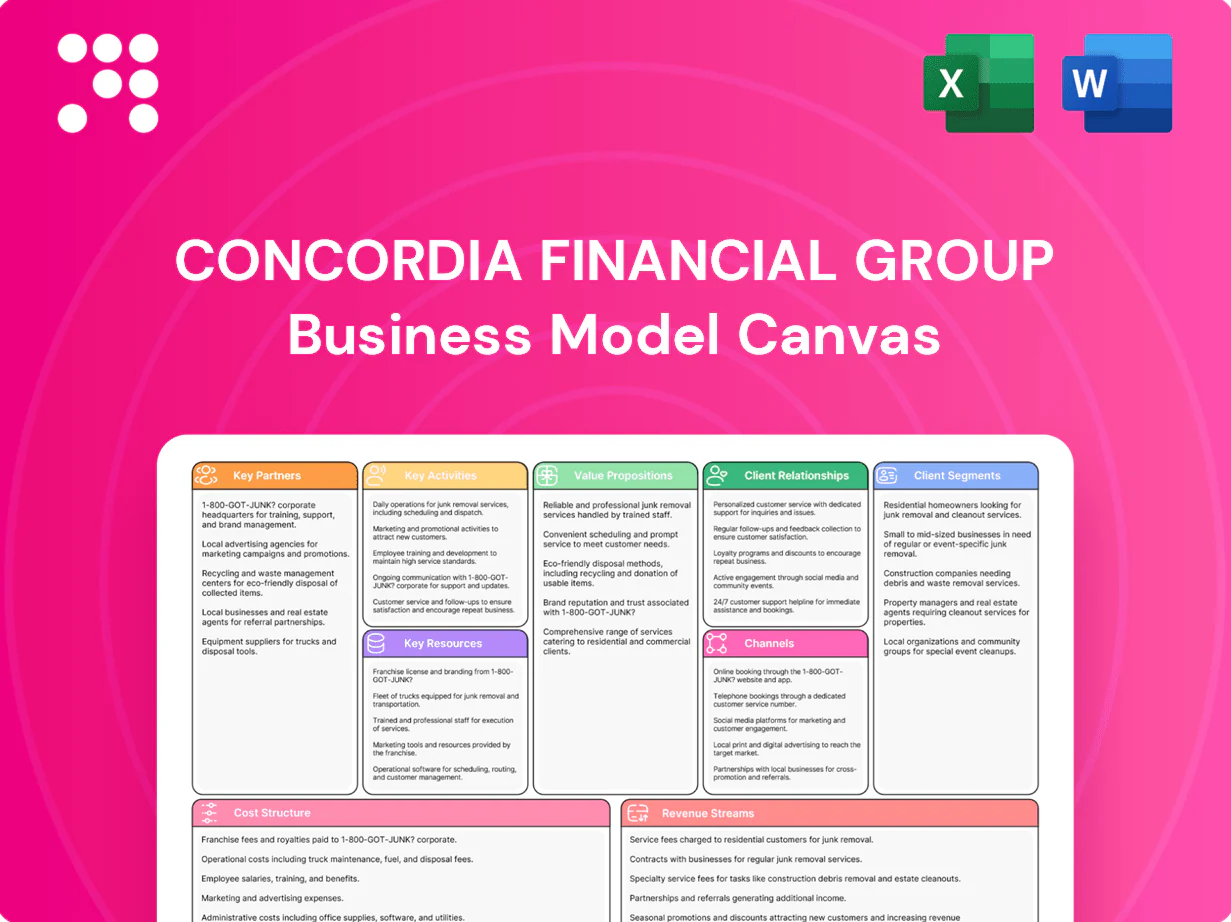

Concordia Financial Group Business Model Canvas

Business Model Canvas: Investor-Ready Blueprint for Strategic Growth and Revenue Mapping

Unlock the full strategic blueprint behind Concordia Financial Group with our Business Model Canvas—three to five clear sentences that map value propositions, customer segments, revenue streams and cost structure. This downloadable, editable canvas is perfect for investors, consultants, and founders seeking actionable, company-specific insights—purchase the full file to benchmark and implement proven strategies.

