Consti PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Gain an edge with our PESTLE Analysis of Consti. Discover how political, economic, and technological forces shape its strategy and risk profile. Ideal for investors and strategists, it’s fully researched and editable. Buy the full report to get actionable, board-ready insights now.

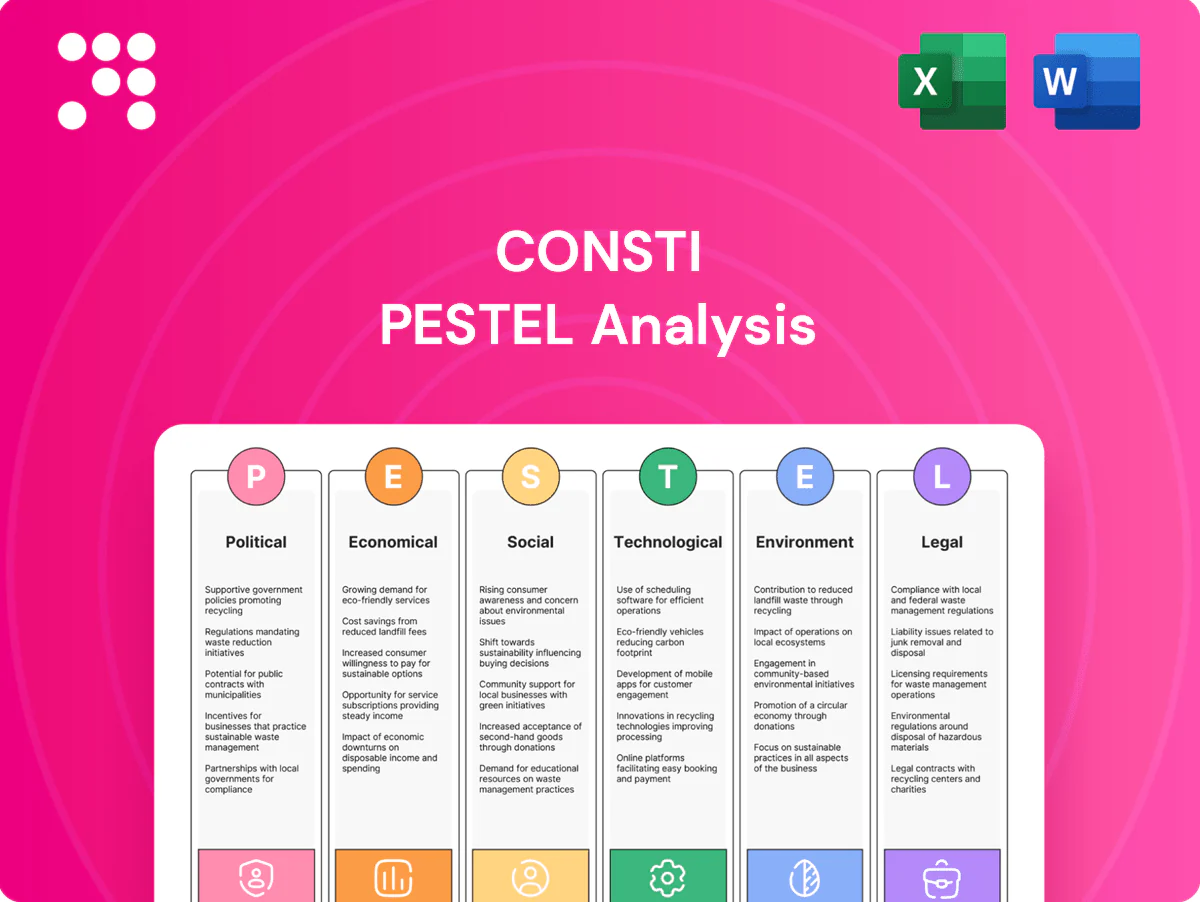

Political factors

EU Green Deal and Fit for 55

EU Green Deal and Fit for 55 push deep renovation—Fit for 55 targets a 55% EU GHG cut by 2030 and the Renovation Wave aims to at least double annual renovation rates by 2030. Buildings account for ~40% of EU energy use and ~36% of emissions, with the Commission estimating an extra €275bn/yr needed for renovations. This sustains Finnish public/private funding; Consti can align scopes to subsidy-eligible work but must deliver compliance proof and reporting to secure pipeline.

