CompoSecure Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

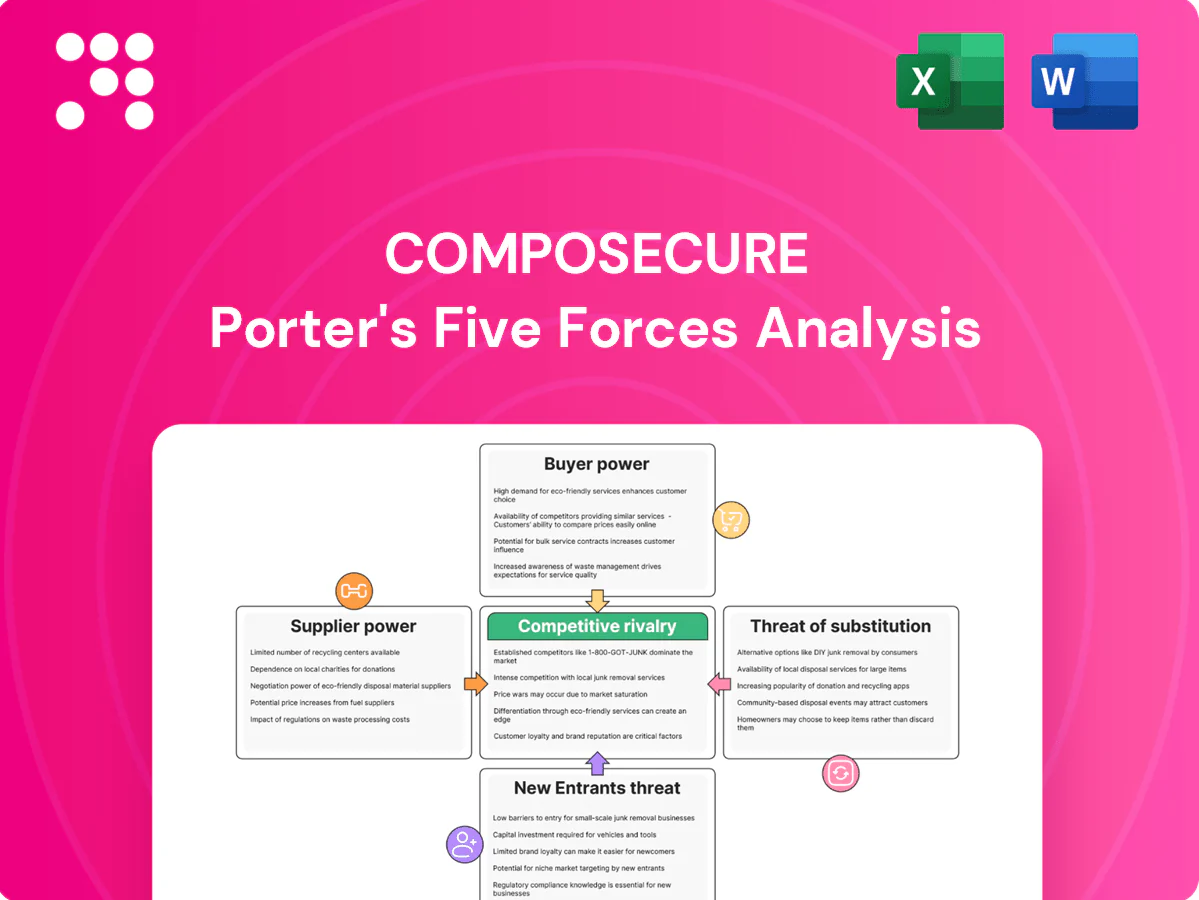

CompoSecure’s Porter's Five Forces snapshot highlights competitive rivalry, supplier and buyer power, entry barriers, and substitute threats, revealing where strategic leverage exists and risks may emerge. This brief only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable implications to inform investment or strategy decisions.

Suppliers Bargaining Power

Concentrated chip and module vendors

Secure element, EMV chip and NFC module supply is concentrated among a few certified vendors—notably NXP, Infineon and STMicroelectronics—giving them leverage on price and lead times. EMVCo and network qualifications typically take 6–12 months, raising switching costs and elongating qualification cycles. Past chip shortages (2021–23) showed how node constraints can ripple through card production schedules; CompoSecure must dual-source where possible to mitigate single-supplier risk.

