Conn's Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

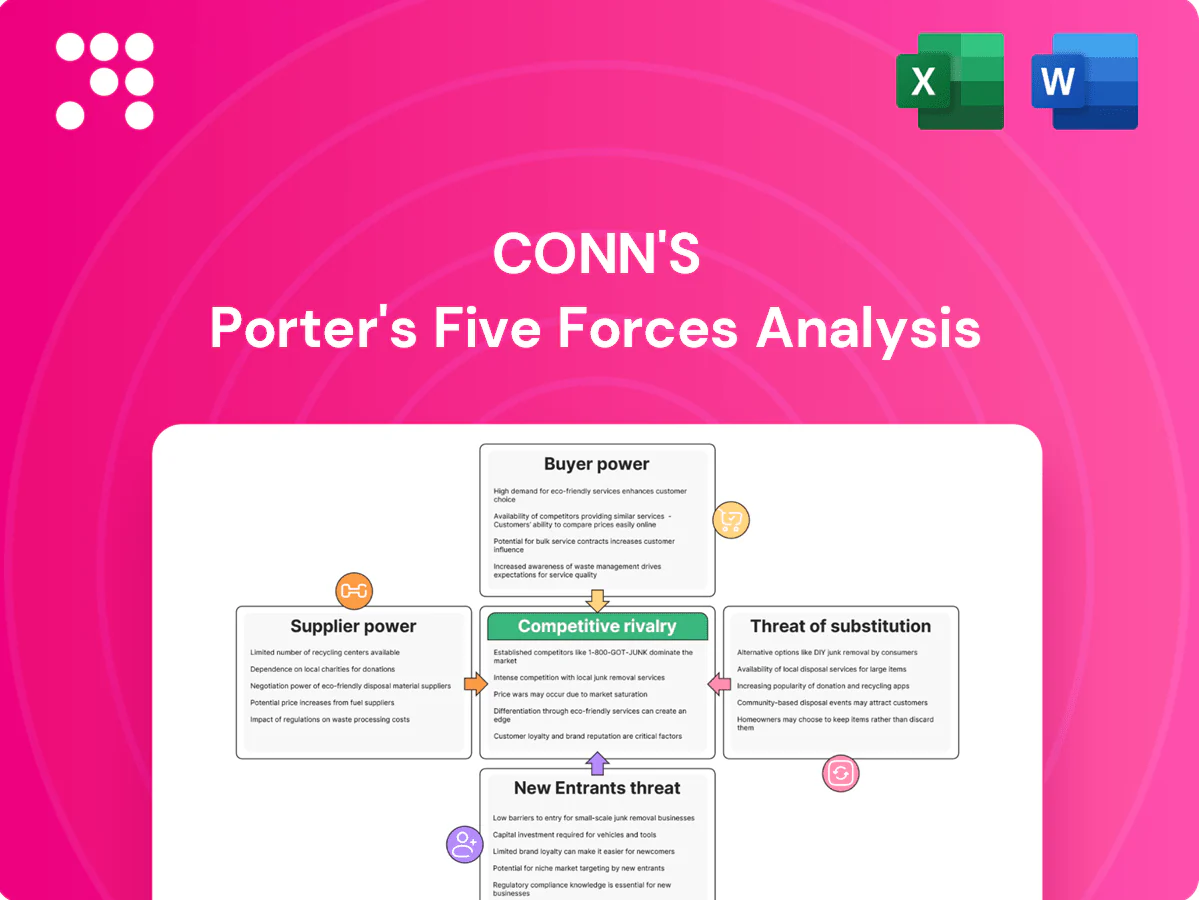

Conn's faces intense buyer power, evolving supplier relationships, and mounting substitute threats as it balances credit-driven sales with retail competition. Our snapshot highlights key pressures and strategic levers but omits force-by-force scoring. Unlock the full Porter's Five Forces Analysis for detailed ratings, visuals, and actionable strategy. Purchase the complete report to inform investment or strategic decisions.