Finnish government renovation subsidies

State renovation subsidies in Finland, targeted at energy retrofits, accessibility and indoor air improvements, have expanded since the 2023 package supporting the national carbon neutrality goal for 2035 and directly boost project volumes. Funding levels and eligibility are set in annual budgets and coalition agreements, so Consti must monitor grant windows and criteria changes to time proposals. Reliance on subsidies leads to cyclical demand spikes when funding rounds open.

Public procurement priorities

Municipal and state tenders increasingly prioritize lifecycle cost, carbon reduction and indoor air quality, aligned with Finland’s national carbon neutrality target of 2035 and EU green procurement trends; public procurement represents about 14% of EU GDP. Weighted tender criteria now favor documented performance and ESG data, so Consti must supply strong references and verified measurement capabilities to score competitively. Protracted approval cycles for public projects can strain cash flow and require tighter working capital planning.

Housing company governance

Most Finnish apartment blocks are owned and managed as housing companies where board-led decisions and annual general meetings determine renovations; political emphasis on healthy schools and public buildings further shifts municipal and owner budgets toward indoor air and energy projects. Stakeholder consensus at housing company meetings can both delay and accelerate Consti projects, making clear communications, phased plans and transparent cost breakdowns critical to securing votes.

- ownership: housing companies govern most apartment blocks

- decision drivers: board + AGM votes

- policy push: healthy public buildings raise demand

- risk: stakeholder delays

- mitigation: phased plans + clear communications

Geopolitical energy security

Geopolitical energy security since Russia's 2022 gas cutoff (EU Russian gas imports fell about 80% in 2022, IEA) has accelerated Finland's drive for energy independence, boosting policy support for heat pumps, insulation and control upgrades and opening market opportunities for Consti to retrofit buildings and reduce district heating demand.

Consti can access public programs targeting district heating load reduction in a market where district heating supplies roughly 50% of residential heat, but must manage supply constraints and price volatility in materials and fuel.

- tags: energy_security, heat_pumps, district_heating

- IEA: EU Russian gas imports down ~80% in 2022

- Finland: district heating ≈50% residential heat

Renovation Wave drives subsidy-backed retrofits; procurement now favors lifecycle carbon and IAQ

EU Fit for 55/Renovation Wave (55% GHG cut by 2030; EC €275bn/yr gap) and Finland 2035 neutrality expand subsidy-backed retrofit pipeline; Consti must provide compliance, reporting and verified performance. Public procurement (~14% EU GDP) now favors lifecycle carbon and IAQ, lengthening award cycles and stressing working capital. Post-2022 gas cuts (~80%) and ~50% residential district heating boost heat-pump/insulation demand.

| Metric | Value |

|---|---|

| EU 2030 GHG target | 55% |

| Renovation funding gap | €275bn/yr |

| Public procurement | ~14% GDP |

| EU Russian gas drop (2022) | ~80% |

| Finland district heating | ~50% res. heat |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact Consti, combining data-driven trends and region-specific regulatory context; tailored for executives and investors, it provides forward-looking insights and ready-to-use findings for strategy, risk mitigation and funding decisions.

A concise, visually segmented Consti PESTLE summary that distills external risks and opportunities for quick decision-making, easily editable for local context and drop‑in ready for presentations or team alignment.

Economic factors

Interest rates and financing

Higher ECB policy rates around 4.0% (July 2025) push housing company and municipal borrowing costs up, often deferring non-urgent renovations while prioritizing projects with rapid energy-payback; Consti should foreground clear ROI metrics and performance guarantees to win constrained budgets. Even modest rate declines can quickly unlock backlogged renovation demand and accelerate tendering cycles.