Specialty metals and finishing inputs

Premium stainless, titanium, specialty coatings and laser/etch finishing are sourced from a narrow set of specialized mills and finishers, constraining CompoSecure’s supplier options and bargaining leverage. Commodity metal volatility pressured margins in 2024 (nickel soared roughly 15% YTD), forcing surcharges or pass-through pricing. Long-term contracts and hedging dampen price swings but limit short-term sourcing flexibility and upside capture.

Tooling, adhesives, and lamination tech

Proprietary adhesives, foils and lamination processes are central to durability and antenna performance, with major suppliers such as Henkel, 3M and H.B. Fuller dominating the space; the electronics adhesives segment grew at roughly a 5% CAGR to 2024. Suppliers providing custom formulations exert power via IP and exclusivity, while switching requires costly requalification and can depress yields. Co-development partnerships with suppliers align incentives and mitigate supplier leverage.

Security components and firmware

As of 2024 Secure OS, firmware and HSM inputs for authentication solutions must meet FIPS 140-3 and Common Criteria certifications, restricting supply; limited certified providers raise dependency and licensing costs. Firmware update cadence and support SLAs materially affect product roadmaps and time-to-market. Negotiating source-code escrow and long-term support contracts reduces supplier hold-up risk.

- Certs: FIPS 140-3, Common Criteria

- Dependency: few certified vendors

- Risk: firmware SLA delays

- Mitigation: escrow & long-term support

Logistics and compliance services

- Capacity constraint: >30% slot reduction in peak 2024

- Rush fees: up to 40% increase (2024)

- Certification delays: revenue lag of weeks

- Mitigation: multi-partner networks + early booking

Supplier power high: chip concentration, 6–12m quals, nickel +15%, slot loss ~30%, rush fees +40%

Supplier power is high: secure chips concentrated at NXP, Infineon, STMicroelectronics; EMV/Network quals take 6–12 months, raising switching costs. 2021–23 chip shortages disrupted output; commodity metal shocks (nickel +15% YTD 2024) compressed margins. Specialized adhesives, firmware certs (FIPS 140-3/Common Criteria) and logistics capacity (peak slot loss ~30%, rush fees up to +40% 2024) further strengthen suppliers.

| Metric | 2024 Value |

|---|---|

| Chip vendor concentration | Top 3 dominant |

| Qualification time | 6–12 months |

| Nickel price change | +15% YTD |

| Peak logistics slot loss | ~30% |

| Rush fee increase | up to +40% |

What is included in the product

Tailored Porter's Five Forces analysis for CompoSecure that uncovers key drivers of competition, supplier and buyer power, and entry and substitute risks specific to its composite materials and secure-ID markets. Highlights disruptive threats, pricing influence, and strategic barriers to help investors and managers assess competitive positioning and profitability.

One-sheet Porter's Five Forces for CompoSecure that pinpoints competitive pain points and relief strategies—easy to update, slide-ready, and decision-focused.

Customers Bargaining Power

Large issuers and networks drive terms

Top banks, card networks and scale fintechs (2024: top 10 issuers ~60% of global card volume) command negotiating power on price, SLA and exclusivity. RFP-driven procurement increases price pressure and feature demands. Winning marquee programs is strategic but often compresses gross margins 200–400 bps. Long tenures (typical 5–7 years) partially offset pressure via predictable volumes.

Customization demands and design control

Buyers demand bespoke metals, finishes and form factors tied to brand identity, pushing suppliers to absorb custom SKU complexity and tooling NRE typically ranging from $10,000 to $250,000 per part. Customers often attempt to shift these NRE and engineering costs onto suppliers, increasing margin pressure. Unique designs raise switching costs once tooling is established, locking suppliers and buyers into longer lifecycles. Clear change-order governance and scoped contracts protect scope and margin.

Alternatives across premium card tiers

Issuers can credibly threaten to shift volume to competitors or to high-end plastics with metallic effects, increasing negotiation leverage against CompoSecure on price and terms.

