Consigli Construction Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

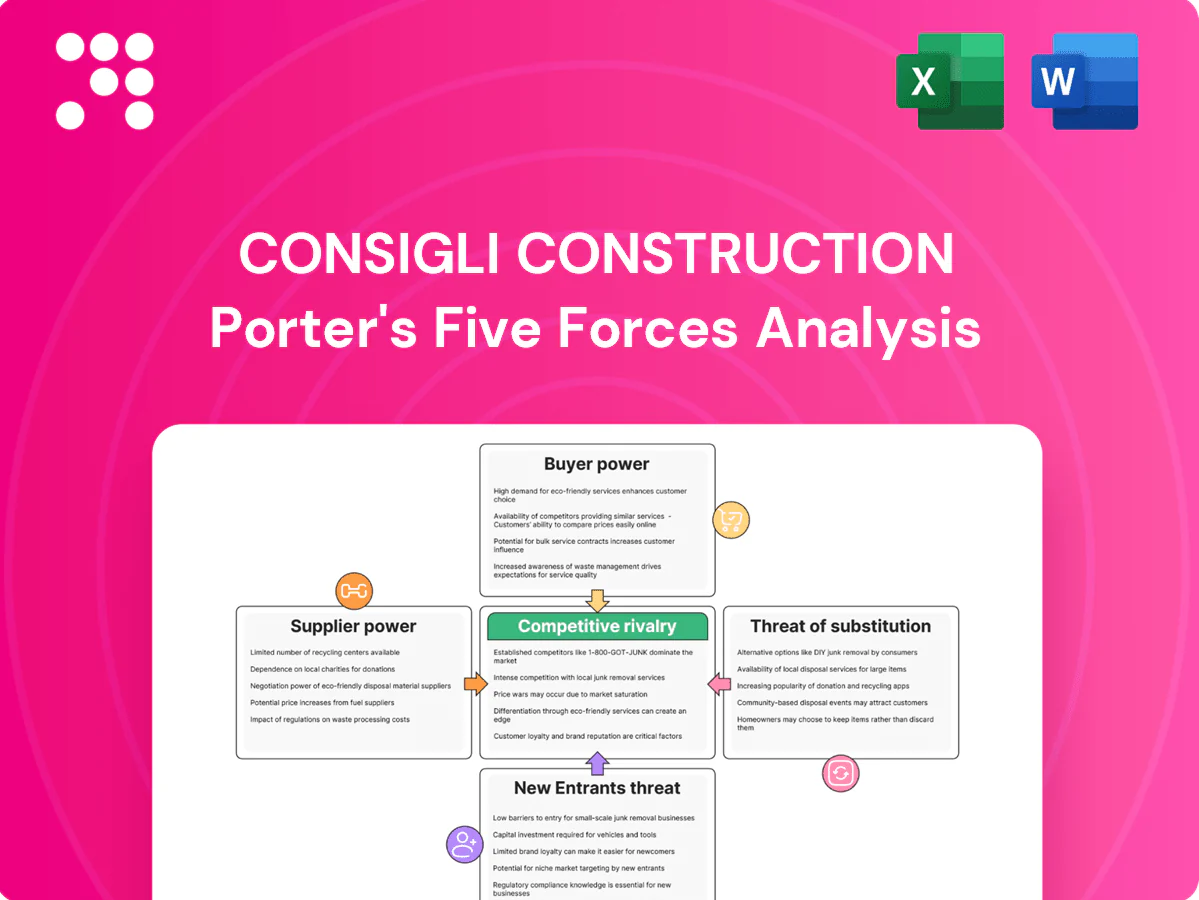

Consigli Construction faces moderate supplier leverage, high buyer expectations for quality and timeliness, and steady rivalry from regional contractors, while barriers to new entrants remain significant due to reputation and bonding requirements. Substitutes are limited but technology-driven delivery models pose emerging threats. This snapshot highlights key pressures; unlock the full Porter's Five Forces Analysis for a force-by-force breakdown and actionable strategy guidance.