Construction cycle softness

New-build softness has redirected capacity into renovation, with European renovation spending at roughly €320bn/year per EU Commission estimates, shifting competition and lifting pricing pressure. Improved labor availability has eased margins pressure while intensifying bids; Consti can capture share through operational efficiency and disciplined risk management. Counter-cyclical renovation demand—stronger in downturns—helps stabilize revenues and backlog visibility.

Material and labor costs

Volatile prices for insulation, electrical gear and metals—which swung roughly 10–25% in 2023–24—compress Consti margins; framework agreements and alternative specs mitigate these swings. Prefabrication and tighter planning boost productivity—McKinsey finds modular methods can cut costs ~20% and schedules 20–50%—offsetting wage inflation. Transparent cost-indexing in contracts improves client acceptance and pass-through of material inflation.

Aging building stock

Urban concentration

Urban concentration concentrates renovation activity in Greater Helsinki (≈1.6M residents in 2024), Tampere (≈500k) and Turku (≈350k) regions, driving higher permit volumes and demand for retrofit services; dense sites increase logistics costs and permit complexity, raising project overheads by an estimated double-digit percent versus rural sites.

- Proximity reduces travel time, improving responsiveness and cutting mobilization costs

- Local partnerships and frameworks boost utilization and speed of approvals

Renovation Wave drives subsidy-backed retrofits; procurement now favors lifecycle carbon and IAQ

ECB policy rate ~4.0% (July 2025) raises financing costs, delaying non‑urgent projects; small rate falls rapidly revive tenders. EU renovation market ≈€320bn/yr (EC), Renovation Wave target ≈2%/yr. Modular methods cut costs ~20% and schedules 20–50%; Greater Helsinki population ≈1.6M (2024) concentrates demand.

| Metric | Value |

|---|---|

| ECB rate (Jul 2025) | ~4.0% |

| EU reno spend | ≈€320bn/yr |

| Renovation target | ~2%/yr |

| Helsinki pop (2024) | ≈1.6M |

| Modular saving | ~20% |

Full Version Awaits

Consti PESTLE Analysis

The preview shown here is the exact Consti PESTLE document you’ll receive after purchase—fully formatted and ready to use. It contains comprehensive Political, Economic, Social, Technological, Legal and Environmental analysis tailored to Consti’s operating context, with clear headings and actionable insights. No placeholders or teasers—this is the real, finished file you’ll download immediately after payment.

Your Shortcut to Market Insight Starts Here

Gain an edge with our PESTLE Analysis of Consti. Discover how political, economic, and technological forces shape its strategy and risk profile. Ideal for investors and strategists, it’s fully researched and editable. Buy the full report to get actionable, board-ready insights now.

Political factors

EU Green Deal and Fit for 55

EU Green Deal and Fit for 55 push deep renovation—Fit for 55 targets a 55% EU GHG cut by 2030 and the Renovation Wave aims to at least double annual renovation rates by 2030. Buildings account for ~40% of EU energy use and ~36% of emissions, with the Commission estimating an extra €275bn/yr needed for renovations. This sustains Finnish public/private funding; Consti can align scopes to subsidy-eligible work but must deliver compliance proof and reporting to secure pipeline.

Finnish government renovation subsidies

State renovation subsidies in Finland, targeted at energy retrofits, accessibility and indoor air improvements, have expanded since the 2023 package supporting the national carbon neutrality goal for 2035 and directly boost project volumes. Funding levels and eligibility are set in annual budgets and coalition agreements, so Consti must monitor grant windows and criteria changes to time proposals. Reliance on subsidies leads to cyclical demand spikes when funding rounds open.

Public procurement priorities

Municipal and state tenders increasingly prioritize lifecycle cost, carbon reduction and indoor air quality, aligned with Finland’s national carbon neutrality target of 2035 and EU green procurement trends; public procurement represents about 14% of EU GDP. Weighted tender criteria now favor documented performance and ESG data, so Consti must supply strong references and verified measurement capabilities to score competitively. Protracted approval cycles for public projects can strain cash flow and require tighter working capital planning.

