Consolidated Edison Boston Consulting Group Matrix

See the Bigger Picture

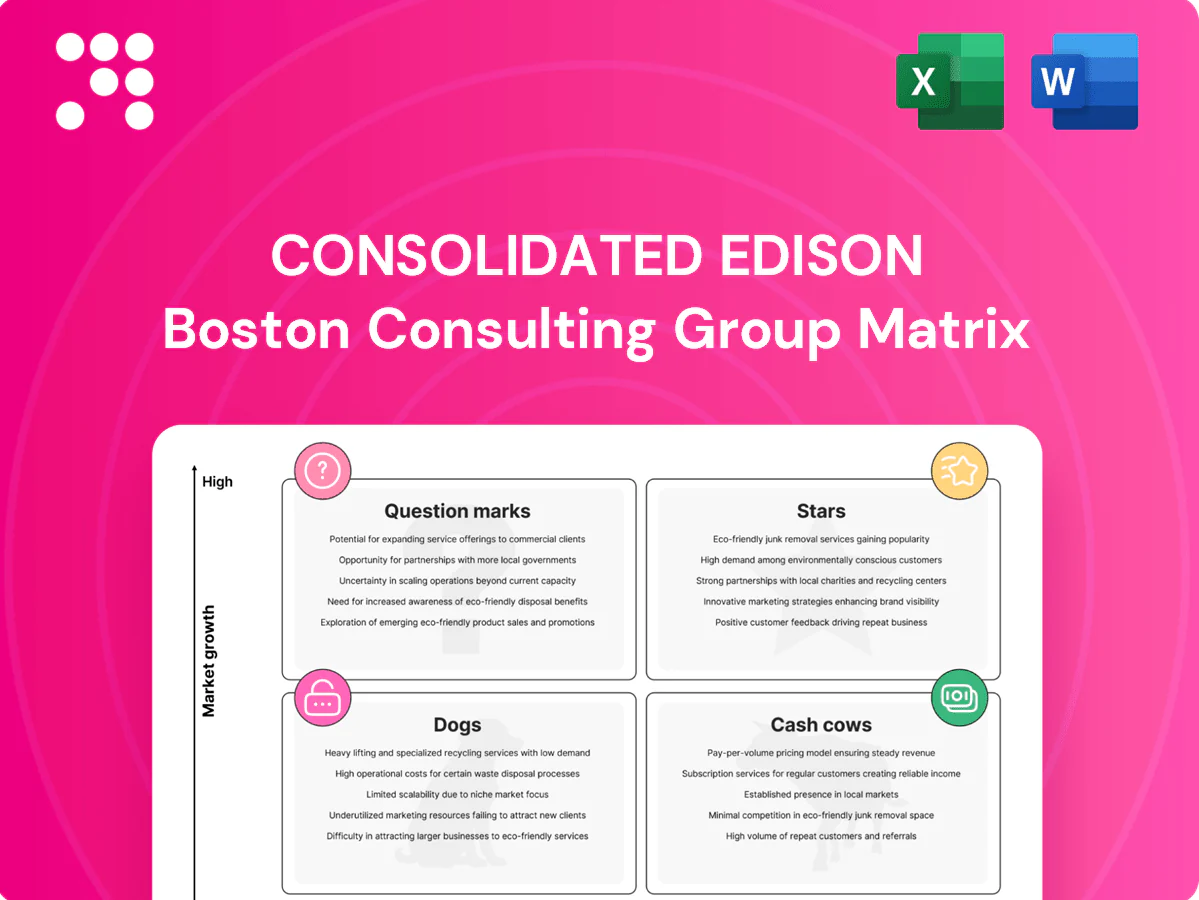

Consolidated Edison’s BCG Matrix preview shows which business lines are steady cash cows and which could become future stars—or costly dogs you’ll want to divest. Want the full map with quadrant placements, data-backed recommendations, and a clear capital-allocation roadmap? Purchase the complete BCG Matrix for a ready-to-use Word report and Excel summary that lets you act fast and present with confidence.

Stars

NYC electric grid modernization & transmission buildout

Load growth from electrification and data centers is material in NYC as New York mandates 70% renewable electricity by 2030 and 100% zero‑emission by 2040 under the CLCPA, driving sustained demand. Con Edison, serving about 3.5 million electric customers, needs urban wires upgrades and new transmission to meet capacity and reliability needs; transmission assets expand the rate base quickly. High market share and regulatory support create a strong growth tailwind; continued investment locks leadership before demand curves plateau.