Suppliers Bargaining Power

Specialty trade concentration

Complex healthcare and life-science projects rely on scarce MEP, cleanroom, and commissioning specialists, creating supplier concentration that limits options. Limited qualified subs can command premium pricing and favorable terms, and 86% of contractors reported hiring difficulty in the AGC 2024 workforce survey. Consigli mitigates risk via preferred networks and early trade partner engagement, but bottlenecks still elevate schedule and cost risk.

Key materials volatility

Key inputs — steel HRC spot near USD 800/ton in 2024, cement prices up about 6% YoY (2024), architectural glass lead times of 12–20 weeks and advanced envelope systems commanding 10–25% price premiums — are price- and lead-time sensitive; suppliers gain bargaining power during commodity spikes or logistics disruptions, and early procurement/hedging mitigate but do not transfer all risk, while sustainable specs further narrow supplier options.

Union labor and wage dynamics

Union agreements and prevailing wage rules (Davis-Bacon on federal jobs and prevailing-wage rules covering roughly 10% of projects) set clear floors on labor costs for Consigli; unionized construction workforce ~13% in 2024. In tight labor markets with construction unemployment near 5% in 2024, skilled trades gain leverage to push rates higher. Workforce development and long-term relations (apprenticeship growth ~15% since 2020) stabilize availability while complex projects increase reliance on top-tier crews.

Green and high-performance products

- Fewer compliant vendors increase pricing and lead‑time power

- Prequalify multiple sustainable suppliers to reduce risk

- Design flexibility offsets supplier leverage

- Owner mandates can restrict substitution

Digital tools and equipment providers

Digital tools (BIM, VDC, reality-capture) create ecosystem dependencies for Consigli as proprietary formats and vendor-specific training raise switching costs; IFC is an open standard maintained by buildingSMART that can reduce that lock-in. Standardizing workflows and requiring open formats in contracts curbs vendor power, while heavy use of equipment rental markets provides short-term leverage on fast-track jobs.

- IFC=open standard (buildingSMART)

- Proprietary formats=increased switching costs

- Standardization=open-standards reduce vendor power

- Equipment rental=leverage on fast-track projects

Supply concentration, tight labor boost construction costs; 86% report hiring difficulty

Supplier concentration for MEP/cleanroom specialists and proprietary digital vendors raises pricing and switching costs; 86% of contractors reported hiring difficulty (AGC 2024). Key inputs: HRC steel ~USD 800/ton (2024), cement +6% YoY (2024), glass 12–20 wk lead. Unionized workforce ~13% and construction unemployment ~5% (2024) tighten labor supply.

| Metric | 2024 |

|---|---|

| Hiring difficulty | 86% |

| HRC steel | ~USD 800/ton |

| Cement YoY | +6% |

| Glass lead | 12–20 wk |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Consigli Construction. Evaluates control held by suppliers and buyers and identifies disruptive substitutes threatening market share.

Clear one-sheet Porter's Five Forces for Consigli Construction—instantly reveals competitive pressures with a customizable radar chart so teams can model scenarios, swap in your data, and export clean slides for boardrooms without macros or coding.

Customers Bargaining Power

Sophisticated institutional owners

Universities, hospitals and labs employ experienced procurement teams that insist on full transparency, detailed preconstruction deliverables and robust performance guarantees such as payment and performance bonds. Their technical expertise raises price sensitivity and enforces strict scope discipline, reducing change-order risk. Long-term campus pipelines, often planned over 5–10 years, preferentially award repeat work to proven partners.

Competitive RFP and CM-at-Risk bids

In 2024 formal RFPs and competitive CM-at-risk bids benchmark fee, GC and contingency structures across multiple CMs, compressing margins and shifting more downside risk to the contractor. Differentiation for Consigli therefore rests on demonstrable schedule certainty and high-value constructability input. Clear win themes in life sciences—repeatable lab fit-out expertise and validation experience—help offset price pressure from tightly contested RFPs.

