Conn's SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

Conn’s combines diversified product lines and a captive financing model with growth potential from e‑commerce and aftercare services, but faces credit risk, margin pressure, and intense retail competition. Our full SWOT unpacks these dynamics with financial context and strategic recommendations. Purchase the complete report for a ready-to-use, editable analysis to guide investment or strategy decisions.

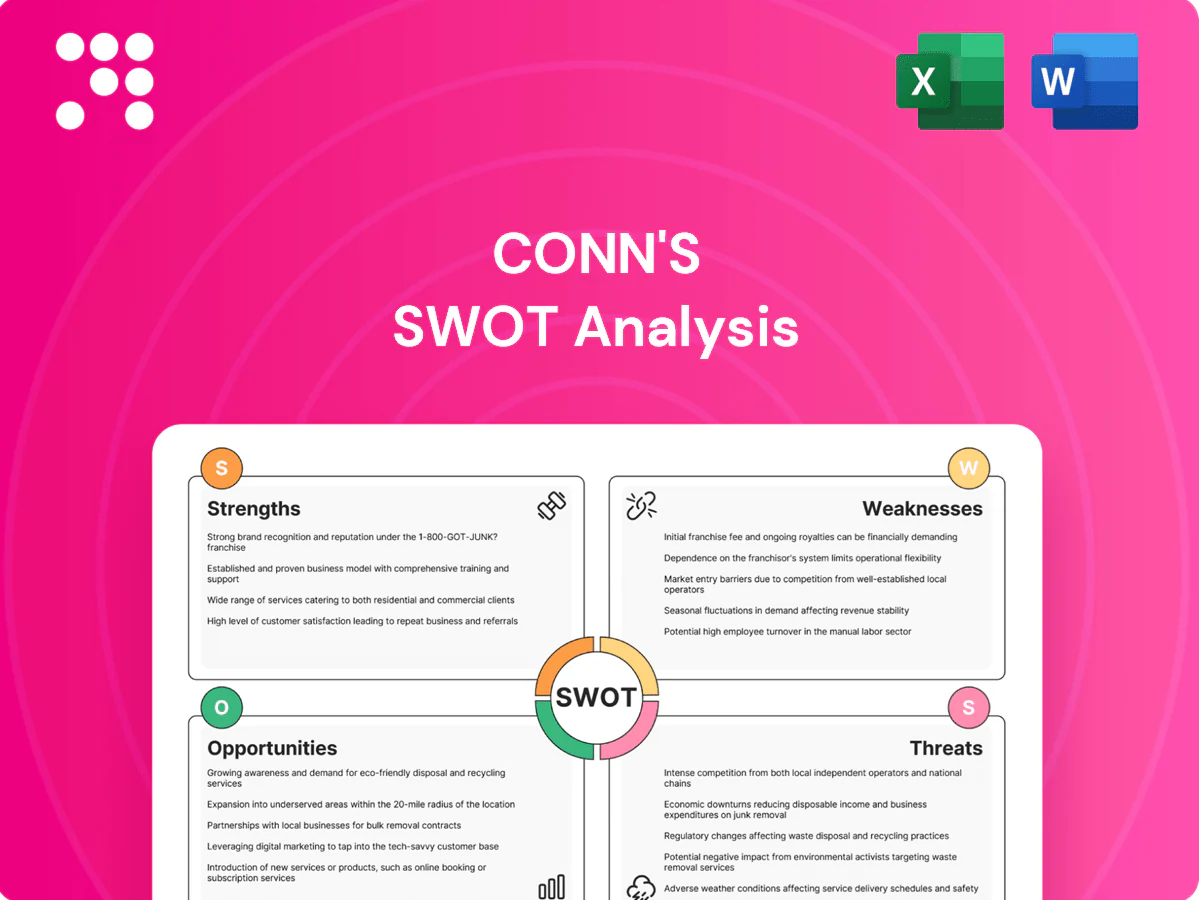

Strengths

Integrated in-house financing

Conn's proprietary in-house financing extends credit to subprime and near-prime customers who are often underserved, boosting conversion rates and enabling larger average ticket sizes. Financing generates recurring interest income and strengthens lifetime customer value through repeat engagement and service relationships. This embedded credit offering differentiates Conn's from cash-only retailers by turning point-of-sale approvals into stable financing revenue streams.

Diverse durable goods assortment

Conn's offers four core durable-goods categories—furniture, mattresses, appliances and electronics—balancing demand across seasonal cycles. This four-category mix reduces reliance on any single product cycle and enables cross-selling and bundled promotions. Customers can outfit multiple rooms through one retailer, helping raise average ticket and lifetime value.