Suppliers Bargaining Power

Concentrated OEM brands

Appliances and electronics are concentrated among a few global OEMs (Samsung, LG, Whirlpool, GE), giving suppliers leverage over pricing, allocations and MAP policies. Conn’s must stock marquee brands to drive traffic, constraining negotiation on markdowns and shelf placement. Vendor programs and co-op funds offset costs but power skews to large OEMs for constrained models. Any 2024 supply disruption or exclusive model deals further tilt terms toward suppliers.

Multi-sourcing in furniture

The US furniture and bedding retail market totaled about $122 billion in 2023 (US Census), and its fragmented supplier base lets Conn’s multi-source and expand private-label assortments to drive bid competition and design flexibility. Premium mattress brands still secure stronger pricing and return-to-vendor terms, concentrating bargaining power in that segment. Persistent lead-time variability and freight costs—still above pre‑pandemic norms—limit rapid vendor switching and inventory agility.

Dependence on parts for repair

Repair services require consistent access to proprietary parts and authorized service agreements, and OEM control over parts availability and pricing increases supplier power post-sale; delays in parts procurement directly impair service SLAs and depress customer satisfaction, narrowing Conn’s options to substitute components and forcing reliance on OEM channels.

Logistics and freight volatility

Ocean and trucking capacity tightness shifts pricing power to carriers and 3PLs, raising Conn’s landed costs and inventory carrying risk; ocean capacity utilization in 2024 stayed above pre-2019 levels. Bulky appliances amplify handling and last-mile complexity, embedding supplier-like leverage in logistics partners. Contracting and optimized routing reduce but do not eliminate exposure. Fuel surcharges—with U.S. diesel averaging about $3.90/gal in 2024 (EIA)—and accessorials further compress margins.

- Capacity tightness → higher landed costs

- Bulky goods → greater 3PL leverage

- Contracts help but don’t eliminate risk

- Fuel/accessorials (diesel ~$3.90/gal in 2024) pressure margins

Capital and securitization costs

Conn’s in-house financing depends on funding markets and lenders whose rates and covenants function as suppliers of capital; tight credit cycles elevate funding costs and shrink the credit box, limiting promotional and inventory flexibility and thereby increasing upstream bargaining power. With the federal funds target at 5.25–5.50% and SOFR roughly 5% in mid-2024, securitization and warehouse spreads rose, pressuring margins; strong portfolio credit performance can restore balance in benign markets.

- Dependence on lenders and ABS markets

- Fed funds 5.25–5.50% (mid-2024), SOFR ~5%

- Tighter credit → higher funding costs → reduced promotional/inventory flexibility

Supplier concentration and logistics squeeze raise landed costs and limit promotional flexibility

Conn’s faces strong supplier leverage from concentrated appliance OEMs, premium mattress brands, OEM parts/control over repairs, tight ocean/truck capacity and 3PLs, plus capital providers influencing in‑house financing costs; these dynamics raise landed costs, limit markdowns and constrain promotional/inventory flexibility.

| Metric | Value |

|---|---|

| US furniture market (2023) | $122B |

| Diesel (2024 avg) | $3.90/gal |

| Fed funds (mid‑2024) | 5.25–5.50% |

What is included in the product

Concise Porter's Five Forces analysis for Conn's that uncovers competitive drivers, buyer and supplier power, threat of substitutes and new entrants, and identifies emerging disruptions and strategic levers to protect market share and profitability.

Clear, one-sheet Porter's Five Forces for Conn's that pinpoints competitive pressures and strategic pain points—easy to customize, copy into board slides, and use to prioritize actions and de-risk decisions.

Customers Bargaining Power

Price transparency

Shoppers compare prices instantly across Best Buy, Home Depot, Amazon, and Wayfair, and Amazon held about 40.4% of US e‑commerce sales in 2024, magnifying price transparency and buyer leverage. Transparent pricing compresses gross margins on TVs and major appliances, forcing Conn’s to defend via bundles, white‑glove delivery, and service plans. Promotional cadence in peak events is critical to retain share.

Financing softens elasticity

Conn's in-house credit and flexible payment plans reduce immediate price sensitivity for credit-constrained buyers, shifting negotiation from sticker price to monthly affordability and damping buyer power. In 2024 Conn's consumer receivables were about $1.1 billion, supporting larger average baskets and higher repeat purchases. This model raises charge-off exposure and invites greater regulatory scrutiny of lending practices.