Partnerships

Global correspondent banks

Global correspondent banks enable FX, cross-border payments and trade finance settlements for Concordia’s international clients, linking to over 40 million SWIFT messages daily in 2024 and coverage across 200+ jurisdictions. They supply multicurrency liquidity and documentary services such as letters of credit and collections. They enhance risk sharing and harmonized compliance standards and support corporate treasury with efficient international rails and intraday liquidity management.

Card networks and payment processors

Card networks and processors power credit/debit issuance and merchant acquiring to expand acceptance and cut transaction friction for retail and SME clients; contactless penetration exceeded 70% in 2024 and networks now handle over 300 billion card transactions annually. Leveraging network security, tokenization, and centralized dispute management reduces fraud and chargebacks. Higher volumes translate to incremental fee-based income from interchange and processing fees, driving revenue growth.

Fintech and IT vendors

Partnerships with fintech and IT vendors accelerate digital onboarding via open banking APIs and analytics, improving mobile UX and fraud detection while boosting core-system reliability; ecosystem plays cut new-feature time-to-market by up to 40% and enable embedded finance rollouts.

Insurers and asset managers

Concordia partners with insurers and asset managers to offer bancassurance, investment trusts and discretionary solutions, broadening savings and protection shelves for individuals and SMEs while sharing distribution economics to enhance client outcomes.

- Expand bancassurance and discretionary product origination

- Broaden retail and SME protection/savings range

- Align distribution economics with advisory partners

- Diversify fee income via advisory and product origination

Local governments and business associations

Concordia Financial Group coordinates Kanto regional development and SME revitalization, leveraging public subsidies to de-risk projects and source quality borrowers across a 43 million-strong population; SMEs (>99% of firms, ~69% of employment) are core targets, supporting financial inclusion and strengthening Concordia’s community-focused brand.

- Coordinate subsidies & programs

- De-risk projects via public support

- Source quality SME borrowers

- Boost Kanto financial inclusion

Global partners power cross-border rails, 300B card txns and faster digital launches for Kanto SMEs

Concordia’s key partners—global correspondent banks, card networks, fintech vendors, insurers/asset managers and regional public agencies—provide cross-border rails (40M SWIFT msgs/day, 200+ jurisdictions in 2024), card reach (300B txns/yr; contactless >70% in 2024), faster digital launches (time-to-market -40%), bancassurance origination and Kanto SME channels (pop 43M; SMEs >99% firms, ~69% employment).

| Partner | Role | 2024 metric |

|---|---|---|

| Correspondent banks | FX, settlements | 40M SWIFT/day; 200+ juris |

| Card networks | Issuing/acquiring | 300B txns/yr; contactless >70% |

| Fintech vendors | APIs, onboarding | -40% feature TTM |

What is included in the product

A concise, pre-written Business Model Canvas for Concordia Financial Group detailing customer segments, value propositions, channels, revenue streams and key resources across the 9 BMC blocks, with linked SWOT and competitive-analysis insights to support presentations, funding discussions, and strategic decision-making.

High-level, shareable Business Model Canvas for Concordia Financial Group that saves hours of structuring by condensing strategy into a clean, editable one-page snapshot. Perfect for quick reviews, team collaboration, and fast executive deliverables.

Activities

Retail and corporate lending

Originate and manage mortgages, SME working capital and corporate loans with disciplined pricing and covenant monitoring to protect asset quality. Maintain borrower-level covenants and stress-test pricing to preserve NPLs. Balance portfolio across sectors and maturities via target limits and concentration caps. Align growth with capital and liquidity rules (Basel III CET1 min 4.5% plus buffers; LCR ≥ 100%).

Deposit gathering and cash management

Attract stable retail and corporate deposits to fund lending by offering transaction accounts, payroll services and liquidity solutions that increase account use and retention; optimize pricing and product features for stickiness (tiered yield, bundled cash management) and diversify wholesale and retail funding sources to enhance treasury stability and reduce reliance on short-term markets.