Project scale and bundling

Large, multi-phase programs give owners leverage via volume, allowing consolidation across projects against a U.S. construction spend of about $1.9 trillion in 2023–24 (Census Bureau). Bundled work routinely extracts discounts and preferred payment or warranty terms, while buyers typically require dedicated teams and guaranteed capacity windows. Strong on-time, on-budget performance converts that negotiating power into repeat awards.

Delivery method choices

Owners toggle between CM, design-build, IPD and P3 to shift risk and control, enabling method shopping that raises buyer bargaining power; U.S. construction put-in-place reached about $1.9 trillion in 2024, amplifying owner leverage across large programs. Consigli must tailor value propositions by delivery method and pursue early engagement to lock influence before price-only selection stages.

Sustainability and lifecycle priorities

Buyers increasingly prioritize energy, carbon, and total cost of ownership outcomes, shifting decisions from lowest bid to lifecycle value; buildings and construction account for about 37% of energy-related CO2 emissions (IEA 2023), so specs that emphasize whole-life performance can narrow vendor pools or expand them to specialists. Data-backed performance gives buyers negotiating leverage while enabling contractors to capture premiums for verified lifecycle savings.

- Lifecycle specs expand specialist vendors

- Value engineering can beat low-bid selection

- Verified performance creates buyer leverage and premium pricing

Institutional buyers force transparency and value-based procurement, squeezing CM margins

Experienced institutional buyers drive price sensitivity, demand transparency and shift downside risk via competitive RFPs and method shopping, compressing CM margins. Large, multi‑phase pipelines and bundled work (US put‑in‑place ≈ $1.9T in 2024) amplify owner leverage; lifecycle specs (buildings ≈ 37% of energy‑related CO2, IEA 2023) shift decisions to value over lowest bid.

| Metric | Value |

|---|---|

| US construction put‑in‑place | $1.9T (2024) |

| Buildings share of CO2 | ≈37% (IEA 2023) |

Preview the Actual Deliverable

Consigli Construction Porter's Five Forces Analysis

This preview shows the exact Consigli Construction Porter's Five Forces Analysis you'll receive—fully written, formatted, and ready to use. It contains the complete competitive assessment, implications, and actionable insights. No samples or placeholders; purchase grants instant access to this identical file.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Consigli Construction faces moderate supplier leverage, high buyer expectations for quality and timeliness, and steady rivalry from regional contractors, while barriers to new entrants remain significant due to reputation and bonding requirements. Substitutes are limited but technology-driven delivery models pose emerging threats. This snapshot highlights key pressures; unlock the full Porter's Five Forces Analysis for a force-by-force breakdown and actionable strategy guidance.

Suppliers Bargaining Power

Specialty trade concentration

Complex healthcare and life-science projects rely on scarce MEP, cleanroom, and commissioning specialists, creating supplier concentration that limits options. Limited qualified subs can command premium pricing and favorable terms, and 86% of contractors reported hiring difficulty in the AGC 2024 workforce survey. Consigli mitigates risk via preferred networks and early trade partner engagement, but bottlenecks still elevate schedule and cost risk.

Key materials volatility

Key inputs — steel HRC spot near USD 800/ton in 2024, cement prices up about 6% YoY (2024), architectural glass lead times of 12–20 weeks and advanced envelope systems commanding 10–25% price premiums — are price- and lead-time sensitive; suppliers gain bargaining power during commodity spikes or logistics disruptions, and early procurement/hedging mitigate but do not transfer all risk, while sustainable specs further narrow supplier options.