Utility-scale and bulk battery storage enablement

Storage is emerging as the new peaker in New York’s Climate Leadership and Community Protection Act, which mandates 70% renewable electricity by 2030 and 100% zero‑emission electricity by 2040. Con Edison’s utility‑owned pilots and favorable siting/interconnection access give it a running start in a fast‑growing storage market. These projects absorb capital today but reinforce the company as a reliability backbone. As penetration rises, storage can convert to stable, regulated earnings.

Offshore wind interconnections and grid readiness

New York targets 9 GW of offshore wind by 2035, creating urgent need for sturdy onshore landing spots. Con Edison’s territory serves roughly 10 million people and dense urban load, making its circuits a strategic prize. Owning interconnection and reinforcement work centralizes project control and leverages regulated recovery mechanisms. That requires heavy near-term capex but supports durable, tariff-backed returns.

Advanced distribution automation and DER orchestration

Advanced distribution automation and DER orchestration address rising rooftop solar, batteries and EVs—EVs reached about 14% global sales in 2023—requiring sensors, automation and control software to keep the grid balanced; as DER penetration grows, Con Edison’s regulated wires monopoly can scale these services, retain share and move toward Cash Cow status.

- Market growth: rising DER adoption drives software/automation demand

- Monopoly edge: regulated wires enable capture of grid-edge services

- Strategy: defend share, scale with DER curve, monetize via ratebase

Public and fleet EV charging enablement

Public and fleet EV charging is a Star for Con Edison: NYC fleets are rapidly electrifying and curbside charging demand is intense; Con Edison serves about 3.5 million customers and its make-ready, interconnection, and targeted owns/ops positioning captures a fast-growth niche. Capex-heavy but central strategically; winning early secures recurring revenue streams and long-tail service demand. US public charging surpassed roughly 150,000 connectors in 2024, underscoring market scale.

- Role: make-ready, interconnection, owns/ops

- Scale: ~3.5M customers (Con Edison)

- Market size: ~150,000 public connectors (2024)

- Tradeoff: high capex vs long-term recurring revenue

Regulated utility: EV charging, storage, 9GW offshore build

Con Edison Stars (EV charging, storage, offshore wind interconnects, DER ops) show high growth with heavy near‑term capex but regulated/tariffed returns as NYC load and CLCPA targets drive demand; ConEd serves ~3.5M customers, NY 9GW offshore by 2035, US public chargers ~150,000 (2024).

| Opportunity | 2024 metric | Implication |

|---|---|---|

| Customers | ~3.5M | Ratebase growth |

| Offshore | 9GW by 2035 | Interconnect capex |

| Public chargers | ~150,000 | Fast EV demand |

What is included in the product

ConEdison BCG Matrix: maps Stars, Cash Cows, Question Marks, Dogs with clear invest/hold/divest guidance and trend context.

One-page Consolidated Edison BCG Matrix highlighting underperformers and stars to simplify capital allocation decisions.

Cash Cows

Regulated electric distribution (NYC & Westchester)

Regulated electric distribution in NYC & Westchester is a baked-in high-share franchise serving roughly 3.5 million customers, with a regulated rate base near $20 billion in 2024. Growth is moderate but predictable; regulation supports strong margins and stable cash flow that fund corporate investments. Lower promotional spend and steady annual capex (around $1.5B) preserve reliability and print the dollars that underwrite ConEdison's strategic bets.

In-service transmission assets (existing rate base)

In-service transmission assets are already built and earning, forming Con Edison's classic utility annuity with a regulated rate base of roughly $34 billion (2024), delivering predictable cash and ROEs set by state commissions.

Market growth is slower than the new-build grid wave, but steady: transmission reliability investments sustain stable margins and cash flow, supporting the companys dividend and credit profile.

Incremental upgrades and targeted efficiency projects lift throughput and cash generation—milk the assets while allocating capex toward the next growth segment.

Regulated gas distribution (near-term)

Regulated gas distribution still throws off reliable cash in a mature market, driven by base rates and utility service obligations that sustain near-term cash flow. Policy headwinds on decarbonization and methane rules create pressure, so keeping infrastructure tight and leaks below regulatory targets is critical to preserve margin. Use the steady proceeds to pivot capital toward electric growth and grid modernization.