Housing company governance

Most Finnish apartment blocks are owned and managed as housing companies where board-led decisions and annual general meetings determine renovations; political emphasis on healthy schools and public buildings further shifts municipal and owner budgets toward indoor air and energy projects. Stakeholder consensus at housing company meetings can both delay and accelerate Consti projects, making clear communications, phased plans and transparent cost breakdowns critical to securing votes.

- ownership: housing companies govern most apartment blocks

- decision drivers: board + AGM votes

- policy push: healthy public buildings raise demand

- risk: stakeholder delays

- mitigation: phased plans + clear communications

Geopolitical energy security

Geopolitical energy security since Russia's 2022 gas cutoff (EU Russian gas imports fell about 80% in 2022, IEA) has accelerated Finland's drive for energy independence, boosting policy support for heat pumps, insulation and control upgrades and opening market opportunities for Consti to retrofit buildings and reduce district heating demand.

Consti can access public programs targeting district heating load reduction in a market where district heating supplies roughly 50% of residential heat, but must manage supply constraints and price volatility in materials and fuel.

- tags: energy_security, heat_pumps, district_heating

- IEA: EU Russian gas imports down ~80% in 2022

- Finland: district heating ≈50% residential heat

Renovation Wave drives subsidy-backed retrofits; procurement now favors lifecycle carbon and IAQ

EU Fit for 55/Renovation Wave (55% GHG cut by 2030; EC €275bn/yr gap) and Finland 2035 neutrality expand subsidy-backed retrofit pipeline; Consti must provide compliance, reporting and verified performance. Public procurement (~14% EU GDP) now favors lifecycle carbon and IAQ, lengthening award cycles and stressing working capital. Post-2022 gas cuts (~80%) and ~50% residential district heating boost heat-pump/insulation demand.

| Metric | Value |

|---|---|

| EU 2030 GHG target | 55% |

| Renovation funding gap | €275bn/yr |

| Public procurement | ~14% GDP |

| EU Russian gas drop (2022) | ~80% |

| Finland district heating | ~50% res. heat |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact Consti, combining data-driven trends and region-specific regulatory context; tailored for executives and investors, it provides forward-looking insights and ready-to-use findings for strategy, risk mitigation and funding decisions.

A concise, visually segmented Consti PESTLE summary that distills external risks and opportunities for quick decision-making, easily editable for local context and drop‑in ready for presentations or team alignment.

Economic factors

Interest rates and financing

Higher ECB policy rates around 4.0% (July 2025) push housing company and municipal borrowing costs up, often deferring non-urgent renovations while prioritizing projects with rapid energy-payback; Consti should foreground clear ROI metrics and performance guarantees to win constrained budgets. Even modest rate declines can quickly unlock backlogged renovation demand and accelerate tendering cycles.

Construction cycle softness

New-build softness has redirected capacity into renovation, with European renovation spending at roughly €320bn/year per EU Commission estimates, shifting competition and lifting pricing pressure. Improved labor availability has eased margins pressure while intensifying bids; Consti can capture share through operational efficiency and disciplined risk management. Counter-cyclical renovation demand—stronger in downturns—helps stabilize revenues and backlog visibility.

Material and labor costs

Volatile prices for insulation, electrical gear and metals—which swung roughly 10–25% in 2023–24—compress Consti margins; framework agreements and alternative specs mitigate these swings. Prefabrication and tighter planning boost productivity—McKinsey finds modular methods can cut costs ~20% and schedules 20–50%—offsetting wage inflation. Transparent cost-indexing in contracts improves client acceptance and pass-through of material inflation.

Aging building stock

Urban concentration

Urban concentration concentrates renovation activity in Greater Helsinki (≈1.6M residents in 2024), Tampere (≈500k) and Turku (≈350k) regions, driving higher permit volumes and demand for retrofit services; dense sites increase logistics costs and permit complexity, raising project overheads by an estimated double-digit percent versus rural sites.