Repair and service capabilities

Conn's in-house repair centers extend product lifecycles and boost customer satisfaction, with the company highlighting expanded service throughput in 2024 as a strategic focus.

Service and warranty revenues in 2024 complemented product margins, creating higher-margin recurring revenues and supporting overall profitability.

These repair capabilities underpin warranty offerings and post-sale touchpoints, helping increase repeat purchases and reduce returns in 2024.

Multi-state retail footprint

Conn's multi-state footprint of over 150 retail locations across the Southern and Southwestern U.S. builds local presence and trust for big-ticket purchases, with showrooms enabling hands-on product experience prior to purchase. Regional scale strengthens supplier terms and logistics, helping enable same- or next-day delivery in core markets and improving fulfillment efficiency.

- Over 150 stores

- Showroom-driven conversion

- Regional logistics enable fast delivery

Customer relationship depth

Conn's depth of customer relationships is driven by its in-house credit accounts, extended warranties and service plans that create multiple engagement hooks and recurring billing; Conn's reported roughly $2.1 billion in net customer receivables in 2024. Ongoing service interactions increase brand stickiness, while payments and purchase data enable personalized offers that boost retention and lifetime value.

- Credit accounts: recurring revenue

- Warranties/service: post-sale touchpoints

- Data: personalized offers → higher LTV

- 2024 receivables: ~$2.1B

In-house finance and services turn subprime demand into recurring income; net receivables $2.1B

Conn's in-house financing converts underserved subprime/near-prime demand into higher conversion and recurring interest income; net receivables were ~$2.1B in 2024. Diverse durable-goods mix and over 150 showrooms support cross-selling and higher AOV. In-house repair/warranty services drive recurring margin and retention, while regional logistics enable fast fulfillment and supplier leverage.

| Metric | 2024 |

|---|---|

| Net receivables | $2.1B |

| Stores | 150+ |

| Core categories | 4 |

What is included in the product

Delivers a strategic overview of Conn's internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to assess competitive position, growth drivers, operational gaps, and key risks shaping its future.

Delivers a focused SWOT snapshot of Conn's to quickly identify issues and prioritize remediation, ideal for executives seeking fast, actionable clarity.

Weaknesses

Credit risk exposure

Reliance on in-house financing concentrates risk in consumer credit performance — Conn’s had over $1.0 billion in retail receivables in 2024, exposing earnings to borrower stress. Rising delinquencies and charge-offs can quickly erode profitability, while higher provisioning adds earnings volatility. Maintaining credit operations demands specialized underwriting and collections expertise to control losses.

Macroeconomic sensitivity

Conn's sells discretionary durable goods that customers often defer in downturns; U.S. unemployment was about 4.0% in mid-2025 and the Federal Reserve target rate of 5.25–5.50% raises financing costs and reduces affordability, pressuring Conn's point-of-sale financing. Higher rates and weaker consumer confidence can compress same-store sales, while increased promotional intensity to sustain traffic further squeezes margins.

Store-centric cost structure

Leases, labor and delivery infrastructure create significant fixed costs for Conn’s, contributing to operating leverage as the retailer ran 136 stores and reported roughly $1.7 billion in net sales in 2024. Underperforming locations compress margins and forced higher provisions in recent quarters. Declining foot traffic can quickly de-leverage earnings given high occupancy and staffing commitments. Store closures or relocations incur sizeable one-time charges and disruption to EMV and customer financing flows.

Competitive pricing pressure

Conn's faces sharp pricing pressure as big-box and e-commerce rivals set low price benchmarks and frequent promotions that can compress gross margins; U.S. e-commerce accounted for about 16% of retail sales in 2023, intensifying real-time price comparisons. Customers commonly showroom and compare online, forcing differentiation—service, in-store experience, or financing—to offset pure price competition.

- Pricing benchmarks set by big-box/e-commerce

- Frequent promotions compress gross margins

- Real-time showrooming by customers

- Need differentiation beyond price

Brand skew to value-oriented segments

Serving a largely credit-challenged customer base constrains Conn's appeal to prime segments, reinforcing a subprime perception that can cap average ticket and product mix; premium brands often limit distribution to higher-tier retailers, reducing cross-sell opportunities. Marketing must signal accessibility while elevating quality cues to avoid entrenching a value-only image.