Customer delivery charges and fixed fees

Urban density yields scale: Consolidated Edison serves about 3.5 million electric and 1.1 million gas customers (≈4.6 million meters in 2024), producing steady billed revenue that is low-growth but highly predictable.

Not flashy, this cash cow needs minimal promotion—focus is operational excellence, reliability, and regulated rate recovery as a quiet engine-room funding strategy.

- High meter density: ≈4.6M customers (2024)

- Stable cash flow: regulated billing predictability

- Low marketing, high O&M focus

Energy efficiency program administration

Energy efficiency program administration at Consolidated Edison functions as a cash cow: admin fees and cost recovery remained stable and low-risk in 2024, typically under 6% of program budgets per NYPSC filings, while annual portfolio spend in New York exceeds $1B, giving scale despite modest growth.

Tight execution boosts throughput and cash flow—focus on efficiency, compliance, and timely cost recovery keeps margins predictable.

- Admin fees: low-risk, ~<6% (2024 NYPSC)

- Scale: NY portfolio >$1B (2024)

- Strategy: efficient ops, strict compliance, prompt payment

Regulated NYC power: stable cash flow from ≈3.5M electric, ≈1.1M gas

Regulated NYC electric and gas distribution (~3.5M electric, 1.1M gas customers; ≈4.6M meters in 2024) deliver predictable, high-margin cash flow funding growth bets. In-service transmission and distribution assets (regulated rate base ≈$20B electric, ≈$34B transmission, 2024) yield stable returns; steady annual capex ≈$1.5B preserves reliability. Energy-efficiency admin fees <6% with NY portfolio >$1B bolster low-risk cash generation.

| Metric | 2024 |

|---|---|

| Electric customers | ≈3.5M |

| Gas customers | ≈1.1M |

| Meters | ≈4.6M |

| Electric rate base | ≈$20B |

| Transmission rate base | ≈$34B |

| Annual capex | ≈$1.5B |

| EE admin fees | <6% |

| NY EE portfolio | >$1B |

What You’re Viewing Is Included

Consolidated Edison BCG Matrix

The Consolidated Edison BCG Matrix you’re previewing here is the exact same file you’ll receive after purchase—no watermarks, no placeholders. It’s a fully formatted, strategy-ready report built for clear portfolio decisions and stakeholder presentations. Once you buy, the final document is immediately downloadable and editable for your team. Trusted analysis, no surprises—just plug-and-play clarity.

See the Bigger Picture

Consolidated Edison’s BCG Matrix preview shows which business lines are steady cash cows and which could become future stars—or costly dogs you’ll want to divest. Want the full map with quadrant placements, data-backed recommendations, and a clear capital-allocation roadmap? Purchase the complete BCG Matrix for a ready-to-use Word report and Excel summary that lets you act fast and present with confidence.

Stars

NYC electric grid modernization & transmission buildout

Load growth from electrification and data centers is material in NYC as New York mandates 70% renewable electricity by 2030 and 100% zero‑emission by 2040 under the CLCPA, driving sustained demand. Con Edison, serving about 3.5 million electric customers, needs urban wires upgrades and new transmission to meet capacity and reliability needs; transmission assets expand the rate base quickly. High market share and regulatory support create a strong growth tailwind; continued investment locks leadership before demand curves plateau.

Utility-scale and bulk battery storage enablement

Storage is emerging as the new peaker in New York’s Climate Leadership and Community Protection Act, which mandates 70% renewable electricity by 2030 and 100% zero‑emission electricity by 2040. Con Edison’s utility‑owned pilots and favorable siting/interconnection access give it a running start in a fast‑growing storage market. These projects absorb capital today but reinforce the company as a reliability backbone. As penetration rises, storage can convert to stable, regulated earnings.

Offshore wind interconnections and grid readiness

New York targets 9 GW of offshore wind by 2035, creating urgent need for sturdy onshore landing spots. Con Edison’s territory serves roughly 10 million people and dense urban load, making its circuits a strategic prize. Owning interconnection and reinforcement work centralizes project control and leverages regulated recovery mechanisms. That requires heavy near-term capex but supports durable, tariff-backed returns.

Advanced distribution automation and DER orchestration

Advanced distribution automation and DER orchestration address rising rooftop solar, batteries and EVs—EVs reached about 14% global sales in 2023—requiring sensors, automation and control software to keep the grid balanced; as DER penetration grows, Con Edison’s regulated wires monopoly can scale these services, retain share and move toward Cash Cow status.

