Constellium Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

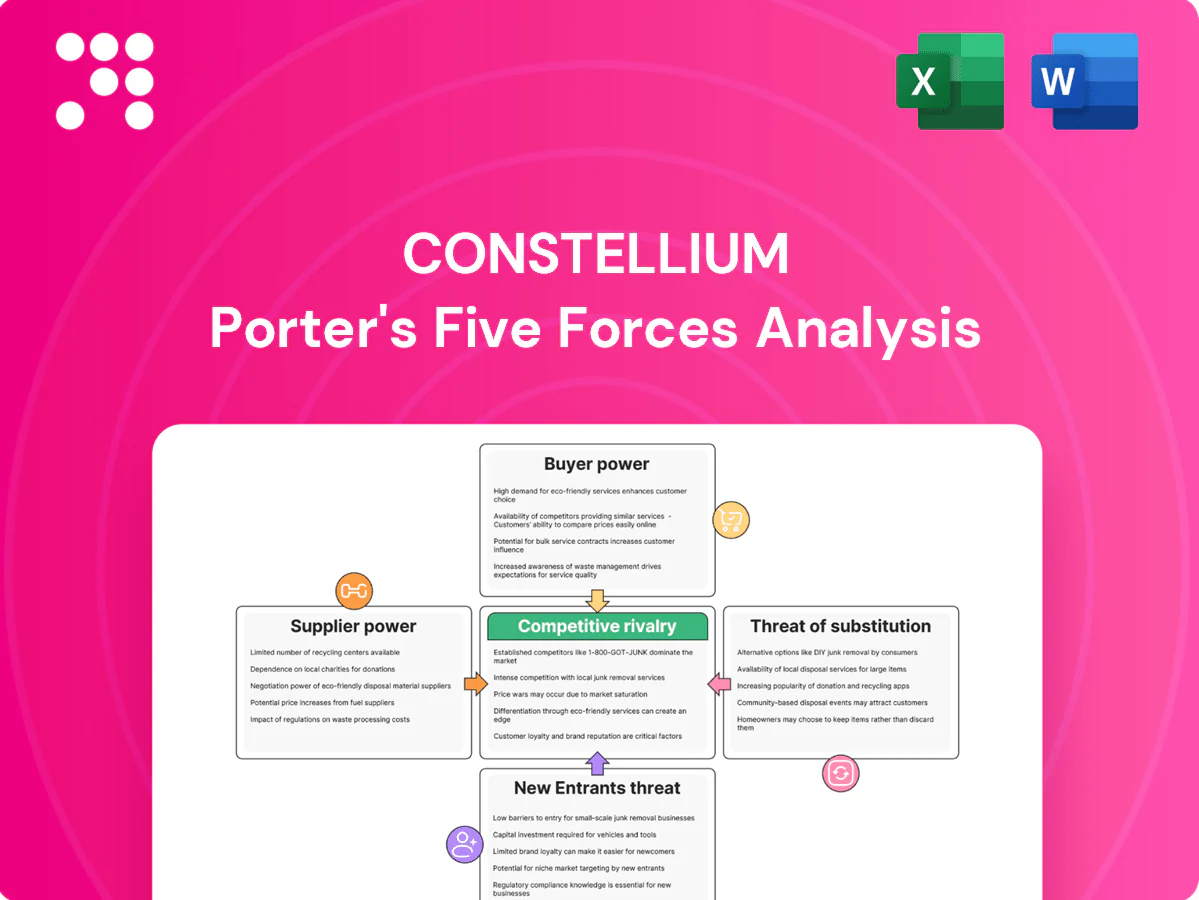

Constellium faces moderate supplier power, cyclical buyer demand, and intense rivalry from global aluminum players, while substitutes and new entrants pose limited but evolving risks; strategic positioning hinges on innovation and downstream integration. This brief snapshot only scratches the surface — unlock the full Porter's Five Forces Analysis to explore Constellium’s competitive dynamics and market pressures in detail.

Suppliers Bargaining Power

Concentrated raw materials

Alumina, specialty alloying elements and carbon anodes are sourced from a concentrated global base—top 5 suppliers control over 60% of capacity—giving suppliers leverage. Energy, especially electricity (≈30% of smelter cost), raises concentration risk in Europe and North America. Constellium mitigates via multi-sourcing and long-term contracts but remains exposed to input-price shocks and transport/logistics bottlenecks that can amplify supplier bargaining power.