Low switching costs

Low switching costs let customers move to competitors for similar SKUs and delivery windows, keeping bargaining power high; Conn's 2024 emphasis on point-of-sale financing and service contracts underscores this pressure. Minimal brand exclusivity across appliances and electronics sustains buyer leverage, while returns and delivery promises act as tie-breakers. Loyalty depends on financing terms, service quality, and speed rather than product uniqueness.

Service expectations

Conn's white-glove delivery, installation, and repair services raise perceived value and can reduce buyer price sensitivity by creating experience-based differentiation; strong execution in service and protection-plan sales lowers churn while service failures quickly drive customers to national rivals. Warranty and protection-plan attach rates historically support recurring revenue and higher lifetime value, making service performance a key lever in weakening customer bargaining power.

- Service-driven differentiation

- Experience lowers price sensitivity

- Failures increase churn risk

- Protection plans lock repeat engagement

Promotions-driven behavior

Holiday and event-driven shopping trains Conn's customers to wait for promotions, concentrating demand into predictable promo windows and amplifying buyer leverage during those periods. That cyclicality forces off-cycle pricing trade-offs: raising prices protects margin but can kill traffic, while discounts boost sales but compress profitability. Conn's in-house financing and promotional payment plans further increase deal sensitivity and negotiation power.

- Promo-driven demand concentrates buying power

- Off-cycle pricing must balance traffic vs margin

- Financing promotions heighten sensitivity to deals

40.4% e-commerce share and $1.1B receivables squeeze margins

Customers wield high bargaining power via instant price comparison—Amazon held about 40.4% of US e‑commerce sales in 2024—pressuring Conn’s margins on appliances and electronics. Conn’s $1.1B consumer receivables in 2024 soften sticker sensitivity but raise credit risk and regulatory scrutiny. Service, financing terms, and promo timing determine loyalty more than product uniqueness.

| Metric | 2024 |

|---|---|

| Amazon US e‑commerce share | 40.4% |

| Conn's consumer receivables | $1.1B |

Same Document Delivered

Conn's Porter's Five Forces Analysis

This Conn's Porter's Five Forces Analysis delivers a clear assessment of competitive rivalry, buyer and supplier power, threat of new entrants, and threat of substitutes specific to Conn's business model and market positioning. The preview you see is the same professionally written analysis you'll receive—fully formatted and ready to use. It includes actionable implications and strategic recommendations. Instant download upon purchase.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Conn's faces intense buyer power, evolving supplier relationships, and mounting substitute threats as it balances credit-driven sales with retail competition. Our snapshot highlights key pressures and strategic levers but omits force-by-force scoring. Unlock the full Porter's Five Forces Analysis for detailed ratings, visuals, and actionable strategy. Purchase the complete report to inform investment or strategic decisions.

Suppliers Bargaining Power

Concentrated OEM brands

Appliances and electronics are concentrated among a few global OEMs (Samsung, LG, Whirlpool, GE), giving suppliers leverage over pricing, allocations and MAP policies. Conn’s must stock marquee brands to drive traffic, constraining negotiation on markdowns and shelf placement. Vendor programs and co-op funds offset costs but power skews to large OEMs for constrained models. Any 2024 supply disruption or exclusive model deals further tilt terms toward suppliers.

Multi-sourcing in furniture

The US furniture and bedding retail market totaled about $122 billion in 2023 (US Census), and its fragmented supplier base lets Conn’s multi-source and expand private-label assortments to drive bid competition and design flexibility. Premium mattress brands still secure stronger pricing and return-to-vendor terms, concentrating bargaining power in that segment. Persistent lead-time variability and freight costs—still above pre‑pandemic norms—limit rapid vendor switching and inventory agility.

Dependence on parts for repair

Repair services require consistent access to proprietary parts and authorized service agreements, and OEM control over parts availability and pricing increases supplier power post-sale; delays in parts procurement directly impair service SLAs and depress customer satisfaction, narrowing Conn’s options to substitute components and forcing reliance on OEM channels.