- Market growth: rising DER adoption drives software/automation demand

- Monopoly edge: regulated wires enable capture of grid-edge services

- Strategy: defend share, scale with DER curve, monetize via ratebase

Public and fleet EV charging enablement

Public and fleet EV charging is a Star for Con Edison: NYC fleets are rapidly electrifying and curbside charging demand is intense; Con Edison serves about 3.5 million customers and its make-ready, interconnection, and targeted owns/ops positioning captures a fast-growth niche. Capex-heavy but central strategically; winning early secures recurring revenue streams and long-tail service demand. US public charging surpassed roughly 150,000 connectors in 2024, underscoring market scale.

- Role: make-ready, interconnection, owns/ops

- Scale: ~3.5M customers (Con Edison)

- Market size: ~150,000 public connectors (2024)

- Tradeoff: high capex vs long-term recurring revenue

Regulated utility: EV charging, storage, 9GW offshore build

Con Edison Stars (EV charging, storage, offshore wind interconnects, DER ops) show high growth with heavy near‑term capex but regulated/tariffed returns as NYC load and CLCPA targets drive demand; ConEd serves ~3.5M customers, NY 9GW offshore by 2035, US public chargers ~150,000 (2024).

| Opportunity | 2024 metric | Implication |

|---|---|---|

| Customers | ~3.5M | Ratebase growth |

| Offshore | 9GW by 2035 | Interconnect capex |

| Public chargers | ~150,000 | Fast EV demand |

What is included in the product

ConEdison BCG Matrix: maps Stars, Cash Cows, Question Marks, Dogs with clear invest/hold/divest guidance and trend context.

One-page Consolidated Edison BCG Matrix highlighting underperformers and stars to simplify capital allocation decisions.

Cash Cows

Regulated electric distribution (NYC & Westchester)

Regulated electric distribution in NYC & Westchester is a baked-in high-share franchise serving roughly 3.5 million customers, with a regulated rate base near $20 billion in 2024. Growth is moderate but predictable; regulation supports strong margins and stable cash flow that fund corporate investments. Lower promotional spend and steady annual capex (around $1.5B) preserve reliability and print the dollars that underwrite ConEdison's strategic bets.

In-service transmission assets (existing rate base)

In-service transmission assets are already built and earning, forming Con Edison's classic utility annuity with a regulated rate base of roughly $34 billion (2024), delivering predictable cash and ROEs set by state commissions.

Market growth is slower than the new-build grid wave, but steady: transmission reliability investments sustain stable margins and cash flow, supporting the companys dividend and credit profile.

Incremental upgrades and targeted efficiency projects lift throughput and cash generation—milk the assets while allocating capex toward the next growth segment.

Regulated gas distribution (near-term)

Regulated gas distribution still throws off reliable cash in a mature market, driven by base rates and utility service obligations that sustain near-term cash flow. Policy headwinds on decarbonization and methane rules create pressure, so keeping infrastructure tight and leaks below regulatory targets is critical to preserve margin. Use the steady proceeds to pivot capital toward electric growth and grid modernization.

Customer delivery charges and fixed fees

Urban density yields scale: Consolidated Edison serves about 3.5 million electric and 1.1 million gas customers (≈4.6 million meters in 2024), producing steady billed revenue that is low-growth but highly predictable.

Not flashy, this cash cow needs minimal promotion—focus is operational excellence, reliability, and regulated rate recovery as a quiet engine-room funding strategy.

- High meter density: ≈4.6M customers (2024)

- Stable cash flow: regulated billing predictability

- Low marketing, high O&M focus

Energy efficiency program administration

Energy efficiency program administration at Consolidated Edison functions as a cash cow: admin fees and cost recovery remained stable and low-risk in 2024, typically under 6% of program budgets per NYPSC filings, while annual portfolio spend in New York exceeds $1B, giving scale despite modest growth.

Tight execution boosts throughput and cash flow—focus on efficiency, compliance, and timely cost recovery keeps margins predictable.