Energy intensity exposure

Smelting, rolling and recycling remain highly energy intensive: primary aluminum uses roughly 14–16 MWh/tonne while secondary recycling consumes about 5% of that, making power utilities pivotal suppliers. Electricity can represent 20–40% of production cash costs and 2024 EU carbon prices averaged near €88/t CO2, squeezing margins. Hedging and renewable PPAs lower but do not eliminate exposure, and regional policy and power-price gaps (e.g., EU vs US) shift supplier leverage at key sites.

Specialty alloy inputs

Magnesium, lithium and specialty alloying elements are supplied by niche producers—China accounted for >80% of refined magnesium and ~70% of lithium chemical processing in 2024—limiting alternatives; tight purity/certification specs restrict substitution; 2022–24 price and supply volatility and geopolitical constraints can rapidly tighten access; strategic inventories and increased recycling/backward integration mitigate but do not eliminate supply risk.

Equipment and maintenance vendors

Equipment and maintenance vendors for hot/cold mills, extrusion presses and furnaces are few and highly specialized, creating supplier concentration and elevated switching costs; long lead times and proprietary spare parts intensify Constelliums dependence while service agreements often embed pricing power for OEMs.

- specialized OEM concentration

- long lead times, proprietary parts

- service agreements = vendor pricing power

- in-house maintenance partially offsets pressure

Scrap and recycling feedstock

High-quality segregated scrap is increasingly sought in 2024 as circularity drives demand; recycled aluminum delivers up to 95% energy savings versus primary metal, boosting competition for clean feedstock. Scrap merchants can command premiums when collection tightens, while closed-loop OEM programs reduce Constelliums exposure to merchant markets; quality variability still impacts yields and operating costs.

- 2024 global primary aluminum ~67 Mt

- Recycled metal saves up to 95% energy

- Closed-loop reduces merchant price exposure

- Quality variability raises yield and cost risk

Supplier concentration, China dominance and carbon costs tighten magnesium supply economics

Suppliers hold meaningful leverage: top‑5 input providers >60% capacity and China >80% refined magnesium, limiting alternatives. Electricity ≈30% of smelter costs and 2024 EU carbon ≈€88/t raise input-price risk. Recycling (~95% energy savings) and long‑term contracts/PPAs mitigate but do not remove exposure.

| Metric | 2024 |

|---|---|

| Global primary Al | ≈67 Mt |

| Top‑5 supplier share | >60% |

| EU carbon price | ≈€88/t |

What is included in the product

Tailored Porter's Five Forces analysis for Constellium that uncovers key drivers of competition, buyer and supplier influence on pricing and profitability, evaluates barriers to entry and incumbency protection, and identifies disruptive threats and substitutes challenging the company’s market share.

One-sheet Porter’s Five Forces for Constellium—condenses competitive pressures into a clean radar chart for quick strategic decisions; customize force levels and swap your data to model scenarios without macros, ready for decks or integration into broader reports.

Customers Bargaining Power

Large OEM concentration

Aerospace primes such as Airbus and Boeing, major auto OEMs and Tier‑1s (Toyota, Volkswagen, Stellantis) and global canmakers (Ball, Crown) are sizable, sophisticated buyers that concentrate volume and command strong price and contract leverage. Rigorous qualification processes create supplier stickiness yet amplify procurement power during renewals. Deep relationships and tight performance KPIs (on-time delivery, scrap rates, alloy specs) directly determine share allocations.

Contracting and pass-throughs

Long-term contracts with LME pass-throughs limit Constellium’s price risk but compress value-add margins; in 2024 LME aluminum averaged about $2,200/t while Constellium reported roughly €6.2bn revenue, highlighting scale but thining per-unit returns. Customers push index-linked surcharges and service-level penalties, and volume commitments are often traded for better pricing. Renegotiation cycles expose Constellium to intense buyer pressure in downturns.