Union labor and wage dynamics

Union agreements and prevailing wage rules (Davis-Bacon on federal jobs and prevailing-wage rules covering roughly 10% of projects) set clear floors on labor costs for Consigli; unionized construction workforce ~13% in 2024. In tight labor markets with construction unemployment near 5% in 2024, skilled trades gain leverage to push rates higher. Workforce development and long-term relations (apprenticeship growth ~15% since 2020) stabilize availability while complex projects increase reliance on top-tier crews.

Green and high-performance products

- Fewer compliant vendors increase pricing and lead‑time power

- Prequalify multiple sustainable suppliers to reduce risk

- Design flexibility offsets supplier leverage

- Owner mandates can restrict substitution

Digital tools and equipment providers

Digital tools (BIM, VDC, reality-capture) create ecosystem dependencies for Consigli as proprietary formats and vendor-specific training raise switching costs; IFC is an open standard maintained by buildingSMART that can reduce that lock-in. Standardizing workflows and requiring open formats in contracts curbs vendor power, while heavy use of equipment rental markets provides short-term leverage on fast-track jobs.

- IFC=open standard (buildingSMART)

- Proprietary formats=increased switching costs

- Standardization=open-standards reduce vendor power

- Equipment rental=leverage on fast-track projects

Supply concentration, tight labor boost construction costs; 86% report hiring difficulty

Supplier concentration for MEP/cleanroom specialists and proprietary digital vendors raises pricing and switching costs; 86% of contractors reported hiring difficulty (AGC 2024). Key inputs: HRC steel ~USD 800/ton (2024), cement +6% YoY (2024), glass 12–20 wk lead. Unionized workforce ~13% and construction unemployment ~5% (2024) tighten labor supply.

| Metric | 2024 |

|---|---|

| Hiring difficulty | 86% |

| HRC steel | ~USD 800/ton |

| Cement YoY | +6% |

| Glass lead | 12–20 wk |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Consigli Construction. Evaluates control held by suppliers and buyers and identifies disruptive substitutes threatening market share.

Clear one-sheet Porter's Five Forces for Consigli Construction—instantly reveals competitive pressures with a customizable radar chart so teams can model scenarios, swap in your data, and export clean slides for boardrooms without macros or coding.

Customers Bargaining Power

Sophisticated institutional owners

Universities, hospitals and labs employ experienced procurement teams that insist on full transparency, detailed preconstruction deliverables and robust performance guarantees such as payment and performance bonds. Their technical expertise raises price sensitivity and enforces strict scope discipline, reducing change-order risk. Long-term campus pipelines, often planned over 5–10 years, preferentially award repeat work to proven partners.

Competitive RFP and CM-at-Risk bids

In 2024 formal RFPs and competitive CM-at-risk bids benchmark fee, GC and contingency structures across multiple CMs, compressing margins and shifting more downside risk to the contractor. Differentiation for Consigli therefore rests on demonstrable schedule certainty and high-value constructability input. Clear win themes in life sciences—repeatable lab fit-out expertise and validation experience—help offset price pressure from tightly contested RFPs.

Project scale and bundling

Large, multi-phase programs give owners leverage via volume, allowing consolidation across projects against a U.S. construction spend of about $1.9 trillion in 2023–24 (Census Bureau). Bundled work routinely extracts discounts and preferred payment or warranty terms, while buyers typically require dedicated teams and guaranteed capacity windows. Strong on-time, on-budget performance converts that negotiating power into repeat awards.

Delivery method choices

Owners toggle between CM, design-build, IPD and P3 to shift risk and control, enabling method shopping that raises buyer bargaining power; U.S. construction put-in-place reached about $1.9 trillion in 2024, amplifying owner leverage across large programs. Consigli must tailor value propositions by delivery method and pursue early engagement to lock influence before price-only selection stages.

Sustainability and lifecycle priorities

Buyers increasingly prioritize energy, carbon, and total cost of ownership outcomes, shifting decisions from lowest bid to lifecycle value; buildings and construction account for about 37% of energy-related CO2 emissions (IEA 2023), so specs that emphasize whole-life performance can narrow vendor pools or expand them to specialists. Data-backed performance gives buyers negotiating leverage while enabling contractors to capture premiums for verified lifecycle savings.

