Consti Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

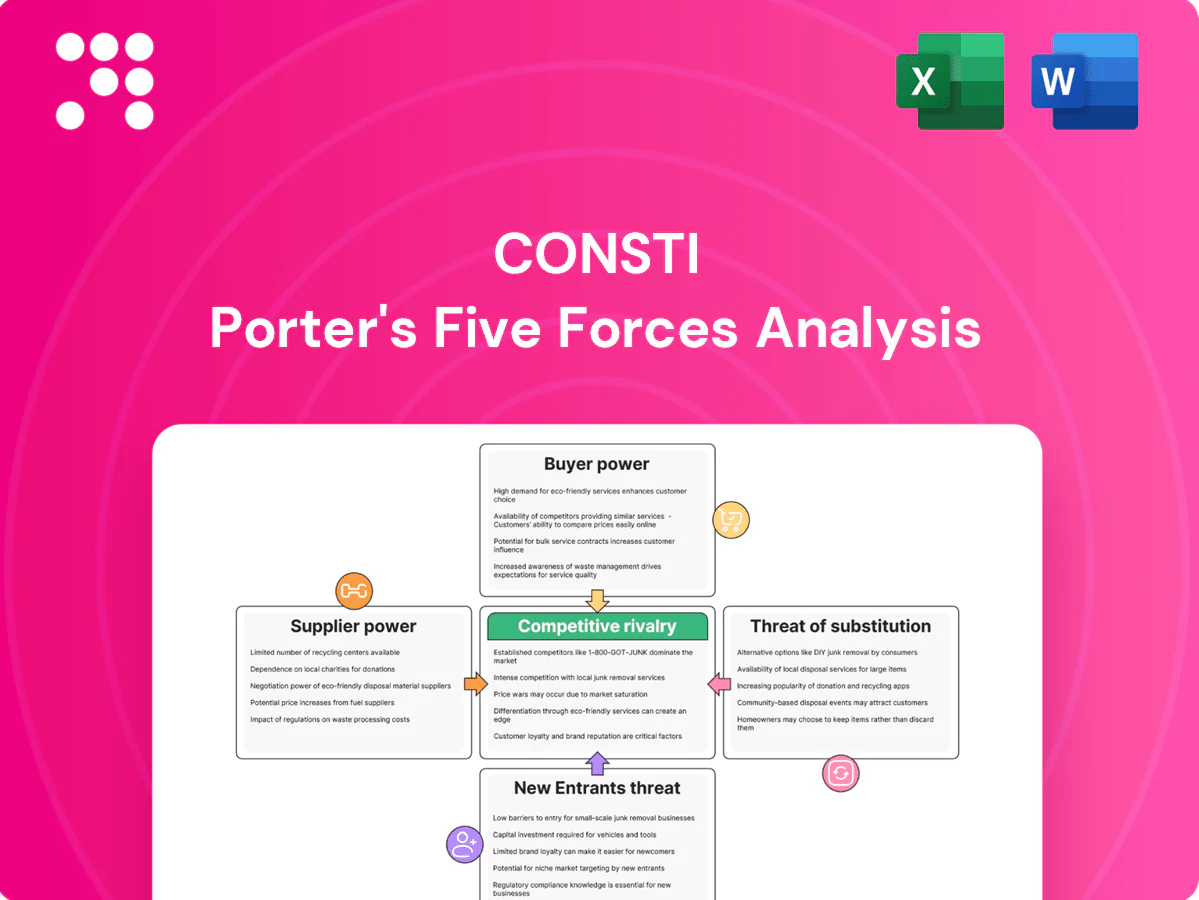

Consti’s Porter's Five Forces snapshot highlights supplier leverage, buyer pressure, substitution risk, entry barriers, and existing competitive rivalry to frame its market position and strategic vulnerabilities. This preview outlines key tensions but omits force-by-force ratings and visuals. The full Porter's Five Forces Analysis reveals detailed impacts, scenarios, and actionable recommendations. Unlock the complete report to inform investment or strategic decisions.

Suppliers Bargaining Power

Specialized building-tech components concentration

HVAC, electrical and control-system components are concentrated among a few OEMs, giving those suppliers leverage on price and lead times. Product compatibility requirements and warranty conditions often lock Consti into specific brands, reducing sourcing flexibility. This concentration raises the risk of project delays and margin pressure when supply tightens. Consti mitigates by qualifying multiple brands and using approved-equivalent specifications.