High switching costs

Material qualification in aerospace and safety-critical auto typically takes 12–36 months and tooling investments often exceed $10m, making switching slow and costly for buyers. Regulatory approvals from authorities like FAA and EASA further lock incumbents and curb day-to-day buyer leverage. OEMs still pursue dual-sourcing to preserve competitive tension, and supplier performance lapses can drive multi-year share shifts over time.

Customization and co-development

Constellium (NYSE: CSTM) embeds advanced alloys and engineered solutions into customer programs via customization and co-development, increasing client dependence and raising switching barriers through integrated designs and qualification processes. Co-development invites buyer requests for IP-sharing and life-of-program cost-downs, pressuring margins while locking in orders. Service quality, lead-time performance and sustainability metrics now materially influence award decisions in 2024.

- Customization increases switching costs

- Buyers pursue IP access and cost-downs

- Service, lead-time, sustainability drive awards

- Constellium (NYSE: CSTM) central in aerospace/auto programs

Sustainability and traceability demands

Customers increasingly demand low-CO2 and recycled-content aluminum; recycled aluminum uses up to 95% less energy than primary, shifting certification and traceability costs to suppliers and strengthening buyer leverage. EU CBAM reporting (2024) and rising Scope 3 commitments make low-carbon credentials a purchase qualifier; failure to meet ESG specs risks losing contracts despite technical fit.

- Buyer leverage: certification/compliance costs

- Differentiator: Scope 3 alignment

- Risk: contract loss if ESG gaps

OEMs & canmakers concentrate vol; LME $2,200/t protects cash; recycled aluminum saves ≈95% energy

Large OEMs and canmakers concentrate volume and exert strong price/contract leverage; qualification and tooling (12–36 months) raise switching costs. LME pass-throughs (LME ≈ $2,200/t in 2024) protect cash but compress margins; Constellium revenue ≈ €6.2bn (2024). ESG/supply-chain rules (EU CBAM 2024) and demand for low‑CO2/recycled (up to 95% less energy) increase buyer bargaining power.

| Metric | Value (2024) |

|---|---|

| LME price | $2,200/t |

| Constellium revenue | €6.2bn |

| Qualification time | 12–36 months |

| Recycled energy saving | ≈95% |

| Regulation | EU CBAM (2024) |

Full Version Awaits

Constellium Porter's Five Forces Analysis

This preview shows the exact Constellium Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The file is the final, fully formatted document ready for download and use the moment you buy. You're viewing the actual deliverable, complete and professional with actionable insights.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Constellium faces moderate supplier power, cyclical buyer demand, and intense rivalry from global aluminum players, while substitutes and new entrants pose limited but evolving risks; strategic positioning hinges on innovation and downstream integration. This brief snapshot only scratches the surface — unlock the full Porter's Five Forces Analysis to explore Constellium’s competitive dynamics and market pressures in detail.

Suppliers Bargaining Power

Concentrated raw materials

Alumina, specialty alloying elements and carbon anodes are sourced from a concentrated global base—top 5 suppliers control over 60% of capacity—giving suppliers leverage. Energy, especially electricity (≈30% of smelter cost), raises concentration risk in Europe and North America. Constellium mitigates via multi-sourcing and long-term contracts but remains exposed to input-price shocks and transport/logistics bottlenecks that can amplify supplier bargaining power.

Energy intensity exposure

Smelting, rolling and recycling remain highly energy intensive: primary aluminum uses roughly 14–16 MWh/tonne while secondary recycling consumes about 5% of that, making power utilities pivotal suppliers. Electricity can represent 20–40% of production cash costs and 2024 EU carbon prices averaged near €88/t CO2, squeezing margins. Hedging and renewable PPAs lower but do not eliminate exposure, and regional policy and power-price gaps (e.g., EU vs US) shift supplier leverage at key sites.

Specialty alloy inputs

Magnesium, lithium and specialty alloying elements are supplied by niche producers—China accounted for >80% of refined magnesium and ~70% of lithium chemical processing in 2024—limiting alternatives; tight purity/certification specs restrict substitution; 2022–24 price and supply volatility and geopolitical constraints can rapidly tighten access; strategic inventories and increased recycling/backward integration mitigate but do not eliminate supply risk.