- Proximity reduces travel time, improving responsiveness and cutting mobilization costs

- Local partnerships and frameworks boost utilization and speed of approvals

Renovation Wave drives subsidy-backed retrofits; procurement now favors lifecycle carbon and IAQ

ECB policy rate ~4.0% (July 2025) raises financing costs, delaying non‑urgent projects; small rate falls rapidly revive tenders. EU renovation market ≈€320bn/yr (EC), Renovation Wave target ≈2%/yr. Modular methods cut costs ~20% and schedules 20–50%; Greater Helsinki population ≈1.6M (2024) concentrates demand.

| Metric | Value |

|---|---|

| ECB rate (Jul 2025) | ~4.0% |

| EU reno spend | ≈€320bn/yr |

| Renovation target | ~2%/yr |

| Helsinki pop (2024) | ≈1.6M |

| Modular saving | ~20% |

Full Version Awaits

Consti PESTLE Analysis

The preview shown here is the exact Consti PESTLE document you’ll receive after purchase—fully formatted and ready to use. It contains comprehensive Political, Economic, Social, Technological, Legal and Environmental analysis tailored to Consti’s operating context, with clear headings and actionable insights. No placeholders or teasers—this is the real, finished file you’ll download immediately after payment.

Original: $10.00

-65%$10.00

$3.50Description

Your Shortcut to Market Insight Starts Here

Gain an edge with our PESTLE Analysis of Consti. Discover how political, economic, and technological forces shape its strategy and risk profile. Ideal for investors and strategists, it’s fully researched and editable. Buy the full report to get actionable, board-ready insights now.

Political factors

EU Green Deal and Fit for 55

EU Green Deal and Fit for 55 push deep renovation—Fit for 55 targets a 55% EU GHG cut by 2030 and the Renovation Wave aims to at least double annual renovation rates by 2030. Buildings account for ~40% of EU energy use and ~36% of emissions, with the Commission estimating an extra €275bn/yr needed for renovations. This sustains Finnish public/private funding; Consti can align scopes to subsidy-eligible work but must deliver compliance proof and reporting to secure pipeline.

Finnish government renovation subsidies

State renovation subsidies in Finland, targeted at energy retrofits, accessibility and indoor air improvements, have expanded since the 2023 package supporting the national carbon neutrality goal for 2035 and directly boost project volumes. Funding levels and eligibility are set in annual budgets and coalition agreements, so Consti must monitor grant windows and criteria changes to time proposals. Reliance on subsidies leads to cyclical demand spikes when funding rounds open.

Public procurement priorities

Municipal and state tenders increasingly prioritize lifecycle cost, carbon reduction and indoor air quality, aligned with Finland’s national carbon neutrality target of 2035 and EU green procurement trends; public procurement represents about 14% of EU GDP. Weighted tender criteria now favor documented performance and ESG data, so Consti must supply strong references and verified measurement capabilities to score competitively. Protracted approval cycles for public projects can strain cash flow and require tighter working capital planning.

Housing company governance

Most Finnish apartment blocks are owned and managed as housing companies where board-led decisions and annual general meetings determine renovations; political emphasis on healthy schools and public buildings further shifts municipal and owner budgets toward indoor air and energy projects. Stakeholder consensus at housing company meetings can both delay and accelerate Consti projects, making clear communications, phased plans and transparent cost breakdowns critical to securing votes.

- ownership: housing companies govern most apartment blocks

- decision drivers: board + AGM votes

- policy push: healthy public buildings raise demand

- risk: stakeholder delays

- mitigation: phased plans + clear communications

Geopolitical energy security

Geopolitical energy security since Russia's 2022 gas cutoff (EU Russian gas imports fell about 80% in 2022, IEA) has accelerated Finland's drive for energy independence, boosting policy support for heat pumps, insulation and control upgrades and opening market opportunities for Consti to retrofit buildings and reduce district heating demand.

Consti can access public programs targeting district heating load reduction in a market where district heating supplies roughly 50% of residential heat, but must manage supply constraints and price volatility in materials and fuel.