- Credit mix: limits prime penetration

- Average ticket: pressured by subprime mix

- Distribution: premium brands selective

- Marketing: balance accessibility and quality

Massive in-house receivables and fixed-cost leverage raise credit, traffic and pricing risks

Conn's concentration in in-house receivables (~$1.0B in 2024) raises credit-loss and provisioning risk; rising delinquencies can quickly erode earnings. High fixed costs and operating leverage (136 stores; $1.7B sales in 2024) amplify downside from traffic declines. Financing-dependent, price-pressured model faces showrooming and big-box/e-commerce competition.

| Metric | Value |

|---|---|

| Retail receivables (2024) | $1.0B+ |

| Net sales (2024) | $1.7B |

| Stores | 136 |

| Fed funds (mid-2025) | 5.25–5.50% |

Full Version Awaits

Conn's SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; purchase unlocks the complete, editable version. You’re viewing a live excerpt of the exact file included in the download, ready to use after checkout.

Elevate Your Analysis with the Complete SWOT Report

Conn’s combines diversified product lines and a captive financing model with growth potential from e‑commerce and aftercare services, but faces credit risk, margin pressure, and intense retail competition. Our full SWOT unpacks these dynamics with financial context and strategic recommendations. Purchase the complete report for a ready-to-use, editable analysis to guide investment or strategy decisions.

Strengths

Integrated in-house financing

Conn's proprietary in-house financing extends credit to subprime and near-prime customers who are often underserved, boosting conversion rates and enabling larger average ticket sizes. Financing generates recurring interest income and strengthens lifetime customer value through repeat engagement and service relationships. This embedded credit offering differentiates Conn's from cash-only retailers by turning point-of-sale approvals into stable financing revenue streams.

Diverse durable goods assortment

Conn's offers four core durable-goods categories—furniture, mattresses, appliances and electronics—balancing demand across seasonal cycles. This four-category mix reduces reliance on any single product cycle and enables cross-selling and bundled promotions. Customers can outfit multiple rooms through one retailer, helping raise average ticket and lifetime value.

Repair and service capabilities

Conn's in-house repair centers extend product lifecycles and boost customer satisfaction, with the company highlighting expanded service throughput in 2024 as a strategic focus.

Service and warranty revenues in 2024 complemented product margins, creating higher-margin recurring revenues and supporting overall profitability.

These repair capabilities underpin warranty offerings and post-sale touchpoints, helping increase repeat purchases and reduce returns in 2024.

Multi-state retail footprint

Conn's multi-state footprint of over 150 retail locations across the Southern and Southwestern U.S. builds local presence and trust for big-ticket purchases, with showrooms enabling hands-on product experience prior to purchase. Regional scale strengthens supplier terms and logistics, helping enable same- or next-day delivery in core markets and improving fulfillment efficiency.

- Over 150 stores

- Showroom-driven conversion

- Regional logistics enable fast delivery

Customer relationship depth

Conn's depth of customer relationships is driven by its in-house credit accounts, extended warranties and service plans that create multiple engagement hooks and recurring billing; Conn's reported roughly $2.1 billion in net customer receivables in 2024. Ongoing service interactions increase brand stickiness, while payments and purchase data enable personalized offers that boost retention and lifetime value.

- Credit accounts: recurring revenue

- Warranties/service: post-sale touchpoints

- Data: personalized offers → higher LTV

- 2024 receivables: ~$2.1B

In-house finance and services turn subprime demand into recurring income; net receivables $2.1B

Conn's in-house financing converts underserved subprime/near-prime demand into higher conversion and recurring interest income; net receivables were ~$2.1B in 2024. Diverse durable-goods mix and over 150 showrooms support cross-selling and higher AOV. In-house repair/warranty services drive recurring margin and retention, while regional logistics enable fast fulfillment and supplier leverage.

| Metric | 2024 |

|---|---|

| Net receivables | $2.1B |

| Stores | 150+ |

| Core categories | 4 |

What is included in the product

Delivers a strategic overview of Conn's internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to assess competitive position, growth drivers, operational gaps, and key risks shaping its future.

Delivers a focused SWOT snapshot of Conn's to quickly identify issues and prioritize remediation, ideal for executives seeking fast, actionable clarity.

Weaknesses

Credit risk exposure

Reliance on in-house financing concentrates risk in consumer credit performance — Conn’s had over $1.0 billion in retail receivables in 2024, exposing earnings to borrower stress. Rising delinquencies and charge-offs can quickly erode profitability, while higher provisioning adds earnings volatility. Maintaining credit operations demands specialized underwriting and collections expertise to control losses.