Equipment and maintenance vendors

Equipment and maintenance vendors for hot/cold mills, extrusion presses and furnaces are few and highly specialized, creating supplier concentration and elevated switching costs; long lead times and proprietary spare parts intensify Constelliums dependence while service agreements often embed pricing power for OEMs.

- specialized OEM concentration

- long lead times, proprietary parts

- service agreements = vendor pricing power

- in-house maintenance partially offsets pressure

Scrap and recycling feedstock

High-quality segregated scrap is increasingly sought in 2024 as circularity drives demand; recycled aluminum delivers up to 95% energy savings versus primary metal, boosting competition for clean feedstock. Scrap merchants can command premiums when collection tightens, while closed-loop OEM programs reduce Constelliums exposure to merchant markets; quality variability still impacts yields and operating costs.

- 2024 global primary aluminum ~67 Mt

- Recycled metal saves up to 95% energy

- Closed-loop reduces merchant price exposure

- Quality variability raises yield and cost risk

Supplier concentration, China dominance and carbon costs tighten magnesium supply economics

Suppliers hold meaningful leverage: top‑5 input providers >60% capacity and China >80% refined magnesium, limiting alternatives. Electricity ≈30% of smelter costs and 2024 EU carbon ≈€88/t raise input-price risk. Recycling (~95% energy savings) and long‑term contracts/PPAs mitigate but do not remove exposure.

| Metric | 2024 |

|---|---|

| Global primary Al | ≈67 Mt |

| Top‑5 supplier share | >60% |

| EU carbon price | ≈€88/t |

What is included in the product

Tailored Porter's Five Forces analysis for Constellium that uncovers key drivers of competition, buyer and supplier influence on pricing and profitability, evaluates barriers to entry and incumbency protection, and identifies disruptive threats and substitutes challenging the company’s market share.

One-sheet Porter’s Five Forces for Constellium—condenses competitive pressures into a clean radar chart for quick strategic decisions; customize force levels and swap your data to model scenarios without macros, ready for decks or integration into broader reports.

Customers Bargaining Power

Large OEM concentration

Aerospace primes such as Airbus and Boeing, major auto OEMs and Tier‑1s (Toyota, Volkswagen, Stellantis) and global canmakers (Ball, Crown) are sizable, sophisticated buyers that concentrate volume and command strong price and contract leverage. Rigorous qualification processes create supplier stickiness yet amplify procurement power during renewals. Deep relationships and tight performance KPIs (on-time delivery, scrap rates, alloy specs) directly determine share allocations.

Contracting and pass-throughs

Long-term contracts with LME pass-throughs limit Constellium’s price risk but compress value-add margins; in 2024 LME aluminum averaged about $2,200/t while Constellium reported roughly €6.2bn revenue, highlighting scale but thining per-unit returns. Customers push index-linked surcharges and service-level penalties, and volume commitments are often traded for better pricing. Renegotiation cycles expose Constellium to intense buyer pressure in downturns.

High switching costs

Material qualification in aerospace and safety-critical auto typically takes 12–36 months and tooling investments often exceed $10m, making switching slow and costly for buyers. Regulatory approvals from authorities like FAA and EASA further lock incumbents and curb day-to-day buyer leverage. OEMs still pursue dual-sourcing to preserve competitive tension, and supplier performance lapses can drive multi-year share shifts over time.

Customization and co-development

Constellium (NYSE: CSTM) embeds advanced alloys and engineered solutions into customer programs via customization and co-development, increasing client dependence and raising switching barriers through integrated designs and qualification processes. Co-development invites buyer requests for IP-sharing and life-of-program cost-downs, pressuring margins while locking in orders. Service quality, lead-time performance and sustainability metrics now materially influence award decisions in 2024.

- Customization increases switching costs

- Buyers pursue IP access and cost-downs

- Service, lead-time, sustainability drive awards

- Constellium (NYSE: CSTM) central in aerospace/auto programs

Sustainability and traceability demands

Customers increasingly demand low-CO2 and recycled-content aluminum; recycled aluminum uses up to 95% less energy than primary, shifting certification and traceability costs to suppliers and strengthening buyer leverage. EU CBAM reporting (2024) and rising Scope 3 commitments make low-carbon credentials a purchase qualifier; failure to meet ESG specs risks losing contracts despite technical fit.

