM ESG demands: CSRD 2024, ~€90/tCO2

- Verified metrics = higher bargaining power

- Poor traceability → discounting/switch risk

- Componenta: opportunity to monetize compliance

OEM tenders squeeze margins: OTIF ≥95%, defects <1%, EU carbon ≈€90/tCO2

OEMs buy via structured tenders/multi-year (3–5y) contracts, pressuring price and extending payment terms to 30–120 days. Tooling ($50k–$500k) and PPAP (4–12w) raise switching costs but dual sourcing caps single-supplier power; buyers demand OTIF ≥95% and defect <1%. ESG rules (CSRD 2024) and EU carbon ≈€90/tCO2 in 2024 increase procurement scrutiny; verified sustainability metrics improve negotiating leverage.

| Metric | 2024 Benchmark | Impact |

|---|---|---|

| Payment terms | 30–120 days | Cash stress |

| Tooling cost | $50k–$500k | High switching cost |

| OTIF / Defect | ≥95% / <1% | Retention/penalties |

| EU carbon price | ≈€90/tCO2 | ESG pricing pressure |

Full Version Awaits

Componenta Porter's Five Forces Analysis

This preview shows the exact Componenta Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or sample excerpts. The file is the full, professionally formatted document ready for download and use the moment you buy. You’ll get instant access to this identical deliverable with no further setup required.