- Admin fees: low-risk, ~<6% (2024 NYPSC)

- Scale: NY portfolio >$1B (2024)

- Strategy: efficient ops, strict compliance, prompt payment

Regulated NYC power: stable cash flow from ≈3.5M electric, ≈1.1M gas

Regulated NYC electric and gas distribution (~3.5M electric, 1.1M gas customers; ≈4.6M meters in 2024) deliver predictable, high-margin cash flow funding growth bets. In-service transmission and distribution assets (regulated rate base ≈$20B electric, ≈$34B transmission, 2024) yield stable returns; steady annual capex ≈$1.5B preserves reliability. Energy-efficiency admin fees <6% with NY portfolio >$1B bolster low-risk cash generation.

| Metric | 2024 |

|---|---|

| Electric customers | ≈3.5M |

| Gas customers | ≈1.1M |

| Meters | ≈4.6M |

| Electric rate base | ≈$20B |

| Transmission rate base | ≈$34B |

| Annual capex | ≈$1.5B |

| EE admin fees | <6% |

| NY EE portfolio | >$1B |

What You’re Viewing Is Included

Consolidated Edison BCG Matrix

The Consolidated Edison BCG Matrix you’re previewing here is the exact same file you’ll receive after purchase—no watermarks, no placeholders. It’s a fully formatted, strategy-ready report built for clear portfolio decisions and stakeholder presentations. Once you buy, the final document is immediately downloadable and editable for your team. Trusted analysis, no surprises—just plug-and-play clarity.

Original: $10.00

-65%$10.00

$3.50Description

See the Bigger Picture

Consolidated Edison’s BCG Matrix preview shows which business lines are steady cash cows and which could become future stars—or costly dogs you’ll want to divest. Want the full map with quadrant placements, data-backed recommendations, and a clear capital-allocation roadmap? Purchase the complete BCG Matrix for a ready-to-use Word report and Excel summary that lets you act fast and present with confidence.

Stars

NYC electric grid modernization & transmission buildout

Load growth from electrification and data centers is material in NYC as New York mandates 70% renewable electricity by 2030 and 100% zero‑emission by 2040 under the CLCPA, driving sustained demand. Con Edison, serving about 3.5 million electric customers, needs urban wires upgrades and new transmission to meet capacity and reliability needs; transmission assets expand the rate base quickly. High market share and regulatory support create a strong growth tailwind; continued investment locks leadership before demand curves plateau.

Utility-scale and bulk battery storage enablement

Storage is emerging as the new peaker in New York’s Climate Leadership and Community Protection Act, which mandates 70% renewable electricity by 2030 and 100% zero‑emission electricity by 2040. Con Edison’s utility‑owned pilots and favorable siting/interconnection access give it a running start in a fast‑growing storage market. These projects absorb capital today but reinforce the company as a reliability backbone. As penetration rises, storage can convert to stable, regulated earnings.

Offshore wind interconnections and grid readiness

New York targets 9 GW of offshore wind by 2035, creating urgent need for sturdy onshore landing spots. Con Edison’s territory serves roughly 10 million people and dense urban load, making its circuits a strategic prize. Owning interconnection and reinforcement work centralizes project control and leverages regulated recovery mechanisms. That requires heavy near-term capex but supports durable, tariff-backed returns.

Advanced distribution automation and DER orchestration

Advanced distribution automation and DER orchestration address rising rooftop solar, batteries and EVs—EVs reached about 14% global sales in 2023—requiring sensors, automation and control software to keep the grid balanced; as DER penetration grows, Con Edison’s regulated wires monopoly can scale these services, retain share and move toward Cash Cow status.

- Market growth: rising DER adoption drives software/automation demand

- Monopoly edge: regulated wires enable capture of grid-edge services

- Strategy: defend share, scale with DER curve, monetize via ratebase

Public and fleet EV charging enablement

Public and fleet EV charging is a Star for Con Edison: NYC fleets are rapidly electrifying and curbside charging demand is intense; Con Edison serves about 3.5 million customers and its make-ready, interconnection, and targeted owns/ops positioning captures a fast-growth niche. Capex-heavy but central strategically; winning early secures recurring revenue streams and long-tail service demand. US public charging surpassed roughly 150,000 connectors in 2024, underscoring market scale.