Widespread availability of near-equivalents amplifies buyer power, though CompoSecure’s proven durability and superior user experience reduce direct comparability for premium programs.

Documented activation and usage lifts tied to premium card programs serve as key proof points that justify pricing and mitigate customer bargaining pressure.

Integration and compliance requirements

Buyers require EMV, network certifications and personalization integration into existing workflows; as of 2024 PCI DSS v4.0 enforcement and EMV liability-shift legacy (2015) raise onboarding effort, shrinking the eligible vendor pool and tempering switching. Strong compliance track records often secure preferred-vendor status, while integration-support quality is a key differentiator in renewals.

- Compliance: PCI DSS v4.0 enforcement (as of 2024)

- Barrier: onboarding effort reduces vendor pool

- Retention: integration support drives renewals

Crypto and tech clients’ agility

Crypto platforms and tech firms pivot rapidly, often running multi-vendor pilots as product cycles shrink to quarters rather than years, raising price sensitivity and feature churn; the 2024 crypto market capitalization at roughly $1.2 trillion intensifies buyer leverage. Demonstrated security credentials and third-party audits materially reduce churn risk, while bundled offerings (card + auth) increase client stickiness and upsell potential.

- Vendor-switching: multi-vendor pilots common

- Cycle length: quarterly product iterations

- Security: audits curb churn

- Bundling: raises retention

Issuer concentration, compliance and metal SKUs squeeze card program margins in 2024

Top banks and top-10 issuers (~60% of global card volume in 2024) exert strong price/SLA leverage, compressing margins 200–400 bps on marquee programs. Custom metal SKUs drive NRE of $10,000–$250,000 and raise switching costs, while PCI DSS v4.0 (2024) and EMV requirements shrink the eligible vendor pool. Crypto market cap (~$1.2T in 2024) and multi-vendor pilots increase price sensitivity.

| Metric | 2024 Value |

|---|---|

| Top-10 issuers share | ~60% |

| Margin compression | 200–400 bps |

| Custom NRE | $10k–$250k |

| Crypto market cap | ~$1.2T |

Same Document Delivered

CompoSecure Porter's Five Forces Analysis

This preview shows the exact CompoSecure Porter’s Five Forces analysis you'll receive after purchase—fully written, professionally formatted, and ready to download. It is the complete, final document with no placeholders, mockups, or edits required. You’ll get instant access to this identical file upon payment.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

CompoSecure’s Porter's Five Forces snapshot highlights competitive rivalry, supplier and buyer power, entry barriers, and substitute threats, revealing where strategic leverage exists and risks may emerge. This brief only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable implications to inform investment or strategy decisions.

Suppliers Bargaining Power

Concentrated chip and module vendors

Secure element, EMV chip and NFC module supply is concentrated among a few certified vendors—notably NXP, Infineon and STMicroelectronics—giving them leverage on price and lead times. EMVCo and network qualifications typically take 6–12 months, raising switching costs and elongating qualification cycles. Past chip shortages (2021–23) showed how node constraints can ripple through card production schedules; CompoSecure must dual-source where possible to mitigate single-supplier risk.

Specialty metals and finishing inputs

Premium stainless, titanium, specialty coatings and laser/etch finishing are sourced from a narrow set of specialized mills and finishers, constraining CompoSecure’s supplier options and bargaining leverage. Commodity metal volatility pressured margins in 2024 (nickel soared roughly 15% YTD), forcing surcharges or pass-through pricing. Long-term contracts and hedging dampen price swings but limit short-term sourcing flexibility and upside capture.

Tooling, adhesives, and lamination tech

Proprietary adhesives, foils and lamination processes are central to durability and antenna performance, with major suppliers such as Henkel, 3M and H.B. Fuller dominating the space; the electronics adhesives segment grew at roughly a 5% CAGR to 2024. Suppliers providing custom formulations exert power via IP and exclusivity, while switching requires costly requalification and can depress yields. Co-development partnerships with suppliers align incentives and mitigate supplier leverage.