- tags: energy_security, heat_pumps, district_heating

- IEA: EU Russian gas imports down ~80% in 2022

- Finland: district heating ≈50% residential heat

Renovation Wave drives subsidy-backed retrofits; procurement now favors lifecycle carbon and IAQ

EU Fit for 55/Renovation Wave (55% GHG cut by 2030; EC €275bn/yr gap) and Finland 2035 neutrality expand subsidy-backed retrofit pipeline; Consti must provide compliance, reporting and verified performance. Public procurement (~14% EU GDP) now favors lifecycle carbon and IAQ, lengthening award cycles and stressing working capital. Post-2022 gas cuts (~80%) and ~50% residential district heating boost heat-pump/insulation demand.

| Metric | Value |

|---|---|

| EU 2030 GHG target | 55% |

| Renovation funding gap | €275bn/yr |

| Public procurement | ~14% GDP |

| EU Russian gas drop (2022) | ~80% |

| Finland district heating | ~50% res. heat |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact Consti, combining data-driven trends and region-specific regulatory context; tailored for executives and investors, it provides forward-looking insights and ready-to-use findings for strategy, risk mitigation and funding decisions.

A concise, visually segmented Consti PESTLE summary that distills external risks and opportunities for quick decision-making, easily editable for local context and drop‑in ready for presentations or team alignment.

Economic factors

Interest rates and financing

Higher ECB policy rates around 4.0% (July 2025) push housing company and municipal borrowing costs up, often deferring non-urgent renovations while prioritizing projects with rapid energy-payback; Consti should foreground clear ROI metrics and performance guarantees to win constrained budgets. Even modest rate declines can quickly unlock backlogged renovation demand and accelerate tendering cycles.

Construction cycle softness

New-build softness has redirected capacity into renovation, with European renovation spending at roughly €320bn/year per EU Commission estimates, shifting competition and lifting pricing pressure. Improved labor availability has eased margins pressure while intensifying bids; Consti can capture share through operational efficiency and disciplined risk management. Counter-cyclical renovation demand—stronger in downturns—helps stabilize revenues and backlog visibility.

Material and labor costs

Volatile prices for insulation, electrical gear and metals—which swung roughly 10–25% in 2023–24—compress Consti margins; framework agreements and alternative specs mitigate these swings. Prefabrication and tighter planning boost productivity—McKinsey finds modular methods can cut costs ~20% and schedules 20–50%—offsetting wage inflation. Transparent cost-indexing in contracts improves client acceptance and pass-through of material inflation.

Aging building stock

Urban concentration

Urban concentration concentrates renovation activity in Greater Helsinki (≈1.6M residents in 2024), Tampere (≈500k) and Turku (≈350k) regions, driving higher permit volumes and demand for retrofit services; dense sites increase logistics costs and permit complexity, raising project overheads by an estimated double-digit percent versus rural sites.

- Proximity reduces travel time, improving responsiveness and cutting mobilization costs

- Local partnerships and frameworks boost utilization and speed of approvals

Renovation Wave drives subsidy-backed retrofits; procurement now favors lifecycle carbon and IAQ

ECB policy rate ~4.0% (July 2025) raises financing costs, delaying non‑urgent projects; small rate falls rapidly revive tenders. EU renovation market ≈€320bn/yr (EC), Renovation Wave target ≈2%/yr. Modular methods cut costs ~20% and schedules 20–50%; Greater Helsinki population ≈1.6M (2024) concentrates demand.

| Metric | Value |

|---|---|

| ECB rate (Jul 2025) | ~4.0% |

| EU reno spend | ≈€320bn/yr |

| Renovation target | ~2%/yr |

| Helsinki pop (2024) | ≈1.6M |

| Modular saving | ~20% |

Full Version Awaits

Consti PESTLE Analysis

The preview shown here is the exact Consti PESTLE document you’ll receive after purchase—fully formatted and ready to use. It contains comprehensive Political, Economic, Social, Technological, Legal and Environmental analysis tailored to Consti’s operating context, with clear headings and actionable insights. No placeholders or teasers—this is the real, finished file you’ll download immediately after payment.