Macroeconomic sensitivity

Conn's sells discretionary durable goods that customers often defer in downturns; U.S. unemployment was about 4.0% in mid-2025 and the Federal Reserve target rate of 5.25–5.50% raises financing costs and reduces affordability, pressuring Conn's point-of-sale financing. Higher rates and weaker consumer confidence can compress same-store sales, while increased promotional intensity to sustain traffic further squeezes margins.

Store-centric cost structure

Leases, labor and delivery infrastructure create significant fixed costs for Conn’s, contributing to operating leverage as the retailer ran 136 stores and reported roughly $1.7 billion in net sales in 2024. Underperforming locations compress margins and forced higher provisions in recent quarters. Declining foot traffic can quickly de-leverage earnings given high occupancy and staffing commitments. Store closures or relocations incur sizeable one-time charges and disruption to EMV and customer financing flows.

Competitive pricing pressure

Conn's faces sharp pricing pressure as big-box and e-commerce rivals set low price benchmarks and frequent promotions that can compress gross margins; U.S. e-commerce accounted for about 16% of retail sales in 2023, intensifying real-time price comparisons. Customers commonly showroom and compare online, forcing differentiation—service, in-store experience, or financing—to offset pure price competition.

- Pricing benchmarks set by big-box/e-commerce

- Frequent promotions compress gross margins

- Real-time showrooming by customers

- Need differentiation beyond price

Brand skew to value-oriented segments

Serving a largely credit-challenged customer base constrains Conn's appeal to prime segments, reinforcing a subprime perception that can cap average ticket and product mix; premium brands often limit distribution to higher-tier retailers, reducing cross-sell opportunities. Marketing must signal accessibility while elevating quality cues to avoid entrenching a value-only image.

- Credit mix: limits prime penetration

- Average ticket: pressured by subprime mix

- Distribution: premium brands selective

- Marketing: balance accessibility and quality

Massive in-house receivables and fixed-cost leverage raise credit, traffic and pricing risks

Conn's concentration in in-house receivables (~$1.0B in 2024) raises credit-loss and provisioning risk; rising delinquencies can quickly erode earnings. High fixed costs and operating leverage (136 stores; $1.7B sales in 2024) amplify downside from traffic declines. Financing-dependent, price-pressured model faces showrooming and big-box/e-commerce competition.

| Metric | Value |

|---|---|

| Retail receivables (2024) | $1.0B+ |

| Net sales (2024) | $1.7B |

| Stores | 136 |

| Fed funds (mid-2025) | 5.25–5.50% |

Full Version Awaits

Conn's SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; purchase unlocks the complete, editable version. You’re viewing a live excerpt of the exact file included in the download, ready to use after checkout.

Description

Elevate Your Analysis with the Complete SWOT Report

Conn’s combines diversified product lines and a captive financing model with growth potential from e‑commerce and aftercare services, but faces credit risk, margin pressure, and intense retail competition. Our full SWOT unpacks these dynamics with financial context and strategic recommendations. Purchase the complete report for a ready-to-use, editable analysis to guide investment or strategy decisions.

Strengths

Integrated in-house financing

Conn's proprietary in-house financing extends credit to subprime and near-prime customers who are often underserved, boosting conversion rates and enabling larger average ticket sizes. Financing generates recurring interest income and strengthens lifetime customer value through repeat engagement and service relationships. This embedded credit offering differentiates Conn's from cash-only retailers by turning point-of-sale approvals into stable financing revenue streams.

Diverse durable goods assortment

Conn's offers four core durable-goods categories—furniture, mattresses, appliances and electronics—balancing demand across seasonal cycles. This four-category mix reduces reliance on any single product cycle and enables cross-selling and bundled promotions. Customers can outfit multiple rooms through one retailer, helping raise average ticket and lifetime value.

Repair and service capabilities

Conn's in-house repair centers extend product lifecycles and boost customer satisfaction, with the company highlighting expanded service throughput in 2024 as a strategic focus.

Service and warranty revenues in 2024 complemented product margins, creating higher-margin recurring revenues and supporting overall profitability.

These repair capabilities underpin warranty offerings and post-sale touchpoints, helping increase repeat purchases and reduce returns in 2024.

Multi-state retail footprint

Conn's multi-state footprint of over 150 retail locations across the Southern and Southwestern U.S. builds local presence and trust for big-ticket purchases, with showrooms enabling hands-on product experience prior to purchase. Regional scale strengthens supplier terms and logistics, helping enable same- or next-day delivery in core markets and improving fulfillment efficiency.