Security components and firmware

As of 2024 Secure OS, firmware and HSM inputs for authentication solutions must meet FIPS 140-3 and Common Criteria certifications, restricting supply; limited certified providers raise dependency and licensing costs. Firmware update cadence and support SLAs materially affect product roadmaps and time-to-market. Negotiating source-code escrow and long-term support contracts reduces supplier hold-up risk.

- Certs: FIPS 140-3, Common Criteria

- Dependency: few certified vendors

- Risk: firmware SLA delays

- Mitigation: escrow & long-term support

Logistics and compliance services

- Capacity constraint: >30% slot reduction in peak 2024

- Rush fees: up to 40% increase (2024)

- Certification delays: revenue lag of weeks

- Mitigation: multi-partner networks + early booking

Supplier power high: chip concentration, 6–12m quals, nickel +15%, slot loss ~30%, rush fees +40%

Supplier power is high: secure chips concentrated at NXP, Infineon, STMicroelectronics; EMV/Network quals take 6–12 months, raising switching costs. 2021–23 chip shortages disrupted output; commodity metal shocks (nickel +15% YTD 2024) compressed margins. Specialized adhesives, firmware certs (FIPS 140-3/Common Criteria) and logistics capacity (peak slot loss ~30%, rush fees up to +40% 2024) further strengthen suppliers.

| Metric | 2024 Value |

|---|---|

| Chip vendor concentration | Top 3 dominant |

| Qualification time | 6–12 months |

| Nickel price change | +15% YTD |

| Peak logistics slot loss | ~30% |

| Rush fee increase | up to +40% |

What is included in the product

Tailored Porter's Five Forces analysis for CompoSecure that uncovers key drivers of competition, supplier and buyer power, and entry and substitute risks specific to its composite materials and secure-ID markets. Highlights disruptive threats, pricing influence, and strategic barriers to help investors and managers assess competitive positioning and profitability.

One-sheet Porter's Five Forces for CompoSecure that pinpoints competitive pain points and relief strategies—easy to update, slide-ready, and decision-focused.

Customers Bargaining Power

Large issuers and networks drive terms

Top banks, card networks and scale fintechs (2024: top 10 issuers ~60% of global card volume) command negotiating power on price, SLA and exclusivity. RFP-driven procurement increases price pressure and feature demands. Winning marquee programs is strategic but often compresses gross margins 200–400 bps. Long tenures (typical 5–7 years) partially offset pressure via predictable volumes.

Customization demands and design control

Buyers demand bespoke metals, finishes and form factors tied to brand identity, pushing suppliers to absorb custom SKU complexity and tooling NRE typically ranging from $10,000 to $250,000 per part. Customers often attempt to shift these NRE and engineering costs onto suppliers, increasing margin pressure. Unique designs raise switching costs once tooling is established, locking suppliers and buyers into longer lifecycles. Clear change-order governance and scoped contracts protect scope and margin.

Alternatives across premium card tiers

Issuers can credibly threaten to shift volume to competitors or to high-end plastics with metallic effects, increasing negotiation leverage against CompoSecure on price and terms.

Widespread availability of near-equivalents amplifies buyer power, though CompoSecure’s proven durability and superior user experience reduce direct comparability for premium programs.

Documented activation and usage lifts tied to premium card programs serve as key proof points that justify pricing and mitigate customer bargaining pressure.

Integration and compliance requirements

Buyers require EMV, network certifications and personalization integration into existing workflows; as of 2024 PCI DSS v4.0 enforcement and EMV liability-shift legacy (2015) raise onboarding effort, shrinking the eligible vendor pool and tempering switching. Strong compliance track records often secure preferred-vendor status, while integration-support quality is a key differentiator in renewals.

- Compliance: PCI DSS v4.0 enforcement (as of 2024)

- Barrier: onboarding effort reduces vendor pool

- Retention: integration support drives renewals

Crypto and tech clients’ agility

Crypto platforms and tech firms pivot rapidly, often running multi-vendor pilots as product cycles shrink to quarters rather than years, raising price sensitivity and feature churn; the 2024 crypto market capitalization at roughly $1.2 trillion intensifies buyer leverage. Demonstrated security credentials and third-party audits materially reduce churn risk, while bundled offerings (card + auth) increase client stickiness and upsell potential.