Logistics and freight volatility

Ocean and trucking capacity tightness shifts pricing power to carriers and 3PLs, raising Conn’s landed costs and inventory carrying risk; ocean capacity utilization in 2024 stayed above pre-2019 levels. Bulky appliances amplify handling and last-mile complexity, embedding supplier-like leverage in logistics partners. Contracting and optimized routing reduce but do not eliminate exposure. Fuel surcharges—with U.S. diesel averaging about $3.90/gal in 2024 (EIA)—and accessorials further compress margins.

- Capacity tightness → higher landed costs

- Bulky goods → greater 3PL leverage

- Contracts help but don’t eliminate risk

- Fuel/accessorials (diesel ~$3.90/gal in 2024) pressure margins

Capital and securitization costs

Conn’s in-house financing depends on funding markets and lenders whose rates and covenants function as suppliers of capital; tight credit cycles elevate funding costs and shrink the credit box, limiting promotional and inventory flexibility and thereby increasing upstream bargaining power. With the federal funds target at 5.25–5.50% and SOFR roughly 5% in mid-2024, securitization and warehouse spreads rose, pressuring margins; strong portfolio credit performance can restore balance in benign markets.

- Dependence on lenders and ABS markets

- Fed funds 5.25–5.50% (mid-2024), SOFR ~5%

- Tighter credit → higher funding costs → reduced promotional/inventory flexibility

Supplier concentration and logistics squeeze raise landed costs and limit promotional flexibility

Conn’s faces strong supplier leverage from concentrated appliance OEMs, premium mattress brands, OEM parts/control over repairs, tight ocean/truck capacity and 3PLs, plus capital providers influencing in‑house financing costs; these dynamics raise landed costs, limit markdowns and constrain promotional/inventory flexibility.

| Metric | Value |

|---|---|

| US furniture market (2023) | $122B |

| Diesel (2024 avg) | $3.90/gal |

| Fed funds (mid‑2024) | 5.25–5.50% |

What is included in the product

Concise Porter's Five Forces analysis for Conn's that uncovers competitive drivers, buyer and supplier power, threat of substitutes and new entrants, and identifies emerging disruptions and strategic levers to protect market share and profitability.

Clear, one-sheet Porter's Five Forces for Conn's that pinpoints competitive pressures and strategic pain points—easy to customize, copy into board slides, and use to prioritize actions and de-risk decisions.

Customers Bargaining Power

Price transparency

Shoppers compare prices instantly across Best Buy, Home Depot, Amazon, and Wayfair, and Amazon held about 40.4% of US e‑commerce sales in 2024, magnifying price transparency and buyer leverage. Transparent pricing compresses gross margins on TVs and major appliances, forcing Conn’s to defend via bundles, white‑glove delivery, and service plans. Promotional cadence in peak events is critical to retain share.

Financing softens elasticity

Conn's in-house credit and flexible payment plans reduce immediate price sensitivity for credit-constrained buyers, shifting negotiation from sticker price to monthly affordability and damping buyer power. In 2024 Conn's consumer receivables were about $1.1 billion, supporting larger average baskets and higher repeat purchases. This model raises charge-off exposure and invites greater regulatory scrutiny of lending practices.

Low switching costs

Low switching costs let customers move to competitors for similar SKUs and delivery windows, keeping bargaining power high; Conn's 2024 emphasis on point-of-sale financing and service contracts underscores this pressure. Minimal brand exclusivity across appliances and electronics sustains buyer leverage, while returns and delivery promises act as tie-breakers. Loyalty depends on financing terms, service quality, and speed rather than product uniqueness.

Service expectations

Conn's white-glove delivery, installation, and repair services raise perceived value and can reduce buyer price sensitivity by creating experience-based differentiation; strong execution in service and protection-plan sales lowers churn while service failures quickly drive customers to national rivals. Warranty and protection-plan attach rates historically support recurring revenue and higher lifetime value, making service performance a key lever in weakening customer bargaining power.

- Service-driven differentiation

- Experience lowers price sensitivity

- Failures increase churn risk

- Protection plans lock repeat engagement

Promotions-driven behavior

Holiday and event-driven shopping trains Conn's customers to wait for promotions, concentrating demand into predictable promo windows and amplifying buyer leverage during those periods. That cyclicality forces off-cycle pricing trade-offs: raising prices protects margin but can kill traffic, while discounts boost sales but compress profitability. Conn's in-house financing and promotional payment plans further increase deal sensitivity and negotiation power.