Risk, compliance, and credit underwriting

Maintain robust KYC/AML and regulatory reporting frameworks aligned with FATF standards and Basel III requirements (CET1 minimum 4.5% as of 2024), supported by strong internal controls and audit trails. Credit decisions combine scorecards with expert judgment to balance model efficiency and forward-looking risk views. NPL monitoring and provisioning are tracked to preserve capital resilience, with routine portfolio analytics. Conduct quarterly stress tests and scenario analysis to validate capital and liquidity buffers.

Digital banking and channel operations

Run mobile, internet, ATM and call center platforms seamlessly, targeting 99.9% uptime and SOC 2–grade cybersecurity; improve user journeys and NPS through continuous UX optimization. Enable self‑service onboarding, payments and investments to reduce friction and operational cost. Integrate unified data to personalize omni‑channel offers, supporting ~20% digital transaction growth in 2024.

- Platform uptime: 99.9%

- Cybersecurity: SOC 2/ISO focus

- Self‑service: onboarding/payments/investments

- Data: unified profiles for personalization

Wealth and FX solutions

Deliver investment trusts, insurance and tailored advisory to retail and HNW clients while providing FX, hedging and trade services to SMEs and corporates, leveraging global FX market liquidity (average daily turnover ~7.5 trillion USD per BIS 2022) to optimize execution and risk transfer.

- Retail & HNW: investment trusts, insurance, advisory

- SME & corporate: FX, hedging, trade services

- Revenue: fee income focus aligned with long-term financial goals

- Client education: risk management and diversification

Prudent lending, 99.9% uptime and CET1≥4.5%: resilient digital bank with FX hedging

Originate and manage mortgages, SME and corporate loans with covenant monitoring and stress-tested pricing to keep NPLs low; maintain CET1 ≥ 4.5% and LCR ≥ 100% (2024). Attract sticky retail/corporate deposits and diversify wholesale funding; digital transactions grew ~20% in 2024. Operate 99.9% uptime platforms with SOC 2 focus; offer wealth, insurance, FX and hedging tied to global FX liquidity (~7.5T USD/day, BIS 2022).

| Metric | 2024 Value |

|---|---|

| CET1 min | 4.5% |

| LCR | ≥100% |

| Platform uptime | 99.9% |

| Digital Tx growth | ~20% |

Delivered as Displayed

Business Model Canvas

The Concordia Financial Group Business Model Canvas you see here is the actual deliverable, not a mockup—this preview is a direct extract from the file you’ll receive after purchase. When you complete your order, you’ll get the same fully formatted document ready for download in Word and Excel. No surprises—what you preview is what you’ll own and can edit, present, or share.

Business Model Canvas: Investor-Ready Blueprint for Strategic Growth and Revenue Mapping

Unlock the full strategic blueprint behind Concordia Financial Group with our Business Model Canvas—three to five clear sentences that map value propositions, customer segments, revenue streams and cost structure. This downloadable, editable canvas is perfect for investors, consultants, and founders seeking actionable, company-specific insights—purchase the full file to benchmark and implement proven strategies.

Partnerships

Global correspondent banks

Global correspondent banks enable FX, cross-border payments and trade finance settlements for Concordia’s international clients, linking to over 40 million SWIFT messages daily in 2024 and coverage across 200+ jurisdictions. They supply multicurrency liquidity and documentary services such as letters of credit and collections. They enhance risk sharing and harmonized compliance standards and support corporate treasury with efficient international rails and intraday liquidity management.

Card networks and payment processors

Card networks and processors power credit/debit issuance and merchant acquiring to expand acceptance and cut transaction friction for retail and SME clients; contactless penetration exceeded 70% in 2024 and networks now handle over 300 billion card transactions annually. Leveraging network security, tokenization, and centralized dispute management reduces fraud and chargebacks. Higher volumes translate to incremental fee-based income from interchange and processing fees, driving revenue growth.

Fintech and IT vendors

Partnerships with fintech and IT vendors accelerate digital onboarding via open banking APIs and analytics, improving mobile UX and fraud detection while boosting core-system reliability; ecosystem plays cut new-feature time-to-market by up to 40% and enable embedded finance rollouts.

Insurers and asset managers

Concordia partners with insurers and asset managers to offer bancassurance, investment trusts and discretionary solutions, broadening savings and protection shelves for individuals and SMEs while sharing distribution economics to enhance client outcomes.