- Vendor-switching: multi-vendor pilots common

- Cycle length: quarterly product iterations

- Security: audits curb churn

- Bundling: raises retention

Issuer concentration, compliance and metal SKUs squeeze card program margins in 2024

Top banks and top-10 issuers (~60% of global card volume in 2024) exert strong price/SLA leverage, compressing margins 200–400 bps on marquee programs. Custom metal SKUs drive NRE of $10,000–$250,000 and raise switching costs, while PCI DSS v4.0 (2024) and EMV requirements shrink the eligible vendor pool. Crypto market cap (~$1.2T in 2024) and multi-vendor pilots increase price sensitivity.

| Metric | 2024 Value |

|---|---|

| Top-10 issuers share | ~60% |

| Margin compression | 200–400 bps |

| Custom NRE | $10k–$250k |

| Crypto market cap | ~$1.2T |

Same Document Delivered

CompoSecure Porter's Five Forces Analysis

This preview shows the exact CompoSecure Porter’s Five Forces analysis you'll receive after purchase—fully written, professionally formatted, and ready to download. It is the complete, final document with no placeholders, mockups, or edits required. You’ll get instant access to this identical file upon payment.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

CompoSecure’s Porter's Five Forces snapshot highlights competitive rivalry, supplier and buyer power, entry barriers, and substitute threats, revealing where strategic leverage exists and risks may emerge. This brief only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable implications to inform investment or strategy decisions.

Suppliers Bargaining Power

Concentrated chip and module vendors

Secure element, EMV chip and NFC module supply is concentrated among a few certified vendors—notably NXP, Infineon and STMicroelectronics—giving them leverage on price and lead times. EMVCo and network qualifications typically take 6–12 months, raising switching costs and elongating qualification cycles. Past chip shortages (2021–23) showed how node constraints can ripple through card production schedules; CompoSecure must dual-source where possible to mitigate single-supplier risk.

Specialty metals and finishing inputs

Premium stainless, titanium, specialty coatings and laser/etch finishing are sourced from a narrow set of specialized mills and finishers, constraining CompoSecure’s supplier options and bargaining leverage. Commodity metal volatility pressured margins in 2024 (nickel soared roughly 15% YTD), forcing surcharges or pass-through pricing. Long-term contracts and hedging dampen price swings but limit short-term sourcing flexibility and upside capture.

Tooling, adhesives, and lamination tech

Proprietary adhesives, foils and lamination processes are central to durability and antenna performance, with major suppliers such as Henkel, 3M and H.B. Fuller dominating the space; the electronics adhesives segment grew at roughly a 5% CAGR to 2024. Suppliers providing custom formulations exert power via IP and exclusivity, while switching requires costly requalification and can depress yields. Co-development partnerships with suppliers align incentives and mitigate supplier leverage.

Security components and firmware

As of 2024 Secure OS, firmware and HSM inputs for authentication solutions must meet FIPS 140-3 and Common Criteria certifications, restricting supply; limited certified providers raise dependency and licensing costs. Firmware update cadence and support SLAs materially affect product roadmaps and time-to-market. Negotiating source-code escrow and long-term support contracts reduces supplier hold-up risk.

- Certs: FIPS 140-3, Common Criteria

- Dependency: few certified vendors

- Risk: firmware SLA delays

- Mitigation: escrow & long-term support

Logistics and compliance services

- Capacity constraint: >30% slot reduction in peak 2024

- Rush fees: up to 40% increase (2024)

- Certification delays: revenue lag of weeks

- Mitigation: multi-partner networks + early booking

Supplier power high: chip concentration, 6–12m quals, nickel +15%, slot loss ~30%, rush fees +40%

Supplier power is high: secure chips concentrated at NXP, Infineon, STMicroelectronics; EMV/Network quals take 6–12 months, raising switching costs. 2021–23 chip shortages disrupted output; commodity metal shocks (nickel +15% YTD 2024) compressed margins. Specialized adhesives, firmware certs (FIPS 140-3/Common Criteria) and logistics capacity (peak slot loss ~30%, rush fees up to +40% 2024) further strengthen suppliers.

| Metric | 2024 Value |

|---|---|

| Chip vendor concentration | Top 3 dominant |

| Qualification time | 6–12 months |

| Nickel price change | +15% YTD |

| Peak logistics slot loss | ~30% |

| Rush fee increase | up to +40% |

What is included in the product

Tailored Porter's Five Forces analysis for CompoSecure that uncovers key drivers of competition, supplier and buyer power, and entry and substitute risks specific to its composite materials and secure-ID markets. Highlights disruptive threats, pricing influence, and strategic barriers to help investors and managers assess competitive positioning and profitability.