Subcontractor dependence in peak seasons

Renovation cycles and Nordic seasonality concentrate construction activity in Q2–Q3, increasing reliance on specialist subcontractors (facade, insulation, scaffolding) during peaks. Tight specialist capacity gives subcontractors leverage to seek higher rates or preferential scheduling. Strong quality and safety records limit substitutability. Framework agreements and preferred-partner programs are used to stabilize availability and cost.

Standards and certifications lift switching costs

Compliance with EU Construction Products Regulation 305/2011 and the 2018 EPBD recast (nZEB for new buildings from 2020) narrows Finland’s supplier pool and raises switching costs as new vendors often need approvals under Finnish building code (RakMK), retraining and added documentation; building automation software ecosystems add further lock-in while pre-approved vendor lists preserve compliance and limited optionality.

Framework agreements moderate pricing power

Framework agreements improve visibility and secure volume rebates (2024 procurement surveys report 3–7% typical rebates), aggregating demand across projects lowers spot exposure and tightens terms, though index-linked clauses can pass supplier inflation through to Consti; dual-sourcing within frameworks preserves leverage and mitigates single-supplier risk.

- Rebates: 3–7% (2024)

- Spot exposure: reduced via aggregation

- Inflation pass-through: index clauses risk

- Mitigation: dual-sourcing maintains leverage

Nordic logistics and input price volatility

Nordic weather, port congestion and seasonal transport constraints in 2024 led to intermittent delivery delays and higher freight premiums, increasing supplier leverage over Consti. Commodity volatility—steel and copper price swings and insulation material shortages—eroded margins on fixed-price projects, while EU carbon pricing near €100/t in 2024 raised low-carbon material costs. Early ordering and hedging reduced but did not eliminate input-cost exposure.

- 2024 EU carbon price ≈ €100/t

- Fixed-price margin pressure from commodity swings

- Weather and transport disruptions raise freight premiums

- Early ordering/hedging partially offsets volatility

Supplier power squeezes HVAC margins; frameworks cut spot risk and secure 3-7% rebates

Supplier power is high for OEM HVAC/electrical and niche subcontractors, driving price and lead-time pressure and raising switching costs via compatibility and compliance. Frameworks and dual-sourcing reduce spot exposure and secure 3–7% rebates (2024), but commodity swings and EU carbon near €100/t still squeeze fixed-price margins.

| Metric | 2024 value |

|---|---|

| Supplier rebates | 3–7% |

| EU carbon price | ≈€100/t |

| Spot exposure | Reduced via frameworks |

What is included in the product

Tailored Porter’s Five Forces analysis for Consti uncovering competitive drivers, supplier and buyer power, entry barriers, substitutes and disruptive threats, with strategic commentary to inform investor and management decisions.

Consti Porter's Five Forces delivers a clean one-sheet summary with customizable pressure levels and an instant spider chart—ready to copy into decks or integrate into Excel dashboards, no macros required.

Customers Bargaining Power

Tender-driven procurement pressures pricing

Public and institutional clients drive tender-driven procurement that prioritizes the lowest compliant bid; OECD data shows public procurement equals roughly 12% of GDP, concentrating buying power. Transparent evaluation criteria compress contractor margins—construction EBIT margins averaged about 4% in 2023–24—shifting risk to bidders. Design-build or alliance models can ease change-order risk but remain highly price-sensitive. Strong prequalification increases win odds without forcing below-cost bids.

Concentration of large public and institutional owners

Major municipalities, housing cooperatives and property funds exercise strong buying power, negotiating stringent warranties and service levels and using repeat procurement to press rates and payment terms; in 2024 their concentration in key urban markets amplified leverage, though deep supplier relationships and documented performance history materially mitigate price pressure.

Ability to split scopes and multi-source

Clients increasingly unbundle projects into lots (facade, MEP, automation), inviting multiple bidders and creating direct trade-level competition that reduces reliance on any single contractor. Multi-sourcing raises coordination and warranty risks for buyers while increasing their negotiating leverage on price and terms. To counter fragmentation, integrated providers must demonstrate clear lifecycle savings, lower total cost of ownership, and stronger risk transfer to retain scope.

Outcome-based specs and warranties shift risk

Timing flexibility amid demand cycles

Owners can defer non-critical renovations when markets are tight, allowing Consti to delay price competition; in 2024 industry reports showed renegotiation pressure rising as utilization dipped. In downturns buyers extract concessions while contractors chase utilization, though essential compliance work remains less deferrable and cushions margins. A balanced backlog (around EUR 160m reported in 2024) helps Consti avoid deep price troughs.