- Buyer leverage: certification/compliance costs

- Differentiator: Scope 3 alignment

- Risk: contract loss if ESG gaps

OEMs & canmakers concentrate vol; LME $2,200/t protects cash; recycled aluminum saves ≈95% energy

Large OEMs and canmakers concentrate volume and exert strong price/contract leverage; qualification and tooling (12–36 months) raise switching costs. LME pass-throughs (LME ≈ $2,200/t in 2024) protect cash but compress margins; Constellium revenue ≈ €6.2bn (2024). ESG/supply-chain rules (EU CBAM 2024) and demand for low‑CO2/recycled (up to 95% less energy) increase buyer bargaining power.

| Metric | Value (2024) |

|---|---|

| LME price | $2,200/t |

| Constellium revenue | €6.2bn |

| Qualification time | 12–36 months |

| Recycled energy saving | ≈95% |

| Regulation | EU CBAM (2024) |

Full Version Awaits

Constellium Porter's Five Forces Analysis

This preview shows the exact Constellium Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The file is the final, fully formatted document ready for download and use the moment you buy. You're viewing the actual deliverable, complete and professional with actionable insights.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Constellium faces moderate supplier power, cyclical buyer demand, and intense rivalry from global aluminum players, while substitutes and new entrants pose limited but evolving risks; strategic positioning hinges on innovation and downstream integration. This brief snapshot only scratches the surface — unlock the full Porter's Five Forces Analysis to explore Constellium’s competitive dynamics and market pressures in detail.

Suppliers Bargaining Power

Concentrated raw materials

Alumina, specialty alloying elements and carbon anodes are sourced from a concentrated global base—top 5 suppliers control over 60% of capacity—giving suppliers leverage. Energy, especially electricity (≈30% of smelter cost), raises concentration risk in Europe and North America. Constellium mitigates via multi-sourcing and long-term contracts but remains exposed to input-price shocks and transport/logistics bottlenecks that can amplify supplier bargaining power.

Energy intensity exposure

Smelting, rolling and recycling remain highly energy intensive: primary aluminum uses roughly 14–16 MWh/tonne while secondary recycling consumes about 5% of that, making power utilities pivotal suppliers. Electricity can represent 20–40% of production cash costs and 2024 EU carbon prices averaged near €88/t CO2, squeezing margins. Hedging and renewable PPAs lower but do not eliminate exposure, and regional policy and power-price gaps (e.g., EU vs US) shift supplier leverage at key sites.

Specialty alloy inputs

Magnesium, lithium and specialty alloying elements are supplied by niche producers—China accounted for >80% of refined magnesium and ~70% of lithium chemical processing in 2024—limiting alternatives; tight purity/certification specs restrict substitution; 2022–24 price and supply volatility and geopolitical constraints can rapidly tighten access; strategic inventories and increased recycling/backward integration mitigate but do not eliminate supply risk.

Equipment and maintenance vendors

Equipment and maintenance vendors for hot/cold mills, extrusion presses and furnaces are few and highly specialized, creating supplier concentration and elevated switching costs; long lead times and proprietary spare parts intensify Constelliums dependence while service agreements often embed pricing power for OEMs.

- specialized OEM concentration

- long lead times, proprietary parts

- service agreements = vendor pricing power

- in-house maintenance partially offsets pressure

Scrap and recycling feedstock

High-quality segregated scrap is increasingly sought in 2024 as circularity drives demand; recycled aluminum delivers up to 95% energy savings versus primary metal, boosting competition for clean feedstock. Scrap merchants can command premiums when collection tightens, while closed-loop OEM programs reduce Constelliums exposure to merchant markets; quality variability still impacts yields and operating costs.