One-sheet Porter's Five Forces for CompoSecure that pinpoints competitive pain points and relief strategies—easy to update, slide-ready, and decision-focused.

Customers Bargaining Power

Large issuers and networks drive terms

Top banks, card networks and scale fintechs (2024: top 10 issuers ~60% of global card volume) command negotiating power on price, SLA and exclusivity. RFP-driven procurement increases price pressure and feature demands. Winning marquee programs is strategic but often compresses gross margins 200–400 bps. Long tenures (typical 5–7 years) partially offset pressure via predictable volumes.

Customization demands and design control

Buyers demand bespoke metals, finishes and form factors tied to brand identity, pushing suppliers to absorb custom SKU complexity and tooling NRE typically ranging from $10,000 to $250,000 per part. Customers often attempt to shift these NRE and engineering costs onto suppliers, increasing margin pressure. Unique designs raise switching costs once tooling is established, locking suppliers and buyers into longer lifecycles. Clear change-order governance and scoped contracts protect scope and margin.

Alternatives across premium card tiers

Issuers can credibly threaten to shift volume to competitors or to high-end plastics with metallic effects, increasing negotiation leverage against CompoSecure on price and terms.

Widespread availability of near-equivalents amplifies buyer power, though CompoSecure’s proven durability and superior user experience reduce direct comparability for premium programs.

Documented activation and usage lifts tied to premium card programs serve as key proof points that justify pricing and mitigate customer bargaining pressure.

Integration and compliance requirements

Buyers require EMV, network certifications and personalization integration into existing workflows; as of 2024 PCI DSS v4.0 enforcement and EMV liability-shift legacy (2015) raise onboarding effort, shrinking the eligible vendor pool and tempering switching. Strong compliance track records often secure preferred-vendor status, while integration-support quality is a key differentiator in renewals.

- Compliance: PCI DSS v4.0 enforcement (as of 2024)

- Barrier: onboarding effort reduces vendor pool

- Retention: integration support drives renewals

Crypto and tech clients’ agility

Crypto platforms and tech firms pivot rapidly, often running multi-vendor pilots as product cycles shrink to quarters rather than years, raising price sensitivity and feature churn; the 2024 crypto market capitalization at roughly $1.2 trillion intensifies buyer leverage. Demonstrated security credentials and third-party audits materially reduce churn risk, while bundled offerings (card + auth) increase client stickiness and upsell potential.

- Vendor-switching: multi-vendor pilots common

- Cycle length: quarterly product iterations

- Security: audits curb churn

- Bundling: raises retention

Issuer concentration, compliance and metal SKUs squeeze card program margins in 2024

Top banks and top-10 issuers (~60% of global card volume in 2024) exert strong price/SLA leverage, compressing margins 200–400 bps on marquee programs. Custom metal SKUs drive NRE of $10,000–$250,000 and raise switching costs, while PCI DSS v4.0 (2024) and EMV requirements shrink the eligible vendor pool. Crypto market cap (~$1.2T in 2024) and multi-vendor pilots increase price sensitivity.

| Metric | 2024 Value |

|---|---|

| Top-10 issuers share | ~60% |

| Margin compression | 200–400 bps |

| Custom NRE | $10k–$250k |

| Crypto market cap | ~$1.2T |

Same Document Delivered

CompoSecure Porter's Five Forces Analysis

This preview shows the exact CompoSecure Porter’s Five Forces analysis you'll receive after purchase—fully written, professionally formatted, and ready to download. It is the complete, final document with no placeholders, mockups, or edits required. You’ll get instant access to this identical file upon payment.