- Deferral leverage: owners delay non-critical work

- Buyer concessions: higher in downturns as utilization falls

- Compliance work: more price-inelastic, stabilizes revenue

- Backlog buffer: EUR 160m (2024) moderates price pressure

Public procurement ~12% GDP; EBIT ~4%; backlog EUR 160m

Customers (public + large owners) concentrate buying power—public procurement ~12% of GDP—forcing tender-led pricing; Consti’s peers saw construction EBIT ~4% in 2023–24. Retentions 5–10% and penalties 0.5–2% squeeze cash flow; unbundling increases bidder competition while backlog ~EUR 160m (2024) cushions downside.

| Metric | 2024 |

|---|---|

| Public procurement | ~12% GDP |

| EBIT (sector) | ~4% |

| Retention | 5–10% |

| Penalties | 0.5–2% |

| Consti backlog | EUR 160m |

Full Version Awaits

Consti Porter's Five Forces Analysis

This preview shows the exact Consti Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The document shown is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the final deliverable; purchase grants instant access to this identical file.

Go Beyond the Preview—Access the Full Strategic Report

Consti’s Porter's Five Forces snapshot highlights supplier leverage, buyer pressure, substitution risk, entry barriers, and existing competitive rivalry to frame its market position and strategic vulnerabilities. This preview outlines key tensions but omits force-by-force ratings and visuals. The full Porter's Five Forces Analysis reveals detailed impacts, scenarios, and actionable recommendations. Unlock the complete report to inform investment or strategic decisions.

Suppliers Bargaining Power

Specialized building-tech components concentration

HVAC, electrical and control-system components are concentrated among a few OEMs, giving those suppliers leverage on price and lead times. Product compatibility requirements and warranty conditions often lock Consti into specific brands, reducing sourcing flexibility. This concentration raises the risk of project delays and margin pressure when supply tightens. Consti mitigates by qualifying multiple brands and using approved-equivalent specifications.

Subcontractor dependence in peak seasons

Renovation cycles and Nordic seasonality concentrate construction activity in Q2–Q3, increasing reliance on specialist subcontractors (facade, insulation, scaffolding) during peaks. Tight specialist capacity gives subcontractors leverage to seek higher rates or preferential scheduling. Strong quality and safety records limit substitutability. Framework agreements and preferred-partner programs are used to stabilize availability and cost.

Standards and certifications lift switching costs

Compliance with EU Construction Products Regulation 305/2011 and the 2018 EPBD recast (nZEB for new buildings from 2020) narrows Finland’s supplier pool and raises switching costs as new vendors often need approvals under Finnish building code (RakMK), retraining and added documentation; building automation software ecosystems add further lock-in while pre-approved vendor lists preserve compliance and limited optionality.

Framework agreements moderate pricing power

Framework agreements improve visibility and secure volume rebates (2024 procurement surveys report 3–7% typical rebates), aggregating demand across projects lowers spot exposure and tightens terms, though index-linked clauses can pass supplier inflation through to Consti; dual-sourcing within frameworks preserves leverage and mitigates single-supplier risk.

- Rebates: 3–7% (2024)

- Spot exposure: reduced via aggregation

- Inflation pass-through: index clauses risk

- Mitigation: dual-sourcing maintains leverage

Nordic logistics and input price volatility

Nordic weather, port congestion and seasonal transport constraints in 2024 led to intermittent delivery delays and higher freight premiums, increasing supplier leverage over Consti. Commodity volatility—steel and copper price swings and insulation material shortages—eroded margins on fixed-price projects, while EU carbon pricing near €100/t in 2024 raised low-carbon material costs. Early ordering and hedging reduced but did not eliminate input-cost exposure.

- 2024 EU carbon price ≈ €100/t

- Fixed-price margin pressure from commodity swings

- Weather and transport disruptions raise freight premiums

- Early ordering/hedging partially offsets volatility

Supplier power squeezes HVAC margins; frameworks cut spot risk and secure 3-7% rebates

Supplier power is high for OEM HVAC/electrical and niche subcontractors, driving price and lead-time pressure and raising switching costs via compatibility and compliance. Frameworks and dual-sourcing reduce spot exposure and secure 3–7% rebates (2024), but commodity swings and EU carbon near €100/t still squeeze fixed-price margins.

| Metric | 2024 value |

|---|---|

| Supplier rebates | 3–7% |

| EU carbon price | ≈€100/t |

| Spot exposure | Reduced via frameworks |

What is included in the product

Tailored Porter’s Five Forces analysis for Consti uncovering competitive drivers, supplier and buyer power, entry barriers, substitutes and disruptive threats, with strategic commentary to inform investor and management decisions.

Consti Porter's Five Forces delivers a clean one-sheet summary with customizable pressure levels and an instant spider chart—ready to copy into decks or integrate into Excel dashboards, no macros required.