- Expand bancassurance and discretionary product origination

- Broaden retail and SME protection/savings range

- Align distribution economics with advisory partners

- Diversify fee income via advisory and product origination

Local governments and business associations

Concordia Financial Group coordinates Kanto regional development and SME revitalization, leveraging public subsidies to de-risk projects and source quality borrowers across a 43 million-strong population; SMEs (>99% of firms, ~69% of employment) are core targets, supporting financial inclusion and strengthening Concordia’s community-focused brand.

- Coordinate subsidies & programs

- De-risk projects via public support

- Source quality SME borrowers

- Boost Kanto financial inclusion

Global partners power cross-border rails, 300B card txns and faster digital launches for Kanto SMEs

Concordia’s key partners—global correspondent banks, card networks, fintech vendors, insurers/asset managers and regional public agencies—provide cross-border rails (40M SWIFT msgs/day, 200+ jurisdictions in 2024), card reach (300B txns/yr; contactless >70% in 2024), faster digital launches (time-to-market -40%), bancassurance origination and Kanto SME channels (pop 43M; SMEs >99% firms, ~69% employment).

| Partner | Role | 2024 metric |

|---|---|---|

| Correspondent banks | FX, settlements | 40M SWIFT/day; 200+ juris |

| Card networks | Issuing/acquiring | 300B txns/yr; contactless >70% |

| Fintech vendors | APIs, onboarding | -40% feature TTM |

What is included in the product

A concise, pre-written Business Model Canvas for Concordia Financial Group detailing customer segments, value propositions, channels, revenue streams and key resources across the 9 BMC blocks, with linked SWOT and competitive-analysis insights to support presentations, funding discussions, and strategic decision-making.

High-level, shareable Business Model Canvas for Concordia Financial Group that saves hours of structuring by condensing strategy into a clean, editable one-page snapshot. Perfect for quick reviews, team collaboration, and fast executive deliverables.

Activities

Retail and corporate lending

Originate and manage mortgages, SME working capital and corporate loans with disciplined pricing and covenant monitoring to protect asset quality. Maintain borrower-level covenants and stress-test pricing to preserve NPLs. Balance portfolio across sectors and maturities via target limits and concentration caps. Align growth with capital and liquidity rules (Basel III CET1 min 4.5% plus buffers; LCR ≥ 100%).

Deposit gathering and cash management

Attract stable retail and corporate deposits to fund lending by offering transaction accounts, payroll services and liquidity solutions that increase account use and retention; optimize pricing and product features for stickiness (tiered yield, bundled cash management) and diversify wholesale and retail funding sources to enhance treasury stability and reduce reliance on short-term markets.

Risk, compliance, and credit underwriting

Maintain robust KYC/AML and regulatory reporting frameworks aligned with FATF standards and Basel III requirements (CET1 minimum 4.5% as of 2024), supported by strong internal controls and audit trails. Credit decisions combine scorecards with expert judgment to balance model efficiency and forward-looking risk views. NPL monitoring and provisioning are tracked to preserve capital resilience, with routine portfolio analytics. Conduct quarterly stress tests and scenario analysis to validate capital and liquidity buffers.

Digital banking and channel operations

Run mobile, internet, ATM and call center platforms seamlessly, targeting 99.9% uptime and SOC 2–grade cybersecurity; improve user journeys and NPS through continuous UX optimization. Enable self‑service onboarding, payments and investments to reduce friction and operational cost. Integrate unified data to personalize omni‑channel offers, supporting ~20% digital transaction growth in 2024.

- Platform uptime: 99.9%

- Cybersecurity: SOC 2/ISO focus

- Self‑service: onboarding/payments/investments

- Data: unified profiles for personalization

Wealth and FX solutions

Deliver investment trusts, insurance and tailored advisory to retail and HNW clients while providing FX, hedging and trade services to SMEs and corporates, leveraging global FX market liquidity (average daily turnover ~7.5 trillion USD per BIS 2022) to optimize execution and risk transfer.