- Over 150 stores

- Showroom-driven conversion

- Regional logistics enable fast delivery

Customer relationship depth

Conn's depth of customer relationships is driven by its in-house credit accounts, extended warranties and service plans that create multiple engagement hooks and recurring billing; Conn's reported roughly $2.1 billion in net customer receivables in 2024. Ongoing service interactions increase brand stickiness, while payments and purchase data enable personalized offers that boost retention and lifetime value.

- Credit accounts: recurring revenue

- Warranties/service: post-sale touchpoints

- Data: personalized offers → higher LTV

- 2024 receivables: ~$2.1B

In-house finance and services turn subprime demand into recurring income; net receivables $2.1B

Conn's in-house financing converts underserved subprime/near-prime demand into higher conversion and recurring interest income; net receivables were ~$2.1B in 2024. Diverse durable-goods mix and over 150 showrooms support cross-selling and higher AOV. In-house repair/warranty services drive recurring margin and retention, while regional logistics enable fast fulfillment and supplier leverage.

| Metric | 2024 |

|---|---|

| Net receivables | $2.1B |

| Stores | 150+ |

| Core categories | 4 |

What is included in the product

Delivers a strategic overview of Conn's internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to assess competitive position, growth drivers, operational gaps, and key risks shaping its future.

Delivers a focused SWOT snapshot of Conn's to quickly identify issues and prioritize remediation, ideal for executives seeking fast, actionable clarity.

Weaknesses

Credit risk exposure

Reliance on in-house financing concentrates risk in consumer credit performance — Conn’s had over $1.0 billion in retail receivables in 2024, exposing earnings to borrower stress. Rising delinquencies and charge-offs can quickly erode profitability, while higher provisioning adds earnings volatility. Maintaining credit operations demands specialized underwriting and collections expertise to control losses.

Macroeconomic sensitivity

Conn's sells discretionary durable goods that customers often defer in downturns; U.S. unemployment was about 4.0% in mid-2025 and the Federal Reserve target rate of 5.25–5.50% raises financing costs and reduces affordability, pressuring Conn's point-of-sale financing. Higher rates and weaker consumer confidence can compress same-store sales, while increased promotional intensity to sustain traffic further squeezes margins.

Store-centric cost structure

Leases, labor and delivery infrastructure create significant fixed costs for Conn’s, contributing to operating leverage as the retailer ran 136 stores and reported roughly $1.7 billion in net sales in 2024. Underperforming locations compress margins and forced higher provisions in recent quarters. Declining foot traffic can quickly de-leverage earnings given high occupancy and staffing commitments. Store closures or relocations incur sizeable one-time charges and disruption to EMV and customer financing flows.

Competitive pricing pressure

Conn's faces sharp pricing pressure as big-box and e-commerce rivals set low price benchmarks and frequent promotions that can compress gross margins; U.S. e-commerce accounted for about 16% of retail sales in 2023, intensifying real-time price comparisons. Customers commonly showroom and compare online, forcing differentiation—service, in-store experience, or financing—to offset pure price competition.

- Pricing benchmarks set by big-box/e-commerce

- Frequent promotions compress gross margins

- Real-time showrooming by customers

- Need differentiation beyond price

Brand skew to value-oriented segments

Serving a largely credit-challenged customer base constrains Conn's appeal to prime segments, reinforcing a subprime perception that can cap average ticket and product mix; premium brands often limit distribution to higher-tier retailers, reducing cross-sell opportunities. Marketing must signal accessibility while elevating quality cues to avoid entrenching a value-only image.

- Credit mix: limits prime penetration

- Average ticket: pressured by subprime mix

- Distribution: premium brands selective

- Marketing: balance accessibility and quality

Massive in-house receivables and fixed-cost leverage raise credit, traffic and pricing risks

Conn's concentration in in-house receivables (~$1.0B in 2024) raises credit-loss and provisioning risk; rising delinquencies can quickly erode earnings. High fixed costs and operating leverage (136 stores; $1.7B sales in 2024) amplify downside from traffic declines. Financing-dependent, price-pressured model faces showrooming and big-box/e-commerce competition.

| Metric | Value |

|---|---|

| Retail receivables (2024) | $1.0B+ |

| Net sales (2024) | $1.7B |

| Stores | 136 |

| Fed funds (mid-2025) | 5.25–5.50% |

Full Version Awaits

Conn's SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; purchase unlocks the complete, editable version. You’re viewing a live excerpt of the exact file included in the download, ready to use after checkout.