Customers Bargaining Power

Tender-driven procurement pressures pricing

Public and institutional clients drive tender-driven procurement that prioritizes the lowest compliant bid; OECD data shows public procurement equals roughly 12% of GDP, concentrating buying power. Transparent evaluation criteria compress contractor margins—construction EBIT margins averaged about 4% in 2023–24—shifting risk to bidders. Design-build or alliance models can ease change-order risk but remain highly price-sensitive. Strong prequalification increases win odds without forcing below-cost bids.

Concentration of large public and institutional owners

Major municipalities, housing cooperatives and property funds exercise strong buying power, negotiating stringent warranties and service levels and using repeat procurement to press rates and payment terms; in 2024 their concentration in key urban markets amplified leverage, though deep supplier relationships and documented performance history materially mitigate price pressure.

Ability to split scopes and multi-source

Clients increasingly unbundle projects into lots (facade, MEP, automation), inviting multiple bidders and creating direct trade-level competition that reduces reliance on any single contractor. Multi-sourcing raises coordination and warranty risks for buyers while increasing their negotiating leverage on price and terms. To counter fragmentation, integrated providers must demonstrate clear lifecycle savings, lower total cost of ownership, and stronger risk transfer to retain scope.

Outcome-based specs and warranties shift risk

Timing flexibility amid demand cycles

Owners can defer non-critical renovations when markets are tight, allowing Consti to delay price competition; in 2024 industry reports showed renegotiation pressure rising as utilization dipped. In downturns buyers extract concessions while contractors chase utilization, though essential compliance work remains less deferrable and cushions margins. A balanced backlog (around EUR 160m reported in 2024) helps Consti avoid deep price troughs.

- Deferral leverage: owners delay non-critical work

- Buyer concessions: higher in downturns as utilization falls

- Compliance work: more price-inelastic, stabilizes revenue

- Backlog buffer: EUR 160m (2024) moderates price pressure

Public procurement ~12% GDP; EBIT ~4%; backlog EUR 160m

Customers (public + large owners) concentrate buying power—public procurement ~12% of GDP—forcing tender-led pricing; Consti’s peers saw construction EBIT ~4% in 2023–24. Retentions 5–10% and penalties 0.5–2% squeeze cash flow; unbundling increases bidder competition while backlog ~EUR 160m (2024) cushions downside.

| Metric | 2024 |

|---|---|

| Public procurement | ~12% GDP |

| EBIT (sector) | ~4% |

| Retention | 5–10% |

| Penalties | 0.5–2% |

| Consti backlog | EUR 160m |

Full Version Awaits

Consti Porter's Five Forces Analysis

This preview shows the exact Consti Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The document shown is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the final deliverable; purchase grants instant access to this identical file.

Description

Go Beyond the Preview—Access the Full Strategic Report

Consti’s Porter's Five Forces snapshot highlights supplier leverage, buyer pressure, substitution risk, entry barriers, and existing competitive rivalry to frame its market position and strategic vulnerabilities. This preview outlines key tensions but omits force-by-force ratings and visuals. The full Porter's Five Forces Analysis reveals detailed impacts, scenarios, and actionable recommendations. Unlock the complete report to inform investment or strategic decisions.

Suppliers Bargaining Power

Specialized building-tech components concentration

HVAC, electrical and control-system components are concentrated among a few OEMs, giving those suppliers leverage on price and lead times. Product compatibility requirements and warranty conditions often lock Consti into specific brands, reducing sourcing flexibility. This concentration raises the risk of project delays and margin pressure when supply tightens. Consti mitigates by qualifying multiple brands and using approved-equivalent specifications.

Subcontractor dependence in peak seasons

Renovation cycles and Nordic seasonality concentrate construction activity in Q2–Q3, increasing reliance on specialist subcontractors (facade, insulation, scaffolding) during peaks. Tight specialist capacity gives subcontractors leverage to seek higher rates or preferential scheduling. Strong quality and safety records limit substitutability. Framework agreements and preferred-partner programs are used to stabilize availability and cost.

Standards and certifications lift switching costs

Compliance with EU Construction Products Regulation 305/2011 and the 2018 EPBD recast (nZEB for new buildings from 2020) narrows Finland’s supplier pool and raises switching costs as new vendors often need approvals under Finnish building code (RakMK), retraining and added documentation; building automation software ecosystems add further lock-in while pre-approved vendor lists preserve compliance and limited optionality.

Framework agreements moderate pricing power

Framework agreements improve visibility and secure volume rebates (2024 procurement surveys report 3–7% typical rebates), aggregating demand across projects lowers spot exposure and tightens terms, though index-linked clauses can pass supplier inflation through to Consti; dual-sourcing within frameworks preserves leverage and mitigates single-supplier risk.