- Retail & HNW: investment trusts, insurance, advisory

- SME & corporate: FX, hedging, trade services

- Revenue: fee income focus aligned with long-term financial goals

- Client education: risk management and diversification

Prudent lending, 99.9% uptime and CET1≥4.5%: resilient digital bank with FX hedging

Originate and manage mortgages, SME and corporate loans with covenant monitoring and stress-tested pricing to keep NPLs low; maintain CET1 ≥ 4.5% and LCR ≥ 100% (2024). Attract sticky retail/corporate deposits and diversify wholesale funding; digital transactions grew ~20% in 2024. Operate 99.9% uptime platforms with SOC 2 focus; offer wealth, insurance, FX and hedging tied to global FX liquidity (~7.5T USD/day, BIS 2022).

| Metric | 2024 Value |

|---|---|

| CET1 min | 4.5% |

| LCR | ≥100% |

| Platform uptime | 99.9% |

| Digital Tx growth | ~20% |

Delivered as Displayed

Business Model Canvas

The Concordia Financial Group Business Model Canvas you see here is the actual deliverable, not a mockup—this preview is a direct extract from the file you’ll receive after purchase. When you complete your order, you’ll get the same fully formatted document ready for download in Word and Excel. No surprises—what you preview is what you’ll own and can edit, present, or share.

Description

Business Model Canvas: Investor-Ready Blueprint for Strategic Growth and Revenue Mapping

Unlock the full strategic blueprint behind Concordia Financial Group with our Business Model Canvas—three to five clear sentences that map value propositions, customer segments, revenue streams and cost structure. This downloadable, editable canvas is perfect for investors, consultants, and founders seeking actionable, company-specific insights—purchase the full file to benchmark and implement proven strategies.

Partnerships

Global correspondent banks

Global correspondent banks enable FX, cross-border payments and trade finance settlements for Concordia’s international clients, linking to over 40 million SWIFT messages daily in 2024 and coverage across 200+ jurisdictions. They supply multicurrency liquidity and documentary services such as letters of credit and collections. They enhance risk sharing and harmonized compliance standards and support corporate treasury with efficient international rails and intraday liquidity management.

Card networks and payment processors

Card networks and processors power credit/debit issuance and merchant acquiring to expand acceptance and cut transaction friction for retail and SME clients; contactless penetration exceeded 70% in 2024 and networks now handle over 300 billion card transactions annually. Leveraging network security, tokenization, and centralized dispute management reduces fraud and chargebacks. Higher volumes translate to incremental fee-based income from interchange and processing fees, driving revenue growth.

Fintech and IT vendors

Partnerships with fintech and IT vendors accelerate digital onboarding via open banking APIs and analytics, improving mobile UX and fraud detection while boosting core-system reliability; ecosystem plays cut new-feature time-to-market by up to 40% and enable embedded finance rollouts.

Insurers and asset managers

Concordia partners with insurers and asset managers to offer bancassurance, investment trusts and discretionary solutions, broadening savings and protection shelves for individuals and SMEs while sharing distribution economics to enhance client outcomes.

- Expand bancassurance and discretionary product origination

- Broaden retail and SME protection/savings range

- Align distribution economics with advisory partners

- Diversify fee income via advisory and product origination

Local governments and business associations

Concordia Financial Group coordinates Kanto regional development and SME revitalization, leveraging public subsidies to de-risk projects and source quality borrowers across a 43 million-strong population; SMEs (>99% of firms, ~69% of employment) are core targets, supporting financial inclusion and strengthening Concordia’s community-focused brand.

- Coordinate subsidies & programs

- De-risk projects via public support

- Source quality SME borrowers

- Boost Kanto financial inclusion

Global partners power cross-border rails, 300B card txns and faster digital launches for Kanto SMEs

Concordia’s key partners—global correspondent banks, card networks, fintech vendors, insurers/asset managers and regional public agencies—provide cross-border rails (40M SWIFT msgs/day, 200+ jurisdictions in 2024), card reach (300B txns/yr; contactless >70% in 2024), faster digital launches (time-to-market -40%), bancassurance origination and Kanto SME channels (pop 43M; SMEs >99% firms, ~69% employment).

| Partner | Role | 2024 metric |

|---|---|---|

| Correspondent banks | FX, settlements | 40M SWIFT/day; 200+ juris |

| Card networks | Issuing/acquiring | 300B txns/yr; contactless >70% |

| Fintech vendors | APIs, onboarding | -40% feature TTM |

What is included in the product

A concise, pre-written Business Model Canvas for Concordia Financial Group detailing customer segments, value propositions, channels, revenue streams and key resources across the 9 BMC blocks, with linked SWOT and competitive-analysis insights to support presentations, funding discussions, and strategic decision-making.