- Promo-driven demand concentrates buying power

- Off-cycle pricing must balance traffic vs margin

- Financing promotions heighten sensitivity to deals

40.4% e-commerce share and $1.1B receivables squeeze margins

Customers wield high bargaining power via instant price comparison—Amazon held about 40.4% of US e‑commerce sales in 2024—pressuring Conn’s margins on appliances and electronics. Conn’s $1.1B consumer receivables in 2024 soften sticker sensitivity but raise credit risk and regulatory scrutiny. Service, financing terms, and promo timing determine loyalty more than product uniqueness.

| Metric | 2024 |

|---|---|

| Amazon US e‑commerce share | 40.4% |

| Conn's consumer receivables | $1.1B |

Same Document Delivered

Conn's Porter's Five Forces Analysis

This Conn's Porter's Five Forces Analysis delivers a clear assessment of competitive rivalry, buyer and supplier power, threat of new entrants, and threat of substitutes specific to Conn's business model and market positioning. The preview you see is the same professionally written analysis you'll receive—fully formatted and ready to use. It includes actionable implications and strategic recommendations. Instant download upon purchase.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Conn's faces intense buyer power, evolving supplier relationships, and mounting substitute threats as it balances credit-driven sales with retail competition. Our snapshot highlights key pressures and strategic levers but omits force-by-force scoring. Unlock the full Porter's Five Forces Analysis for detailed ratings, visuals, and actionable strategy. Purchase the complete report to inform investment or strategic decisions.

Suppliers Bargaining Power

Concentrated OEM brands

Appliances and electronics are concentrated among a few global OEMs (Samsung, LG, Whirlpool, GE), giving suppliers leverage over pricing, allocations and MAP policies. Conn’s must stock marquee brands to drive traffic, constraining negotiation on markdowns and shelf placement. Vendor programs and co-op funds offset costs but power skews to large OEMs for constrained models. Any 2024 supply disruption or exclusive model deals further tilt terms toward suppliers.

Multi-sourcing in furniture

The US furniture and bedding retail market totaled about $122 billion in 2023 (US Census), and its fragmented supplier base lets Conn’s multi-source and expand private-label assortments to drive bid competition and design flexibility. Premium mattress brands still secure stronger pricing and return-to-vendor terms, concentrating bargaining power in that segment. Persistent lead-time variability and freight costs—still above pre‑pandemic norms—limit rapid vendor switching and inventory agility.

Dependence on parts for repair

Repair services require consistent access to proprietary parts and authorized service agreements, and OEM control over parts availability and pricing increases supplier power post-sale; delays in parts procurement directly impair service SLAs and depress customer satisfaction, narrowing Conn’s options to substitute components and forcing reliance on OEM channels.

Logistics and freight volatility

Ocean and trucking capacity tightness shifts pricing power to carriers and 3PLs, raising Conn’s landed costs and inventory carrying risk; ocean capacity utilization in 2024 stayed above pre-2019 levels. Bulky appliances amplify handling and last-mile complexity, embedding supplier-like leverage in logistics partners. Contracting and optimized routing reduce but do not eliminate exposure. Fuel surcharges—with U.S. diesel averaging about $3.90/gal in 2024 (EIA)—and accessorials further compress margins.

- Capacity tightness → higher landed costs

- Bulky goods → greater 3PL leverage

- Contracts help but don’t eliminate risk

- Fuel/accessorials (diesel ~$3.90/gal in 2024) pressure margins

Capital and securitization costs

Conn’s in-house financing depends on funding markets and lenders whose rates and covenants function as suppliers of capital; tight credit cycles elevate funding costs and shrink the credit box, limiting promotional and inventory flexibility and thereby increasing upstream bargaining power. With the federal funds target at 5.25–5.50% and SOFR roughly 5% in mid-2024, securitization and warehouse spreads rose, pressuring margins; strong portfolio credit performance can restore balance in benign markets.