- Rebates: 3–7% (2024)

- Spot exposure: reduced via aggregation

- Inflation pass-through: index clauses risk

- Mitigation: dual-sourcing maintains leverage

Nordic logistics and input price volatility

Nordic weather, port congestion and seasonal transport constraints in 2024 led to intermittent delivery delays and higher freight premiums, increasing supplier leverage over Consti. Commodity volatility—steel and copper price swings and insulation material shortages—eroded margins on fixed-price projects, while EU carbon pricing near €100/t in 2024 raised low-carbon material costs. Early ordering and hedging reduced but did not eliminate input-cost exposure.

- 2024 EU carbon price ≈ €100/t

- Fixed-price margin pressure from commodity swings

- Weather and transport disruptions raise freight premiums

- Early ordering/hedging partially offsets volatility

Supplier power squeezes HVAC margins; frameworks cut spot risk and secure 3-7% rebates

Supplier power is high for OEM HVAC/electrical and niche subcontractors, driving price and lead-time pressure and raising switching costs via compatibility and compliance. Frameworks and dual-sourcing reduce spot exposure and secure 3–7% rebates (2024), but commodity swings and EU carbon near €100/t still squeeze fixed-price margins.

| Metric | 2024 value |

|---|---|

| Supplier rebates | 3–7% |

| EU carbon price | ≈€100/t |

| Spot exposure | Reduced via frameworks |

What is included in the product

Tailored Porter’s Five Forces analysis for Consti uncovering competitive drivers, supplier and buyer power, entry barriers, substitutes and disruptive threats, with strategic commentary to inform investor and management decisions.

Consti Porter's Five Forces delivers a clean one-sheet summary with customizable pressure levels and an instant spider chart—ready to copy into decks or integrate into Excel dashboards, no macros required.

Customers Bargaining Power

Tender-driven procurement pressures pricing

Public and institutional clients drive tender-driven procurement that prioritizes the lowest compliant bid; OECD data shows public procurement equals roughly 12% of GDP, concentrating buying power. Transparent evaluation criteria compress contractor margins—construction EBIT margins averaged about 4% in 2023–24—shifting risk to bidders. Design-build or alliance models can ease change-order risk but remain highly price-sensitive. Strong prequalification increases win odds without forcing below-cost bids.

Concentration of large public and institutional owners

Major municipalities, housing cooperatives and property funds exercise strong buying power, negotiating stringent warranties and service levels and using repeat procurement to press rates and payment terms; in 2024 their concentration in key urban markets amplified leverage, though deep supplier relationships and documented performance history materially mitigate price pressure.

Ability to split scopes and multi-source

Clients increasingly unbundle projects into lots (facade, MEP, automation), inviting multiple bidders and creating direct trade-level competition that reduces reliance on any single contractor. Multi-sourcing raises coordination and warranty risks for buyers while increasing their negotiating leverage on price and terms. To counter fragmentation, integrated providers must demonstrate clear lifecycle savings, lower total cost of ownership, and stronger risk transfer to retain scope.

Outcome-based specs and warranties shift risk

Timing flexibility amid demand cycles

Owners can defer non-critical renovations when markets are tight, allowing Consti to delay price competition; in 2024 industry reports showed renegotiation pressure rising as utilization dipped. In downturns buyers extract concessions while contractors chase utilization, though essential compliance work remains less deferrable and cushions margins. A balanced backlog (around EUR 160m reported in 2024) helps Consti avoid deep price troughs.

- Deferral leverage: owners delay non-critical work

- Buyer concessions: higher in downturns as utilization falls

- Compliance work: more price-inelastic, stabilizes revenue

- Backlog buffer: EUR 160m (2024) moderates price pressure

Public procurement ~12% GDP; EBIT ~4%; backlog EUR 160m

Customers (public + large owners) concentrate buying power—public procurement ~12% of GDP—forcing tender-led pricing; Consti’s peers saw construction EBIT ~4% in 2023–24. Retentions 5–10% and penalties 0.5–2% squeeze cash flow; unbundling increases bidder competition while backlog ~EUR 160m (2024) cushions downside.

| Metric | 2024 |

|---|---|

| Public procurement | ~12% GDP |

| EBIT (sector) | ~4% |

| Retention | 5–10% |

| Penalties | 0.5–2% |

| Consti backlog | EUR 160m |

Full Version Awaits

Consti Porter's Five Forces Analysis

This preview shows the exact Consti Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The document shown is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the final deliverable; purchase grants instant access to this identical file.