- 2024 global primary aluminum ~67 Mt

- Recycled metal saves up to 95% energy

- Closed-loop reduces merchant price exposure

- Quality variability raises yield and cost risk

Supplier concentration, China dominance and carbon costs tighten magnesium supply economics

Suppliers hold meaningful leverage: top‑5 input providers >60% capacity and China >80% refined magnesium, limiting alternatives. Electricity ≈30% of smelter costs and 2024 EU carbon ≈€88/t raise input-price risk. Recycling (~95% energy savings) and long‑term contracts/PPAs mitigate but do not remove exposure.

| Metric | 2024 |

|---|---|

| Global primary Al | ≈67 Mt |

| Top‑5 supplier share | >60% |

| EU carbon price | ≈€88/t |

What is included in the product

Tailored Porter's Five Forces analysis for Constellium that uncovers key drivers of competition, buyer and supplier influence on pricing and profitability, evaluates barriers to entry and incumbency protection, and identifies disruptive threats and substitutes challenging the company’s market share.

One-sheet Porter’s Five Forces for Constellium—condenses competitive pressures into a clean radar chart for quick strategic decisions; customize force levels and swap your data to model scenarios without macros, ready for decks or integration into broader reports.

Customers Bargaining Power

Large OEM concentration

Aerospace primes such as Airbus and Boeing, major auto OEMs and Tier‑1s (Toyota, Volkswagen, Stellantis) and global canmakers (Ball, Crown) are sizable, sophisticated buyers that concentrate volume and command strong price and contract leverage. Rigorous qualification processes create supplier stickiness yet amplify procurement power during renewals. Deep relationships and tight performance KPIs (on-time delivery, scrap rates, alloy specs) directly determine share allocations.

Contracting and pass-throughs

Long-term contracts with LME pass-throughs limit Constellium’s price risk but compress value-add margins; in 2024 LME aluminum averaged about $2,200/t while Constellium reported roughly €6.2bn revenue, highlighting scale but thining per-unit returns. Customers push index-linked surcharges and service-level penalties, and volume commitments are often traded for better pricing. Renegotiation cycles expose Constellium to intense buyer pressure in downturns.

High switching costs

Material qualification in aerospace and safety-critical auto typically takes 12–36 months and tooling investments often exceed $10m, making switching slow and costly for buyers. Regulatory approvals from authorities like FAA and EASA further lock incumbents and curb day-to-day buyer leverage. OEMs still pursue dual-sourcing to preserve competitive tension, and supplier performance lapses can drive multi-year share shifts over time.

Customization and co-development

Constellium (NYSE: CSTM) embeds advanced alloys and engineered solutions into customer programs via customization and co-development, increasing client dependence and raising switching barriers through integrated designs and qualification processes. Co-development invites buyer requests for IP-sharing and life-of-program cost-downs, pressuring margins while locking in orders. Service quality, lead-time performance and sustainability metrics now materially influence award decisions in 2024.

- Customization increases switching costs

- Buyers pursue IP access and cost-downs

- Service, lead-time, sustainability drive awards

- Constellium (NYSE: CSTM) central in aerospace/auto programs

Sustainability and traceability demands

Customers increasingly demand low-CO2 and recycled-content aluminum; recycled aluminum uses up to 95% less energy than primary, shifting certification and traceability costs to suppliers and strengthening buyer leverage. EU CBAM reporting (2024) and rising Scope 3 commitments make low-carbon credentials a purchase qualifier; failure to meet ESG specs risks losing contracts despite technical fit.

- Buyer leverage: certification/compliance costs

- Differentiator: Scope 3 alignment

- Risk: contract loss if ESG gaps

OEMs & canmakers concentrate vol; LME $2,200/t protects cash; recycled aluminum saves ≈95% energy

Large OEMs and canmakers concentrate volume and exert strong price/contract leverage; qualification and tooling (12–36 months) raise switching costs. LME pass-throughs (LME ≈ $2,200/t in 2024) protect cash but compress margins; Constellium revenue ≈ €6.2bn (2024). ESG/supply-chain rules (EU CBAM 2024) and demand for low‑CO2/recycled (up to 95% less energy) increase buyer bargaining power.

| Metric | Value (2024) |

|---|---|

| LME price | $2,200/t |

| Constellium revenue | €6.2bn |

| Qualification time | 12–36 months |

| Recycled energy saving | ≈95% |

| Regulation | EU CBAM (2024) |

Full Version Awaits

Constellium Porter's Five Forces Analysis

This preview shows the exact Constellium Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The file is the final, fully formatted document ready for download and use the moment you buy. You're viewing the actual deliverable, complete and professional with actionable insights.