- Dependence on lenders and ABS markets

- Fed funds 5.25–5.50% (mid-2024), SOFR ~5%

- Tighter credit → higher funding costs → reduced promotional/inventory flexibility

Supplier concentration and logistics squeeze raise landed costs and limit promotional flexibility

Conn’s faces strong supplier leverage from concentrated appliance OEMs, premium mattress brands, OEM parts/control over repairs, tight ocean/truck capacity and 3PLs, plus capital providers influencing in‑house financing costs; these dynamics raise landed costs, limit markdowns and constrain promotional/inventory flexibility.

| Metric | Value |

|---|---|

| US furniture market (2023) | $122B |

| Diesel (2024 avg) | $3.90/gal |

| Fed funds (mid‑2024) | 5.25–5.50% |

What is included in the product

Concise Porter's Five Forces analysis for Conn's that uncovers competitive drivers, buyer and supplier power, threat of substitutes and new entrants, and identifies emerging disruptions and strategic levers to protect market share and profitability.

Clear, one-sheet Porter's Five Forces for Conn's that pinpoints competitive pressures and strategic pain points—easy to customize, copy into board slides, and use to prioritize actions and de-risk decisions.

Customers Bargaining Power

Price transparency

Shoppers compare prices instantly across Best Buy, Home Depot, Amazon, and Wayfair, and Amazon held about 40.4% of US e‑commerce sales in 2024, magnifying price transparency and buyer leverage. Transparent pricing compresses gross margins on TVs and major appliances, forcing Conn’s to defend via bundles, white‑glove delivery, and service plans. Promotional cadence in peak events is critical to retain share.

Financing softens elasticity

Conn's in-house credit and flexible payment plans reduce immediate price sensitivity for credit-constrained buyers, shifting negotiation from sticker price to monthly affordability and damping buyer power. In 2024 Conn's consumer receivables were about $1.1 billion, supporting larger average baskets and higher repeat purchases. This model raises charge-off exposure and invites greater regulatory scrutiny of lending practices.

Low switching costs

Low switching costs let customers move to competitors for similar SKUs and delivery windows, keeping bargaining power high; Conn's 2024 emphasis on point-of-sale financing and service contracts underscores this pressure. Minimal brand exclusivity across appliances and electronics sustains buyer leverage, while returns and delivery promises act as tie-breakers. Loyalty depends on financing terms, service quality, and speed rather than product uniqueness.

Service expectations

Conn's white-glove delivery, installation, and repair services raise perceived value and can reduce buyer price sensitivity by creating experience-based differentiation; strong execution in service and protection-plan sales lowers churn while service failures quickly drive customers to national rivals. Warranty and protection-plan attach rates historically support recurring revenue and higher lifetime value, making service performance a key lever in weakening customer bargaining power.

- Service-driven differentiation

- Experience lowers price sensitivity

- Failures increase churn risk

- Protection plans lock repeat engagement

Promotions-driven behavior

Holiday and event-driven shopping trains Conn's customers to wait for promotions, concentrating demand into predictable promo windows and amplifying buyer leverage during those periods. That cyclicality forces off-cycle pricing trade-offs: raising prices protects margin but can kill traffic, while discounts boost sales but compress profitability. Conn's in-house financing and promotional payment plans further increase deal sensitivity and negotiation power.

- Promo-driven demand concentrates buying power

- Off-cycle pricing must balance traffic vs margin

- Financing promotions heighten sensitivity to deals

40.4% e-commerce share and $1.1B receivables squeeze margins

Customers wield high bargaining power via instant price comparison—Amazon held about 40.4% of US e‑commerce sales in 2024—pressuring Conn’s margins on appliances and electronics. Conn’s $1.1B consumer receivables in 2024 soften sticker sensitivity but raise credit risk and regulatory scrutiny. Service, financing terms, and promo timing determine loyalty more than product uniqueness.

| Metric | 2024 |

|---|---|

| Amazon US e‑commerce share | 40.4% |

| Conn's consumer receivables | $1.1B |

Same Document Delivered

Conn's Porter's Five Forces Analysis

This Conn's Porter's Five Forces Analysis delivers a clear assessment of competitive rivalry, buyer and supplier power, threat of new entrants, and threat of substitutes specific to Conn's business model and market positioning. The preview you see is the same professionally written analysis you'll receive—fully formatted and ready to use. It includes actionable implications and strategic recommendations. Instant download upon purchase.