- Lifecycle specs expand specialist vendors

- Value engineering can beat low-bid selection

- Verified performance creates buyer leverage and premium pricing

Institutional buyers force transparency and value-based procurement, squeezing CM margins

Experienced institutional buyers drive price sensitivity, demand transparency and shift downside risk via competitive RFPs and method shopping, compressing CM margins. Large, multi‑phase pipelines and bundled work (US put‑in‑place ≈ $1.9T in 2024) amplify owner leverage; lifecycle specs (buildings ≈ 37% of energy‑related CO2, IEA 2023) shift decisions to value over lowest bid.

| Metric | Value |

|---|---|

| US construction put‑in‑place | $1.9T (2024) |

| Buildings share of CO2 | ≈37% (IEA 2023) |

Preview the Actual Deliverable

Consigli Construction Porter's Five Forces Analysis

This preview shows the exact Consigli Construction Porter's Five Forces Analysis you'll receive—fully written, formatted, and ready to use. It contains the complete competitive assessment, implications, and actionable insights. No samples or placeholders; purchase grants instant access to this identical file.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Consigli Construction faces moderate supplier leverage, high buyer expectations for quality and timeliness, and steady rivalry from regional contractors, while barriers to new entrants remain significant due to reputation and bonding requirements. Substitutes are limited but technology-driven delivery models pose emerging threats. This snapshot highlights key pressures; unlock the full Porter's Five Forces Analysis for a force-by-force breakdown and actionable strategy guidance.

Suppliers Bargaining Power

Specialty trade concentration

Complex healthcare and life-science projects rely on scarce MEP, cleanroom, and commissioning specialists, creating supplier concentration that limits options. Limited qualified subs can command premium pricing and favorable terms, and 86% of contractors reported hiring difficulty in the AGC 2024 workforce survey. Consigli mitigates risk via preferred networks and early trade partner engagement, but bottlenecks still elevate schedule and cost risk.

Key materials volatility

Key inputs — steel HRC spot near USD 800/ton in 2024, cement prices up about 6% YoY (2024), architectural glass lead times of 12–20 weeks and advanced envelope systems commanding 10–25% price premiums — are price- and lead-time sensitive; suppliers gain bargaining power during commodity spikes or logistics disruptions, and early procurement/hedging mitigate but do not transfer all risk, while sustainable specs further narrow supplier options.

Union labor and wage dynamics

Union agreements and prevailing wage rules (Davis-Bacon on federal jobs and prevailing-wage rules covering roughly 10% of projects) set clear floors on labor costs for Consigli; unionized construction workforce ~13% in 2024. In tight labor markets with construction unemployment near 5% in 2024, skilled trades gain leverage to push rates higher. Workforce development and long-term relations (apprenticeship growth ~15% since 2020) stabilize availability while complex projects increase reliance on top-tier crews.

Green and high-performance products

- Fewer compliant vendors increase pricing and lead‑time power

- Prequalify multiple sustainable suppliers to reduce risk

- Design flexibility offsets supplier leverage

- Owner mandates can restrict substitution

Digital tools and equipment providers

Digital tools (BIM, VDC, reality-capture) create ecosystem dependencies for Consigli as proprietary formats and vendor-specific training raise switching costs; IFC is an open standard maintained by buildingSMART that can reduce that lock-in. Standardizing workflows and requiring open formats in contracts curbs vendor power, while heavy use of equipment rental markets provides short-term leverage on fast-track jobs.