High-level, shareable Business Model Canvas for Concordia Financial Group that saves hours of structuring by condensing strategy into a clean, editable one-page snapshot. Perfect for quick reviews, team collaboration, and fast executive deliverables.

Activities

Retail and corporate lending

Originate and manage mortgages, SME working capital and corporate loans with disciplined pricing and covenant monitoring to protect asset quality. Maintain borrower-level covenants and stress-test pricing to preserve NPLs. Balance portfolio across sectors and maturities via target limits and concentration caps. Align growth with capital and liquidity rules (Basel III CET1 min 4.5% plus buffers; LCR ≥ 100%).

Deposit gathering and cash management

Attract stable retail and corporate deposits to fund lending by offering transaction accounts, payroll services and liquidity solutions that increase account use and retention; optimize pricing and product features for stickiness (tiered yield, bundled cash management) and diversify wholesale and retail funding sources to enhance treasury stability and reduce reliance on short-term markets.

Risk, compliance, and credit underwriting

Maintain robust KYC/AML and regulatory reporting frameworks aligned with FATF standards and Basel III requirements (CET1 minimum 4.5% as of 2024), supported by strong internal controls and audit trails. Credit decisions combine scorecards with expert judgment to balance model efficiency and forward-looking risk views. NPL monitoring and provisioning are tracked to preserve capital resilience, with routine portfolio analytics. Conduct quarterly stress tests and scenario analysis to validate capital and liquidity buffers.

Digital banking and channel operations

Run mobile, internet, ATM and call center platforms seamlessly, targeting 99.9% uptime and SOC 2–grade cybersecurity; improve user journeys and NPS through continuous UX optimization. Enable self‑service onboarding, payments and investments to reduce friction and operational cost. Integrate unified data to personalize omni‑channel offers, supporting ~20% digital transaction growth in 2024.

- Platform uptime: 99.9%

- Cybersecurity: SOC 2/ISO focus

- Self‑service: onboarding/payments/investments

- Data: unified profiles for personalization

Wealth and FX solutions

Deliver investment trusts, insurance and tailored advisory to retail and HNW clients while providing FX, hedging and trade services to SMEs and corporates, leveraging global FX market liquidity (average daily turnover ~7.5 trillion USD per BIS 2022) to optimize execution and risk transfer.

- Retail & HNW: investment trusts, insurance, advisory

- SME & corporate: FX, hedging, trade services

- Revenue: fee income focus aligned with long-term financial goals

- Client education: risk management and diversification

Prudent lending, 99.9% uptime and CET1≥4.5%: resilient digital bank with FX hedging

Originate and manage mortgages, SME and corporate loans with covenant monitoring and stress-tested pricing to keep NPLs low; maintain CET1 ≥ 4.5% and LCR ≥ 100% (2024). Attract sticky retail/corporate deposits and diversify wholesale funding; digital transactions grew ~20% in 2024. Operate 99.9% uptime platforms with SOC 2 focus; offer wealth, insurance, FX and hedging tied to global FX liquidity (~7.5T USD/day, BIS 2022).

| Metric | 2024 Value |

|---|---|

| CET1 min | 4.5% |

| LCR | ≥100% |

| Platform uptime | 99.9% |

| Digital Tx growth | ~20% |

Delivered as Displayed

Business Model Canvas

The Concordia Financial Group Business Model Canvas you see here is the actual deliverable, not a mockup—this preview is a direct extract from the file you’ll receive after purchase. When you complete your order, you’ll get the same fully formatted document ready for download in Word and Excel. No surprises—what you preview is what you’ll own and can edit, present, or share.