- Role: make-ready, interconnection, owns/ops

- Scale: ~3.5M customers (Con Edison)

- Market size: ~150,000 public connectors (2024)

- Tradeoff: high capex vs long-term recurring revenue

Regulated utility: EV charging, storage, 9GW offshore build

Con Edison Stars (EV charging, storage, offshore wind interconnects, DER ops) show high growth with heavy near‑term capex but regulated/tariffed returns as NYC load and CLCPA targets drive demand; ConEd serves ~3.5M customers, NY 9GW offshore by 2035, US public chargers ~150,000 (2024).

| Opportunity | 2024 metric | Implication |

|---|---|---|

| Customers | ~3.5M | Ratebase growth |

| Offshore | 9GW by 2035 | Interconnect capex |

| Public chargers | ~150,000 | Fast EV demand |

What is included in the product

ConEdison BCG Matrix: maps Stars, Cash Cows, Question Marks, Dogs with clear invest/hold/divest guidance and trend context.

One-page Consolidated Edison BCG Matrix highlighting underperformers and stars to simplify capital allocation decisions.

Cash Cows

Regulated electric distribution (NYC & Westchester)

Regulated electric distribution in NYC & Westchester is a baked-in high-share franchise serving roughly 3.5 million customers, with a regulated rate base near $20 billion in 2024. Growth is moderate but predictable; regulation supports strong margins and stable cash flow that fund corporate investments. Lower promotional spend and steady annual capex (around $1.5B) preserve reliability and print the dollars that underwrite ConEdison's strategic bets.

In-service transmission assets (existing rate base)

In-service transmission assets are already built and earning, forming Con Edison's classic utility annuity with a regulated rate base of roughly $34 billion (2024), delivering predictable cash and ROEs set by state commissions.

Market growth is slower than the new-build grid wave, but steady: transmission reliability investments sustain stable margins and cash flow, supporting the companys dividend and credit profile.

Incremental upgrades and targeted efficiency projects lift throughput and cash generation—milk the assets while allocating capex toward the next growth segment.

Regulated gas distribution (near-term)

Regulated gas distribution still throws off reliable cash in a mature market, driven by base rates and utility service obligations that sustain near-term cash flow. Policy headwinds on decarbonization and methane rules create pressure, so keeping infrastructure tight and leaks below regulatory targets is critical to preserve margin. Use the steady proceeds to pivot capital toward electric growth and grid modernization.

Customer delivery charges and fixed fees

Urban density yields scale: Consolidated Edison serves about 3.5 million electric and 1.1 million gas customers (≈4.6 million meters in 2024), producing steady billed revenue that is low-growth but highly predictable.

Not flashy, this cash cow needs minimal promotion—focus is operational excellence, reliability, and regulated rate recovery as a quiet engine-room funding strategy.

- High meter density: ≈4.6M customers (2024)

- Stable cash flow: regulated billing predictability

- Low marketing, high O&M focus

Energy efficiency program administration

Energy efficiency program administration at Consolidated Edison functions as a cash cow: admin fees and cost recovery remained stable and low-risk in 2024, typically under 6% of program budgets per NYPSC filings, while annual portfolio spend in New York exceeds $1B, giving scale despite modest growth.

Tight execution boosts throughput and cash flow—focus on efficiency, compliance, and timely cost recovery keeps margins predictable.

- Admin fees: low-risk, ~<6% (2024 NYPSC)

- Scale: NY portfolio >$1B (2024)

- Strategy: efficient ops, strict compliance, prompt payment

Regulated NYC power: stable cash flow from ≈3.5M electric, ≈1.1M gas

Regulated NYC electric and gas distribution (~3.5M electric, 1.1M gas customers; ≈4.6M meters in 2024) deliver predictable, high-margin cash flow funding growth bets. In-service transmission and distribution assets (regulated rate base ≈$20B electric, ≈$34B transmission, 2024) yield stable returns; steady annual capex ≈$1.5B preserves reliability. Energy-efficiency admin fees <6% with NY portfolio >$1B bolster low-risk cash generation.

| Metric | 2024 |

|---|---|

| Electric customers | ≈3.5M |

| Gas customers | ≈1.1M |

| Meters | ≈4.6M |

| Electric rate base | ≈$20B |

| Transmission rate base | ≈$34B |

| Annual capex | ≈$1.5B |

| EE admin fees | <6% |

| NY EE portfolio | >$1B |

What You’re Viewing Is Included

Consolidated Edison BCG Matrix

The Consolidated Edison BCG Matrix you’re previewing here is the exact same file you’ll receive after purchase—no watermarks, no placeholders. It’s a fully formatted, strategy-ready report built for clear portfolio decisions and stakeholder presentations. Once you buy, the final document is immediately downloadable and editable for your team. Trusted analysis, no surprises—just plug-and-play clarity.