- IFC=open standard (buildingSMART)

- Proprietary formats=increased switching costs

- Standardization=open-standards reduce vendor power

- Equipment rental=leverage on fast-track projects

Supply concentration, tight labor boost construction costs; 86% report hiring difficulty

Supplier concentration for MEP/cleanroom specialists and proprietary digital vendors raises pricing and switching costs; 86% of contractors reported hiring difficulty (AGC 2024). Key inputs: HRC steel ~USD 800/ton (2024), cement +6% YoY (2024), glass 12–20 wk lead. Unionized workforce ~13% and construction unemployment ~5% (2024) tighten labor supply.

| Metric | 2024 |

|---|---|

| Hiring difficulty | 86% |

| HRC steel | ~USD 800/ton |

| Cement YoY | +6% |

| Glass lead | 12–20 wk |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Consigli Construction. Evaluates control held by suppliers and buyers and identifies disruptive substitutes threatening market share.

Clear one-sheet Porter's Five Forces for Consigli Construction—instantly reveals competitive pressures with a customizable radar chart so teams can model scenarios, swap in your data, and export clean slides for boardrooms without macros or coding.

Customers Bargaining Power

Sophisticated institutional owners

Universities, hospitals and labs employ experienced procurement teams that insist on full transparency, detailed preconstruction deliverables and robust performance guarantees such as payment and performance bonds. Their technical expertise raises price sensitivity and enforces strict scope discipline, reducing change-order risk. Long-term campus pipelines, often planned over 5–10 years, preferentially award repeat work to proven partners.

Competitive RFP and CM-at-Risk bids

In 2024 formal RFPs and competitive CM-at-risk bids benchmark fee, GC and contingency structures across multiple CMs, compressing margins and shifting more downside risk to the contractor. Differentiation for Consigli therefore rests on demonstrable schedule certainty and high-value constructability input. Clear win themes in life sciences—repeatable lab fit-out expertise and validation experience—help offset price pressure from tightly contested RFPs.

Project scale and bundling

Large, multi-phase programs give owners leverage via volume, allowing consolidation across projects against a U.S. construction spend of about $1.9 trillion in 2023–24 (Census Bureau). Bundled work routinely extracts discounts and preferred payment or warranty terms, while buyers typically require dedicated teams and guaranteed capacity windows. Strong on-time, on-budget performance converts that negotiating power into repeat awards.

Delivery method choices

Owners toggle between CM, design-build, IPD and P3 to shift risk and control, enabling method shopping that raises buyer bargaining power; U.S. construction put-in-place reached about $1.9 trillion in 2024, amplifying owner leverage across large programs. Consigli must tailor value propositions by delivery method and pursue early engagement to lock influence before price-only selection stages.

Sustainability and lifecycle priorities

Buyers increasingly prioritize energy, carbon, and total cost of ownership outcomes, shifting decisions from lowest bid to lifecycle value; buildings and construction account for about 37% of energy-related CO2 emissions (IEA 2023), so specs that emphasize whole-life performance can narrow vendor pools or expand them to specialists. Data-backed performance gives buyers negotiating leverage while enabling contractors to capture premiums for verified lifecycle savings.

- Lifecycle specs expand specialist vendors

- Value engineering can beat low-bid selection

- Verified performance creates buyer leverage and premium pricing

Institutional buyers force transparency and value-based procurement, squeezing CM margins

Experienced institutional buyers drive price sensitivity, demand transparency and shift downside risk via competitive RFPs and method shopping, compressing CM margins. Large, multi‑phase pipelines and bundled work (US put‑in‑place ≈ $1.9T in 2024) amplify owner leverage; lifecycle specs (buildings ≈ 37% of energy‑related CO2, IEA 2023) shift decisions to value over lowest bid.

| Metric | Value |

|---|---|

| US construction put‑in‑place | $1.9T (2024) |

| Buildings share of CO2 | ≈37% (IEA 2023) |

Preview the Actual Deliverable

Consigli Construction Porter's Five Forces Analysis

This preview shows the exact Consigli Construction Porter's Five Forces Analysis you'll receive—fully written, formatted, and ready to use. It contains the complete competitive assessment, implications, and actionable insights. No samples or placeholders; purchase grants instant access to this identical file.